The video of Jim Hamilton’s inaugural Juli Plant Grainger Institute lecture at the University of Wisconsin-Madison Economics is now up!

Click here for YouTube video.

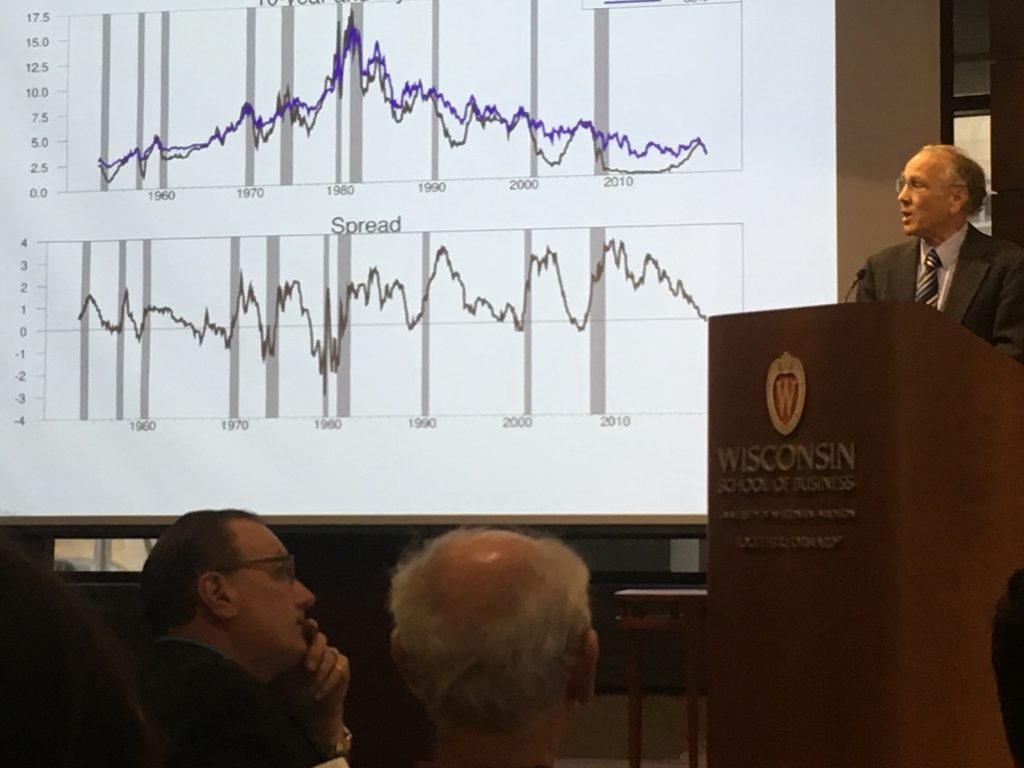

Must see for anybody who is serious about critically reading the tea leaves regarding an incipient recession (Spoiler: As of 9/11, he was sceptical a recession had begun). Interesting conjecture about using holding period returns on Treasury securities of different maturities to isolate a expectations hypothesis of term structure component (my reading).

(Aside: for conventional wisdom, see my Econ 435 notes for Econ on EHTS/yield curve/recession prediction)

Thanks for the heads up. Bet it’s a good one. Will put it somewhere at the top of my “watch this soon” list.

GREAT lecture by Professor Hamilton, I just watched it all. I can’t decide if Hamilton’s lecture is quite as good as Edward Leamer’s on Youtube. I don’t know, he’s got some pretty tough competition there, but a great lecture nonetheless.

Also impressed with the WU students attending. Seemed like a courteous and thoughtful group. We take cheap shots at the younger generation all the time, but as the kids attending this lecture proved—there’s a lot of good/intelligent youngsters out there. Let’s recognize their efforts and the difficulties they face.

“UW students,” not “WU students”

Professor Hamilton,

Thank you!

Any chance of getting an update from Michael Dueker related to the Econbrowser post in February 2008?

https://econbrowser.com/archives/2008/02/predicting_rece

Should have thanked both Professor Chinn and Professor Hamilton.

Apologies.

Excellent talk, very patiently presented.

“Prediction is very difficult, especially if it is about the future.” Attributed to Niels Bohr. But in his case, he wasn’t trying to be funny. As economists know, prediction does not necessarily involve the future. For example, I can use a regression to predict 1980 income based on 1980 consumption. Forecasting, on the other hand, necessarily involves the future.

Just to emphasize the difficulty in forecasting. Ed Leamer (an economist for whom I have great respect and who engages actively in forecasting) missed entirely the great recession, even after the bust in housing prices.

@ Professor Hamilton

I had heard Menzie’s thoughts on Brainard’s Detroit comments before, and I think he also agreed these comments were good and worthy of highlighting (though I think I was a little more vociferous about them being above-average in insightfulness). I copy/pasted my prior comment with Brainard’s quote in bold print, and was wondering if Professor Hamilton had any thoughts on it, or if Professor Hamilton thought is was “typical federal reserve boilerplate”???

When we look at this yield curve inversion stuff in the last roughly year, my mind keeps returning again and again and again to Lael Brainard’s very perceptive, keen, and prescient comments in a public speech she made. She is a very highly intelligent woman, and I believe these are quite conceivably the best comments that have been made on the yield curve (with the possible exceptions of Menzie’s general observations over that same time period) in the entire last year.

“As we try to assess the implications of this flattening of the yield curve, it is important to take into account the very low level of the current 10-year yield by historical standards. For the 20 years before the crisis, the 10-year Treasury yield averaged about 6‑1/4 percent, compared with recent readings around 3 percent. One reason the 10-year Treasury yield may be unusually low is that market expectations of interest rates in the longer run may be unusually low. A second reason may be that the term premium–the extra compensation an investor would demand for investing in a 10-year bond rather than rolling over a shorter-dated instrument repeatedly over a 10-year period–has fallen to levels that are very low by historical standards. According to one estimate from Federal Reserve Board staff, the term premium has tended to be slightly negative in recent years. By contrast, when the spread between the 10-year and 3-month Treasury yields was at its peak in early 2010, this measure of the term premium was close to 100 basis points.

Other things being equal, a smaller term premium will make the yield curve flatter by lowering the long end of the curve. With the term premium today very low by historical standards, this may temper somewhat the conclusions that we can draw from a pattern that we have seen historically in periods with a higher term premium. With a very low term premium, any given amount of monetary policy tightening will lead to an inversion sooner so that even a modest tightening that might not have led to an inversion in the past could do so today. ”

May I semi-humbly suggest, that when looking at the yield curve inversion (in the current 2019 context), and trying to draw any conclusion from the confounded mystery of inversion—people keep Brainard’s comments somewhere in their mind.

https://www.federalreserve.gov/newsevents/speech/brainard20180531a.htm

A reasonable comment.

We now have three presentations by headline economists — Ken Rogoff, John Williams and Jim Hamilton — that are noting declining yields without so much as a peep about the underlying causes.

Not one word about demographics in any of these presentations. Williams (in the previous post) notes that short term rates have fallen from about 4.5% to 2% without so much as a hint as to why this might be happening. And then he assures us that , notwithstanding this development, the Fed has plenty of firepower to handle the next recession, even though short rates are around 2% and the Fed normally cuts rates by 4-5% in a recession. WIlliams claims that another round of QE would do the trick (again, this is simply a bizarre assertion wrt the customary monetary policy toolkit in the pre-2007 economy) when in fact Jim’s analysis (see his comment, previous post) suggests that QE was associated with rising, not falling rates. We can therefore conclude that the does not have a full spectrum toolkit right now, if recessions are to be considered in the same light as they were pre-2007.

I have the same impression watching and reading these presentations as I do shopping at our local Stop ‘n Shop. The background music is all familiar, the greatest hits of the 1970s and 1980s. I know them all, they bring back great memories and I sing along with the lyrics. And this happens in store after store that I visit. And my kids, now in college, know all these songs — they are part of their standard canon. But I keep asking myself: Where are the songs of this generation? Where are their voices? Why are we still listening to songs from two generations ago?

I have the exact same reaction to these economics presentations. Truly, they are the greatest hits. Wonderful insights, great people, I can sing along with the graphs. But where are the modern interpretations? How can Williams say, oh rates have fallen from 4.5% to 2% and leave it at that? How can Jim say the term premium is negative because now people fear deflation more than inflation and leave it at that? Why? Why do people fear deflation? What has changed? Are we still in the Great Recession (the China Depression)? Unemployment just hit a 50 year low, so that doesn’t seem all that probable, does it? So what’s different? We need to hear some new songs, if not from new artists, at least from the superstars of our youth.

…the Fed does not…

A reasonable comment.

Do not forget, historically a negatively sloped yield curve is accompanied by rising short rates.

That is not happening this time. Recession may be due to rising short rates and the yield curve does not have anything to do with it.

Why aren’t we discussing this possibility?

Isn’t it kind of like saying “we know dark storm clouds overhead are connected to levies breaking, which is historically accompanied by rain”. The two things are pretty much married are they not?? By the time short term rates are rising you’re not getting much prognostication “lead time” are you??

A thought on whether inversion of the yield curve still implies recession if fears of inflation have shrunk and fears of deflation have grown….can we have deflation without recession? If the yield on a 10 year instrument falls below that on a one-year instrument, wouldn’t that still imply an expectation of recession? Granted, the same amount of inversion may be a weaker indicator if we expect recession to be accompanied by deflation, but still, the simple fact of inversion predicts an economic slowdown is coming. Stated another way, can growth ever simply stop without turning negative?