The economy plugs along much as it did before the election, while the stock market hits new highs. What about other variables?

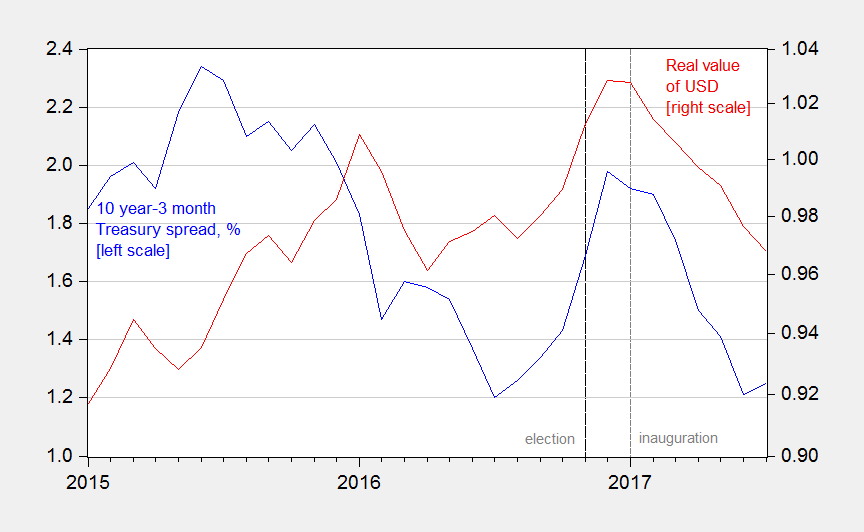

First, the yield curve and the dollar are at levels lower than what was recorded on the eve of the election. The former suggests slower anticipated growth relative to pre-election. The lower dollar suggests less of an anticipated economic boom relative to foreign countries.

Figure 1: Ten year minus three month secondary market Treasury yield, % (blue, left scale), and real value of US dollar on broad basis, 1973M01=1 (red, right log scale). Source: Federal Reserve Board, and author’s calculations.

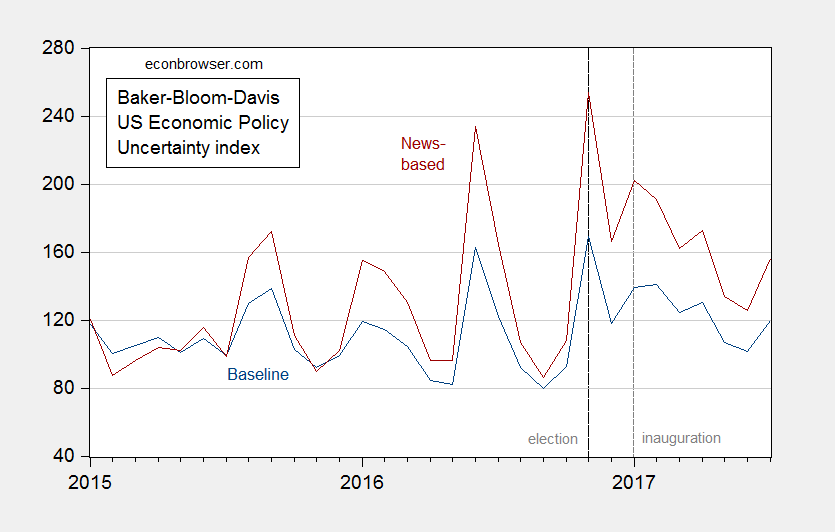

Economic policy uncertainty, as measured by the Baker-Bloom-Davis index remains heightened, but less than what was recorded in November 2016.

Figure 2: US Economic Policy Uncertainty baseline index (dark blue), and news-based (dark red). Source: policyuncertainty.com, accessed 7 August 2017.

High economic policy uncertainty is thought to depress particularly long-lived activity, like investment. This has not apparently been detectable in US aggregates (after all, importance of uncertainty does not mean offsetting expectations of higher aggregate demand don’t matter), but the example of UK Brexit is sobering. Anecdotal information here.

Did the consensus ever price in an economic boom in the US? Growth expectations in the US for 2017 did not shift, at least according to Blue Chip – essentially flat at 2.2%. Meanwhile, expectations for growth in the euro area, Canada and Japan have picked up materially. So, it may not be fair to characterize the way you do. The USD has sold off because growth overseas has surprised to the upside, not because growth in the US has disappointed.

Neil: WSJ surveys indicate 2017 US annual growth accelerating from 2.2% to 2.4% from October to December surveys (mean); 2018 annual growth from 2.0% to 2.4%.

May to June, 2018 mean growth forecast has dropped from 2.5% to 2.4%; 2019 dropped from 2.1% to 1.9%.

Seems like there was a shift in growth expectations upward then back to starting point.

If the stock market was discounting stronger future earnings — maybe due to lower taxes — it would show up as a higher market PE.

But it has not happened. In the months leading up to the election the S&P 500 PE on trailing operating earnings was trading just over 21. In the months since the election it has traded just below 21.

Trailing earnings bottomed just before the election — largely due to oil prices and energy stocks earnings –and in the first half of the year EPS has grown at double digit rates. All this was in motion before the election and would have happened regardless of who won the election. Since the election the surge in trailing earnings has accounted for over 100% of the stock market increase. The data clearly shows that there has been no Trump bump.

The market may be pricing in more business friendly policies, while the Fed tightens the money supply.

A fed tightening the money supply essentially always shows up as a lower stock market PE.