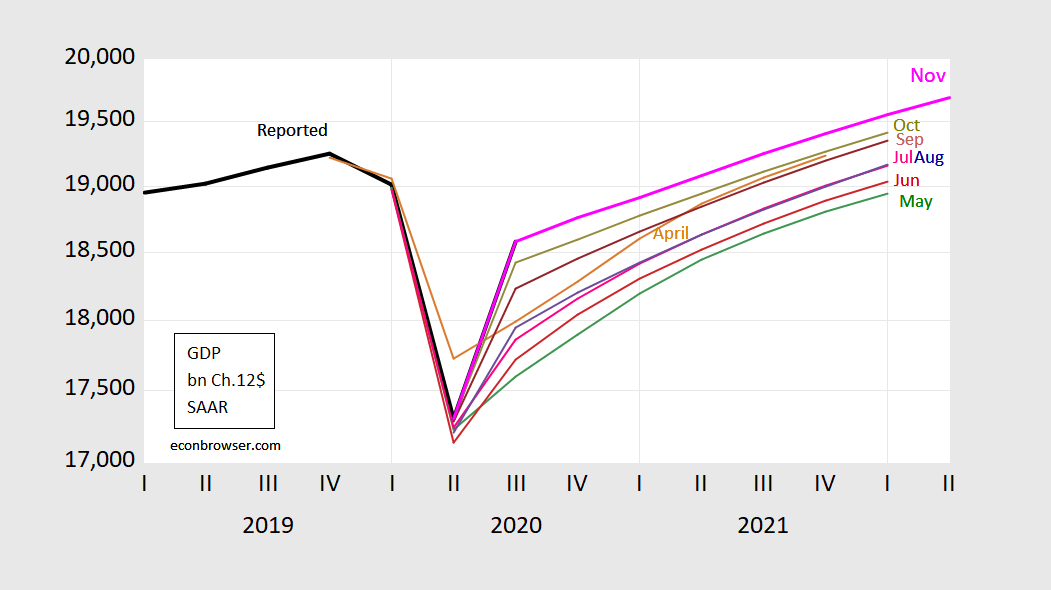

No acceleration in growth rates, but GDP level higher relative to October survey; few see a true “V”, or a true “W”.

Figure 1: GDP as reported in 2020Q2 3rd release (black), WSJ April survey (tan), May survey (green), June survey (red), July survey (pink), August survey (blue), September (brown), October (chartreuse), November (pink), all in billions Ch.2012$, SAAR, all on log scale. Source: BEA, various vintages, WSJ survey, various vintages, author’s calculations.

Note that while the implied projected level of GDP is higher in the November survey, this is not because growth prospects have brightened going forward. Rather, it’s because Q3 growth outperformed the 28.5% growth (SAAR) in the mean October survey (results discussed in this post).

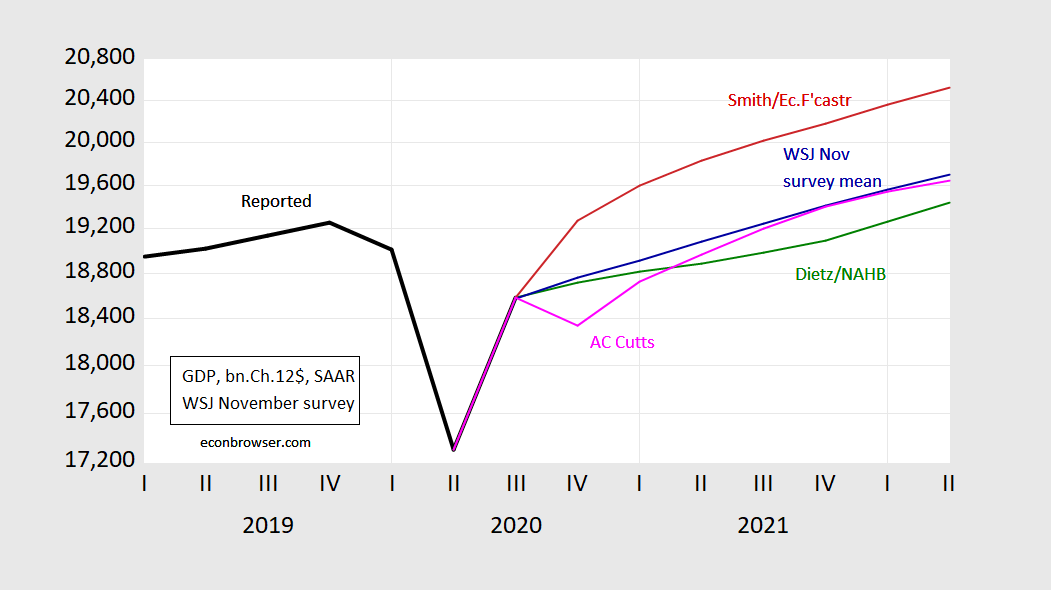

Figure 2 shows the mean GDP forecast, and the fastest forecasted growth (James Smith).( I want whatever pharmaceutical that guy takes!) and the slowest (Robert Dietz of the NAHB) over the next four quarters (2020Q3-2021Q2).

Figure 2: GDP as reported in 2020Q3 advance release (black), James Smith/Economic Forecaster LLC (red), Robert Dietz/National Assn of Home Builders (green), Amy Crew Cutts/A.C. Cutts & assoc. (pink), all in billions Ch.2012$, SAAR, on log scale. Source: BEA, 2020Q2 3rd release, October WSJ survey, and author’s calculations.

Smith predicts a “V” recovery. Only one forecasts a “W” recovery (Amy Crew Cutts).

The survey was taken between November 6-10, so after election day, and presumably after it became somewhat clear who would win the presidency and who would control the senate.

Personally, I think that with the fast-deteriorating Covid-19 situation (cases, hospitalizations, deaths all rising), Trump administration complete abdication of a public health response, and administration obstruction of a transition to the new administration, I think most of these forecasters are underestimating the likelihood of zero growth in 2020Q4 and into 2021Q1.

In today’s newsletter, Goldman Sachs represents mainstream consensus view that a relatively small fiscal stimulus ($1 trn) is likely, but not arriving until the new congress is seated. With many programs ending at years-end, the heightened uncertainty (not to mention decrease in disposable income) is sure to constrain consumer spending. Torsten Slok (Apollo) notes:

The ongoing rise in the number of covid cases is likely to have a negative impact on mobility, shopping, and restaurant bookings, even in a situation where the US economy does not enter a second lockdown similar to what we are seeing in Europe. …The bottom line is that the near-term outlook for the global economy is negative because of the ongoing spike in the number of cases, but with the vaccine news we are likely to see growth accelerating going into 2021. In short, it looks like this will end up being a W-shaped recovery.

Countering the depressing effects of the pandemic is (for now) optimism regarding the development of an effective vaccine, although widespread distribution is not expected until something near mid-2021. That optimism should help sustain consumer spending by households and business fixed investment by firms, that are not liquidity constrained.

Additional discussion of the survey results in the WSJ article.

“Goldman Sachs represents mainstream consensus view that a relatively small fiscal stimulus ($1 trn) is likely, but not arriving until the new congress is seated.”

Certainly what happens on the virus and what your fiscal stance becomes are two key components on what kind of growth we might see in 2021. Right now the Baby in Chief is doing nothing on the former. And Mitch McConnell gives me no hope on the latter. Then again if Georgia Democrats turn out on Jan. 5 – maybe McConnell becomes irrelevant even before Trump becomes irrelevant.

Menzie, do you know if Amy Crew Cutts is any relation to Sammy Supercuts?? I’ve been hunting around for a new barber and ever since I switched over to Rabbi Snippit who I met at that Bris I just haven’t felt the same.

All of my usual BS aside that Menzie probably semi-regretfully tolerates, Torsten Slok’s intimation at a “W” recovery is VERY eye-brow raising. Unlike Barkley JuniorMeister, not a man I want to be on the other side of an argument on. Very fascinating. NOT “disagreeing”, as I am waaaaay waaaaaay too chickensh*t to disagree with a dude as razor sharp as Torsten Slok. But at the same time, it’s very eye-brow raising. That is a fascinating one. As we expect from our man Menzie, pulling the more interesting jewels hiding underneath the headline. Hmmmm, this one I will be turning around in my mind for awhile. Wish I could read that confounded premium Apollo newsletter. Those damnded Apollo fancy pantsers.

Whether it’s a “V” or a “W” or a “K”…who knows? Not this guy. But this is all about the shape of the recovery that will close the potential output gap. Increasing demand will shrink that gap with either because of a vaccine or because of more stimulus; but a drop in potential GDP will also shrink that gap…only in a bad way. I think Fed Chairman Powell hit the nail on the head when he opined about what a post-pandemic economy will look like over the longer run. It will almost certainly be a less productive economy and an even less egalitarian economy, if such a thing is even possible. Women will be slow to return to the workforce. Children will have lost a year of education. Workers will continue to suffer debilitating effects from COVID for many years. It will be a less social and more private world as people avoid interactions outside the household, such as restaurants, live theater, concerts, sporting events, etc. All things point to a less productive global economy. And oh by the way, we’ll have to deal with climate change. Sadly, there are other pandemics waiting in the wings. Governments should be pouring money into STEM programs and research. Instead of training more baristas we should be training and employing more chemists and biologists. It will be hard to fight future pandemics when a large segment of the population believes Adam and Eve rode around on the backs of dinosaurs.

Do please keep in mind, 2slug, which I think you know, that the k pattern can happen with a V or a flattening V or a W. It is about income distribution getting more unequal as poorer people get worse off and the richer get better off, whatever the pattern of aggregate GDP. Much of what you talk about here is in fact related to the negative aspects of the k pattern and the need to address those.

Barkley Rosser Yes, I understand that a “k” pattern captures the rich getting richer (the “V” portion) with the poor getting poorer. But my larger point is that we shouldn’t just be focusing on getting people back to their same old jobs because many of those same old jobs will be dead ends in a post-pandemic world. We don’t know what a post-pandemic economy will look like, but we do have a pretty good idea of what it won’t look like. As an old ORSA guy my instincts are to worry about path dependence, so the stimulus decisions we make today will likely exclude certain possibilities in the future. We shouldn’t try to fully resuscitate a lot of “dirty” capital and “dirty” jobs that we will only have to kill off in the future. We should recognize that pandemics will probably become regular features of life, so we should keep that in mind as we stimulate demand; e.g., redesigning the HVAC systems for public buildings and schools. Bottom line, I want to see economists pay as much attention to how we work the old aggregate supply curve as they do the aggregate demand curve. This isn’t your garden variety recession, so we shouldn’t rely solely upon garden variety solutions. If we don’t marry our short-term stimulus with long-term economic changes, then we risk the kind of low productivity economy that Chairman Powell warned about.

2slug,

I don’t think we have any disagreement here. I would like to see a more vigorous effort to deal with inequality, but pretty obviously the ability to do anything about that will be severely lmited if the GOP continues to control the Senate. I was basically being fussy about having the possible aggregate shapes lumped in without comment with the one that focuses on income distribution dynamics.

Powell, the moron who thought unemployment would be at 9.3% in December. Grounds for a firing.

Once again, for the umpteenth time now, we had a V that has now flattened, as I forecast before anybody else here. I do not know if it will turn into a W or not.

I can’t be the only person who reads this blog that about once every other day prays that Barkley Junior never grades essay exams.

Moses,

Is this completely stupid remark more reflective of your self-confessed sadism or your self-confessed hatred?

And what on earth are doing commenting yet again on the shape of the GDP pattern when you have refused to tell us what your prediction was for it, even after being challenged to put up or shut up on this matter? Really. Shut up and get lost.

sorry Barkes but GDP is not at its previous llevels let alone higher levels as it would be for a V recovery.

@ Not Trampis

Barkley Junior calls this his “I’m never wrong, and so am I” theory on recovery shape permutations. It’s based on a algorithm that sends narcissism into an endless feedback loop. He came up with it one morning when he was looking in the bathroom mirror and hypnotized himself for two straight weeks saying “I love you”. His wife “woke” him out of the self-induced trance by injecting a small amount of battery acid into his left inner eardrum and saying “God, thou dost rule over this bathroom.” It was moving for everyone involved and was later renamed “Rosser’s Equation” by a small hamster Barkley Junior was keeping as a house pet which Barkley said spoke to him in English later that same day. There’s a wiki page which recounts the entire event.

Look at the bloody graph, mate, and also read what I have written umpteen million times, including right here once again. It has been a V that flattened. Look at it. That is what it is. That the V flattened before it got all the way back up does not obviate it having been a V for awhile.

BTW, are you curious what our mate Moses’s secret forecast that he refuses to reveal was for the pattern? I have repeatedly asked him to tell us, “put up or shut up,” but he has ridiculed the request while most certainly not shutting up.

So, if you do not think calling it a “V that flattens,” what do you think it should be called? Of course, if it turns down it becomes a W, although a sort of wiggly one.

Also, NT, when I forecast accurately that it would be V that would flatten I never said that it would go all the way back up before it flattened. Indeed, I implied quite the opposite in that I forecast it to flatten quite soon. If anything my error was to fail to forecast how long it kept on being a V before the flattening finally did appear.

But, if you wish to insist that it cannot be a proper V unless it goes all the way back up before it does something else, have it your way. But, for the record, I never said it would do that. My forecast of what it would do fits what we have seen, even if you want to insist that it cannot be properly called a V unless it goes all the way up before changing.

well Barkes it seems some yanks do not understand what a V recovery is or should I say have changed the definition just like some have changed what seasonally adjusted annual rates means!

NT,

Sorry, but I do not think this is some sort of “yanks vs Ozzies” schtick, although I know you like to play that game. On the SAAR matter, where I tend to agree with you, and it is Moses Herzog who is running around declaring that everybody everywhere all the time should use SAAR. My only concern in all of that has been to be clear which numbers are being used because there have been media reports in he US and elsewhere that report numbers but are unclear what they are reporting. To be on the safe side somebody should report what both measures say with them clearly marked.

As for your bloody insistence on defining a “V pattern” a certain way, this is also not Ozzies vs yanks, just you being absurdly picky. Since you are asserting that somehow your view is something found in a dictionary, go ahead, quote us a dictionary. I think you are just being silly with this. Sorry, mate. In any case, I think I have been very clear about what I was forecasting, even if you insist that it cannot be called a V. But like Moses Herzog, you have not said what it should be called.

NT,

I confess that I am this moment not in a good mood., and I know you are basically a good guy, mate. But I really think you overdid it with this V definition matter. I apologize for what I am about to do, but I am going to really pound on you for this.

So, NT, your “definition” of a V pattern is that the tops on both sides must be equal, otherwise it is not a V and worthy of snotty remarks from down under. Fine. So obviously in the real world with data, we never see the tops of series exactly equaling each other, which is the hardline interpretation of your “definition.” So the question is how much can those tops differ and it still can pass muster with you for being a V. I assume you would agree that a billionth of a difference would not make it not a V, right, mate?

So, a billionth is way too small, lol. But what about 1%? Now we are getting in range. Recently the difference between current GDP and the Feb peak was about 3.5%, oh, less than 5%. Is 5% is too much? But the flattening hit sooner, so more than 3.5%, but we do not know exactly where or when the flattening started, so the gap is more than 3.5%. So, NT, just exactly what is the cutoff for when a V stops being a V, mate?

The rumor is this quote is on a small plaque on Junior’s desk facing towards visitors to his work office, residing in the place some people put their name plate.

https://cdn.someecards.com/someecards/usercards/-i-have-only-been-wrong-once-there-was-a-time-where-i-thought-i-might-be-wrong-but-that-turned-out-not-to-be-the-case-9fb07.png

Disagree. GDP will likely surge later in 2021 as the virus peters out at the end of winter and a vaccine therapy stops any renewed outbreaks. 7 trillion of excess dollars born of Cares and private bank bank creation. Which will squirl in the financial system for years. Your post is already dead.

Amy Cuts was expecting a deeper second dip in her October forecast, taking Q3 results into account. I’m not a client, so I don’t know whether her Q4 call has always anticipated a policy failure. (Bill at Calculated Risk appears to speak highly of her, by the way: https://www.calculatedriskblog.com/2020/11/a-comment-on-q4-gdp.html?m=1) Goldman’s latest text suggests most forecasts had anticipated an aid package and have now given up on it.

A forecast in the range of 2.9% (NY Fed) to 3.5% (Atlanta Fed) would not normally imply a substantial risk of a decline in real GDP. Now, however, given the high variability in GDP in recent quarters, those estimates would seem to suggest a pretty big risk of a decline.

I suspect we have built in a buffer against the supply-side impact of the new (who’d a thunk it?) surge in infections. Many who now work from home and have had a chance to get up to speed there can go on working without interruption. That’s an improvement over the first spike.

Demand is another matter. Real disposable income and savings were in good shape as of September, though not as good as in August. October data could well show a substantial weakening, given the slide in government transfers. Given the strong finish to real personal consumption in Q3, a decline in PCE would be needed in Q4 to generate even flat Q/Q performance in Q4. Could happen, especially if holiday spending is weak.

2slugbaits pointed out (https://econbrowser.com/archives/2020/10/record-breaking-increase-in-gdp) that inventories could become a sizable drag soon. That seems to me an important issue to watch as Q4 data come in.