…using plain vanilla 10yr-3mo probit regression, over 1986M01-2019M08 period, using data shown below in Figure 1 [corrections to data, update results 9/5]

Figure 1: Treasury 10yr-3mo spread (blue) in %. NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, Treasury, NBER, and author’s calculations.

As noted in this post, based on the first half of August, the probability of recession in August 2020 was 47%. Using the entire August data, I obtain the following regression estimates:

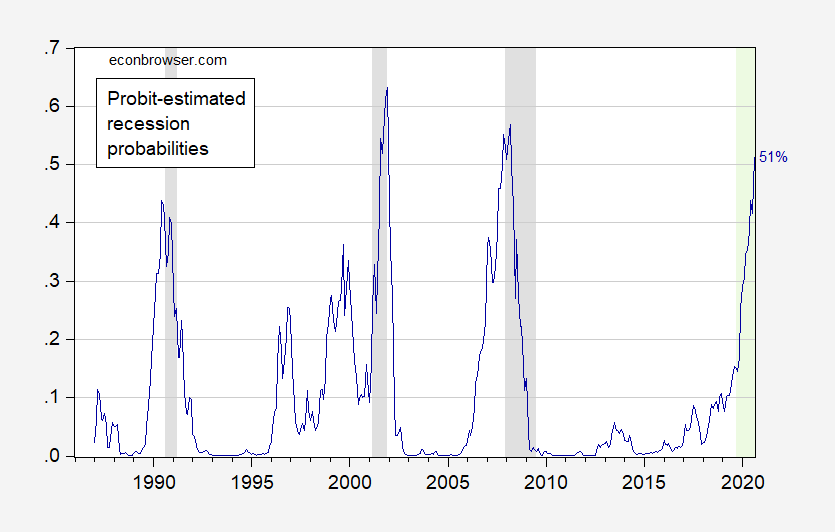

Prob(recessiont+12) = -0.329 – 0.869 spreadt + ut+12

Prob(recessiont+12) = -0.329 – 0.895 spreadt + ut+12

McFadden R2 = 0.300.29, NObs = 392. Coefficients significant at 5% msl bold. The spread is in percentage points.

Here are the predicted probabilities:

Figure 2: 12 month ahead probability from probit regression on 10yr-3mo spread, (teal). NBER defined recession dates shaded gray. Forecast period shaded light green. [Probability using correction 1990M07 to be no-recession, 9/5] Source. NBER and author’s calculations.

Should one deliver a recession call? That would depend on the threshold. Over the last three recessions, a 40% threshold would catch all three recessions, and yield no false positives. 49% 51% > 40%.

Obviously, if one believes this time is different — so one should use a term premium adjusted spread — the implied probability of recession would be lower (as demonstrated in this post).

I don’t see a call from Bill McBride yet. So, we aren’t in a recession just yet. All the indicators of a coming slowdown are there – RV sales, construction, the stock market, manufacturing, interest rates. What am I missing? As far as I’m concerned, 49% that it will hit in August 2020 means there’s a 26% chance it will hit in July 2020 and a 25% chance it will hit in September 2020.

A question that I have is what to make of ongoing consumer spending. If wages and hours aren’t growing enough to support spending growth, it’s going to have an impact eventually. If we see a lot of consumer spending the fourth quarter of this year, does it mean that the spending will come to a screeching halt in the first quarter of 2020 or will it mean that things won’t be so bad? I don’t know the answer because I haven’t thought about it enough to have the historic pattern in my head.

Willie: Recall, when I refer to the yield curve, I’m doing a prospective assessment. If one is looking at reported indicators (like GDP, industrial production), that is typically a retrospective (or at best “real time”) assessment.

Understood. Replying like a garbled wise acre didn’t come across too well. Ah, well. Apparently I do clarity and humor as well as I do numbers.

Being a little more serious, the article’s analysis lines up with what my non-technical analysis concludes. I don’t expect a technical recession until mid-2020 sometime. The more serious part of my comment was the question. I don’t know if a healthy fourth quarter of consumer spending is a good sign or a bad sign if the economy is stagnant or faltering. If people overspend for the holidays, it makes for good retail results, but it means reduced or negative growth in 2020. That, combined with the effects of tariffs that are due to kick in about then, could push the economy into recession before the middle of 2020. I don’t think there’s a whole lot of chance of making it to the end of 2020 without noticeable slowing.

my best guess is that the recession will hit full speed next summer. we already see a slowdown around the globe. trump has damaged our own economy and began losing steam from that “weak” recovery peak trader loved to gloat about. why do i say next summer then? in late spring, china will ramp up their tariffs and lower their currency, in an unveiled attempt to influence our elections and make trump a one term president. at that point, trump will be powerless to stop china or fix the recession. after the election, china will retreat to a neutral position until more rational actors move into the white house. this is why trump is trying to pressure them into a deal now. unfortunately he has backed himself into very weak corner, and china senses time is on their side. chinese leadership can longer withstand a downturn than trump and his next election. to further exacerbate the problems, trump is forcing china to modernize its economy into a more domestic consumption engine. this is exactly the time when us firms need to be inside of china, establishing their brand. and the trump approach is ensuring that our companies will remain outside of what will become the fastest growing consumer driven economy for another decade. and yet trump and his minions call this winning….for china i guess.

That assumes China is a rational actor. And, that seems to be a pretty good assumption. What I find interesting is that the WH is now saying that tariffs are going to hit consumer goods starting right about now. They aren’t going to wait until after the holiday retail season. So, there’s a reason to think a downturn, whether it’s a technical recession or not, will hit sooner rather than later.

I don’t recall where the quote came from, but somebody, somewhere noted that the next recession will happen because of a blunder by the fed or the administration. I’m not completely sold on that idea, since there is such a thing as the business cycle. But, with that in mind, we are watching an administration blunder unfold. The administration won’t back down if they are goaded by the idea that backing down to preserve the holiday shopping season is a sign of weakness of any kind. The current administration is not a rational actor. The Chinese and everyone else understands this by now and have the ability to use that knowledge to their benefit.

Buckle up for a bumpy 2020 is my take on things.

the latest news from china seems to be optimistic about a resolution. the question becomes, what will china get in return for opening up its markets to the us? i don’t think they will accept the elimination of tariffs, as those were instituted to cause the trade war. so the us will need to give up something else, probably something that has not been discussed in the media. not sure what that will be, but it is interesting. although i have called a recession next year due to escalation by china prior to the elections, i would be happy as can be if we can avoid it altogether. on the domestic front, ending the trade war and “winning” may not be enough to reelect trump anyways.

i was last in china about 6 years ago. beijing very much impressed me then. just spoke with some folks who traveled with me back then, and are visiting beijing again for the first time in 6 years. they say if i was impressed then, i would be totally amazed now. the city has continued to grow. some new growth areas then (think empty condo buildings in a field) are now fully functioning communities with shops, eateries, work and lots of people. those “ghost” cities you used to hear about may be in third tier, but certainly not in first tier cities.

what seems to have amazed these visitors the most is the pervasive use of technology in the city. a smartphone is a MUST. and they have effectively tarnished the apple brand so that most folks no longer want to buy the iPhone-it seems to be national pride. but the phone is used for everything, especially electronic purchasing. you order from a restaurant with the phone. Amazon style delivery of product is advanced. waiting lines at most museums, etc has been virtually eliminated with phone reservations taking its place-much more efficient for the people. the shopping is even more extravagant.

it seems to me the chinese economy is continuing to develop its domestic consumerism. as time moves on, this will place trump’s trade approach into an increasingly weaker position. he needs to cut a deal soon, before he loses his economic advantage. he does not have the ability to negotiate out of a weak hand-filing bankruptcy is not an option in trade negotiations.

Didn’t you read the title? “Estimated Probability of Recession in August 2020”. Dude – it is early September 2019 so sit back and wait.

August 2019 Manufacturing ISM Report On Business

https://www.instituteforsupplymanagement.org/ISMReport/MfgROB.cfm?SSO=1

New Orders, Production, and Employment Contracting

Supplier Deliveries Slowing at a Slower Rate; Backlog Contracting

I am not sure “this time is different” due to term premium. It might be different because the Fed is cutting rates.

But: the probability of recession is really the probability of a policy mistake either by the Fed or by Trump admin (or both, those are not mutually exclusive or even independent events). So, the probability is either 0% or 100% depending whom one asks.

Will it be live streamed?

My questions for Jim would be:

1. Yes, the yield curve is inverted, but credit to small business is reported to remain ample. Which matters more?

2. Can we have a recession without it being preceded by an oil shock?

3. Can trade and tariffs take the world into recession?

4. Is China big enough to lead the world into recession?

5. If so, explain the transmission mechanism.

6. How have demographics changed our thinking of the business cycle? To wit, I believe ordinary business cycles are caused by liquidity increasing faster than the fixed asset base in the expansionary phase of the business cycle. That is, the lag from ordering to delivery in fixed assets like housing or deepwater drilling rigs means that returns to these assets In dollars) and their values rise until fixed asset deliveries begin to catch up with demand. At that point, returns (in dollar terms) begin to fall, leading to depressed orders , lay offs and falling asset prices. In a world with low population growth and a declining workforce, this kind of cyclicality would appear to be muted, ie, liquidity never outruns the fixed asset base, because there just isn’t that much incremental demand (hence low interest rates). Agree or disagree? Is this time different, or not?

7. Bonus questions: What would a financial crisis in China look like? What is the transmission mechanism to RoW? In the case of heavily indebted Japan, would could be the impact on its fiscal situation?

I think the university officials could obviously livestream this if they wanted to. I strongly suspect the reason they don’t livestream these things is to encourage students to get out and interact with each other, “network”, and create an environment for learning. I was extremely anti-social in my college years, and I know I would have taken the stream option and sat in from of my computer monitor watching Professor Hamilton. I certainly empathize with these students lacking in social skills (because I was there myself, and know that internal struggle)—but I think “nudging” them to get out with their classmates is more healthy—not just career-wise but more emotionally healthy.

Professor Chinn,

While trying to tie-into your numbers, I seem to have some differences. I used FRED data updated on 9/4/2019 for the month-end series “T10Y3M”. I also used “USREC” as the recession indicator, which seems to agree with the NBER indicators. Are you using the “T10Y3M” series for the interest rate spread? I am not quibbling about the difference in probabilities or any output, just trying to tie-in.

Professor Chinn: Model Output Probability 49%

Prob(rec(t+12)) = -0.329 – 0.869 spreadt + u t+12

McFadden R2 = 0.29

NObs= 392

Coefficients significant at 5% msl bold

Using T10Y3M(ave) : Model Output Probability 46%

Prob(rec(t+12)) = -0.402 – 0.826 spreadt + u t+12

McFadden R2 = 0.28

NObs = 392

Coefficients significant at 1% msl bold

FRED series USREC used for recession indicator

Obs with Dep= 0 = 358

Obs with Dep = 1 = 34

Using T10Y3M(EOM): Model Output Probability 46%

Prob(rec(t+12)) = -0.464 -0.765 spreadt + u t+12

McFadden R2 = 0.25

Nobs = 392

Coefficients significant at 1% msl bold

FRED series USREC used for recession indicator

Obs with Dep= 0 = 358

Obs with Dep = 1 = 34

AS: I hand-entered NBER recession dates, using peak-trough months inclusive as 1’s. Don’t know if that matches USREC from FRED. Sometimes I use Treasury 3 month secondary market for long spanned data, but for this short span, I used 3 month constant maturity. I suspect treatment of lags and/or recession indicator probably drives diference of results.

AS A ran the probit regression a few days ago and got the same result as your first equation. I also used the “USREC” and “T10Y3M” files from FRED.

2Slugs,

Thanks for the comment. Nice to know I am not completely on another planet.

AS

Oops. My mistake. This is the regression I get when using USREC and T10Y3M:

coefficient std. error z p-value

——————————————————-

const −0.290376 0.150175 −1.934 0.0532 *

T10Y3MM −0.894773 0.160280 −5.583 2.37e-08 ***

Mean dependent var 0.094388 S.D. dependent var 0.292741

McFadden R-squared 0.304504 Adjusted R-squared 0.288181

Log-likelihood −85.21835 Akaike criterion 174.4367

Schwarz criterion 182.3792 Hannan-Quinn 177.5845

Number of cases ‘correctly predicted’ = 361 (92.1%)

f(beta’x) at mean of independent vars = 0.069

Likelihood ratio test: Chi-square(1) = 74.621 [0.0000]

Predicted

0 1

Actual 0 353 2

1 29 8

2Slugs,

From my latest understanding, it appears that we need to use USRECM in order to assign a “1” to peak tthrough trough.

How about running ” USRECM(+12) c T10Y3M(ave)” to see how we compare?

When I compared the NBER dates of peak through trough with USRECM, the dates agreed, but the dates did not agree with USREC as I had earlier thought.

AS Here’s what I get when running USRECM and T10Y3MM:

Dependent variable: USRECM

QML standard errors

coefficient std. error z p-value

——————————————————-

const −0.290376 0.150175 −1.934 0.0532 *

T10Y3MM −0.894773 0.160280 −5.583 2.37e-08 ***

Mean dependent var 0.094388 S.D. dependent var 0.292741

McFadden R-squared 0.304504 Adjusted R-squared 0.288181

Log-likelihood −85.21835 Akaike criterion 174.4367

Schwarz criterion 182.3792 Hannan-Quinn 177.5845

Number of cases ‘correctly predicted’ = 361 (92.1%)

f(beta’x) at mean of independent vars = 0.069

Likelihood ratio test: Chi-square(1) = 74.621 [0.0000]

Predicted

0 1

Actual 0 353 2

1 29 8

Test for normality of residual –

Null hypothesis: error is normally distributed

Test statistic: Chi-square(2) = 9.97968

with p-value = 0.00680676

RECESSION PROB IN ONE YEAR: 51%

And here is what I get when running USREC and T10Y3MM:

Dependent variable: USREC

QML standard errors

coefficient std. error z p-value

——————————————————-

const −0.402766 0.150927 −2.669 0.0076 ***

T10Y3MM −0.825076 0.151767 −5.436 5.43e-08 ***

Mean dependent var 0.086735 S.D. dependent var 0.281806

McFadden R-squared 0.275766 Adjusted R-squared 0.258466

Log-likelihood −83.72694 Akaike criterion 171.4539

Schwarz criterion 179.3964 Hannan-Quinn 174.6017

Number of cases ‘correctly predicted’ = 360 (91.8%)

f(beta’x) at mean of independent vars = 0.071

Likelihood ratio test: Chi-square(1) = 63.7613 [0.0000]

Predicted

0 1

Actual 0 357 1

1 31 3

Test for normality of residual –

Null hypothesis: error is normally distributed

Test statistic: Chi-square(2) = 7.32283

with p-value = 0.0256961

RECESSION PROB IN ONE YEAR: 46%

Lesson to be learned: Too damn many different versions of recession start/stop dates.

AS: I downloaded USRECM, reran the regression. Turns out I had an error in my RECESSION dummy, coding 1990M07 as recession month. If I re-run using USRECM and GS10 minus GS3M I get same results as you, but coefficient on spread is -0.895. Turns out the series on FRED for the term spread is slightly different from mechanically calculating the spread using the average of DGS10 and average of DGS3M…I can replicate your second set of regressions if I use USRECM and T10Y3M.

Professor Chinn,

Thank you! I go into “tilt mode” when the model I compute is different from yours.

I assume the “second set of equations” refers to the model I submitted at 1:35 PM on 9/5.

AS: Yes, that is correct. I haven’t tried to replicate your first set of regression results.

Just a random thought here while checking in, Funny to watch Boris Johnson fall flat on his face after trying to play an empty poker hand. That poker hand was so weak poor Boris couldn’t even manage to bluff the table on two raises. Apparently Boris thought British Parliament is as dumb-A$$ as America’s Republican Senate. Not enough Kentucky frog-boys with limp shlangs to play that one out. Hope Boris can get those dark bruises off his face from the London pavement, poor guy.

Not that I’m against Brexit mind you, just funny to watch a disingenuous twat make a fool of himself. In these MAGA times, one has to get a few chuckles out of the spectator sports when the rare fun event arises.

I might add, at the risk of coming across as a very low-class and callous individual (as Professor Chinn knows all too well, a risk I’m willing to take in the name of self-entertainment, and eh, my version of accuracy )—— Uuuuuuhh, if some economists had a little bit more macabre humor, they might have been “better able” to weather their pig not getting blue ribbon at the state fair. Just a passing thought for those who tie the joy of life to external measures in a world jam-packed with buffoons.

“Not that I’m against Brexit mind you, just funny to watch a disingenuous twat make a fool of himself. ”

But that is a statement with a contradiction in itself: The cause of Johnson’s weak hand is that brexit has no real advantages. It became a cult which could not be sold any longer as rational.

Or from a different POV: It was easy to sell brexit at the beginning as people could be fooled into a belief that the EU-27 would damage its core principles in order to please (stupid) brexiters. Add the fact that there was no clear vote for one brexit, but various forms of brexit were conveniently pooled to look strong (-> “will of the people”) at the beginning. It was always clear that a UK government pays a high price when these lies and tactics collide with reality.

the brexit movement was supported by russian trolling as a means to weekend great britain and europe. and it was successful. the russians continue to wager political war around the globe, and will attempt to once again impact the next election for their soviet candidate trump. moscow mitch seems willing to permit this, as long as it is the communist republican party that putin is supporting. reagan must be rolling over in his grave at how his republican party welcomed putin and the russians.

Professor Chinn,

If my hand entries are correct, the NBER peak to trough dates seem to agree with the FRED series: USRECM.

The resultant equation is still a bit different.

“I suspect treatment of lags and/or recession indicator probably drives difference of results.” I am not certain what is meant by “treatment of lags”.

For the probit model I used :

Recession (+12) c T10Y3M

Using T10Y3M(Ave): Model Output Probability 51%

Prob(rec(t+12)) = – 0.290 – 0.896 spreadt + u t+12

McFadden R2 = 0.30

Nobs = 392

Coefficients are significant at 5% msl for “C” and at better than 1% for T10Y3M.

FRED series USRECM used for recession indicator agreeing with NBER dates.

Obs with Dep= 0 = 355

Obs with Dep = 1 = 37

Question #8 to add to Steve Kopits’ list is:

Can the Euro area, with or without a Brexit settlement in the next 6 months, lead the world into recession, and bring China along because most of China’s value add exports are to the Euro zone? Extra credit if your scenario can correctly forecast whether the $17 trillion amount of bonds with negative interest rates (mostly in Europe) goes up or down.

I’m still waiting on “Princeton”Kopits’ prediction that Chinese peasants (proletariate if you prefer) are going to tear of Xi Jinping’s limbs to come to fruition. I know “Princeton”Kopits’ had given himself the allowance that this could happen anytime between now and the year 5555AD. But also he hinted it could happen in our lifetime, so we can’t ask “Princeton”Kopits’ to be thatdefinitive or it might be implied he’s actually said something useful to anyone.

The probability went from 49% to 51%?! I guess the tax attorneys of the world are declaring a 2020 recession “more likely than not”. Now what are the chances of seeing Trump’s tax returns?

Lower than the likelihood of a recession. No doubt he’s hiding things. Probably not criminal activity, just attempted criminal activity and failure to make any money legitimately or criminally.

interesting article in the financial times, talking about how capitalism is changing (or should change) from the primacy of shareholder value to valuing all stakeholders in a company, including the workers and community in which we work. seems as though capitalism went off the rails in the 60’s and 70’s, and conservatives in the 80’s successfully implemented policy to reinforce the “rights” of a corporation to make money any way possible. i guess the movie “wall street” and “greed is good” came out of the 80’s for a reason.

https://www.ft.com/content/b35342fe-cda4-11e9-99a4-b5ded7a7fe3f