The below is a republication of a post from July 19, 2019 entitled “What Does Judy Shelton Believe GDP Growth and Inflation Are in 2019?” in response to Senate Majority Leader Mitch McConnel’s invocation of cloture on the nomination of Judy Shelton to the Federal Reserve Board of Governors.

In a 2015 Cato Institute session, Fed Board Nominee Judy Shelton discusses whether to trust or not official GDP and inflation statistics (she says no — see 1:07:07) (h/t Sam Bell).

This makes me wonder (1) what is the basis for her beliefs, and (2) what would she use that is different.

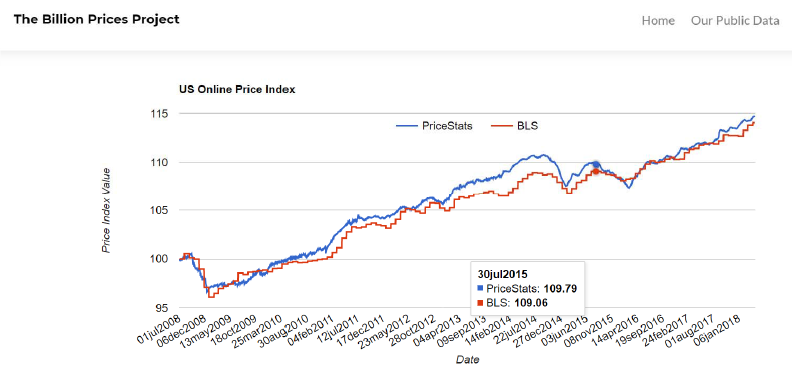

Let’s consider inflation, presumably CPI inflation. One recent innovation is the Billion Prices Project’s price value indicator (see Jim’s post on this subject). For the US, the comparison against the official CPI series is depicted below.

Source: Billion Prices Project, accessed 7/19/2019.

With both series rescaled to July 2008, the price levels are virtually the same at July 30, 2015, the day of Dr. Shelton’s speech. It might be that Dr. Shelton is consulting Shadow Government Statistics; if so, I hope she will immediately cease and desist (per discussion by Jim Hamilton, and subsequent “debate” with ShadowStats’ John Williams).

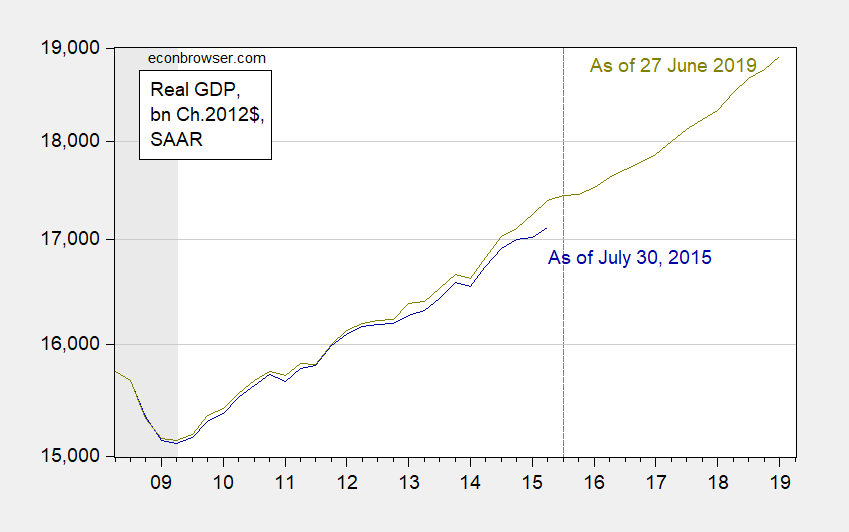

What about GDP? Well, here she might be on slightly firmer footing, although it leaves open the question of what would be a better indicator of total economic activity. In point of fact, with revisions based upon more detailed data, GDP was actually 1.6% higher than estimated in 2015Q2 (she had access to an advance estimate of GDP as of 30 July 2015). I suspect her view at the time was that reported GDP was lower than actual economic activity…

Figure 1: Reported GDP as of July 30, 2015 (dark blue), and as of June 11, 2019 (chartreuse), both in billions of Ch.2012$, SAAR. July 2015 vintage series rescaled from Ch.2009$ to Ch.2012$ using ratio of implicit GDP deflator in 2009 vs. 2012 (0.95004). NBER defined recession dates shaded gray. Dashed line at 2015Q3, encompassing Shelton’s statement. Source: BEA via FRED, and ALFRED, and author’s calculations.

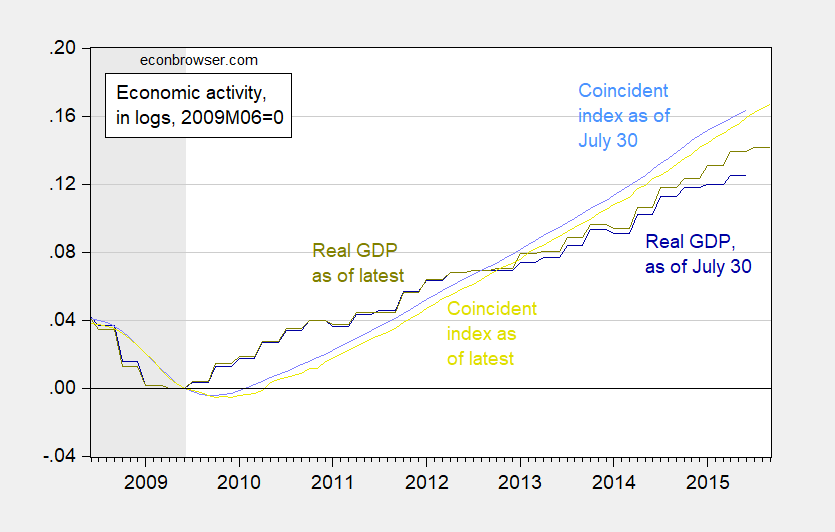

How about alternative indicators to GDP. Well, there are numerous, but they usually aim at detecting cyclical fluctuations in advance (CFNAI, monthly GDP from Macroeconomic Advisers, etc.). [As an aside, an interesting high frequency measure recently developed is described here, and compared to Aruba-Diebold-Scotti.] I suspect that Shelton is uninterested in this high-frequency/cyclical aspects, and more in the trend. Here, I compare the July 2015 and latest vintage of GDP measures, plotted against the Philadelphia Fed coincident indices of comparable vintages.

Figure 2: Reported GDP as of July 30, 2015 (dark blue), and as of June 11, 2019 (chartreuse), SAAR, and Philadelphia Fed coincident indices as of July 30, 2015 (light blue), and as of June 28, 2019 (light chartreuse), all series rescaled to log 2009M06=0. NBER defined recession dates shaded gray. Dashed line at 2015Q3, encompassing Shelton’s statement. Source: BEA, Philadelphia Fed via FRED, and ALFRED, and author’s calculations.

Note that the advance GDP release available to Shelton in 2015 understated real GDP as we understand it in 2019. The coincident indices also suggest that economic activity is higher than indicated by GDP, although given the normalization on end-of-recession (June 2009), the gap is only 2% in log terms, using the latest vintages.

So, we are left with wondering exactly what Dr. Shelton believes those key price and activity variables that the Fed follows (technically, it’s PCE deflator rather than the CPI, but you get the idea). Of course, if as indicated elsewhere, she wants the price of gold as a nominal anchor, this discussion is moot — and she’s just a data-conspiracy crank like so many others.

I will also say that if she plans to implement retaliation for currency manipulation by other countries, she had better figure out what variables to look at, and whether they are measured correctly (here I think there is room for debate, although I think she would say if another country pegs its exchange rate, its prima facie evidence of manipulation).

Isn’t Ms. Shelton a proponent of the gold standard? Our new troll (JohnH) is too as he thinks going on a gold standard would actually be good for workers. And yea – JohnH shares Ms. Shelton’s disdain for reliable economic data.

More seriously, however, I read somewhere she might be about to placed on the Federal Reserve. I hope this does not happen. You have tried to warn everyone.

https://www.washingtonpost.com/business/2020/11/12/fed-shelton-senate/

November 12, 2020

Senate readies vote on Judy Shelton, granting Trump another opportunity to shape Federal Reserve

Shelton’s confirmation could mark Trump’s final imprint on the Fed board, just months before the Biden administration is inaugurated.

By Rachel Siegel – Washington Post

The Senate is expected to confirm President Trump’s controversial Federal Reserve nominee Judy Shelton to a seat on the central bank’s board of governors, giving the president another chance to shape the long-term direction of one of the government’s most powerful entities.

Senate Majority Leader Mitch McConnell (R-Ky.) took procedural steps Thursday to set up a vote on Shelton’s long-pending nomination for as early as next week. Also on Thursday, Sen. Lisa Murkowski (R-Alaska) — a key moderate whose support had not been assured — said she would back Shelton’s nomination….

PGL,

David Glasner would have you for breakfast on that remark re gold Standard

What can a new Prez do about Fed appointees

What would breakfast consist of? pgl doesn’t favor a good standard. Glasner doesn’t favor a gold standard (https://uneasymoney.com/2016/12/25/golden-misconceptions/). Has pgl shown disfavor toward a gold standard in a way you find problematic?

Judy Shelton has a lot of Rick Stryker inside her. Only having the courage of her convictions when it provides her with her true end means.

This is how you get pro QE under a Republican anti-QE under a Democrat type of analysis coming from the same individual. This is how you get the Mitt Romneys who love redistribution of wealth when it goes into his own pocket. And the same goes for fiscal policy. Judy Shelton and Stephen Moore types don’t care if the officiating for the football game is good or bad. If bad officiating benefits their team, they couldn’t care less.

It’s not that GDP is accurate or inaccurate. That’s not the real point for Judy Shelton. She can only get the goal posts for the football game moved by claiming the goal posts aren’t a valid way to judge accuracy of kicking. If the goal posts are seen as the best measure, then no means exists to move the goal posts.

“This is how you get pro QE under a Republican anti-QE under a Democrat type of analysis coming from the same individual.”

The same can be said about John “interest rates were too low for too long” Taylor and he used to be a well respected macroeconomist.

2 pgl

Not that this is something you ever hold your breath to hear, but you and I basically agree 100% on this. If I was to parse things out to the nth degree I would say even John Taylor I would rank above Shelton and Moore, but I would bet a lot you also agree on this latter part as well. But, no, I pretty strongly dislike John Taylor as well. I don’t always even mind guys with gargantuan egos, like Eugene Fama, I mean his ego is mammoth sized, but at least you can actually see why Fama has the mammoth ego because he has some reason for that. Taylor?? I don’t see it.

* @ pgl Damn it I swear I fixed that. Keyboard finally getting back at me for spilling off brand Mountain Dew on it about 4 months ago.

John Taylor was a decent economist back in the 1980’s and 1990’s. But there was something about that White House Kool Aid in the George W. Bush era (Taylor was on the economics team) that got Dr. Taylor forever drunk on partisan hackery.

So this is step one in Mitch’s plan to sabotage the Biden administration’s economic growth agenda. Next step will likely be to reimpose the debt ceiling in order to send the economy off another fiscal cliff. Mitch is just pure evil and that has nothing to do with Trump.

Won’t work. 7 trillion dollars have been created. That will slush around for years and blow up bubbles. The drift has already began(and may add a extra trillion by Valentine’s day). Fed policy won’t change that and due to inflation lags, enhance it.

The Rage: M2 has increased $3.36 trn since end-February. What is your 7$ trn figure referring to?

Fiscal and bank liabilities created by Cares debt and post crisis lending. It’s created a new carry trade which is a impending bubble that will start post-pandemic.

In other words you just made this figure up – Lawrence Kudlow style!

https://www.nytimes.com/2020/11/12/opinion/biden-mitch-mcconnell-economy.html

November 12, 2020

A Republican Senate Would Be Bad for Business

What’s bad for America would be bad for corporations, too.

By Paul Krugman

So the blue wave fell short of expectations. Joe Biden will be the next president, but unless Democrats pull off an upset in the Georgia Senate runoffs — which, to be fair, they might, given the remarkable strength of their organizing efforts there — Mitch McConnell will still be the Senate majority leader.

Big business seems happy with this outcome. The stock market was rising even before we got good news about prospects for a coronavirus vaccine. Corporate interests appear to imagine that they will flourish under a Biden presidency checked by Republican control of the Senate.

But big business is wrong. Divided government is all too likely to mean paralysis at a time when we desperately need strong action.

Why? Despite the vaccine news, we are still on track for a nightmarish pandemic winter — which will be made far worse, in human and economic terms, if a Republican Senate obstructs the Biden administration’s response. And while the economy will bounce back once a vaccine is widely distributed, we have huge long-term problems that will not be resolved if we have the kind of gridlock that characterized most of the Obama years.

First, the pandemic: With much of the public’s attention focused either on Donald Trump’s last-ditch efforts to steal the election or on hopes that a vaccine will let us resume normal life, I’m not sure how many people realize just how ruinous a prospect we’re facing for the next few months.

Over the past week, Americans have been dying from Covid-19 at the rate of more than 1,000 a day. But deaths typically lag a few weeks behind reported cases — and the daily number of new cases has doubled over the past three weeks. This means that we’re almost surely looking at 2,000 deaths a day at some point next month.

And the number of new cases is still rising exponentially, so things will get much, much worse over the months that follow, especially because until Jan. 20 we will, for all practical purposes, not have a president. By the time Biden is finally inaugurated we may well be having the equivalent of a 9/11 every day.

In addition to bringing death as well as long-term health damage for many survivors, the exploding pandemic will bring immense economic hardship. Responsible governors are imposing new lockdowns that may help curb the spread of the coronavirus, but that will also lead to a new wave of job losses.

True, some of the worst coronavirus outbreaks are now in states with irresponsible governors who won’t even impose mask mandates. But even in those states people can’t help noticing that friends and neighbors are dying and that the hospitals are full; they will cut back on their spending, leading to many lost jobs, even without political guidance.

What we need, clearly, is a very large-scale program of disaster relief, providing families, businesses and, not least, state and local governments with the help they require to avoid financial ruin until a vaccine arrives. And you might think that a Republican Senate would be willing to work with the Biden administration on such an obviously necessary program.

That is, you might think this if you’ve been hiding in a cave for the past 12 years….

“Divided government is all too likely to mean paralysis at a time when we desperately need strong action.”

Krugman was also advocating strong action some 12 years ago. But of course McConnell style filibustering scaled down the Obama stimulus.

Now one might have to give Krugman some due here but wait for it, wait for it, JohnH will likely chime in with his usual BS that Krugman is being a center right neoliberal. He is both that STUPID and that dishonest at the same time.

There are two arguments I am aware of for divided government. One is that stocks have historically performed better under divided government, don’t bother me win details. The problem with this view is that it is wrong: https://www.wsj.com/articles/political-gridlock-is-supposed-to-be-good-for-stocks-the-data-dont-support-that-11604847910

Of course, the other problem with this mistaken view is that it assumes enough data point to allow reliable inference, and that we are in an all-else-equal world. Krugman’s point is that our ceteris ain’t paribus. He says Democrats will be better for earnings. Stock investors know that pre-tax earnings are only a part of their calculation of the value of equities. This is key to the understanding that “the stock market isn’t the economy”, something Krugman has pointed out often enough himself. It is a tacit concession to our rentier “masters” to argue that equity performance is a reasonable that’s of the economic outlook.

Policy analysis by short-term equity performance is a tricky enterprise, one which assumes near complete knowledge of what drives stock prices in the short term. Contrary to the impression garnered from the financial press, the drivers of short-term equity performance are often pretty obscure to the casual analyst, which includes many market commentators and academics.

Krugman’s intention is good in this article, but his method is faulty.

“…a reasonable forecast of the economic outlook.”

November 12, 2020

Coronavirus

US

Cases ( 10,873,936)

Deaths ( 248,585)

India

Cases ( 8,727,900)

Deaths ( 128,686)

France

Cases ( 1,898,710)

Deaths ( 42,960)

UK

Cases ( 1,290,195)

Deaths ( 50,928)

Mexico

Cases ( 986,177)

Deaths ( 96,430)

Germany

Cases ( 749,638)

Deaths ( 12,276)

Canada

Cases ( 282,577)

Deaths ( 10,768)

China

Cases ( 86,299)

Deaths ( 4,634)

November 12, 2020

Coronavirus (Deaths per million)

US ( 749)

UK ( 749)

Mexico ( 745)

France ( 658)

Canada ( 284)

Germany ( 146)

India ( 93)

China ( 3)

Notice the ratios of deaths to coronavirus cases are 9.8%, 3.9% and 2.3% for Mexico, the United Kingdom and France respectively. These ratios are high, but have been significantly higher, while falling recently as new cases are being rapidly recorded.

https://news.cgtn.com/news/2020-11-13/Chinese-mainland-reports-eight-new-COVID-19-cases-all-from-overseas-VnnGxkGTiU/index.html

November 13, 2020

Chinese mainland reports 8 new COVID-19 cases

The Chinese mainland registered 8 new COVID-19 cases on Thursday, all from overseas, the National Health Commission announced on Friday.

A total of 15 new asymptomatic COVID-19 cases were recorded, all from overseas, while 697 asymptomatic patients remain under medical observation. No COVID-19 related deaths were reported on Thursday, and 27 patients were discharged from hospitals after recovering.

As of Thursday, the total confirmed COVID-19 cases reached 86,307, with 4,634 fatalities.

Chinese mainland new imported cases

https://news.cgtn.com/news/2020-11-13/Chinese-mainland-reports-eight-new-COVID-19-cases-all-from-overseas-VnnGxkGTiU/img/a2d0d464911441138b0aa3a8359a1089/a2d0d464911441138b0aa3a8359a1089.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2020-11-13/Chinese-mainland-reports-eight-new-COVID-19-cases-all-from-overseas-VnnGxkGTiU/img/bd3092c6928f4d8b8d540a67fad0f476/bd3092c6928f4d8b8d540a67fad0f476.jpeg

[ There has been no coronavirus death on the Chinese mainland since May 17. Since June began there have been 5 limited community clusters of infections, each of which was contained with mass testing, contact tracing and quarantine, with each outbreak ending in a few weeks.

Single local infections have recently been recorded in 3 cities, with mass testing, contact tracing and quarantine again being used to identify the origin of as well as to contain and end each possible outbreak.

Imported coronavirus cases are caught at entry points with required testing and immediate quarantine. Asymptomatic cases are all quarantined. The flow of imported cases to China is low, but has been persistent.

There are now 394 active coronavirus cases in all on the Chinese mainland, 3 of which cases are classed as serious or critical. ]

The GOP vandalism of this country continues. It is frustrating to watch it happen.

What is happening now, is that the Trump administration is doing all that can be done to make sure that policy plans and actions taken by this administration in domestic and international spheres are very, very difficult for the Biden administration to undo. The analogy would be to the Hoover administration * which sought to the end to undo the plans of Franklin Roosevelt.

http://www.nytimes.com/2008/11/30/opinion/30leuchtenburg.html

November 30, 2008

Keep Your Distance

By WILLIAM E. LEUCHTENBURG

November 12, 2020

Coronavirus

US

Cases ( 10,873,936)

Deaths ( 248,585)

New Cases ( 165,306)

New Deaths ( 1,188)

Current Serious, Critical Cases ( 19,261)

Lev Bordorovsky has an interesting take in graphs about why Americans are skeptical of the CPI. You have to subscribe to see it, but if you like economics graphs, no one does it better than Lev.

https://thedailyshot.com/2020/11/13/why-many-americans-are-skeptical-about-the-official-cpi-figures/

Steven Kopits: Don’t want to subscribe, so can’t read the article. But here are my views on CPI-skepticism: https://econbrowser.com/archives/2014/07/unanchored (you commented on the article).

I read his comment – ugh! Relative price changes occur? STOP the presses!

I also read a comment from Peak Trader who at least that day made a LOT more sense that Stevie did.

I don’t believe it’s a paid subscription. You just have to sign up.

Lev does lots and lots of graphs. If you like macro, you’ll find some of his work interesting. It is not ideological.

Even if it is free – I’m not wasting my time on junk. Same way I’m not wasting my time on your junk.

Back in the pre-pgl days. Nostalgic. The point I was making there was that a price increase is not necessarily the same as inflation.

Like I said – stop the presses. Come on – it was beyond an obvious point. Except maybe for you.

Steven Kopits: pgl has been commenting on Econbrowser since June 2005.

A hedge fund manager from Oklahoma? You do have a habit of relying on crack pots. No – not subscribing to his nonsense no more than I’m reading your worthless blog.

Looks like Judy Shelton won’t be on the fed, at least temporarily. Moscow Mitch cast what was apparently a strategic NO vote. I’m not sure what that means, but I’m sure that it doesn’t mean the nomination is as gone as it should be. If she’s confirmed, it would be the first lame duck confirmation ever, so far as I know.