Today, we present a guest post written by Jeffrey Frankel, Harpel Professor at Harvard’s Kennedy School of Government, and formerly a member of the White House Council of Economic Advisers. He was a member of the NBER’s Business Cycle Dating Committee for 25 years, with his term ending last fall. A shorter version appeared in Project Syndicate and in The Guardian.

This post follows up on “What Determines When a Recession is Recession?” which pointed out some drawbacks of defining a recession by two negative quarters of growth.

In some countries there is another, more fundamental, basis for questioning the two-quarter rule for determining recession, or any GDP-based rule. Some countries experience sharp slowdowns or periods of diminished economic activity and yet their long-term trend growth rates are either so high or so low that the negative-growth rule does not capture what is needed to describe the cyclical state of the economy. For such countries, the problem is that perhaps there is nothing special about the number zero.

Consider first a country where the rule would yield excessively frequent “recessions.” In Japan, the population is shrinking and productivity growth is far below what it used to be, so the country’s output growth has averaged only 1% per year in recent decades. As a result, even small fluctuations can turn GDP growth negative. The two-quarter rule would suggest that Japan had seven recessions between 1993 and 2015, or one every three to four years.

Now consider the opposite problem, when the two-quarter rule yields infrequent recessions. Australia is said to have had the world-record for the length of its recent expansion, at 28 years. To be sure, Australia has earned much of its success. Still, one reason why Australia’s GDP showed no downturns in the past 28 years is that the country’s labor force grew substantially faster than those in other advanced economies, especially in Europe and East Asia.

Similarly, China has not had an outright recession in 26 years (since 1993). The reason, of course, is that its trend growth rate has been high, owing to rapid growth in labor productivity. Chinese growth slowed sharply in the Great Recession of 2008-09, but did not turn negative. GDP did fall sharply when the coronavirus hit in the first quarter, but if the level of GDP rises even a little off the floor in the current quarter, China will not meet the technical definition of a recession even now.

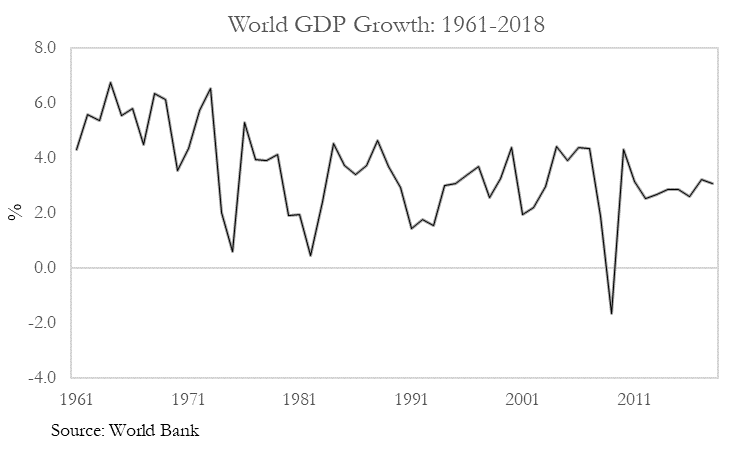

This problem arises when seeking a definition of a global recession. If negative GDP growth is the criterion, then global recessions are very rare, as a result of high trend growth among the average of EM and developing countries. (To be sure, the 2008 and 2020 recessions qualify even under this strict criterion.) For this reason, the IMF and other observers tend to adopt other less strict rules-of-thumb for calling a global recession, such as global GDP growth below 2 ½ % or negative growth in GDP per capita.

This post written by Jeffrey Frankel.

Labels are necessary, but often obscure more than they reveal. We will continue to use the term “recession” or something like it, but Frankel is of course right that a one-size-fits-all definition is a problem. Selling the public on some sort of deviation from trend or a definition based in GDP/capita is probably too hard, so we are likely to be left with a label that is often not very helpful.

We may someday stop using the term “recession” as we mostly have stopped using “depression” except in an historical sense, but not because it is vague. “Banana”, anyone?

I would argue there is a difference between a recession and a depression. Quite a big difference, actually.

Steven Kopits: Well, yes, that’s why we have different words for them. But there is a technical definition for a recession, which was first formally defined by Burns and Mitchell of the NBER in their history of business cycles. NBER has no formal definition of a depression, so there are a variety of equally quite plausibe definitions, usually indicating a duration and severity exceeding that of a typical recession.

Productivity per capita seems like the best way to think about growth. Logically, a rapidly shrinking population with reasonable productivity growth could be technically in recession even though output per capita was rising. It’s a good thought exercise for now, but it may end up being a far more important exercise in the future as the human population peaks and begins to decline. That seems like a real possibility in the next few decades.

I agree completely with this post by Jeffrey Frankel.

I shall only note for the current situation that it is unlikely that the world GDP will obey the “two-quarter rule.” I gather that we did have negative global GDP growth for the first quarter, although I have not seen a definitive number on that. But as I have noted elsewhere, global carbon emissions seem to have hit bottom around April 7. They are not perfectly correlated with GDP, but pretty strongly so, and they have been rising since that time. So it is highly likely that global GDP will exhibit positive GDP growth for the second quarter of 2020.

“If negative GDP growth is the criterion, then global recessions are very rare, as a result of high trend growth among the average of EM and developing countries.”

Yea if the mean is high, then variance is less likely to create a negative value. But world GDP also includes some diversification to the statistic unless national macroeconomies are highly correlated.

Maybe we should do like in 1967 when growth slowed to significantly below trend but did not turn negative.

We ended-up labeling it a growth recession.

A personal side note, I’ve long believed that the inflation of the 1970s began when we did not have a recession in 1967 and wage growth did not slow down.

Consequently, we entered the 1970s with wages already at a very high growth rate. Yes, oil and food played a big role in the 1970s, but wage growth and poor productivity were still more important.

Yep another interesting post.

Let me add another problem.

You might get a country that has a depression ( a drop in output of 10%) although my old pard Barkely hadn’t heard of it. What a terrible education system you have there!! however the country might not have two consecutive quarters of negative growth.

Yes we did avoid a recession during the GFC BUT we did have two consecutive quarters of negative growth in GDP per capita,

Excuse me, NT, but where did I ever claim we had never seen nations experience 10% declines? You popped up with the claim that somehow a 10% decline defines a depression, which I said is not the case. Then you amended this to add a duration component to it. But as Menzie notes above, there is nor formal definitiono of a depression, although in general we tend to think of such involving both substantial severity, with 10% perhaps being a possible criterion, as well as some duration, probably well over a year, although again there is no agreement on either of those and nobody official, including especially NBER committee has put forth an official set of criteria to define a depression.

As for claiming that I somehow do not know that we have seen 10% output declines, are you joining macroduck in imitating the currently absent Moses H. in making false claims about what I have said here? That would be unfortunate, mate.

Well me old mate there might not be a definition in the US but your education system is deficient. And all I said is you haven’t heard of that definition.

come down under and get a decent education!!

As for the NBER committee I have already said I like how they make their declarations so i will not be dogmatic.

As for comparing me to macroduck or moses I am appalled.

I need to take more blue pills before i have another attack.

You yanks hit below the vulnerable area.!

NT,

I am not sure what you are up to with all this ranting about “your education system.” Whether there is a formal definition of a depression in the US is not a matter of the US education system, but of what authorities say about it, notably in particular that committee of the NBER. Maybe they should have come up with a definition, and one that you approve of, but they have, and a different education system here is not likely to move them one way or the other toward doing so, mate.

Maybe you were not out to imitate MH and md on their bad days, but you seemed to have putting on a good show of trying to, mate.

BTW, NT, I have seen this 10% for three years floating around, but it is not official in US. Maybe it is in OZ, but you all have not had a decline in GDP for decades until recently, mate. Did this long period of positive growth lead to the OZzie education system to decide that a 10% decline in GDP for a three year period is the true definition of an economic depression that all around the world should officially adopt?