That’s a title from an oped by former GW Bush speechwriter and current AEI scholar Marc Thiessen nearly a year ago. We can now evaluate whether in fact the implementation of individual insurance mandate component of the ACA did implode. From “New Data Show Early Progress in Expanding Coverage, with More Gains to Come,” White House blog today:

From the post:

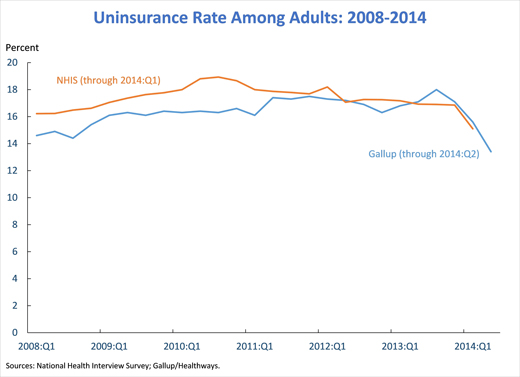

…today’s results from the NCHS’ National Health Interview Survey (NHIS) show that the share of Americans without health insurance averaged 13.1 percent over the first quarter of 2014, down from an average of 14.4 percent during 2013, a reduction corresponding to approximately 4 million people. The 13.1 percent uninsurance rate recorded for the first quarter of 2014 is lower than any annual uninsurance rate recorded by the NHIS since it began using its current design in 1997.

As striking as this reduction is, it dramatically understates the actual gains in insurance coverage so far in 2014. The interviews reflected in today’s results were spread evenly over January, February, and March 2014. As a result, the vast majority of the survey interviews occurred before the surge in Marketplace plan selections that occurred in March; 3.8 million people selected a Marketplace plan after March 1,with many in the last week before the end of open enrollment on March 31. Similarly, these results only partially capture the steady increase in Medicaid enrollment during the first quarter.

For this reason, private surveys from the Urban Institute, Gallup/Healthways, and the Commonwealth Fund in which interviews occurred entirely after the end of open enrollment have consistently shown much larger gains in insurance coverage. An analysis published last month in the New England Journal of Medicine based on the Gallup/Healthways data estimated that coverage gains reached 10.3 million by the middle of 2014.

Some points that will surely annoy some commentators, particularly those who bewailed the early low rates of enrollment of young adults:

- Increases in coverage were concentrated among non-elderly adults, with the youngest adults seeing the largest gains: Insurance coverage increased among non-elderly adults increased by 2.0 percentage points from 2013 through the first quarter of 2014, while insurance coverage was essentially unchanged for children and individuals over the age of 65. This pattern reflects the fact that children and older adults had much greater access to insurance coverage prior to reform.Young adults ages 18-24 saw their uninsurance rate drop by 5.5 percentage points from 2013 to the first quarter of 2014, a much larger decline than seen by other groups.

The gains in this report are on top of very large coverage gains among young adults from 2010 through 2013, gains that are largely attributable to a provision of the Affordable Care Act that permits young adults to remain on their parents’ insurance policies until they turn 26. From 2010 through the first quarter of 2014, the insurance rate among young adults ages 19-25 (the full group affected by this earlier Affordable Care Act provision) has increased by a total of 13 percentage points.

- Blacks and Latinos saw particularly large increases in coverage: Insurance coverage among non-Hispanic blacks increased by 3.8 percentage points from 2013 to the first quarter of 2014, while coverage among Latinos increased by 3.1 percentage points. Both increases were considerably larger than 1.3 percentage point increase in the full population.

Had states like Wisconsin expanded Medicare coverage, the uninsured rate would have declined further.

Returning to Marc Thiessen’s prognostications:

President Obama may have no choice but to delay the individual mandate. As my American Enterprise Institute colleague, Dr. Scott Gottlieb, points out, how can Obama penalize people for not having health insurance if the government’s Web site to provide that insurance doesn’t work?

Without the individual mandate, Obamacare unravels. The only way the law works is if the government forces young, healthy people into it by threatening them with penalties for not carrying health insurance. But if there is no penalty for not signing up, then fewer Americans will sign up.

Even if the administration manages to fix the Web site and finally implement the individual mandate, people still may not join — because the plans being offered are so unattractive. To entice people to join the exchanges, the administration forced insurers to offer low monthly premiums and cover people with preexisting conditions. Insurers have responded by increasing deductibles — the out-of-pocket costs people must pay before insurance benefits kick in — to stratospheric levels.

There must be a special place where people who predict hyperinflation in response to quantitative/credit easing, gold prices always going upward, and the collapse of ACA go to commiserate and convince themselves they are actually right.

Running List of Predictions and Predictors of ACA Collapse (send me your suggestions, so we can be as comprehensive as possible, and induce a little humility into these folks!)

Menzie,

Did I miss it? Where are your predictions?

There must be a special place for those who never predict anything but only criticize others who do.

“There must be a special place where people who predict hyperinflation in response to quantitative/credit easing, gold prices always going upward, and the collapse of ACA go to commiserate and convince themselves they are actually right.”

And that place is the Republican party.

But there is more. How can you do a graph when the numbers are virtually meaningless. Obamacare has been changing almost daiy since it was passed. The criteria for subsidies are continually changing. The White House continues to insist that they can’t provide numbers of how many have enrolled. it seems that daily we are told that hundreds of thousands either have or may lose their coverage. And the business mandate has not even been instituted. No one knows how many will lose their jobs when businesses have to force their employees onto Obamacare because the rules have not even been written. Will this be implemented in January 2015 or will it once again be postponed? There is not election in 2015 so there is a good chance that it will be implemented but how many waivers will be granted since we will be entering the beginning of the presidential election. Speaking of foolish, trying to do any statistical analysis of health care enrollment numbers is beyond foolish.

ricardo, you continue to look like a fool with your obamacare “the sky is falling” arguments. just face the facts, obamacare is working and you were wrong about its future performance. doubling down on a bad bet is plain stupid.

Ricardo, the very source that you link to says that almost a half million could lose their insurance –115,000 plus 363000— but 8 million have gained coverage.

In my book that is a gain of over 7.5 million people with insurance coverage.

What is it in you book to reach the conclusion that Obama-care has failed?

Ricardo Did you even read your link? Or did you just latch onto something that sorta, kinda sounded like it might be pitch against Obamacare. Try reading it and then ask yourself if it supports your claim that Obamacare is a train wreck in the making.

But since you oppose Obamacare so strongly, let me ask you if you would support universal coverage of the kind that you get….you know…single-payer Medicare. Or is it a case of something being almost good enough for Ricardo but too good for anyone else?

BTW and since Menzie brought it up, how have those gold investments done over the last 6 months?

Perhaps this is an occasion to revisit this stupendous blooper courtesy of Steve Kopits: “So it costs us $140 bn per year to insure an incremental 3 million people. Only $35,000 per head. What a bargain!”

https://econbrowser.com/archives/2014/04/aca-insurance-coverage-cost-update-from-cbo#comment-181240

This is a blunder so big it actually took two numerically challenged conservatives working in tandem to gin up — Steve Kopits who misread a simple line graph to come up with the wrong denominator and Rick Stryker who failed elementary multiplication in coming up with the wrong numerator.

Getting health care insurance is not the same as getting health care.

What if someone buys health care insurance and wants to use it, and then discovers, with millions of new users, doctors aren’t accepting new patients or there’s a long waiting list?

They wouldn’t be too happy, would they?

Particularly, since they fell behind on their bills, or stopped going to the Sizzler and Starbucks, because they had to buy health care insurance.

PwK Trader — how many angels can dance on the tip of a pin?

How about something approaching reality in your arguments– not made-up examples.

Spencer, not as many angels as you think.

Doctors Say Obamacare Rule Will Stick Them With Unpaid Bills

March 19, 2014

NPR

“Doctors worry they won’t get paid by some patients because of an unusual 90-day grace period for government-subsidized health plans.

So several professional groups for doctors are urging their members to check patients’ insurance status before every visit.

Consumer advocates say these checks could lead to treatment delays or denials for some patients.”

****

Government went in the wrong direction with Obamacare. Here’s what the son of a MD said:

“Dad worked 80 hours a week on average, including three weekends a month on call. Few breaks for holidays. We rarely saw him during the week. Divide $250k a year (just guessing – he wasn’t one to talk about money) into 4,000 hours a year and you get about 60 bucks an hour.

Out of that salary:

– 25% or more went to taxes

– $70-80k a year for malpractice insurance to protect his family and practice from all the worthless patient lawsuits by crooked lawyers.

– Salary for his administrative staff to process and follow up on reams of insurance and government paperwork.

– Costs of OSHA and other compliance overhead to run his clinic and x-ray machine.

I’m not saying we didn’t live comfortably. He took good care of us. Rather than credit his salary, I’d say God blessed him for all the pro-bono work he did for patients that couldn’t afford care but still took up his time. And trips to Africa on his own dime for medical missions.

I don’t know if these MD’s in other countries are as over-lawyered and over-regulated as US doctors are.”

My comment: Some potential MDs may find microbiology or biochemistry much better.

peak,

malpractice insurance would be significantly reduced if the medical field would actually purge the bad doctors-but they do not. the vast majority of malpractice suits are related to a small, select few doctors, many repeat offenders. but the AMA takes no action against them. hence they exist in the doctor population, and their risk is spread to the rest of the medical field.

OSHA compliance is meant to keep workers safe from bosses cutting safety corners. how would you like to work at an xray machine 8 hours a day without radiation protection because the boss wanted to save a few dollars? maybe skip on safety glasses and fume hoods?

“Some potential MDs may find microbiology or biochemistry much better.”

salary is MUCH lower, but i guess that is their choice. then again, it sounds like somebody feels entitled to make $250k without sacrifices! you know how many people would jump at the chance to earn $250k a year, even if it meant working 80 hours a week? the rest is the cost of doing business. a doctor could always work as a hospital internist, at lower salary but also shorter hours.

Malpractice insurance needed because of all the frivolous lawsuits perpetrated by trial attorneys.

I live in Florida, and daily there are 20-30 ads by trial attorneys wanting to gig companies for everything from A to Z. It’s immoral.

Now they are running ads to put people on SSI. SSI has doubled since the Bummer was president. It’s worse than welfare, food stamps, etc. When will the dependency stop.

Spencer is the type of guy who would run down the street waving a piece of paper happily saying:

“I have health care insurance! – I have health care insurance! – thanks Obama – thanks Obama!”

Then, when he gets to the doctor’s office, there’s a sign that says:

“Closed – Out of business (Gone into microbiology).”

He goes to the doctor next door and sees a line – out the building, down the street, and around the corner.

Nancy Pelosi pulls-up in her limo and goes into the building to see the doctor upstairs, who doesn’t accept Obamacare, right away.

PeakTrader: “What if someone buys health care insurance and wants to use it, and then discovers, with millions of new users, doctors aren’t accepting new patients or there’s a long waiting list?”

And what if pigs could fly, since we are imagining pure hypotheticals. Let’s just assume your hypothetical were true, hypothetically of course, then you are saying you preferred the previous system in which other people, primarily poor people, are prevented from going to the doctor so that your own wait times are shorter. Conservatives say they are opposed to healthcare rationing — Palin’s death panels and all that — yet seem to favor the most brutal, senseless kind of rationing.

Joseph, I was imagining supply & demand.

How do you know people won’t be more likely to use health care, since they bought health care insurance? (are people more likely to see a dentist if they have dental insurance?).

And, where will the doctors come from? – The VA system?

Maybe, you want a health care system similar to the public school system. With the Bronze Plan you can go to an inner city doctor in Chicago 🙂

“Maybe, you want a health care system similar to the public school system. With the Bronze Plan you can go to an inner city doctor in Chicago ”

Whoops. That’s the tell. You want to share doctors with THOSE people in the INNER CITY!?!

“Whoops. That’s the tell.” Ignore quality and focus on race.

Why not ignore race and focus on quality instead?

Has playing “mom” with “THOSE people” really worked out well?

I don’t mind sharing doctors with “THOSE people.”

I do mind the quality difference between a PPO and a HMO, for example.

Peak trader: it’s september. If there was going to be a huge supply-demand imbalance we should be seeing signs of it.

Which is not to say that we shouldn’t break up the doctor’s guild that prevents nurse practicioners from handling many routine health-care tasks and that acts to restrict immigration of doctors.

But it is to say that you can speculate until the cows come home but to demonstrate an imbalance, you need to show us actual data.

Professor Chinn, why would you use such a discredited website, as Obama.com

to provide honest and factual data?

Have our intellectuals so debase themselves from reality.

Gov Walker cannot do anything right, but CommieCare is a magic bullet.

Commiecare? Do you even understand how the law works?

Hans: Thank you for your — as usual — tightly reasoned and carefully documented comment.

You can cross-check the figures; here is CDC’s numbers. Gallup’s figures for Q2 are here.

By the way, you will notice that when I comment on progress in Wisconsin, I cite figures from the Department of Workforce Development (DWD), headed by a Walker appointee, or Legislative Fiscal Bureau (both chambers are controlled by Republicans). That’s because the statistical agencies and the LFB are run by technocrats. To my knowledge this is true also of the CDC and Census Bureau. Do you think there is a conspiracy so vast that the government controls Gallup? If so, please provide documentation, and while you’re at it, also tell me where you think the black helicopters will be landing…

You folks must be old. Being in our twenties, my friends and I hate Obamacare. We give up most of our discretionary income (about $230 a month) for insurance that before Obamacare we would not have paid for until we were in our forties. Our money is clearly going to older people, and it is not a coincidence that older people are the ones voting. Obamacare is a massive redistribution of wealth from one generation to the next. All Dems that love Obamacare should be footing the bill, not us healthy young people that don’t want or need insurance, and statistically will not need it for many many years.

Anonymous, thinking that you don’t need health insurance until you are in your 40s couldn’t possibly be more foolish.

Howard, I will agree with you if you statistically prove your point. How many people in their 20s get a hospital at more than $5,000 (I will have to pay $5,000 in case of emergency).

Average cost of a normal, low risk birth is now about $20,000. But you must be a guy so you are not going to get pregnant. Also gay, so you are not going to get any woman pregnant either. Usually happens in the 20s to early 30s. Happens a lot.

Anonymous, do yourself a favor and do some googling about why people in their 20s should have health insurance: you will find loads of people like you, people who thought “I’m a healthy 20-something, I don’t need no stinking health insurance.”

And who then suffered a medical emergency.

Your statistical reasoning is faulty: being above average doesn’t keep you from having appendicitis, or a skiing accident, or an allergic reaction you didn’t know you suffered from, or a pregnancy, or many other very expensive situations.

As it happens, I went without health insurance in my 20s: it was one of the stupidest things I ever did, because, like you, I didn’t consider event risk appropriately.

P.s. the good news is that even if you are diagnosed with cancer tomorrow, thanks to the aca, you will at least be able to get insurance in the future.

Anonymous,

You could forgo the insurance. The penalty is small in 2014 but it climbs in 2015 and 2016. If you are making 60K in 2016, you don’t receive insurance from your employer and you don’t want to buy it on the exchange, you’ll need to pay a penalty of approximately $1250. That’s less than the cost of the insurance but then you don’t get anything for the penalty tax. Neither option is good–buy expensive insurance with a high deductible that you don’t need. Or pay a hefty tax.

In general, this Administration’s policies have been very bad for your generation (and for mine too actually)

anonymous, when you slip and fall and break your leg after a night on the town, are you going to foot the emergency room bill and followup costs without the insurance? just note, hospital rates for the uninsured are much higher than the others with insurance. you are so naive when it comes to understanding risk.

Lol – statistically, how many people in their 20s get a healthcare bill that is larger than a $4000 or $5000 deductible, which is what the cheaper insurance plans (also the only ones that single men making $35K a year can afford) cost.

anonymous, i would have no problem with those opting out to have the term “loser” tattooed onto their forehead, so when they arrive unconscious at the emergency room we don’t have to treat them. i guess you could carry around the $3000 cash in your pockets, and if we find that cash in your pockets we can give you $3000 in medical care to cover our expenses to that point. then we stop.

just out of curiosity, you don’t mind paying a higher premium when you are older because we cannot spread the risk to the younger population at that point in time either? you pay either way, its just now or in the future. or will you avoid health insurance when you are older as well?

If Obamacare was not around I would look at how healthy I am compared to the average person and make my decision based on that. If I was much more healthy I would not buy it, if I was average or less than average than I would not buy it. Statistically, this is the best way to do it. If I was very healthy and ended up with cancer, which is what happened to my dad, I would either pay for the treatments if I could afford them or, if I couldn’t afford them, not get the treatments.

anonymous, you would get the treatments. but not pay for them, and pass the cost onto others. that is why you are required to have insurance. to protect the rest of us from deadbeats.

your problem with statistics is that you do not understand you are simply a probability. you think you can choose which probability you are, but you cannot. ignorance is bliss i guess.

All insurance is a redistribution from one population to another. That is the system that the private capitalist sector came up with when it created insurance.

I gather you are a young man, so how much do you pay in auto insurance. I bet it is more than the average.

So why aren’t you making up numbers to contest auto insurance–required in virtually every state.

Lol – Obamacare makes you buy insurance for yourself, auto insurance FOR YOURSELF is NOT REQUIRED. Otherwise I would protest it. The insurance you purchase for you car, if it is liability, is to cover the externality that you could cause someone else. Obamacare is not a liability plan, or at least it isn’t priced as such for people in their 20s.

anony, i bet you have auto insurance to cover yourself.

“Obamacare is not a liability plan, or at least it isn’t priced as such for people in their 20s.”

actually it operates that way. because otherwise joe public has to cover your stupid trips to the emergency room. you are required to have insurance so somebody else does not have to cover your medical bills.

baffling – I know it operates that way! That is why I am saying it is so unfair to those in their twenties: it operates as liability but IS NOT PRICED like liability. Do you not understand that? Nobody in their right mind would give a substantial portion of their discretionary income to liability insurance, which is why Obama mandated it, and which is why Obamacare is controversial. If it weren’t for the mandate, which screws over all healthy people that are my age and don’t want insurance, than no healthy person that doesn’t want insurance and is my age would purchase it.

And note that I am not saying that all healthy people in their 20s are getting the shaft from Obamacare, it is all people that are healthy and in their 20s and do not want to purchase insurance that are getting the shaft from Obamacare.

Do you understand how insurance works ? Apparently not!

Yes I do – and I understand risk, and on a risk adjusted basis there is no need for most people in their 20s to have insurance. If it were, Obamacare would not work because all of the funds that 20 year olds were paying into the insurance would be being paid out to people in their 20s. In reality, the whole idea behind Obamacare is that healthcare risks are spread out between sick people AND healthy people, and the healthiest people are in their 20s, which is why the mandate was a “must have” for liberals. If it wasn’t mandated, most in their 20s would not buy insurance because it is not a good deal for people until they get older.

Anonymous, if you really don’t want health insurance, you don’t need to pay for it. The penalty for 2014 is only $95 per adult or 1% of your household income, whichever is greater, with a maximum of $285. So if you really don’t want health insurance, don’t buy it. Nobody is making your do it. If you are single and your adjusted gross income is below $46,000, then you will be getting a subsidy for your ACA insurance. It’s your choice whether or not to buy health insurance.

I love the way supporters of Obamacare have moved the goal post. You guys are celebrating its success because it didn’t collapse? How things have changed.

Let’s go back to those heady days of 2010. You were so convinced that Obamacare was going to be your magic ticket to electoral success that you rammed it through on a risky one-party vote. Not to worry, as the massive new entitlement program was supposed to manufacture grateful, premium-subsidized voters. The creators of Obamacare expected to cruise to victory in both 2012 and 2014. But look what happened instead. They lost the House in 2012 and are poised to lose the Senate in 2014. The shutdown of the government is long forgotten but the bitter taste of Obamacare lingers on.

Republicans have stopped making ads about Obamacare. Why bother? It would be beating a dead horse: Obamacare is at all-time highs of unpopularity, with a 53% unfavorable rating. And Democrats are not defending it. Meanwhile, the few supporters left are desperately fishing around for something that they can point to. They don’t want to talk about the narrow networks. They don’t want to talk about the high costs to those who don’t qualify for a subsidy. They don’t want to rehash “if you like your policy you can keep it” or “if you like your doctor you can keep it.” They want people to forget that the Administration, in an attempt to limit the political damage, and without Congressional consent, delayed or mitigated the key objectionable parts of the law: the individual mandate, the employer mandate, etc. The only straws that they have to grasp are the polls that suggest that the uninsurance rate has dropped.

Of course it probably has–Obamacare is subsidizing the purchase of insurance. But how much is that drop really? A big part of the drop is the inclusion of young adults under 26 on their parent’s plans. But that could have been done separately without the rest of Obamacare. Another big piece is the expansion of medicaid. But that could have also been done without the rest of Obamacare. So how much of the remaining decline is a result of Obamacare–with all of its unpopular rules, regulations, and massive intervention into the health marketplace?

We really don’t know. Uninsurance rates climbed over the great recession and then started to come down naturally as the economy improved. With the recent improvements in economic conditions and labor market growth, the uninsurance rate would naturally drop independently of Obamacare. How much of the remaining drop in the uninsurance rate is just a result of an improved economy and how much is the result of more affordable subsidized insurance available through Obamacare? We don’t know. And how much does the drop in the uninsurance rate really matter anyway? People manage to get health care without insurance before Obamacare. And access to insurance does not necessarily imply access to health care.

I think you need another argument for Obamacare’s success besides the fact that it didn’t collapse. How about this? Obamacare is a success because….cancer death rates didn’t climb. Or how about: Obamacare is a success because….the web site is partially working. Or: Obamacare is a success because….premiums didn’t rise 25% this year.

sorry 2012 = 2010

Rick, “facts” created within and released from the confines of your self-generated reality matrix are like Soviet rubles were in the days of the USSR – curiosities when brought outside the Soviet empire, but curiosities with no with no real value.

Ottnott,

Can you be more specific on the facts that I’ve manufactured in my self-generated reality? Might help me to break out of my conservative intellectual prison.

Wow, talk about a complete projection! There’s hardly an actual thought on display, which makes responding hard, but one must try to at least try to make 2 points:

1. Yes, it’s true that “obamacare” polls poorly; on the other hand the provisions of the affordable care act poll extremely well so what of it?

2. The success of the affordable care act is measured the same way it always has been: thanks to regulation, subsidies, and the end to bans on pre-existing and to recission, millions more have insurance and tens of millions have better insurance, while the progressivity of the tax system has been enhanced. This is bad because?

P.s. you have probably noticed that even mitch mcconnell has noticed that straight repeal is not a winning approach, obamacare polling or not….

Howard,

There are quite a few thoughts on display in my comment but you don’t seem to know how to respond to them. But I’ll respond directly to your points:

1) The fact that individual pieces of Obamacare poll well is irrelevant. If you ask people questions in the abstract such as “Should insurance companies be allowed to deny people coverage on the basis of pre-existing conditions?” or “Should oil companies be required to charge less for oil?” it’s not surprising that many people would answer “no” to the first question and “yes” to the second. People like benefits. The problem of course is that the benefits come with costs and the only relevant question is to ask them how they feel when we include the benefits and the costs in a complete package. The public has answered that relevant question pretty consistently on Obamacare.

2) Among the many thoughts in the comment you seem to have missed were those that questioned the relevance and magnitude of the poll numbers on increases in insurance rates. I pointed out that much of the increase could have been achieved very simply without all the complexity of Obamacare. And I also asked how much of the remaining increase results from subsidized insurance and how much results from a recently improving economy. When you subsidize something, you get more of it, so not doubt Obamacare increased the numbers. But by how much?

I also questioned the relevance of these increases, pointing out that people get medical care without insurance and that access to insurance does not imply access to health care. The relevant question is, are people actually getting more health care and at what cost? The number of people insured doesn’t really answer that question.

You didn’t respond to any of these thoughts. And you didn’t respond to the others either.

To your other point, it’s true that marginal tax rates have gone up, but not in the way you think. Obamacare has raised marginal tax rates not on the rich so much but rather on the poor. It’s phased-out insurance subsidy scheme imposes substantial penalties on the marginal benefits of working, which is exactly what the poor don’t need. Very bad economic policy.

If you have been following my comments on this topic in the past, you might remember that I have argued that the serious Democratic politicians know that they need to fix Obamacare. But I’ve also argued that the serious Republican politicians know that repeal is not a viable political position. So, I think at some point they will fix it. What’s not clear is whether they’ll do it after the election to take the issue out of the Presidential race. Plus, I think a number of Democrats would like to delay any fix as long as possible, hoping that the poll numbers will get better.

Rick stryker, I’m going to continue to ignore most of your non-thoughts, since they amount to saying that you personally would have written a different law.

So would I.

So what.

The law we have is working perfectly well even though, shockingly enough, of course it could be improved. As for your conclusion regarding “obamacare,” it would hold water if we didn’t have the now-classic kyconnect comment: “this is a lot better than that obamacare.”

In short, thanks to incessant right-wing lying, lots of people have no idea what “obamacare” is. They think it’s death panels and a broken web site.

I guess having health insurance rather than no insurance is no benefit in your books. I wonder if you would have a different opinion if you were the one without insurance!

Slug and Josepy,

You guys conflate Menzie’s point about enrollments with the cost of Obamacare. The federal government is spending billions on implementation even before we get to the actual cost of the insurance. Then all the insurance premiums are going up. Just because the government is paying half or more doesn’t change the fact that government provided healh insurance cost is flying through the roof. Menzie has his enrollment numbers because of the government is taking from the healthy to subsidize anyone, because there is no verification of income. And that doesn’t even touch on the fraud becuase the system has no security and the Obamacare staff has no background checks. The fiasco of Obamacare is deeper than any statistical analysis of phony enrollment numbers can come close to.

Slug, You are so ignorant when it comes to gold. Don’t you know it is better to remain silent and be thought a fool than to open your mouth and remove all doubt. Over and over I have tried to help you understand that gold is not a good investment; gold is an indicator. I discourage investment in gold because its value is determined by the whims of the government and the FED. If you want to invest in gold be my guest.

What gold is telling us and has been telling us for a few years now is that he FED has been pulling back on their Keynesian stimulus efforts. But since you asked, I did make money on gold in the recent run up but I got out fast because the FED is telling us it is pulling back. I know I am wasting my time because I have tried to teach you this lesson before and you did not learn, but it will be good for others to read for understanding..

Now Slug and Joseph, can you tell me specifically how the government subsidy is calculated? Also what the restrictions are on business plans and when will they go into effect? Also just what is the net number of those who has lost their insurance to those who are new to insurance? And while you are at it perhaps you could tell me just how many angels can dance on the head of a pin?

stryker

“I love the way supporters of Obamacare have moved the goal post. You guys are celebrating its success because it didn’t collapse? How things have changed.”

my how things have changed. you were the one writing the absurd pieces about your son and brother opting out of obamacare, leading to its eventual collapse. still waiting to hear you acknowledge how wrong you were in those rambling posts. your scaremongering was just a waste of time.

Baffles,

Those comments were about the perverse incentives created by Obamacare and they are just as valid today.

rick, those “perverse incentives” were your excuse for why obamacare would fail. and you were WRONG. mostly because you use strawman arguments, which ultimately fail in the long run. strike one.

‘ Today’s results from the American Community Survey corroborated earlier results from the National Health Interview Survey indicating that insurance coverage had approximately returned to its pre-recession levels by 2013. That recovery in insurance coverage is thanks in significant part to the dramatic expansion in insurance coverage among young adults since 2010 that was described above and some States’ early expansions of Medicaid.’

Wow!

Patrick R. Sullivan: I am still waiting to hear whether you will admit your views on the depth of the downturn in Canada vs. US during the Great Depression were incorrect or not.

baffling

September 17, 2014 at 7:44 am

anonymous, when you slip and fall and break your leg after a night on the town, are you going to foot the emergency room bill and followup costs without the insurance

Different anon here. He’ll pay for it anyway with his $3,500 deductible.

PS Let me know when I start saving $2,500 a year. At that point I’ll call O-care a success.

It is amazing how many of the responses reveal how ideology blinds intelligent people to facts.

>when you slip and fall and break your leg after a night on the town, are you going to foot the emergency room bill and followup costs without the insurance

>Different anon here. He’ll pay for it anyway with his $3,500 deductible.

Ha, this just illustrates how little young adults know about the cost of healthcare. Just arriving at the door of the emergency room will set you back $1000 to $2000 before they even begin treatment. A surgical treatment for a broken leg will cost between $15,000 and $35,000. Are you sure you still don’t need health insurance?

PS Let me know when I start saving $2,500 a year. At that point I’ll call O-care a success.

Contrary to Ricardo above, rate increases for insurance premiums have been slowing down from their pre-Obamacare years. The average person today has a $2000 savings in insurance premiums from projections before Obamacare. How much of that decrease is directly attributable to Obamacare is debatable, but the fact remains that people are paying much less for premiums today than they thought just a few years ago. You certainly are saving thousands per year. You will be saving even more if the current trend continues.

Joseph,

Funny, I didn’t hear the President say that he was going to reduce the rate of growth of health spending below its forecasted value, saving families $2500 per year with respect to what premiums would have been, even though premiums actually go up. I thought that I and the rest of the country heard him say over, and over, and over that our premiums were going to go down on an absolute basis by $2500. Maybe I missed the nuance?

Oh well, at least the rate of health care spending has slowed with respect to previous expectations, whatever the reason.

Wait a minute. Houston. We have a problem.

“Health spending in July 2014 grew 4.3% over July 2013, bringing the year-to-date increase to 4.4%. This is well above the 3.6% growth rate estimated for 2013 by the Centers for Medicare and Medicaid Services and, with further acceleration expected in the final two quarters, puts 2014 on track to be the first year since 2008 in which growth has exceeded 4%.”

Anonymous First, you won’t be a twentysomething forever. If you’re rational you will want to smooth out the cost of health insurance over your lifetime. That means overpaying somewhat when you’re young and underpaying when you’re old. Second, almost every insurance program involves redistribution of one kind or another. Medicare is a generational redistribution program. So is Social Security. And older drivers subsidize the insurance rates of younger drivers. And education is also a generational redistribution, from the old to the young. So wake up from your solipsistic slumber. Finally, even though the young are generally a low health risk, keep in mind that a “low” health risk is not the same as a “zero” health risk. Most young people tend to underestimate their health risk because they suffer from too much survivor bias.

Ricardo The effect of Obamacare on involuntary unemployment is ambiguous. The CBO predicts an increase in voluntary unemployment (a good thing if you believe in free choice), which would likely open up jobs for those who are currently involuntarily unemployed. In some cases the employer mandate could increase unemployment for those who work in a business that does not currently offer health insurance. On the other hand, the employer mandate is likely to increase employment for those businesses that have always provided health insurance because premium increases for those businesses will be less than they otherwise would have been. My hunch is that when all is said and done the net effect on employment will be a wash. But we can be fairly sure that over the long run Obamacare will make for healthier and more productive workers. Of course, if you’re really worried about the employment effects of Obamacare, then you should be pushing for single payer, which eliminates the employer-based health insurance system that is surely one of the stupidest and most unfortunate historical accidents ever to plague this country.

Rick Stryker You’re making some very dishonest arguments. But let’s be clear about one thing. You unambiguously predicted that Obamacare would fall well short of meeting its enrollment goals and would collapse of its own weight. You were wrong…just flat out wrong on the facts. Second, you are mischaracterizing the poll numbers. One thing we know is that people like Obamacare if you call it by a different name. Ask the folks in Kentucky. We call them “low information voters.” And one of the reasons that people dislike Obamacare is because it wasn’t left-wing enough. It did not offer a public option, which upset a lot of folks. Discontent with Obamacare isn’t restricted to just right-wing kooks. Obamacare is a kluge and far from my ideal plan. But given our dysfunctional politics and given the stupidity of red state voters and the corrupt nature of our politicians, Obamacare is probabllyl about as good as we’re likely to get. Maybe things would be different if we could somehow persuade states from the Old Confederacy to reconsider secession, but other than that we just have to accept second/third/fourth best solutions. You are also misreading the political tea leaves. The Republicans haven’t stopped talking about Obamacare because they feel it will die on its own. They’ve stopped talking about it because some of them started to find out (to their horror) that “repeal and replace” invites voters to ask what Republicans would replace it with. This is a consequence of the ratchet effect. Repealing Obamacare is no longer an option. The status quo ante isn’t credible and everyone knows it. People may not be fully aware of all the goodies that Obamacare gave them, but try taking away those goodies and they will quickly become aware.

And nice attempt to try and turn things around by pretending that the supporters of Obamacare are the ones that have to explain its failures. Wrong. You were the one that was predicting it would fail, and it hasn’t. The fact that a very small number of fairly healthy and well-to-do people (less than 5%) might see their premiums go up is not exactly an argument against Obamcare when 95% will see significant benefits. But like a lot of conservatives you shed an ocean of tears for any slight that affects the rich, but you’re strangely indifferent to policies that hurt the poor. And downright hostile to any policies that help the less fortunate. It’s the Republican way. Now I agree that Obama never should have overstated things by promising that everyone would be able to keep their doctors, but that was never true even before Obamacare. The difference is that prior to Obamacare the rich did get to keep their doctors and it was only the poor who not only didn’t get to keep their doctors, but were lucky to have any doctor at all. I just love all of your crocodile tears. At times they’re almost convincing. But like I said, nice attempt.

2slugs,

I, like many others, looking at the trends, didn’t think that Obamacare would meet its enrollment goals. When it did, I acknowledged that you were right about that.

I also spent a lot of time pointing out the perverse incentives and problems with Obamacare and I don’t take any of that back.

rick stryker, you completely overstated your “perverse incentives” through strawman arguments. that is why you were completely wrong. and you have not acknowledged your mistakes, you simply moved the goal posts yourself by pushing the “failure point” into the future. you never backed down from claiming obamacare would collapse. you just like to advertise your ideology.

Maybe the best thing about Obamacare is that conservatives are *finally* talking about fixing America’s health care system which was, before Obamacare, totally F*ed up, and now is still F*up, but not totally.

Maybe now we’ll see some progress, though I doubt it. After all progress sounds too too much like progressive which is anathema for “conservatives,” though most conservatives are anything but.

I am more conservative than those boys and I voted for Obama twice and would again even though I think of him as a center right politician similar to Dwight Eisenhower!

People forget that what started the speculation about Obamacare imploding was the disastrous web site roll out. Since that hasn’t been in the news, people think that problem has been fixed, especially when we learn that the Administration spent $840 MILLION to build the website. $840 MILLION!!! OF THE TAX PAYERS’ MONEY. FOR A WEB SITE!!!

Close observers of the Administration will not be surprised to learn, that despite the $840 MILLION!!!, the web site’s not fixed. Up against the wall last year, the Administration solved their problem by making sure the ecommerce functions of the web site worked well enough to mount their last minute marketing campaign. But they never fixed the back end. Even now, it’s not built. And they didn’t solve the security problems.

In November, the Administration knows that it will have to somehow sign up new people and not lose a significant number of current participants in order to keep claiming success. But they are afraid to have too many people on the web site. What’s their solution? Hide the problem and shift the consequences to a later time, of course– the way they solve all Obamacare problems.

The Administration has announced that it will auto-enroll people in the same plan as last year, unless people explicitly choose to change plans. That sounds benign and most people will assume that it’s just like getting rolled over into the same plan at work. But the Administration still hasn’t built the back end of the website, despite spending $840 MILLION!!!. Thus, the Administration has no way to verify income automatically and compute correct subsidies given current prices. In practice being rolled over means that you will get the same plan (with potentially new pricing) and the same subsidy as the previous year, even though your subsidy may have changed.

That can be very problematic. Many insurance plans that priced higher than the average in 2014 didn’t get much market share and are planning to lower prices this year to grab market share, with their risks subsidized by the Obamacare reinsurance scheme. However, the consumer’s subsidy depends on his current income and the cost of the second cheapest silver plan, which can change if the repricing changes the cost of the second cheapest silver plan. Come 2015, consumers could be surprised to find relatively large percentage changes in their premiums if their subsidy unexpectedly changes. Or, they could find that they have a sizable tax bill in 2016 when the subsidy they received in 2015 is reconciled to 2015 taxes.

But all those problems happen in the future. The focus on the Administration is to keep people off the website now. Thus, the Administration continues its policy of shifting the costs and problems of Obamacare into the future while front loading the benefits, so that its loyal supporters can point to the benefits and say “it’s a success.”

rick stryker, how much money was wasted when the republican’s shut down the government? your bold type is a fraction of that event. republicans wasted an enormous amount of money in that ideological demonstration. please show your contempt for waste there as well.

Rick Stryker: I think you have officially joined the grumpy old man club, writing in ALL CAPS. In reading the numbers, I see you exercised over $840 million (to provide infrastructure for health care for over 300 million people in a $17 trillion economy), and yet not exercised at all (as far as I can see) over the nearly $1 trillion spent in Iraq for a war sold on the premise of WMDs. Let me say that you seem to have no sense of proportionality.

In addition, when you type in $840 MILLION!!! in bold caps, you remind me of the evil character in one of the Austin Powers movies. I just can’t stop laughing.

Keep up the good work!

Menzie,

You might be surprised to learn that there is a lot that the Bush Administration did that I was not happy with. The Bush Administration claimed the Iraq War would cost $100 billion and fired Lawrence Lindsey for estimating the cost at $200 billion. That they spent $1 trillion on it is outrageously irresponsible. As you know, I don’t buy into the conspiracy theories that they were making up the WMD threat to justify a war. They did believe in good faith that there were WMD in Iraq, just like most of the Democrats. However, I do blame them for not being realistic about the spending nor honest with the public about it. That they ended up wasting obscene sums of money is symptomatic of the more basic problem, which was they didn’t have a well-thought out rationale for what they wanted to accomplish and a plan for how and when they would get out.

Rick Stryker, as someone who apparently has never been a participant in the individual health insurance market, you might be surprised to learn that health insurance companies have always defaulted to automatic renewal each year. There is no conspiracy here. The insurance companies are simply doing what they have always done.

This is typical ignorance of basic facts about the individual health insurance market that people like you have demonstrated over and over again and suddenly discovered that the rest of us have been living with for decades.

Joseph,

Once again it’s you who are ignorant of the basic facts. And you’ve missed the point, yet again, to boot.

The government is now heavily involved in the individual insurance market and it’s government, not the private insurance companies, that is making the decisions. Of course the insurance companies would like to auto-enroll as is the practice, but they can’t do that unilaterally since the government is paying part or most of the premiums for about 85% of their customers.

Thus, HHS announced that consumers would be automatically renewed on the Federal exchanges. This does not apply to state run exchanges, which will have to determine their own policy. In practice, this means that consumers will automatically get the same subsidy as last year, even if that subsidy has changed.

That policy is good politics but bad for consumer economics. It’s good politics because the Administration needs to keep most of the people they have and then sign up new ones in order to keep claiming success. If people had to go through the redetermination process on the web site to renew their insurance, a lot of them might just bag it, which the Administration doesn’t want. Plus, it’s a shorter sign up window and the Administration wants millions of new people on the site. There is obvious concern about the ability of the site to handle a potentially much higher volume of traffic. The insurance companies are of course happy with the HHS decision since it allows them to continue their practice of auto-renewal, which helps them keep a stable customer base.

It’s bad for consumers though because most people really should go through the redetermination process on the web site to have the opportunity to change plans if their subsidy level has changed. Yet, this policy is encouraging them to do something that’s not in their own best interest.

“The government is now heavily involved in the individual insurance market ”

rick, what percentage of the insured has obtained coverage through the federal exchange?

LOL. Rick is upset that the government is auto-enrolling consumers instead of letting the insurance companies do it.

Per your comment, Rick, the government is now the one who makes the decision whether or not to auto-enroll those who obtained insurance through the Federal exchange. Given that the alternative, not to auto-enroll, would almost certainly lead to a lot of people losing coverage, your position appears to be that it is better for those who fail to act each year to lose their coverage altogether rather than to keep their existing coverage and subsidy without going through the “redetermination process on the web site to have the opportunity to change plans if their subsidy level has changed”.

To simplify:

Government plan: auto-enroll consumers and advise that they should go through the redetermination process, because the plan offerings and their subsidy levels are likely to change each year

Stryker plan: advise consumers that they should go through the redetermination process, because the plan offerings and their subsidy levels are likely to change each year

Because, in Strykerland, failure to redetermine should be severely punished.

Wow, the statists on this blog are feeling their oats. Let me see if I have this right. By (1) mandating purchase of a product that most people already purchased (and liked) and for which there is an innate, relatively inelastic need; (2) subsidizing purchases for those who it is deemed could not; and (3)enforcing enrollment using the most powerful and feared government agency (IRS), you think it’s a great accomplishment that more people (ignoring really bad measurement error and conflating Medicaid sign- ups) have signed up? That required only slightly more product design and marketing prowess than that exhibited by the designers and marketers of Kim Jong-Il’s last election campaign where he won 99.9% of the vote. Big whoop.

The sad thing is that initially, these socialist enterprises live off the existing financial, physical, and human capital in place. Venezuela didn’t go to hell in a hand basked immediately, but surely as incentives and freedoms were crushed things have headed south. Toilet paper for all! Even more sadly, market responses to the ACA, many of which were actually underway prior (drugstore clinics, concierge medicine, alternative medicine, “Walmartization”) will make things look better, and you’ll think it’s because of your “policy genius”. But make no mistake, whether its accelerated doctor retirements, longer wait times, more mistakes, fiscal cost overruns, gross fraud, resource misallocation….IS ALREADY occurring.

I can tell that even some of those who support all the subsidization in the ACA, and are economists recognize how distortionary and inefficient the ACA is, especially compared to simple, much less distorting vouchers. But you say, “Well, the ACA is better than nothing”. No, that wasn’t the choice. When you have the ability to ram anything through Congress and you come up with this, then you are not about efficiently subsidizing access to healthcare, you are about statism and control. Because YOU know better.

You say that the enrollment data and enrollment metrics are the clincher. President Obama spelled out the “Key Success Factors”, KSF’s in the run up. You can keep your plan if you want; you can keep your doctor if you want; the average family’s insurance cost will go down $2,500 per year. These are HIS promises, HIS metrics. The ACA has failed based on these metrics. Measuring purchases of a product that you force or pay people to buy, and that nearly everyone already wants and buys is a ludicrous metric. Anybody can use this total amount of government force an increase coverage.

Menzie,

How would this factor into your analysis?

The largest insurer with the lowest premium rates on Minnesota’s Obamacare exchange is dropping out because the government health-exchange is unsustainable, the company announced Tuesday.

PreferredOne Health Insurance told MNsure, the state-run exchange, Tuesday morning that it would not continue to offer its popular insurance plans on the marketplace in 2015. It’s “purely a business decision,” spokesman Steve Peterson told KSTP-TV. The company is losing money on administrative costs for plans offered on the bureaucratic and glitchy government exchange.

ricardo, considering you are linking to a limbaugh article i would say you don’t factor a single thing into the analysis. but glad to see limbaugh has an influence in your world view!

PreferredOne has specialized as a 3rd Party Administrator (TPA) for self-insured groups, most of whom went from insured carriers with structured benefit programs. As a covered party with previous experience in managed care, I saw their expertise isn’t in designing/managing benefits — they rely upon the employer groups to do that. Surprisingly, their “back-room” structures were pretty weak as well. My sense was they were always playing catch-up and never got ahead of the curve.

It’s a great recipe for disaster: high volume of members, a relatively new role, weakly developed infrastructure. When they decided to bail, they realized what many thought: the odds were against them from the get-go.

Slug,

When I talk about the employee mandate for business Obamacare I am not talking about employment. While businesses will see their health insurance costs reduced it is doubtful they will add employees because of this. The business reductions in health insurance costs will be pulled from other productive businesses. As a matter of fact many businesses will totally eliminate their company health insurance and push their employees on to the exchanges. The exchanges can’t handle what they have now so the log-jam, the confusion, and the fraud (both from those hacking Obamacare information and the criminals who will be hired in the Obamacare system) will only increase. This is where Menzie will see his numbers skewed. He is premature in making his analysis. Don’t forget, not even 50% of the provisions of Obamacare have been implemented, that is not even counting those who will find that their tax bill is going to be huge once their incomes are verified (if they ever will be).

I am not worried about the employment effects of Obamacare, but if I was I would push for a free market solution not a totalitarian top-down-driven government system. We have tried that with Medicare and it is costing a fortune, not paying doctors, and reducing care. No thanks!.

«I would push for a free market solution not a totalitarian top-down-driven government system. We have tried that with Medicare»

Ricardo, please prove your point by quoting which part of Medicare law has made it illegal for senior citizens to have private insurance along with Medicare if they choose so. We need to know because there are probably millions if not dozens of millions of criminals who are cheating the “totalitarian top-down-driven” Medicare and Veterans health systems by having integrative private insurance too.

«and it is costing a fortune, not paying doctors, and reducing care. No thanks!.»

So you want to abolish Medicare and the Veterans health systems because they are “top-down-driven government system”s that are “costing a fortune, not paying doctors, and reducing care”.

I am sure that you want to protect civilian and military senior citizens from exploitation and other horrors of Medicare and the Veterans health system, and only abolition will do, but those are mostly committed Republican voters, and they think that the government should keep their hands off their Medicare and Veterans health system accounts.

What would tell those Republican voters that you want the government to confiscate their Medicare and Veterans health accounts?

Menzie,

Could you give us your estimate on how much pulling our military out of Iraq prematurely will cost us? It has cost Iraq almost 50% of their land mass, not counting the number of heads that have rolled, literally!

We pulled out of Iraq on the date President GW Bush agreed to with the Iraqi government.

Ricardo, PreferredOne is actually one of the smaller health insurance companies in Minnesota. Other insurance companies are remaining in the Minnesota insurance exchange — Blue Cross Blue Shield of Minnesota is 10 times the size of PreferredOne, HealthPartners is 4 times the size of PreferredOne, Medica is 3 times the size of PreferredOne, and UCare is 2 times the size of PreferredOne. All of these larger insurance companies will remain in the health exchange for 2015.

In 2014 PreferredOne lowballed their bid and managed to attract 31,000 customers by vastly underpricing their competitors. Except they made a fatal error in calculation and ended up losing millions of dollars by underpricing. The company managers made a stupid mistake and are being forced out of business by their stupid mistake. Apparently their shareholders are angry with the PreferredOne managers for losing millions of dollars and the cowardly managers are inventing excuses for their blunder — the dog ate my homework.

The larger, more successful and better managed health insurance companies will remain in the exchange for 2015. Isn’t that the way capitalism and competition is supposed to work — poorly managed businesses shrink and well-managed businesses grow?

Professor Chinn, I am sorry I do not have the time for a long rebuttal but

to you and your cohorts this is all that matters.

http://washingtonexaminer.com/article/2553569

One of the funniest things about this whole discussion is that the ACA was designed by red-blooded Republicans to ensure that “strapping young bucks” would have to pay health insurance premiums instead of merely turning up at the emergency room and to get fixed at the expense of “moral majority” premium payers after a day of drug-fueled crime and eating of t-bone steaks and accidents driving around in the Cadillacs of “welfare queens”.

Because the mandate in the AEI/Romney plan that was renamed as the ACA was designed to solve the problem of young dark-skinned deadbeats getting treated at the expense of older light-skinned business owners paying increased healthcare premiums for their employees, not the problem of them not having healthcare insurance.

Ah the irony!

Rick Stryker,

I work for a very large corporation. We needed to do a complete overhaul of our accounting system and after the design only estimate came back it would cost us $8 million. The corporation determined thtis was excessive and directed the planners to develop a phased approach. We spend $1 million in the first year and since have spend about $2 million. We will probably spend another 10 million spread over 5 years. Our accounting system was installed in about 9 months and is working fine. there were initial problems but all glitches were fixed within the first 3 months. Operations continued and no accounting data was lost.

I agree with you. An $840 million price tag is outrageous and could only be justified by the government spending other people’s money. And it is even worse to consider that the system still does not work. I think it is criminal. I know our officers would never put up with it and every company involved would be in a law suit. But then a business’s primary purpose isn’t greasing palms and asking for donations. Businesses actually produce products or they go out of business.

Ricardo,

Yes, indeed. Government should not be engaged in activities best left to private business. $840 million for a web site is completely ridiculous.

For the Administration, the web site was an important symbol that government could provide goods and services just like private businesses do, and deliver them in a cool way, just like they do in Silicon Valley. But no matter how many times government fails, people never seem to learn.

A fascinating historical example goes back to the dawn of modern aviation. The British novelist Nevil Shute, who wrote some famous books such as “On the Beach,” was an entrepreneur and engineer before he became a successful author. Shute’s great interest was in the nascent field of aviation, and Shute helped to start companies and build the first airplanes. In his wonderful autobiography, Slide Rule Shute relates a controlled experiment he participated in that was designed to determine whether government or private industry could do a better job building a new technology.

At the time, in the mid-1920s, expert opinion did not believe that fixed wing aircraft would ever be technically capable of commercially carrying passengers and cargo. Instead, it was believed that dirigibles were the technology of the future. Shute’s company, Vickers Ltd, proposed to the government in 1923 to build 6 airships and the Conservative government agreed. But before any documents were signed, the government lost the election and was replaced by Labor, who were naturally suspicious of private companies and felt the government should be in charge of a new strategic technology.

The new Labor government of Ramsay McDonald appointed a Cabinet Committee to decide between Vickers and the government, but they were not able to come to a definitive conclusion. So, they decided to perform perhaps the only controlled experiment of capitalism vs. government in history. It was decided that Vickers and the Air Ministry would compete against each other to build an airship of comparable design. Vickers would need to raise private capital to build its ship, the R100, whereas the Air Ministry would use state funds to build the R101. Once the ships were built, Vickers would demonstrate a successful design by flying the ship from England to Montreal, Canada. The Air Ministry would fly their ship to India. In this contest. the government had all the advantages. For example, each side’s plans had to be reviewed and approved. And who was responsible for doing that? The government, of course, which had to review and approve its own plans as well as the private company it was competing against.

Shute relates a lot of interesting details of the story. But in the end, Shute and his fellow businessmen and engineers did successfully fly their airship, the R100, to Montreal and back. However, the R101 took off from England with political dignitaries aboard for India, but crashed into a fiery explosion in France, killing 48 of the 54 people on board, including all the dignitaries.

After the disaster, the government convened an inquiry but did not invite anyone from Shute’s company to give an opinion about what happened. Rather than conclude that the government should not have been involved in private business, the government instead concluded that no one should be building airships!

Ironically enough, this turned out to be the right decision, albeit for the wrong reason. Soon after the R101 disaster, aviation engineers realized that fixed wing aircraft were commercially viable and the market shifted in that direction quickly, leaving the airships of the 1920s behind as historical curiosities.

Shute goes through the reasons for the disaster in some detail. His main conclusion is that it wasn’t caused by incompetence. The government had access to the same technology, to the best experts, and to ample funding. Despite these advantages, the government had the wrong incentives and therefore made a series of very subtle mistakes that resulted in disaster.

I often think of this story when I read about something like Healthcare.gov.

Rick Stryker: “Yes, indeed. Government should not be engaged in activities best left to private business. $840 million for a web site is completely ridiculous. For the Administration, the web site was an important symbol that government could provide goods and services just like private businesses do, and deliver them in a cool way, just like they do in Silicon Valley.”

Then you should be delighted to learn that the state of Oregon hired Oracle from the private sector, the world’s largest database software company, headquartered right in the middle of Silicon Valley and staffed by the best and brightest Silicon Valley software developers to build their state’s health exchange. Oracle billed Oregon $240 MILLION (did I get the bold and caps right?) to develop an ACA exchange for just one medium size state. And how well did that work? To date Oregon has not signed up one single person on their web site. Not one single person has been able to use the site, even today. They have had to resort to all paper forms. So much for the miracles of the private sector in Silicon Valley.

Meanwhile, the federal site, healthcare.gov, serving 34 states, signed up 7 million.

Joseph,

Oregon is not a counterexample to the point I made but rather another example. Both Covered Oregon and HealthCare.gov hired private contractors. And in both cases the results were disastrous. However, the Federal government had the clout to bring in a team of very experienced developers who managed to repair ecommerce components so that they were good enough to avert disaster. As I have already noted, they did not fix the back end or really deal with the security issues. That’s not criticism–I think they were wise to focus on the ecommerce part given the timeline they had. If they had tried to do everything, they would have surely failed. If Oregon had been able to airlift the same people in, they might have gotten the site fixed well enough to avoid the mortification they suffered.

Some of the $248 MILLION!!! from the project was spent on absurd, surreal commercials, which were amusingly lampooned by John Oliver. You’ll note that I’ve written the $248 MILLION!!! the proper way, with 3 bold exclamation points (since you asked.)

What HealthCare.gov and Covered Oregon had in common is that the government tried to manage the project by hiring private contractors. But government has no ability or experience in managing and delivering large scale software projects. A useful contrast is Covered California, which worked. The difference was that California wisely did not try to manage the software project but rather took bids and hired a private company to manage the project as well as run the website. That’s much better.

Even better still would be for the government to stay out of it all together. There are already private companies that provide electronic marketplaces for the purchase of health insurance. If the ACA had never required that these websites be built, these companies and new ones would have jumped in to provide that service, more cheaply and more efficiently than government can do it. The competition would have meant that consumers would have had choices as to which health ecommerce website they preferred to use and the technology available would have ultimately been much better.

Feds lack the data to determine how well key Obamacare provisions are working

Ottnot,

“Stryker plan: advise consumers that they should go through the redetermination process, because the plan offerings and their subsidy levels are likely to change each year

Because, in Strykerland, failure to redetermine should be severely punished.”

No, that would not be the plan in the Stryker Administration. Let me lay out what my plan would be:

1) Unlike the previous Administration, I would not by executive fiat change the features of the law that I didn’t like or that I found inconvenient, despite my opposition to Obamacare. I would work with Congress to repeal and replace it but for now would make the best of a bad situation.

2) Unlike my predecessor, I would not play even one round of golf or take one vacation until I had personally overseen the repair of the website.

3) I would not have a policy of auto-enrolling people.

If you think about how auto-enroll would work in practice, you have to have a whole new set of rules to cover all kinds of situations that are likely to come up. And indeed the Administration has created a whole new set of convoluted rules. Under the Administration’s current plan, you will be automatically enrolled in your current plan. But what if that plan is no longer available? Then, the consumer is enrolled in the the following choices in order of priority:

a) Another plan of the same metal level offered by the current provider

b) If a) is unavailable, another plan one metal level lower or higher offered by the current provider

c) if b) is unavailable, some other product offered by the current provider even if off exchange

My Administration would have a number of problems with rules like these.

First, is this even legal? The Supreme Court signed off on the Obamcare mandate on the grounds that it is a tax and not a mandate. But can you just enroll people in some product without their consent and force them to unenroll themselves if they don’t agree? If you can do this, why can’t you then just auto-enroll the whole country? Why not have universal coverage right now?

Second, should the government be favoring the current insurer at the expense of potential competitors by giving the current insurer a privileged position? Is this best for the consumer to allow the current insurer to assign consumers to their current products when other providers might be better? Should the current provider be able to auto-enroll a consumer off exchange with no subsidy available even if that consumer qualifies for a subsidy? If given the choice between allocating a consumer to a higher or lower metal level, is it OK if the provider always chooses the higher and more expensive metal level? These rules shift the re-enrollment work away from the Administration to the provider, who is incentivized to comply because of the competitive advantage they receive, but is this best for the consumer?

Third, does auto-enroll really maximize the number of insured people? Although auto-enroll will keep people who are too busy to re-enroll, or just forget, etc. in the system, at least temporarily, it will also put quite a few of those same people into a situation in which their premiums are a lot higher than they expected. When people are too busy to re-enroll or just forget, they also don’t read letters carefully or don’t think about it too much. But once they start getting the higher monthly bill they might just stop paying. So, it’s not at all clear that auto-enroll will maximize the number of insured people on net.

4) The Stryker Administration would follow a different strategy. All those sacrificed rounds of golf and vacations would have yielded some new functionality into the IT systems. Since the website database has all the new insurance plans, it should be possible to calculate new payment levels for insurance plans that the consumer may qualify for conditional on no consumer information changing and conditional on maintaining the same subsidy as last year. That information would be assembled and mailed to every consumer currently enrolled. The letter would also remind the consumer of dates of the upcoming re-enrollment period, the obligation to re-enroll and the increased tax penalty in 2015 for not doing so. And the letter would also explain the new “one-click” re-enrollment. As part of the overhaul of the website, the web-site would allow you to log in and click “automatically re-enroll.” The one click page would explain that the website has chosen for you the cheapest and most similar plan to what you had last year and is applying the same subsidy as last year. The rules for how the web site chooses the automatic plan would be transparent (“click for more information”) and would not be designed to favor any particular provider. The page would also explain that the automatic choice may not be best for each consumer and would advise that most consumers should complete the full process. And the page would also explain that in any event the auto-enroll price would eventually be reconciled with tax data and the consumer may end up owing more or less next year.

The one-click process would be designed to be completed in 60 seconds. But if people can’t be bothered to do even that, then they don’t get the insurance and will pay the tax penalty. Sorry.