Private nonfarm payrolls down 301K vs. +207K consensus (Bloomberg). Still, don’t over-read.

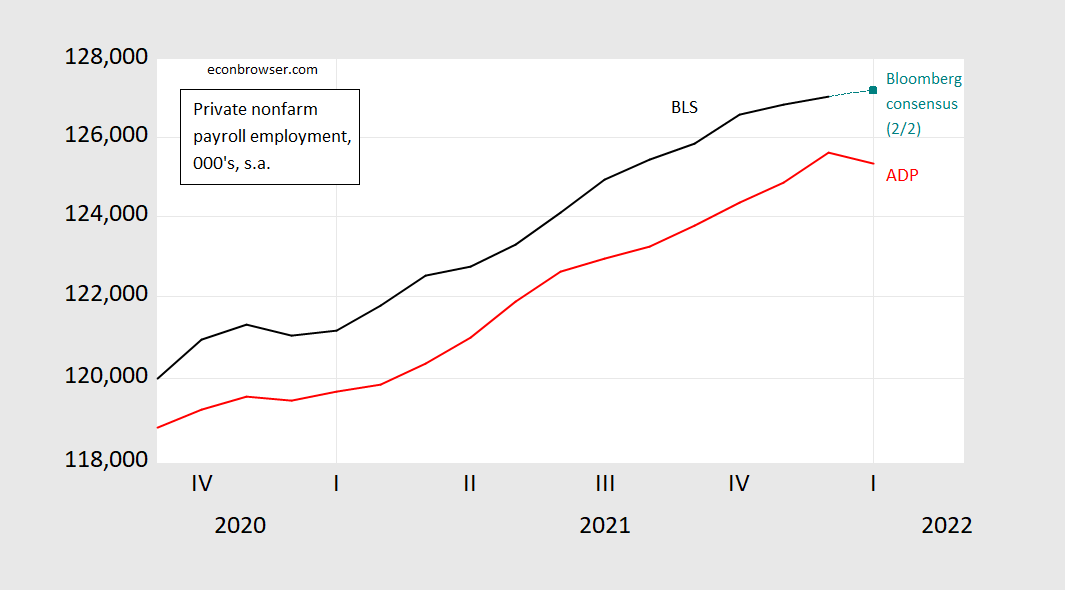

Figure 1: BLS private nonfarm payroll employment from December release (black), Bloomberg consensus as of 2/1 (teal square), ADP (red). Source: BLS, Bloomberg, and ADP via FRED.

ADP private nonfarm has not tracked BLS private nonfarm very well in levels; and not in differences either, in recent months. (See this post for pre-covid era analysis.)

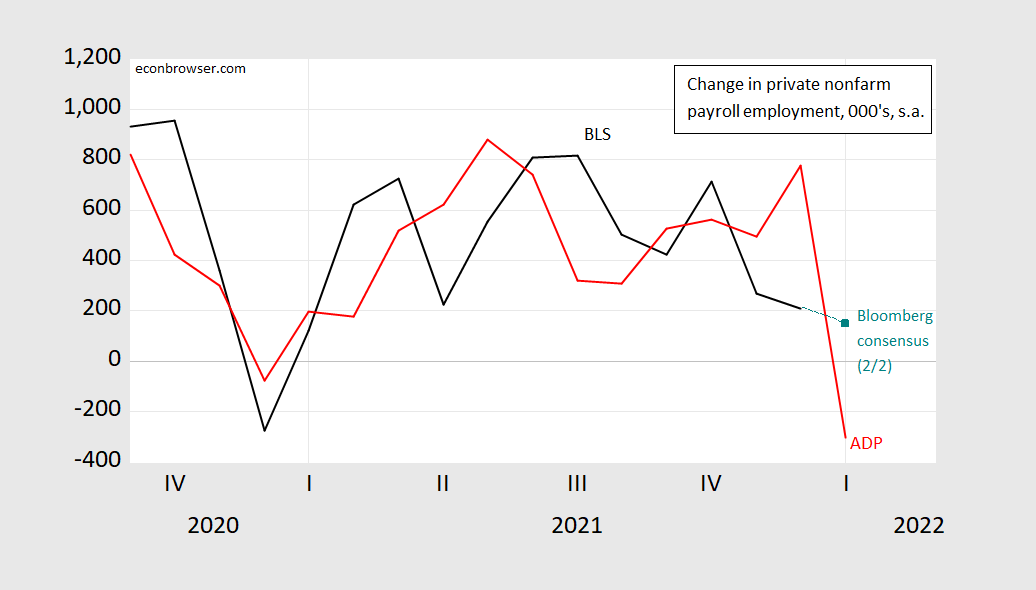

Figure 2: Change in BLS private nonfarm payroll employment from December release (black), Bloomberg consensus as of 2/1 (teal square), ADP (red). Source: BLS, Bloomberg, ADP via FRED, and author’s calculations.

The US (total) nonfarm payroll 95% confidence interval is +/- 110K (BLS)

For this sample (arbitrarily chosen), the regression coefficient of change in BLS series on change in ADP series 1.03 (significant at the 1% msl, using HAC robust standard errors), and the regression yields an adjusted R-squared of 0.86 (2020M05-21M12). A regression using log first differences yields similar R-squared. The point estimate for 2022M01 from this regression is -186K, but the 60% prediction interval is [269,-640] – in other words, the incremental information from the ADP release is still pretty small.

I read a brief news story and decided to stop reading altogether the news was stressing me out. Under we get this pandemic under control, I might just check with the BLS on an annual basis!

Over the past two months, ADP has counted 791,000 more new private sector jobs than has the BLS establishments survey. ADP counted 565,000 more in December alone.

There is no particular reason to think ADP counted new jobs earlier than BLS, but it would offer a potential explanation if BLS reports job growth in January. Sometimes, counting is hard.

Anyone aware of a tax or transfer-payment change between 2021 and 2022 that would encourage firms to fiddle with hiring dates?

Wonder if one weak jobs report could put a hitch in the Fed’s plans. There is already reason to think Q1 GDP growth will be weak and that y/y inflation comparisons will cool in Q2. Bit of a headache for Fed folk.

Oh, and both new and used jobless claims remain very low, though up slightly in the last week, while Challenger reported the fewest lay-off announcements on record in December. Not the sort of numbers consistent with declining employment.

I’ll stop now.

Heh, I enjoy it and learn from it. Hit that “post comment” button, never stops me : )

in nys >4000 fewer staff hospital beds.

health workers refusing the jab, as well as other safety minded workers don’t claim ui when fired for refusing the mandated medical experiment….. ak an mrna treatment keyed to alpha.

biden made the collateral damage from the virus that he promised but could not defeat worse!

the eia report for week of 28 jan 2022 has huge increase in imported crude and every supply level declined well below last year except gasoline which is about even with supply last year.

imports again are up >2.0 million barrels a day than last.

So, amateur “analysts” often fall into the trap of thinking any outcome they don’t like is evidence of a mistake. Take, for instance, anonymous blaming Biden for the effects of Covid.

Covid’s effects are bad, so there must have been a mistake. The chain of tortured logic continues by trying to pin the imagined mistake on somebody. Biden didn’t cause Covid, but he’s in charge (though not in charge of Covid), so he must have made a mistake.

In order to tie this elaboration of illogical up in a neat bow, the purported mistake needs to be something over which Biden has authority. Ah, so the mistake is requiring that people who are paid partly with public money for providing safe health-care services to the public be vaccinated against an extremely contagious disease. There’s that neat little bow!

Real analysts attempt to consider not just whether a choice leads to happy times, but whether any other choice could have led to happier times. Economists often look at what are called “opportunity cost” in considering alternatives. I don’t think anonymous bothered?

But why bother with real analysis? Biden wants to take some modest steps to slow the pace of climate change. Anonymous apparently makes money from things which contribute to climate change. Blame Biden and let the world burn!

OK, I’ll stop after this one. I’m not much impressed wih one month’s ADP shocker. Water under the bridge, even if BLS data come in weak, too. I’m more worried about other stuff.

Despite a lovely headline growth figure in Q4, real final sales of domestic product rose at only 1.9% (SAAR). That’s a truer indication of underlying grow. The U.S grew only slightly better than trend in Q4 and there are at least a couple of predictable drags on growth this year. First, the end-2021 credit impulse was negative:

https://www.home.saxo/content/articles/macro/saxo-quarterly-credit-impulse-update-15012020

The global impulse has improved slightly due to China’s easing, but U.S. credit trends appear to be cooling. Lags in credit’s impact suggest global weakness in Q2/Q3, U.S. cooling in late Q2 to Q4.

U.S. fiscal policy has been contractionary since Q2 of last year and is set to remain so through 2023:

https://www.brookings.edu/interactives/hutchins-center-fiscal-impact-measure/

Meanwhile, the Fed’s tapering will amount to a steadily increasing demand on the credit system from Treasury borrowing through Q1. If private credit demand cools at the same time, upward pressure on rates from tapering will be mitigated, but still with the implication that credit-financed private activity will be cooling. If Fed policy manages to steepen the curve, the credit impulse could deteriorate further.

These are not the typical headline economic data series, but the headline series are mostly symptoms, not underlying causes. Credit data and foreseeable fiscal data are foreward-looking and causal. The U.S. economy faces headwinds this year on top of Covid problems.

Larry “I Need to Be Relevant Again” Summers and Lawyer Georgetown Jerome say we’re shooting to the moon. No worries /sarc

Moses Herzog: I think that since Larry Summers proved to be right about the extent and duration of elevated inflation, one might want to accord his views some respect, even if you wonder about the motivations.

I may be letting my personal/subjective feelings “bleed into” or “seep into” the inflation argument. But I think a big part of Larry’s arguments are that either if we had less fiscal stimulus and/or a quicker move to raise rates “we would be better off now” If you asked me was I (humbly Mr Armchair Wannabe Economist here) wrong about inflation getting this high and Mr. Summers was correct I might begrudgingly say “OK, I was wrong, Mr. Summers was right on inflation”~~but if you were to ask me a very similar question “Do you think there should have been less fiscal stimulus and more expedient moves on raising rates, don’t you think America would be better off at this juncture right now??” I think this 2nd question is ground I’m not willing to give ground on yet.

Are those two questions the same questions?? They’re pretty near to the same question, but really I think they are different questions. Those two questions are not even brothers, more like nephews or cousins~~if my analogy isn’t too weird there.

Another question that keeps making racket in my mind like an oversized piece of dice, is “How does raising rates or lessening fiscal stimulus fix GVC supply problems???~~which is most of the cause of inflation” And I keep getting a vacuous space in the answer blank on that one.

Moses Herzog: Reducing government transfers would reduce consumer spending now tilted toward goods, so lessening the amount of goods that have to be moved through the transportation system.

Fixing the problems/challenges/costs associated with fast growth by growing slowly has long been the accepted wisest course of action at the macro level. Confusingly, the wise ones who recommend slow growth as the answer to challenges will often complain about the resulting slow growth.

Yeah, but capital spending is rising. Your credit creates little real growth. The headwinds are not real economy.

When your margin of error is plus-or-minus 500,000 jobs, why is anyone surprised by this “miss”, and why not take the opportunity to learn to put a million-job margin around all these figures?

rsm: I don’t think you understand my point. The confidence interval for the change in NFP is +/- 110K.

The 60% prediction interval from my regression is about 900K – but that’s me highlighting the point that the correlation is not high, so that one should *not* infer from the ADP report a definitive change in the BLS series.

I really think you are just responding to each and every estimate by writing “margin of error” or “error bars”, without really understanding what is being written.

Have you recently taken a stats course?

Can you imagine the poor instructor who tried to teach rsm statistics? rsm does not listen – he just chirps 24/7.

The Econoday Economic Calendar shows a range forecast for the Establishment Survey, FRED series PAYEMS, at -400,000 to + 280,000 with a consensus of 150,000. Too bad the forecasters that forecast negative change of 400,000 would not give us a hint on the forecasting method. What is the adjustment that is driving the negative forecast? Is it the new Covid cases? Seems possible. Must be judgment adjustments to models for various factors. I have not made any judgment adjustments.

Well here goes the “fools rush-in” comment. Forecasting PAYEMS, I show a forecast of 197,000 with a standard error forecast from-63,000 to 457,000. The uncertainty is large. My first goal is to at least be in the Econoday spread. Second, optimum goal, is to be close to the actual report. At least goal one was achieved being in the Econoday forecast spread. The large standard error, however, casts doubt with the forecast mentioned that any change can be assumed.

A second forecast, forecasts 14 detail job categories. For the sum of the detail forecasts, I show a forecast of 222,000 for the change in jobs. Again, I made no judgment adjustments.

https://us.econoday.com/byshoweventfull.asp?fid=541713&cust=us&year=2022&lid=0&prev=/byweek.asp#top

https://fred.stlouisfed.org/series/PAYEMS

140,000 no model.

100% goofball judgement adjustment. We draw guns in 7 hours. Loser buys me a bourbon shot at the Long Branch Saloon.

For whatever it’s worth many banks have adjusted their predictions for Friday morning’s numbers downward (I did not read the ZH article until after I had made my own prediction of 140,000 ). With GS going with a negative 250k. I’m obviously not going to change my number now. But I was pretty surprised so many banks adjusted their forecasts downward and it even changed the consensus number pretty drastically.

@ AS Your number beat a lot of the banks’ forecasts and obviously beat mine. Hats off from Roy Harper.

Moses,

Thanks for the comment. It is fun to try to match the experts.

Omicron driven illusion. Come back by the March report……all recovered.