Not by me, but by Jeffrey A. Tucker, today:

In 2024, Brownstone Institute commissioned a study (by E.J. Antoni and Peter St. Onge) that concluded that we have never really entered recovery after 2022. We’ve been in a technical recession since that time. They got this with some limited adjustments of price data bumped up against output data. That study was met with brutal attacks, with every critic falling back on official data and doubting the supposed extremism of the conclusion.

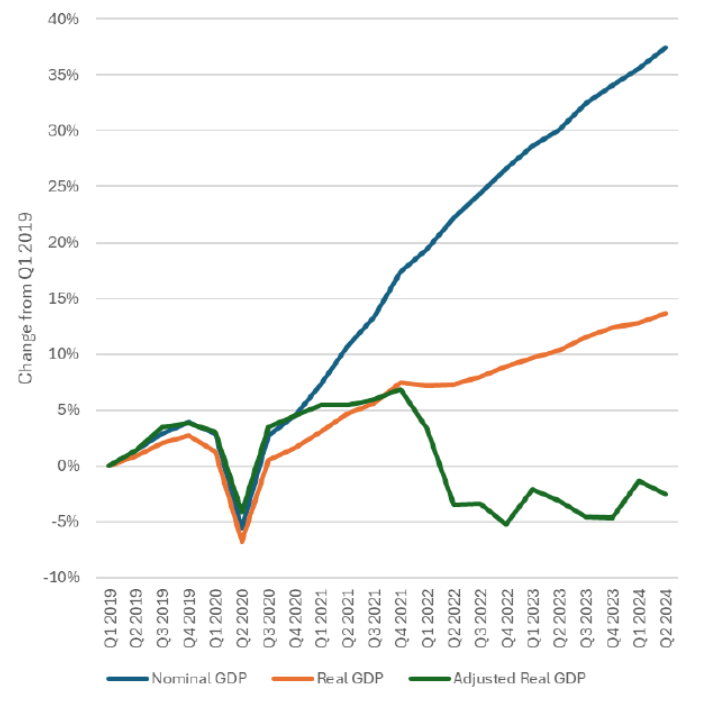

To remind people, here is the relevant graph from that paper.

Source: Antoni and St. Onge (2024).

For those who are interested, in this paper, I document the impossibility of replicating their results, without an explanation of how they constructed their alternative deflator.

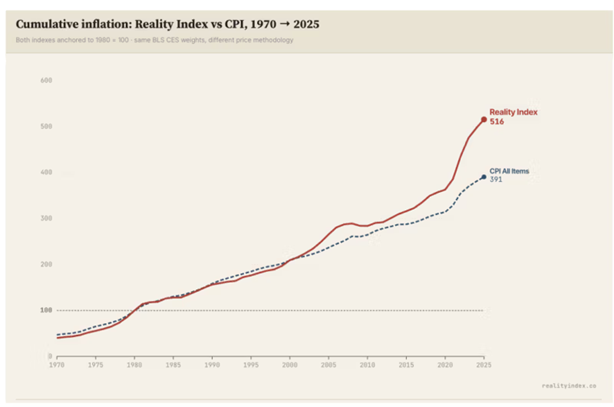

Now, I think I understand how Antoni and St. Onge (2024) obtained their results. It’s hinted at in reference to a “Reality Index”, credited to “independent intellectual Tom Elliott“.

The Reality Index v1 tracks the retail price of fifteen specific items in five categories: food, energy, housing, health care, and services. Each item is selected on three criteria: (a) the item is a fixed-specification good or service that households actually purchase, (b) an authoritative retail-price time series exists for it going back at least to 1980, and (c) the item is non-discretionary, in the sense that the typical household consumes some amount of it whether or not its price has risen.

There are several key distinctions from the CPI, including using fixed weights (i.e., Laspeyres price index), no hedonic adjustments, different treatment of housing. (While it’s true that CPI used to be characterized as Laspeyres, over time the treatment has changed so it approaches the chained measure).

Here’s the relevant comparison:

Source: Tucker (2026).

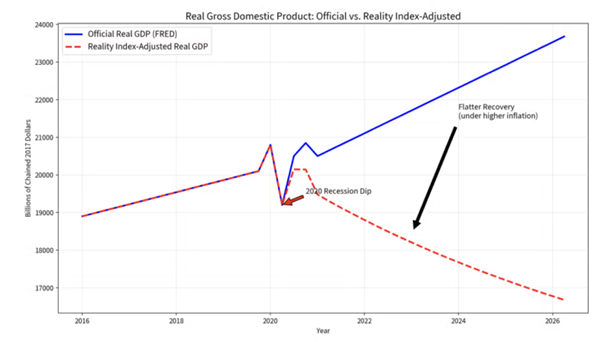

I’ve got no beef with anybody analyzing data, making up their own indices (as long as properly documented, and data posted for replication). However, Tucker then conducts this interesting exercise.

Source: Tucker (2026).

I can say two things with perfect certitude: (1) the above graph, labeling “Official Real GDP (FRED) is definitively NOT official real GDP from FRED — it’s much too straight. (2) It makes no sense to deflate nominal GDP with a deflator for consumption, unless prices rose at the same rate for firms (investment), government (government spending on tanks and civil servants) and exports (purchases of American goods and services imported by other countries).

From this, I can only conclude that in the original Antoni-St. Onge paper obtained their bizarre result by deflating GDP using their (undocumented, unreproducible) consumer price deflator.

All I can say is that if we were in recession in 2022, 2023 and 2024 — can we have more of it, please?

I think the reason job growth prior to 2025 looks so much better than now is because we’re using the wrong inflation index for jobs.

They’ve got that excuse covered. Both Hassett and Navarro have said: “All of the job growth under Biden was illegal immigrants and the Job growth number is lower under Trump because of mass deportations.”

Huh? I thought that one of the major reasons for deportations was to free up jobs for native born Americans. But under Trump, deportations reduced the total number of jobs, and ironically the native born unemployment rate increased.

Turns out that immigration increases the number of jobs and reduces the native born unemployment rate, Yep, those numbers must be wrong because of the wrong job inflation index.

Mr. Tucker is a polemicist, and a polemicist of a particular kind. He has worked for Lew Rockwell and Ron Paul, and is a bitcoin huckster. He campaigned against public health efforts against Covid, based on his libertarian view of how the world should run.

Tucker’s op-ed at the Eurasia Review (not to be confused with the Eurasia Group, though I suspect confusion is the intent) is a sort of a kitchen-sink effort – any bad thing he can find in recent headlines comes in for mention, even though most of it is irrelevant to his argument. Tucker simply assumes the little Antoni’s pick-your-deflator exercise is valid and goes from there.

So, the idea is that we deflate the nominal prices of every good and service in the U.S. economy by the price fluctuations of 15 items? I’m pretty sure I could pick out five items and create an index which would show prices falling since 2020. Very sure.

We deflate using appropriate deflators because to do otherwise is idiocy. No wonder little Antoni didn’t publish the data he uses to tell his cockamamie tale.

ADP reports the best private-sector hiring in some time, 122,000 net new jobs, after a gain of 105,000 in April. Firms of all sizes added jobs. Only information and natural resources shed jobs:

https://adpemploymentreport.com/

Small-firm paycheck processors Gusto and Paychex also report health hiring:

https://www.marketplace.org/story/2026/06/03/why-many-small-business-are-hiring-right-now

Part of this story is apparently that smaller firms which have wanted to hire – especially computing specialists of various kinds – can now find them because of layoffs at bigger firms. That doesn’t jibe with the net decline in information jobs, but whatever.