Just in case you were still wondering.

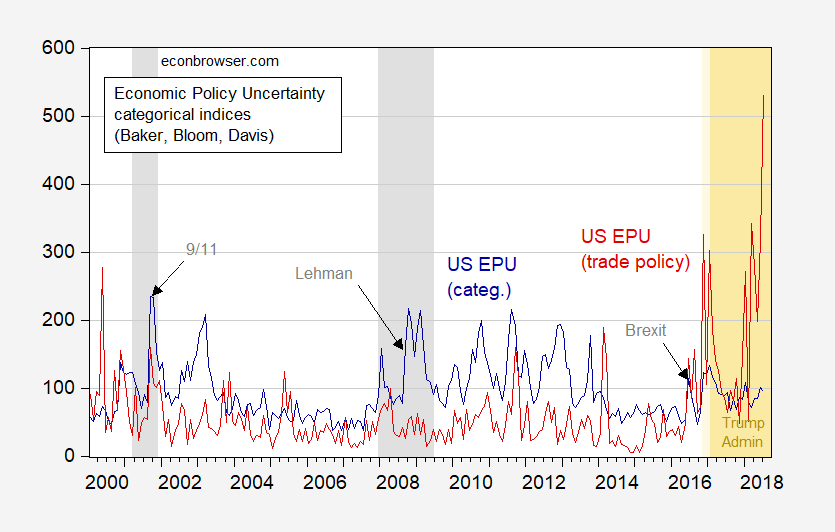

Figure 1: US Economic Policy Uncertainty (blue), and Trade Policy component (dark red), normalized to geometric mean 1985-2010=100. Source: PolicyUncertainty.com, categorical page

Does this uncertainty matter? Krol (2018) thinks both economic policy and trade policy uncertainty matters to varying degrees for FDI, imports and exports. Here, I’ll just observe that inbound FDI has decreased, as has industrial equipment investment (what I think should be particularly sensitive uncertainty regarding exports).

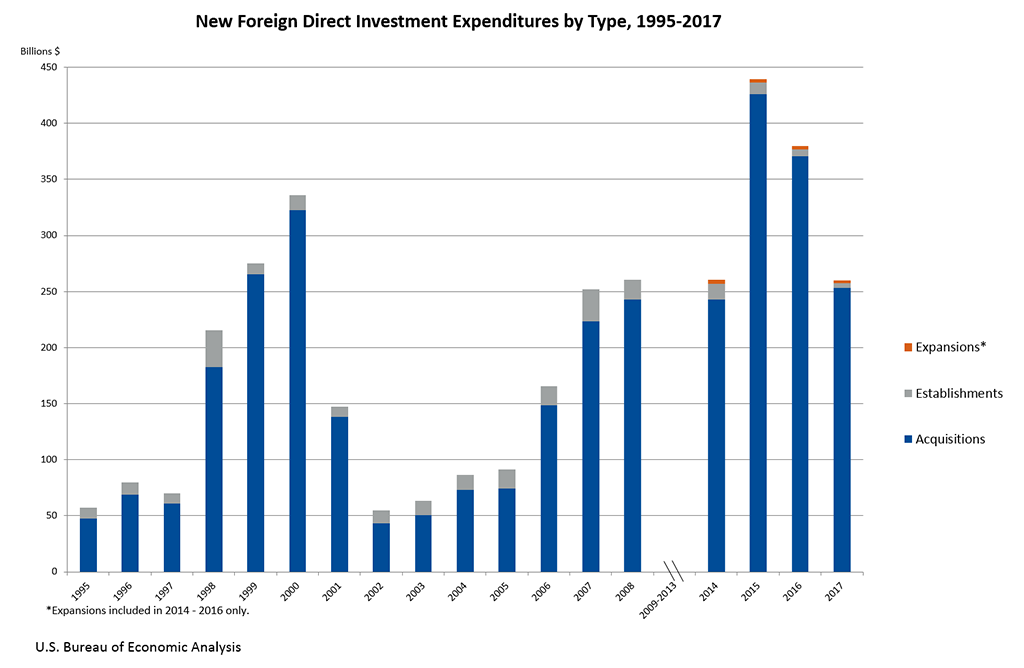

Source: BEA (July 11, 2018).

Inbound FDI has decreased measurably in 2017.

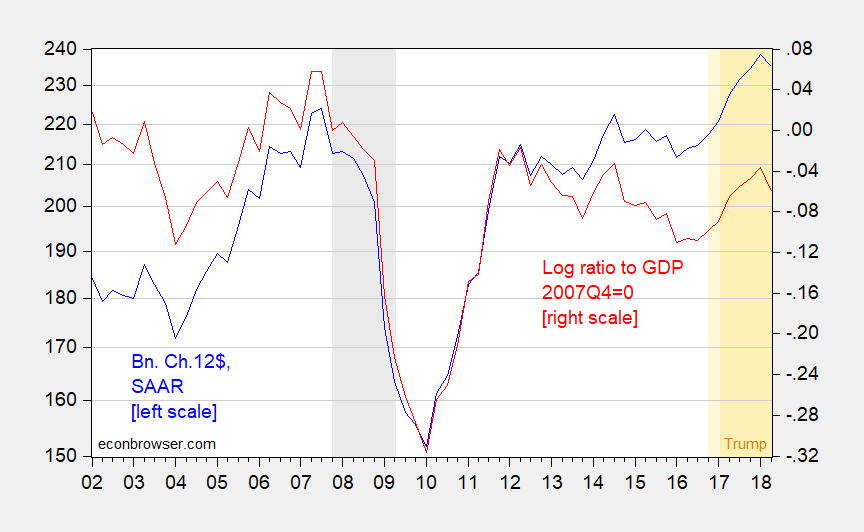

Figure 2: Investment in industrial equipment, in bn.2012$, SAAR (blue, left log scale), and log investment to GDP ratio, normalized to 2007Q4=0 (red, right scale). NBER defined recession dates shaded gray. Source: 2018Q2 advance GDP release, NBER, and author’s calculations.

Investment in industrial equipment turned down in 2018Q2 by a remarkable 5.6% (q/q annualized rate). This number is preliminary, but as of now, this is a surprising outcome given the booming economy.

OMG. Was the quoting of a Mercatus paper meant to be facetious?? Or please tell me Krol is the single good apple sitting amongst about 50 rotten ones??

Here’s some relevant info:

https://www.google.com/amp/s/www.cnbc.com/amp/2018/07/16/industrial-production-june.html

I suspect, most trade disputes, perhaps with the exception of China, will be settled by the end of the year, which will result in improved conditions to facilitate U.S. exports.

Conservative economist John Cochrane must have read your BS about this and he has made a mockery of it:

https://johnhcochrane.blogspot.com/2018/07/trade-war-1914.html

I noted this piece yesterday insisting that you read it before your next Trump cheerleading. Clearly you did not. So read it as he has made you look like a complete fool.

That’s a lot of information for PT to digest. I did notice one of the commenters referred to Cochrane’s “ignorance” on the subject. Always good when the know-it-alls feel it’s their duty to inform a respected economist of his lack of knowledge. How DID he ever get to Stanford and the Hoover Institute anyway?

Cochrane is decent at some things but his international economics is a bit naive as it is free trade is all good. Of course Cochrane’s limited knowledge of international economics is still about a 1 billion times greater than the total lack of knowledge we get from PeakStupidity.

Pgl, you’re in no position to judge real economists.

I passed the comp exams in International Trade.

You call others stupid. Yet, you make the most ignorant comments I’ve ever heard about economics.

At least, noneconomist, as the name shows, is honest.

passing the comp exams is really meaningless if you cannot complete the phd program.

I heard, China’s tariffs have been targeting Trump districts to turn the House to the Democrats, because the commies believe that will strengthen their negotiating position.

So, China may not settle any trade disputes, till after November.

China will cave. China will not cave. Excuse me but I think there are multiple Peak Traders post here. Talk about gaslighting!

A virtuous cycle of consumption-employment, where consumption generates employment and employment generates consumption, will eventually raise real wages.

There remains too much slack in the economy, reflected in weak employment growth, after the sharp downturn with huge job losses. After nine nine years of expanding, we haven’t closed the output gap, although there has been substantial destruction of potential output from the slow “recovery.”

Seriously? Your latest is the most naive form of Keynesian economics ever. Not even Keynes would find this compelling. Hey Peaky – the moment you ignore the full employment constraint is the moment you fall off the cliff with Gerald Friedman.

I know this is off topic, but it is humorous. For those of you who enjoy Wiley Miller: https://www.gocomics.com/nonsequitur/2018/08/02

Trade policy is undoubtedly uncertain, and one senses it is beginning to take a toll on Trump among his own supporters in the heartland (as did the Surrender Summit).

2017 FDI levels were unexceptional in dollar terms. I would note that almost all these are acquisitions, and it’s not clear to me how this helps the economy net, ie, those acquisitions free up capital for presumably US investors, but they are effectively a wash in terms of economic activity, at least in the short run.

Inbound FDI as a percent of GDP is about average for post-recession period. It collapsed under Obama, almost certainly related to the collapse of oil prices and the related surge in the US exchange rate, ie, investing in the US became less attractive priced in foreign currency. That effect has been fading, but the Q1 data is no worse than average for the Obama administration.

So, policy uncertainty is real, but to date, it’s impact has not moved FDI out of historical ranges, either in dollar terms or as a percent of GDP.

That could change, of course.

Menzie

Your chart goes back 16 years, so I assume that it is true that absolute industrial investment is at an all time high (blue line). In a previous comment Bruce Hall mentioned that much of the huge and surprising revision of GDP growth in 2012 was industrial investment that was missed for for several years. Is it common to miss such large investments? What confidence is there in current investment measures? Are you confident in the present reading?

Ed

Ed Hanson: I believe Bruce Hall is referring to a different category (computing and communications equipment) rather than industrial equipment.

Menzie

So you agree that industrial investment spending in absolute terms is at its highest in history. And you have confidence in the present numbers and will not see large revisions. So, do you really believe that investment will always rise until the government does something to stop the rise? In other words, all those quarterly drops in the past are government created.

Ed

P.S. Interesting that statistics have to be separated in so many categories.

Ed Hanson: I actually don’t know, partly because I’m not sure what “industrial investment” is. There is total nonresidential fixed investment…

I will say that it’s likely gross investment is at a high in real dollar terms. Whether it’s at a maximum in net terms, we probably won’t know for a while. And in terms of net investment to GDP, I doubt it. For discussion of net vs. gross, see this post. You commented on the post, so you should remember that distinction.

“So you agree that industrial investment spending in absolute terms is at its highest in history.”

It might be nice if you provided a source for this claim/ Oh wait – BEA does not measure “industrial investment” as it is a term you made up. Even if it did, a rise in nominal spending is not the same thing as an increase in real spending. Have you not learn even that yet?

Anyone else noticed the writing over at FT Alphaville has really dropped in quality recently?? Their most recent is about an NYC taxi company (“scintillating” stuff in the age of Uber and Lyft) which seems to only be an excuse to put a photo in the link of Niki Minaj in a push-up bra. Great job guys!!! Hey FT, how about about letting the summer interns stick to fetching the coffee and get some REAL financial journalists posting.

Found this over on Mark Thoma’s hangout. Related to our recent GDP rancor (or rather my strong disbelief in the most recent BEA number of 4.1%)

https://www.moneyandbanking.com/commentary/2018/7/29/gdp-one-size-no-longer-fits-all

Don't want to be misunderstood here, GDP is still obviously very much an important number. But the discussion is still interesting.

Moses Herzog: Better to read the symposium on measurement, in the Journal of Economic Perspectives (2017).

@ Menzie

Will do. I appreciate it.

@ Menzie

I plan on reading the entiremeasurement symposium journal, but reading the papers directly related to GDP first. Reading Feldstein the very first. I see some points on some things that is changing my view somewhat (meaning the way I am looking at it, not my feeling on the 4.1%), but even accounting for one of his major points, I still don’t see a 4.1% number being within the realm of realism. I’ll admit to being stubborn sometimes in admitting I’m wrong, but it gets down to this–even if they had announced 3.5% I would have said the GDP number was a load of crap. The only thing that could even come near to swaying me is the jump in equities since November ’16—and even that doesn’t sell me. So you know, I see it as at least a 0.6% gap from anything even near to reality.

The best analogy I can make on what this measurement symposium journal reading is doing for me (and I do greatly appreciate you providing the link and material)— it’s like looking at a partly cloudy sky, there’s clouds covering a lot of the sky, but I know it’s blue right??? Because the measurement symposium journal reading many of those clouds are rolling away and I can see almost all the blue sky right??—>> but it’s still colored blue. That’s how I view the journal reading thus far.

https://www.cnbc.com/2018/08/02/the-trump-administration-is-headed-for-a-gigantic-debt-headache.html

trillion dollar deficits as far as the eye can see. and no evidence the tax cuts are going to pay for anything. revenue down compared to last year. our miracle gdp growth appears to be debt fueled. trump is mortgaging the future to try and buy a victory in the midterms. he learned some lessons from st reagan afterall.

@ baffling

5-star comment there. Right out of Ronald Reagan’s “destroy the future to take curtain calls applause now” playbook. Zero consideration of how that affects thousands/millions of lives, nevermind an unknown emotion to either Reagan or trump known as empathy.

Look at the time periods where the debt number (as percent of GDP) is drastically rising in the non-recessionary (white) parts of the graph. The numbers clearly show which party does the gabbing about debt, and which party actually considers the debt when they are implementing policy.

https://fred.stlouisfed.org/series/GFDEGDQ188S

But Apple’s market valuation just hit $1 trillion. Hey let’s tax that at 100%!

pgl,

I think something like that was tried in Venezuela with the oil industry. They called it “nationalization”. That really worked out well, too.

Well, they actually called it saving the patrimony – the core concept that the resources of a country are the birthright of the citizenry, and that dates back in Venezuela’s history for many decades. It’s the same cultural philosophy that led to Pemex being formed back in 1938.

On a related note what I do find interesting is how conveniently folk overlook the fact the largest oil producer in the world is Saudi Aramco, a State owned company, along with other small fry like Kuwait Petroleum, National Iranian, et al.

Obvious major failures, right?

Bruce must not realize that nations like Norway tax oil profits at a 74% rate.

I think, Bruce was implying corruption, incompetence, inefficiency, etc..

It may not seem state-owned oil is failing when a country’s oil production per capita is high:

http://www.nationmaster.com/country-info/stats/Energy/Oil/Production/Per-capita

Also, it should be noted, it’s a lot cheaper to extract oil in the Middle East than in most countries.

ARAMCO is owned by the state. And its market value is estimated at $2 trillion.

“I think, Bruce was implying corruption, incompetence, inefficiency, etc..”

No PeakStupidity. All he said was nationalization. Not all nationalizations mean “corruption, incompetence, inefficiency, etc..”

Of course your boy (Trump) is the poster child for corruption and incompetence!

Bruce Hall In general, the problem with nationalized industries isn’t that they produce too little, but that they tend to produce more than is economically efficient.

As to taxing oil profits, it’s important to distinguish how much of the revenue above costs is what economists call “profit” versus how much is what economists call “rent.” Profits are the return to capital, so this would be income earned due to oil wells, oil exploration, management, etc. That portion of the revenue from oil should be taxed at the normal corporate tax rate that we apply to returns to capital. But some of the oil revenues are unearned rent that are due to the natural productivity of the well. Rent is a gift of nature and is not due to any human effort. There is human effort in finding the well, but that’s what should be taxed as profit. Rent on the other hand is unearned income, so taxing rent at 100% does not effect the productivity of the well. Now, how much of the oil revenue should be attributed to profits on earned income and how much should be attributed to unearned rent is tricky to say the least. But it’s useful to keep the conceptual distinction in mind. One way to keep things straight is to go back to the old Physiocrat model that first introduced the distinction in agriculture. Take two plots of land. One earns 10 bushels of corn per acre and the other earns 12 bushels per acre. The farmer that owns the first plot earns a profit on the capital he has to use in order to yield those 10 bushels per acre. The second farmer earns a comparable profit on the first 10 bushels, but the last two bushels just happen because of the relative fertility of the soil and is therefore unearned. The Quesnay and Physiocrat argument was that the second farmer’s two bushels should be taxed at a higher rate than the first 10 bushels. But even though the conceptual difference between profits and rent isn’t all that difficult to comprehend, the practical matter of applying that difference is another thing entirely. But the main point is that taxing rents at 100% should not necessarily reduce output if a government can correctly distinguish profit and rent…and that’s a big if.

this is a nice example. makes you consider how much “rent” is given away to big oil companies at the expense of small oil companies and the citizens in general.

2slug, Yeah, that’s the theory….

2slug, that’s the theory….

“While the Trump administration has said that economic growth would make up for shortfalls from tax cuts and spending increases, the early results do not bear that out.”

Ah but the Trump cheerleaders will mine the data the way the Laugher crowd did back in the 1980’s. So much real data to manipulate in the cause for Dooh Nibor!

I am interested in the delineation between FDI and gross transfers and capital repatriation, including into USTs. How is this appraised in the models?

C

China is dropping the tariff hammer:

https://money.cnn.com/2018/08/03/news/economy/china-us-tariffs-retaliation/index.html

Real exports accounted for almost 30% of the 4.1% growth rate for 2nd Q real GDP. But that data only had one months trade data.

June real trade data was released by Census this morning and the real trade deficit rose from 7.5 B (2012 $) in May to 7.9 B ( 2012 $) in June.

This essentially moved the trade balance back to where it was at the end of the first quarter. So trades contribution to the 4.1% estimate for2nd Q growth is quite likely to be revised down.

I’m trying to reconcile what BEA says about exports versus what Census says. The former suggests a jump in exports in 2018QII as well all now but I don’t see that in the Census data.

Always keep in mind that the trade balance is the difference between two very large and noisy data sets. So very small changes in either exports or imports can generate very large changes in the trade balance.

I focus on the real trade deficit and the monthly Census data shows a very sharp drop in late 2017 and a rebound in the first and second quarters of 2018.