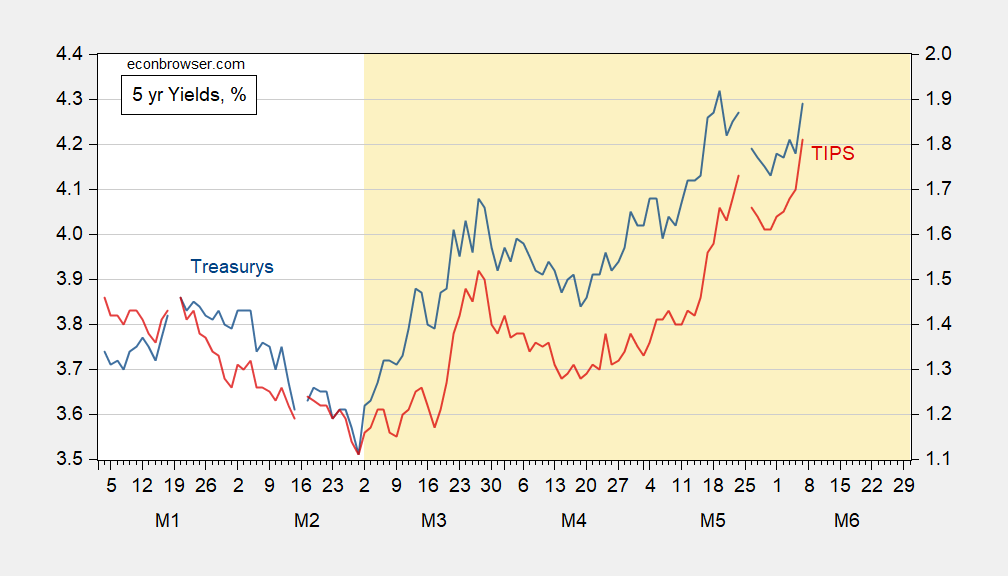

Big jumps in yields; as shown at the five year maturity, the move is evident in both nominal and real yields:

Figure 1: Treasury 5 year yield (blue, left scale), TIPS 5 year yield (red, right scale), both in %. Source: Treasury via FRED.

What is notable is that this is not a recent peak in the nominal yield, but it is in the real yield. This suggests not upward revision primarily in inflation expectations, but rather in real yields (higher economic activity leads to greater demand for credit). It could be that term premia in real and nominal rates could be obscuring the inflation component. However, inspection of the D’Amico, Kim, and Wei (DKW) measures of 5 and 10 year expected inflation suggests that the 5/29 rate is the same as that for 2/27, the day before the war’s start.

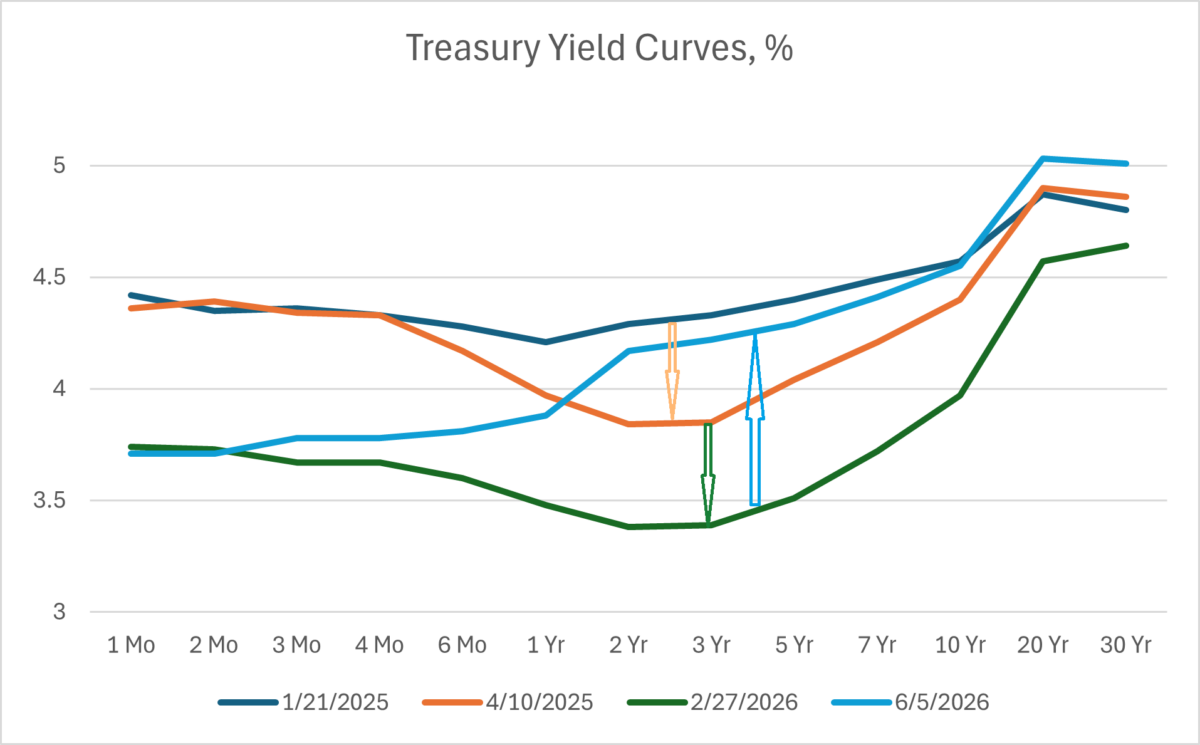

Another way to look at matters is to examine the yield curve. There is no inversion remaining in today’s curve, as compared to just before the war.

Figure 2: Yield curve for US Treasurys as of 1/21/2025 (blue), as of 4/10/2025 (tan), as of 2/27/2026 (green), and as of 6/5/2026 (sky blue), all in %. Source: Treasury.

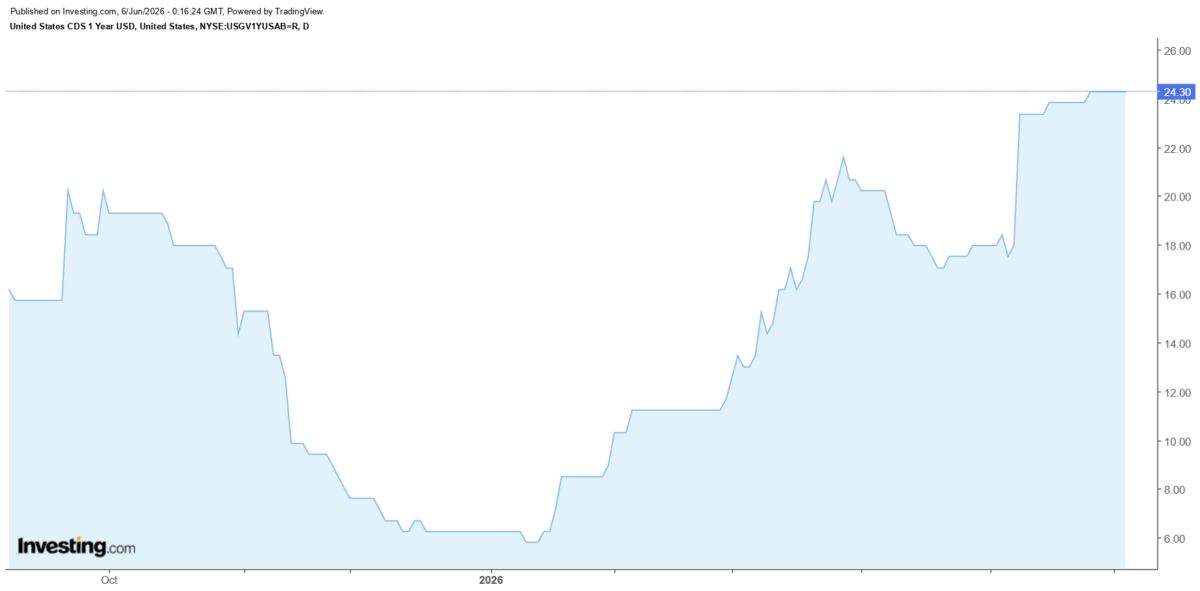

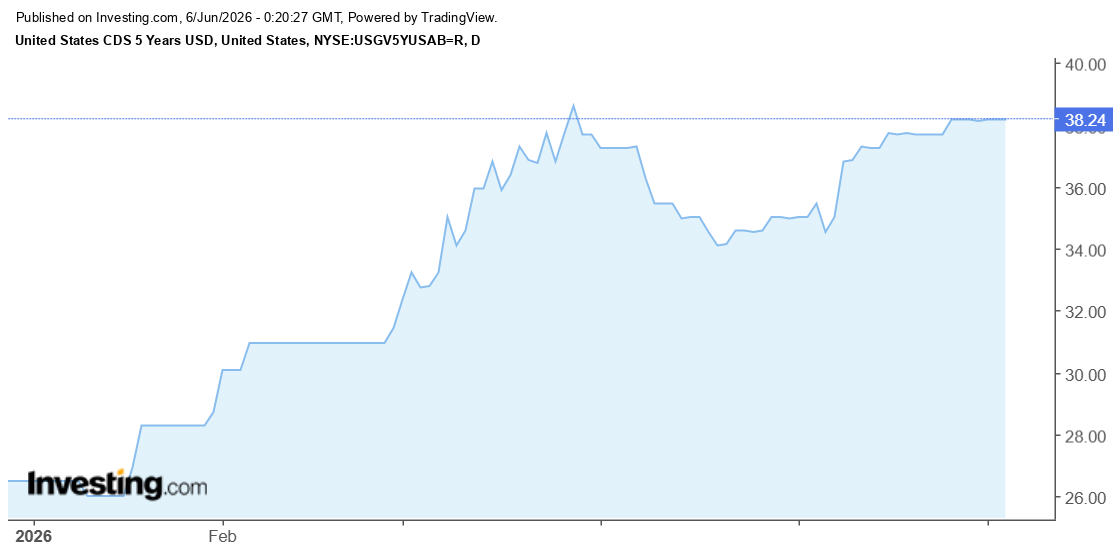

The rise in the long yield could also be attributable to default risk, but this remains pretty small, as far CDS’s are concerned.

The 5 yr CDS rate implies a 0.64% default probability assuming a 40% recovery rate.

“This suggests not upward revision primarily in inflation expectations, but rather in real yields (higher economic activity leads to greater demand for credit). It could be that term premia in real and nominal rates could be obscuring the inflation component.”

Increased economic activity means higher demand for credit. The greatest increase in credit demand these days is from government and AI server farms – Keynesianism gone wild and speculative capital investment. Another explanation for higher real rates would be a cooling in the supply of credit. We can see that happening in the decision by private credit funds to limit withdrawals. There are also a hell of a lot fewer petrodollars right now than before the war. I don’t have numbers, but I imagine the decline in dollar-denominated oil trade is a larger decrement that, say, any decline in appetite for dollar reserves. If my petrodollar speculation is correct, then the Iran war is raising rates through another channel than just the inflation premium.

Oh, and uncertainty about future inflation and future monetary policy would show up in term premium. Again, ’cause of the Iran war.