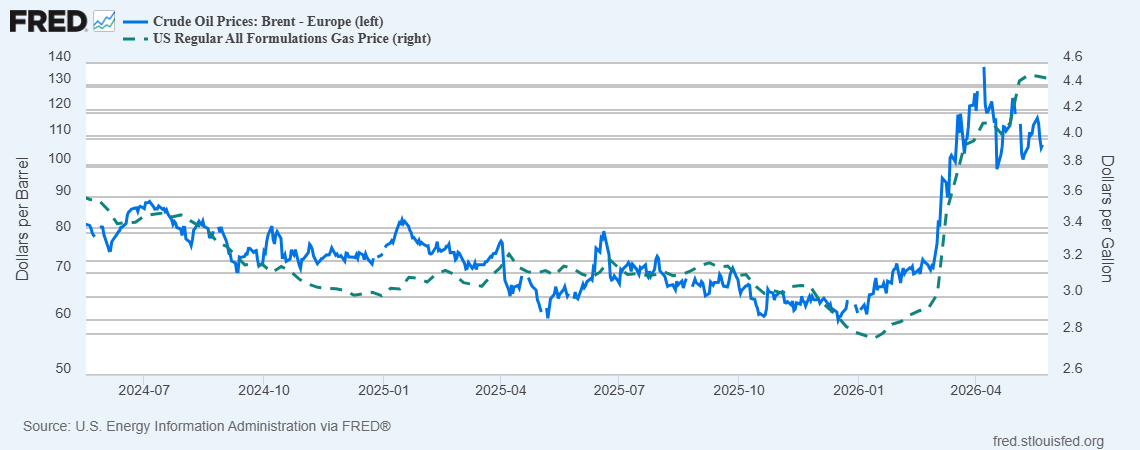

Gasoline prices through Monday, vs. Brent. Why the divergence?

Both prices are depicted using log scales. It’s clear it’s not a one-for-one relationship, but the gap is interesting. I don’t know if this is the reason, but the gasoline (and distillates) stocks are way down (for week ending 5/22).

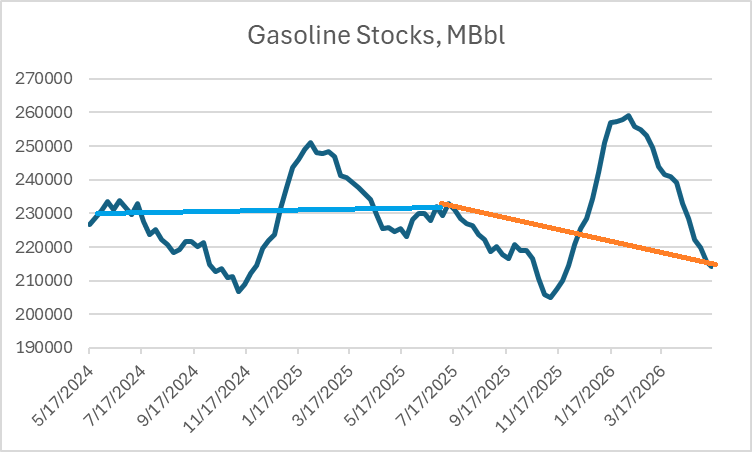

Figure 2: Gasoline stocks end-of week, Mbbls, n.s.a. (blue). Source: EIA.

I’ve drawn year to year trends, since the data are not seasonally adjusted.

Rocket-and-feather?

Though when I look at these two series back around 2022, I don’t see any similar rocket-and-feather behavior in gasoline.

One additional detail which might matter here. The Brent/WTI spread is back to normal at around 5 bucks. That’s partly because transit times for North American crude to Asia are shorter than for Brent, and Asian buyers have had time to make the adjustment. Compare WTI to gasoline and the gap may not be so pronounced.

Off topic – In non-war news, China is taking steps to prevent capital outflow:

https://www.msn.com/en-us/money/other/china-cracks-down-on-overseas-investing-after-record-1-trillion-capital-flight-to-us-hong-kong-markets/ar-AA24aXMj

So naturally, Chinese investors have stepped up the pace of offshore investing:

https://www.bloomberg.com/news/articles/2026-05-25/china-traders-rush-for-exit-after-cross-border-flow-crackdown

According to the first link, a net $1 trillion left China last year, nearly matching the $1.2 trillion trade surplus. Now, I recall reading somewhere that the current account and capital account have to balance, so I’m not sure this trillion-dollar outflow is inexplicable or even odd.

The thing which apparently has Chinese regulators worried is that so much of the outflow is headed into Hong Kong stocks:

https://www.benzinga.com/Opinion/26/04/52124632/how-chinas-trade-surplus-is-floating-hong-kong-equities-even-as-western-bulls-retreat

The Hang Seng is up 7.5% from a year ago, but down nearly 10% from its late January peak, suggesting that Chinese authorities are closing the barn door after the horse is already out. All of which seems just the normal to-and-fro of financial markets, unless China suffers enough capital flight to cause spill-over to other markets, or takes further steps to prevent outflow, and those steps spill over.

China is big now, and generates big flows, so spill-over to other markets can be big. Also, incidentally, capital controls are antithetical to reserve-currency status; maybe that’s why Iran wants oil tolls paid in cryptocurrency, not yuan.

Yeah, but no. Calling that capital is erroneous. Its debt. Nor is it alot.

Oh, you’re one of those guys. Bouncing around the internet, trying to pretend you know stuff.

The Hang Seng is an equity exchange. Equity, not debt. Income from exports is an asset, not debt. I don’t know which of these you’ve mistaken for debt, but it’s as wrong as wrong can be. Silly mistake.

A trillion dollars is not a lot of money? At the end of April, the market cap of the Hang Seng was just under HKD 48 trillion. That’s about US$6.25 trillion. China’s GDP is about $21 trillion. You don’t think $1 trillion is much money? You’re new at this, aren’t you?

GDP is not total capital. China’s capital base is over 100 trillion of mostly debt. US over 300 trillion of all debt.

GDP is a flow. Capital outflow is a flow. China’s capital stock is a stock. You’ve confounded sticks and flows. Rioky mistake.

The Great Pyramid at Giza is built out of rocks. It’s big. Only a fool would look at it and say “That’s not a lot of rock. The earth’s crust is much bigger.” That’s kinda what you’re doing.

There are press reports of a tentative peace deal, good for 60 days while unsettled issues are negotiated. In other words, Big Boy negotiations, instead of the my-way-or-the-highway crap we’ve seen so far. The war-criminal-in-chief hasn’t signed on yet, so we’ll see:

https://www.nytimes.com/2026/05/28/world/middleeast/iran-us-agreement-plan.html

Naturally, the remaining issues are nuclear stuff and control of Hormuz. Iran apparently has agreed to allow ships through Hormuz for 30 days of the 60-day ceasefire negotiating period; whether tolls must be paid is not clear, but the U.S. position and international law both say no tolls, so I’m guessing no tolls for 30 days.

That’s because the deal doesn’t exist.

For those keeping score, Vance, the administrations resident peacenik, is talking about the deal, not Rubio. Another epusode if The Apprentice – White House Style.

Presumably Rubio will threaten Cuba real soon.