Today, we’re pleased to present a guest contribution written by Laurent Ferrara (SKEMA Business School and International Institute of Forecasters) and Capucine Nobletz (University Paris Nanterre).

In this post we assess contagion among government bond markets by focusing on the Covid-19 crisis period. Using the approach put forward by Diebold and Yilmaz (2014), we empirically show that the connectedness dramatically increased on international bond markets over the crisis period. More specifically, this global shock seems to discriminate between safe and risky countries, those latter seeing a large increase in sovereign spreads.

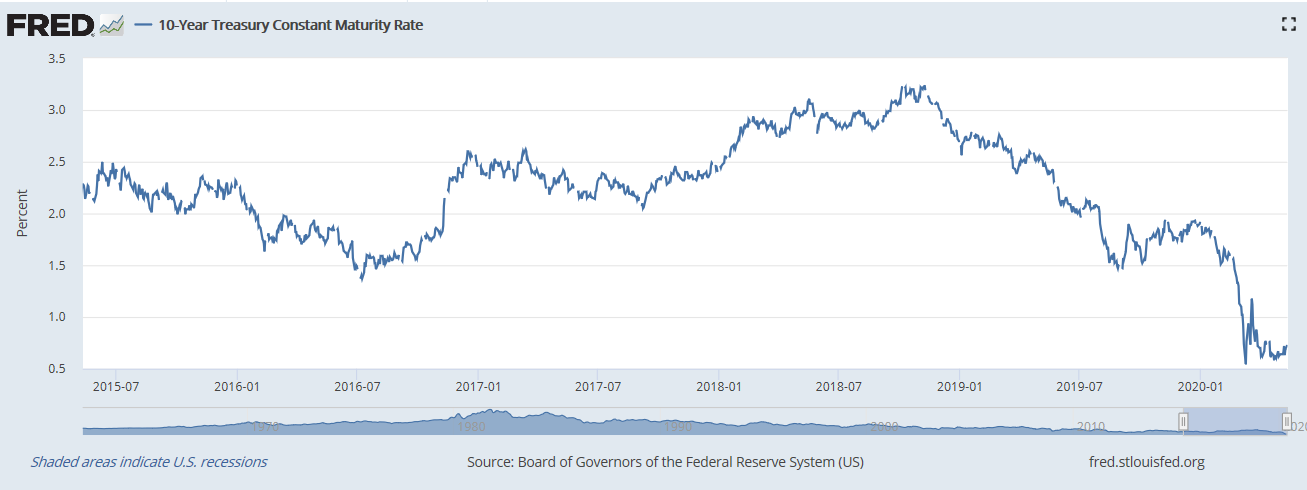

The Covid-19 global crisis generated a worldwide recession (see previous Econbrowser posts here, here and here), as well as abrupt movements on financial markets. For example, oil prices sharply dropped so that price of the May crude-oil futures contract closed on April 20 at negative $37.63 a barrel (see this Econbrowser post here). On the bond market, the 10-year US government bond yield went down from a level close to 2% end of December 2019 to levels between 0.6%-0.7%, in a flight-to-quality move (see Figure 1).

Figure 1. 10-year US government bond yield

Source: Fred database Federal Reserve Bank of St Louis. Last point May 11, 2020.

How to assess contagion dynamics on the global bond market?

In order to assess contagion on the global sovereign bond market, let’s consider daily 10-year government bond returns denominated in local currencies for a bunch of industrialized and emerging countries. The countries selected are: Brazil, China, South Africa for emerging economies and the United Kingdom (UK), the United States (USA) and Germany for advanced economies. The study period runs from January 03, 2006, to April 13, 2020, and all data are extracted from Thomson Reuters Datastream. To obtain time series with the same integration order, we use bond returns and not yields.

The methodology that we use to compute contagion within this system is the one developed by Diebold and Yilmaz in a series of papers in order to compute connectedness indexes. To this aim, we estimate a VAR (Vectorial AutoRegressive) model and compute the generalized forecast error variance. By decomposing this forecast error variance, we identify for each country the share of variance attributable to the different countries in the system. The “own variance share” is the share of variance due to the country itself (thus measuring the openness of the country). The “cross variance share” or “pairwise spillover” is the share of variance of a given country only due to other countries. Once the covariance matrix is computed, we can measure the total spillover index (‘TSI’), measuring the global connectedness of the system. In addition, we can measure the directional and the net spillover indexes. The directional spillovers are the government yield spillovers transmitted by a country to all other markets (‘TO’) and the government yield spillovers received by a country from all other markets (‘FROM’). The net spillover from a given country to others consists in the difference between the share of variance given to others (‘TO’) and the share of variance received from others (‘FROM’).

Network analysis of over the sample

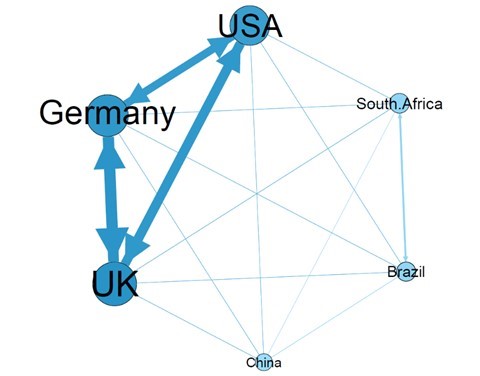

First, we study government bond market spillovers through a full-sample static analysis to get the average contagion behavior. Figure 2 is the network graph of the “cross variance share”. The size of the nodes represents the average pairwise connectedness; the larger the node, the more strongly the country’s bond market is connected to the other bond markets within the system. The link arrows indicate the pairwise connectedness “TO” and “FROM”. Their sizes are proportional to the percentage variance of the forecast errors they give or receive from other markets. We observe that there is a strong connectedness between the bond markets of the advanced economies. Those three markets represent the primary senders (“TO”) and receivers of shocks (“FROM”). The strongest interconnection is between Germany and the UK: about 25% of the forecast error variance of the UK (Germany) bond market is explained by a shock stemming from the German (UK) bond market. We also note that bond markets of emerging economies are, on average, only slightly affected by shocks from other markets. This result can be explained by the lower level of financial openness to foreign investors, particularly as regards the Chinese bond market. A similar result has been found for equity markets in emerging countries (see here).

Figure 2. Network graph

Source: Author’s computations

Dynamic analysis of contagion

In a second step, to account for the possible variation over time of our spillover indexes, we analyze these indexes in a dynamic rolling-sample analysis. In Figure 3, we observe significant evolutions in the degree of contagion across government bond markets. In particular, the degree of interconnectedness increases during economic or financial turmoil, as illustrated by the spikes during the Global Financial crisis and the Brexit uncertainty period in the wake of the June 2016 referendum. What is striking to observe is the sharp rise in contagion for the Covid-19 pandemic crisis at the end of the sample, reflecting thus a much higher connectedness within the global sovereign bond market over the recent period.

Figure 3. Evolution of contagion among the system

Source: Author’s computations

Conclusions

What are the main take-aways of this contagion analysis? First, the global bond market is in general mainly driven by connections between advanced economies. Second, every time there is an economic crisis, the contagion tends to increase. Third, the Covid-19 crisis reveals a very sharp increase in the degree of connectedness within the system, reflecting the fact that the emerging countries have been also impacted by this global shock (see data on Figure 4).

Overall, it seems that today investors discriminate between safe countries, for which government bond yields dropped and are likely to stay low, and riskier countries that have seen a jump in their sovereign bond yields. The consequences of this market discrimination might be crucial as regards public debt sustainability. Indeed, if some emerging economy governments have to increase their spending to fight the Covid-19 crisis, then they will have to borrow on markets at a much higher rate, leading to some future public debt issues. It is true that on average, the debt ratio is lower for emerging countries as a whole (see this IMF blog), but some countries, especially oil exporters, are likely to be at risk in upcoming months. Against this background, support from international institutions and international cooperation will have to step up.

Figure 4. 10-year government bond yields (in %)

Source:Datastream, daily data from January 03, 2006, to April 13, 2020.

This post written by Laurent Ferrara and Capucine Nobletz.

“On the bond market, the 10-year US government bond yield went down from a level close to 2% end of December 2019 to levels between 0.6%-0.7%, in a flight-to-quality move”

Corporate bonds rated BBB saw higher yields reflecting a rather dramatic increase in credit spreads.

https://fred.stlouisfed.org/series/DBAA

Do you know that quality spreads move in lock step with capacity utilization?

Sometimes spreads lead.

If we’re talking about debt instruments, I would like to see more discussion along these lines,

https://www.nakedcapitalism.com/2020/05/wall-streets-useful-idiot-financial-times-shills-for-clos-as-fed-hasnt-bailed-them-out.html

…… instead of discussion about debt instruments that were garbage to begin with.

What am I worried about contagion or “connectedness” of garbage paper?? If the instruments were properly capitalized and banks were properly capitalized then contagion or connectedness would be ameliorated. Would it be eliminated?? No, but it would be greatly ameliorated. If I have a very small classroom of children, let’s say 15 of them. None of them take showers for a month and none of then wash their hands after using the bathroom. Do I sit there worrying which one of them is going to touch the other one?? With all due respect to the researchers, and I do respect the efforts of their research and math, this appears to be the type of discussion we are having. And I include Diebold and Yilmaz in this, in case the researchers above think I’m picking on them in particular.

And before one of our poser/preeeners on this blog decides to pipe up, yes, I know there is a difference between bonds and CLOs and CDOs. The problem is it’s really getting harder to tell the difference in the quality and asset collateral backing of the paper. I think we should make this a discussion before worrying about which kid who didn’t take a shower is going to touch another kid that didn’t take a shower.

Interesting link. The chart that proceeds this discussion is something people should take a look at:

‘The viewer’s eye naturally goes to the top line, for the BB tranches the yields have risen the most. Those BB instruments are a mere 3-4% of the total value of the CLO market! They are rounding error. By contrast, the AAA tranches are yielding pretty much what they did in later 2019. Yes, they aren’t trading the same as other AAA instruments, but seasoned structured credit investors ought to know that these AAA creations can and often do trade down in crises, unlike Treasuries and government guaranteed credits. Moreover, eyeballing the charts, yields have improved since mid-late April, meaning investors are less edgy, when even then, Reuters reported that new CLO deals were getting done on reasonable terms.’

It shows how corporate bond yields spiked in late March but yea yields in April moderated. I have spent my spare time reading the intellectual garbage that emanates from transfer pricing practitioners at the Big 4 accounting firms and international tax law firms, which is particularly stupid when it comes on what is known as intercompany financing. I will not bore people with the sheer crap they write but people like CoRev are smarter than these arrogant morons. And corporate America pays big bucks for long winded stupidity because they think these clowns know something. Most of them could not pass an undergraduate money and banking course but they someone manage to get paid the big bucks. Then again Lawrence Kudlow is Trump’s chief economic adviser. Go figure!

I am one who thinks this paper looks pretty well done. Network analysis is now taken seriously by many involved in studying dynamics of inter-financial relations, and the basic econometrics here looks reasonable. Of course this may not explain everyting, but describing this as a “garbage” paper is unacceptable coming from somebody who has made so many comments here on bakikng and finance that have been themselves pure garbage.

@ Barkley Junior

If you weren’t so busy navel-gazing with the refuse of a brain infested with clumps of beta-amyloid, you’d know (as pgl EASILY figured out) that garbage paper was a reference to bonds and debt instruments in general, not what Ferrara’s and Nobletz’s paper. I am writing this for your sorry A$$, no one else’s, as I’m certain the authors and Menzie figured that out. This is why I don’t get Menzie’s sheltering you from my references to dementia, as which is more shameful??— someone in your field of learning not figuring that out, or giving you an “out” with the excuse of dementia. I would go with the latter if I were you Junior.

Moses Herzog: To the best of my recollection, I have not deleted any of your comments referencing dementia, except for one – coupled with misogyny – applied to Speaker Pelosi. I will note that I *know* what dementia looks like. I do not think it is something that is to be leveled at somebody without good cause.

@ Menzie

There’s nothing you said, that I can argue with, or say is false. I would only say this, in “defense” of myself, or a “rationalization”. Feel free to call it what you will—-

I would be very happy to “act like the adult” in any argument, if I wasn’t very well aware through multiple experiences where that gets one in life. Something like a run over mashed raccoon on West I-90.

And I want to add this–if you think Pelosi’s ice cream stunt on TV was acceptable behavior for a national level political figure at the outset of a severe recession—I advise you strongly never to run for political office.

Two women discussing Nancy Pelosi. I had no part in this conversation, and plead total innocence in sending them a script for their discussion:

https://soundcloud.com/katie-halper/running-against-debbie-wasserman-schultz-with-jen-perelman

https://twitter.com/kthalps/status/1261370485151019008

I advise jumping to roughly around the 9:55 mark which gets more to the meat of the discussion, and/or at the 24:40 mark is where they get more into Pelosi.

The Fed’s decision is likely to include the point about contagion which Naked Capitalism calls into question, as well as the broader issue of getting cash into the financial system to fund recovery when the time comes. The Fed probably knows what NC knows, but still may choose to offer rescue money.

This notion that risky debt performance is becoming more highly correlated around the globe fits with other research showing that equity performance is also more highly correlated now. The divergence between higher quality debt between advanced economies and others is hardly a surprise, but this time the Fed and her sisters are doing more than ever before to shore up credit in their economies, arguably making the divergence greater.

I am entertained by Naked Capitalism insisting the housing crisis was in reality a financial crisis while Dean Baker insists that the financial crisis was actually a housing crisis, with the loss of value and liquidity in the most widely held asset at the core of every other problem. False dichotomy, anyone?

Off topic but Biden was asked last night whether he “would pull a Gerald Ford” and pardon Trump. I love his answer:

https://talkingpointsmemo.com/news/biden-vows-to-not-pardon-trump-if-he-defeats-potus-i-guarantee-that-wont-happen

You’re counting your eggs, and women in rural America haven’t spoken on that one yet. It’s a kind of arrogance Hillary had that didn’t end well, which, again, is why I suppose your type jumps up and down when Pelosi tells you she got another “victory” handing out gifts to the opposing party’s lobbyists. Go on, get giddy, jump and spin around if you enjoy it.

Oh dear, denouncing both Hillary and Pelosi, Moses. Did you do anything for your mother for Mother’s Day, anyting at all (assuming she is still alive)?

The Lancet is a highly respected medical journal that was established in London 197 years ago. Here is their latest on COVID-19 in the U.S.

https://www.thelancet.com/journals/lancet/article/PIIS0140-6736(20)31140-5/fulltext

“The COVID-19 pandemic continues to worsen in the USA with 1·3 million cases and an estimated death toll of 80 684 as of May 12. States that were initially the hardest hit, such as New York and New Jersey, have decelerated the rate of infections and deaths after the implementation of 2 months of lockdown. However, the emergence of new outbreaks in Minnesota, where the stay-at-home order is set to lift in mid-May, and Iowa, which did not enact any restrictions on movement or commerce, has prompted pointed new questions about the inconsistent and incoherent national response to the COVID-19 crisis.

The US Centers for Disease Control and Prevention (CDC), the flagship agency for the nation’s public health, has seen its role minimised and become an ineffective and nominal adviser in the response to contain the spread of the virus. The strained relationship between the CDC and the federal government was further laid bare when, according to The Washington Post, Deborah Birx, the head of the US COVID-19 Task Force and a former director of the CDC’s Global HIV/AIDS Division, cast doubt on the CDC’s COVID-19 mortality and case data by reportedly saying: “There is nothing from the CDC that I can trust”. This is an unhelpful statement, but also a shocking indictment of an agency that was once regarded as the gold standard for global disease detection and control. How did an agency that was the first point of contact for many national health authorities facing a public health threat become so ill-prepared to protect the public’s health.”

It continues starting with the founding of the CDC in 1946 noting its great history until Donald Trump decided to undermine its mission. The close?

“The Trump administration’s further erosion of the CDC will harm global cooperation in science and public health, as it is trying to do by defunding WHO. A strong CDC is needed to respond to public health threats, both domestic and international, and to help prevent the next inevitable pandemic. Americans must put a president in the White House come January, 2021, who will understand that public health should not be guided by partisan politics.”4

A Biden endorsement?

i find it sadly ironic that the trump position is that obama left the cupboard bare for trump to respond. now trump has had over three years to restock that cupboard, and he has yet to do so. lets take for argument sake that obama did leave the cupboard bare. exactly when should trump have noticed this and fixed it? apparently, in trumps view he could go an entire election cycle and still believe it was obama’s fault that his cupboard was bare. if after three years you still have empty shelves, it is not your predecessors fault. now trump is trying to undermine the CDC, again to shift blame from him to somebody/something else. so trump will go four years and leave the cupboard bare for the next president, but won’t take the same blame, will he? what a failure in leadership and dysfunction this administration has become. lives and fortunes lost as a result. this must be rick strykers definition of success.

Non-technical thoughts from the outhouse economist and knuckle dragger.

1. Finance has become a parasite, not a facilitator in this economy. In a properly functioning economy, finance is a means to an end. It’s a tool that makes production of useful goods and services possible. It does not have any inherent value of its own, and it does not merit deference beyond its contribution to production of other things. When it holds the rest of the economy hostage, we have a problem. I don’t know the solution. Start by re-regulating and bringing the finance industry to heel instead of continuing to fertilize it, but beyond that, it needs to be put back into the secondary role it should occupy.

2. There is a whole lot of unproductive money sloshing around the system right now, and it’s not buying anything except bonds. Hence the low yields, low inflationary pressures in other things, and no apparent shortages of anything except places to park money. Cutting taxes was a dumb idea. What’s happening in this epidemic demonstrates that.

3. Of course, contradicting what I just said, demand for all kinds of things will go down when the vast majority of people do not have money. Money has stopped flowing, and that means everything falls apart. This will take a long, long time to fix.

4. The Trump administration is its own worst enemy. It will harm Americans to get quick results, but quick results will cause even more long-term suffering. GOP led states that are pushing to open now will suffer outbreaks, and those outbreaks will kill people and drag down the economy in those states. New York, California, Washington, and other states that are being more cautious are likely to have faster recoveries in the long term. I’m expecting a problem in Wisconsin after the partisan GOP court judicially allowed bars to reopen. If I’m wrong, it is a good thing. But, for now, I expect that an outbreak in Wisconsin is inevitable.

” Finance has become a parasite, not a facilitator in this economy.”

we had a resident troll on this site, peak trader, who was of the opinion bankers and financiers were the angels of the world. not a bad word to be said about any of them (of course peak loser was a former banker, unemployed since the great recession illustrated his lack of worth both of for society and the industry, but that is another story). but i agree whole heartedly with you. bankers have enough confidence and arrogance to take others people’s money and hold it hostage unless they get their own cut. most (not all) of them have lost their value in this world.

My local financial institution is a credit union. Those are typically non-profit and have not sold their souls for filthy lucre just yet.

my credit union was the only one to pay any interest over the past decade. i imagine because they did not need to overpay a bunch of bank executives and traders, who were worthless.

Beyond worthless. Actually counterproductive in plenty of instances. Getting rid of them would be a positive move for both the economy and their employers.

Having provided analysis to the trading and sales operations of financial institutions for three decades, I must strongly agree with your points 1 and 2.

Y is the USA.EU and UK not bothered,about the COVID deaths in their part of the world ?

Could it be that they want it ? Who are the dead ? The dead are the pensioners, and the persons,who are fatally sick.dindooohindoo

The gainer in every combo,is the West – which makes one wonder,how the COVID magically mutated in its new avatar.

Posit No.1

Assuming that these dead persons in the West,had a residual life of 15 years, and we can assume that,by August,2020,there will be around 600000 dead in the West.

The pension to a pensioner,would not be less than 12,000 USD per annum, on an average,at the minimum.In addition, the medical and other social costs,on an aged pensioner,would be not less than another 8,000 USD per annum.

If they die,then on 6,00,000 people,if the West saves 20,000 USD per annum, you net USD 12 Billion,PER ANNUM – which will be around 200-300 billion for 15 years

One could argue that the US Fed just printed,the USD 12 Billion – but now it need not.The Youth in the west,had to work at high rates of tax and deductions – to finance the aged pension and health care benefits – which ultimately,led to outsourcing.

The scam would be shocking,if the dead,had no insurance ! That would be telling ! If 6,00,000 are dead,with insurance and an average insurance claim,of USD 1,00,000 – then you have a bomb – to wipe out the insurers.

If 10 million die – we are looking at net savings of USD 200 billion per annum and USD 3 Trillion over 15 years.This will also solve the health insurance problems in the US/EU,as the high claim insurers,will cease to exist – and thus lower the insurance costs,for the young,and the cost of labour in manufacturing.

if the aggregate savings on pensions and medical costs are USD 100,000 per annum,then on 10 million dead,we have a saving of ISD 1 trillion per annum,as a perpetual annuity (which is the minimum target – I suspect) – as the strategem ,is to kill people,with co-morbidities – and these are the people,who are a burden on the medical and pension infrastructure.

So the private LIFE insurers,take a 1 time HIT,in terms of claims paid out – and the state,gets a recurring benefit,in terms of pensions and health care costs – of which,some of the gains of the state,are passed back to the insurers,to offset the claim losses (and keep insurance rates low),and some of the gains to the state, are passed back to the residual young population,to reduce the rates of medical and life insurance.

Posit No.2

Large number of services and industries,in the west,will die out.That will release labour and reprice resources and rents – to drastically lower costs – and that will make,”Make in USA”,viable

How will the state finance the loss of tax revenue and GDP.Ultimately,the state will have to demonetise the deposits, in banks, of the westerners.Simple ! The USA will not be able to demonetise the PRC holdings of US T-bills – not even if the PRC sinks a US aircraft carrier in the South China Sea.

Posit No.3

All the nations who borrowed loans from PRC – will now force the PRC to do debt write offs.That will be a huge loss to the PRC,after the manufacturing shift from PRC to West.Post COVID,If 200 million people are unemployed in PRC – then you have Tiananmen – Part 2 – and then a PRC attack,on the Indian weasels, and US satellite states,like Taiwan.and new stooges like Vietnam.

Of Course,the PRC could also force the IMF,and the WB,to waive loans – but the harm to the PRC,will be done 1st.

Posit No.4

Trump postpones the US Polls,as people cannot stand in queues,and no electioneering,is possible – and he has the cure – and by September,the pensioners are dead – death rate and infections rates drops ….. who is the gainer ? If Trump is winning – Putin will stay calm – else,he might attack Eastern EU.If Trump is winning – then it will be the last chance for PRC to annex Taiwan and Vietnam – and make Trump lose face. But the odds of PRC action is medium.

Posit No.5

With massive unemployment in the West – the migrants will exit.Asians were made to clean toilets – that is their worth.They will exit.That will solve the migrants problem,rents and property rates will fall,labour will reprice,and the Westerners,will have to,start to work

The West has to take a BIG PICTURE view.South East Asia and Indian and Nepal ,are over populated,and there is no humanity there.There is no sentience,in the “so called humans”.They are robots – and 80% of them,have to die.Their time is over – they are obsolete, a dead weight,and a burden on earth.This will de-price the resources sector,lower demand,and solve the environment problem,forever.

Africans have been exploited,for at least ,2000 years – and they deserve,many more chances.

There are 3 simple steps

Are the “so-called humans” – having a “sentience” – to be assessed based on their “individual and collective actions”

If not,then they are “robots”

It is time to “terminate the robots”

It is the moral and ethical solution.They are redundant and obsolete

Reply

if i were menzie, i would delete and ban such garbage. it almost sounds like a bot trying to troll for trouble to see how many folks can be offended in one post.