Today, we’re fortunate to have Alex Nikolsko-Rzhevskyy, Assistant Professor of Economics at Lehigh University, David Papell and Ruxandra Prodan, respectively Professor and Clinical Assistant Professor of Economics at the University of Houston, as Guest Contributors

The “Federal Reserve Accountability and Transparency Act of 2014”, introduced into Congress on July 7, requires the Fed to adopt a policy rule. It actually specifies two rules. The “Directive Policy Rule” would be chosen by the Fed, and would describe how the Fed’s policy instrument, such as the federal funds rate, would respond to a change in the intermediate policy inputs, presumably inflation and one or more measures of real economic activity such as the output gap, the unemployment rate, and real GDP growth. If the Fed deviated from its rule, the Chair of the Fed would be required to testify before the appropriate congressional committees as to why it is not in compliance. In addition, the report must include a statement as to whether the Directive Policy Rule substantially conforms to the “Reference Policy Rule,” with an explanation or justification if it does not. The Reference Policy Rule is specified as the sum of (a) the rate of inflation over the previous four quarters, (b) one-half of the percentage deviation of real GDP from an estimate of potential GDP, (c) one-half of the difference between the rate of inflation over the previous four quarters and two, and (d) two. This is the Taylor rule, and is obviously not chosen by the Fed. John Taylor has recently discussed this proposed legislation on his blog and in Congressional testimony.

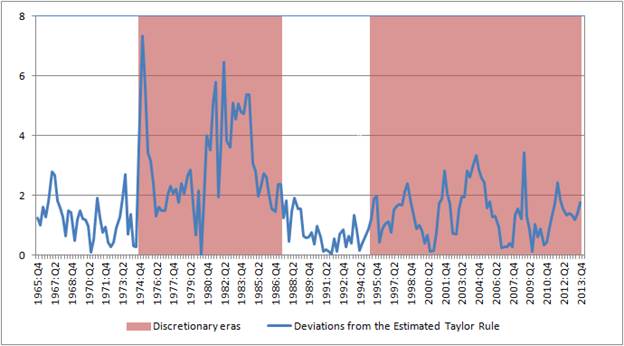

What is the justification for using the Taylor rule as the Reference Policy Rule? We recently presented a paper, “Deviations from Rules-Based Policy and Their Effects,” at a conference on “Frameworks for Central Banking in the Next Century” at the Hoover Institution. Using real-time data on inflation and the output gap from 1965 – 2013, we calculate policy rule deviations, the absolute value of the difference between the actual federal funds rate and the rate prescribed by (1) the “original” Taylor rule described above, (2) a “modified” Taylor rule with a coefficient of one, instead of one-half, on the output gap, and (3) an “estimated” Taylor rule from a regression of the federal funds rate on a constant, the inflation rate, and the output gap. We use the shadow federal funds rate in Wu and Xia (2014) to capture the effects of unconventional monetary policy after 2008. The estimated Taylor rule has almost the same coefficients on inflation and the output gap as the original Taylor rule, but a lower intercept, which is consistent with either an inflation target higher than two or a lower equilibrium real interest rate. Janet Yellen has expressed her preference for the modified Taylor rule over the original Taylor rule.

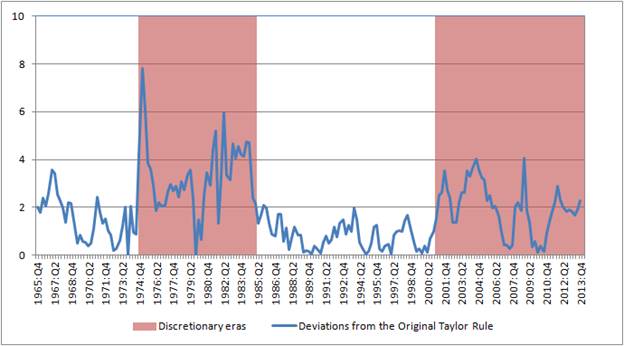

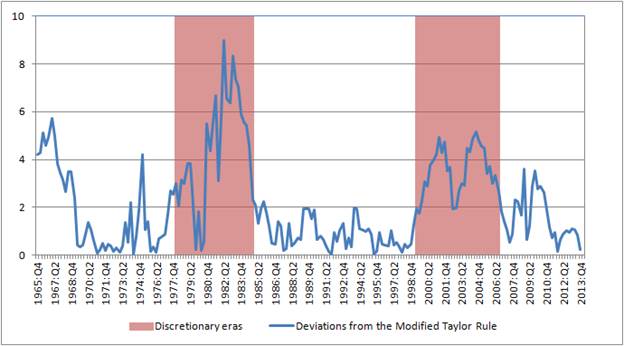

We identify monetary policy eras by allowing for changes in the mean of the policy rule deviations with tests for multiple structural breaks and tests for multiple restricted structural changes, which restrict the mean of the deviations in the small and large deviations periods to be the same. The results are depicted in Figure 1, with discretionary eras defined by large deviations and rules-based eras defined by small deviations. The original Taylor rule produces rules-based eras for 1966 – 1974 and 1985 – 2000 and discretionary eras for 1974 – 1984 and 2001 – 2013. For the modified Taylor rule, the first discretionary era starts in 1977 and there is a significant break in 2006:Q3, producing an additional rules-based era for 2007 – 2013. With the estimated Taylor rule, the last break for the restricted and unrestricted tests is very different and the last discretionary era runs from 1995 – 2013. The result that policy during 2007 – 2013 is discretionary according to the original Taylor rule and rules-based according to the modified Taylor rule is consistent with Fed policy since 2008 being more stimulative than would be warranted by the original Taylor rule.

Figure 1. Structural Change Tests for Taylor Rule Deviations

A. Original Taylor Rule: Restricted Structural Change Model

B. Modified Taylor Rule: Restricted Structural Change Model

C. Estimated Taylor Rule: Structural Change Model

We proceed to analyze the effects of deviations from rules-based policies by comparing the economic performance between our rules-based and discretionary eras. Using six loss functions involving inflation and unemployment: Okun’s misery index, a linear absolute loss function, and four quadratic loss functions, we show that economic performance is uniformly better in rules-based than in discretionary eras. The results, reported in Columns 1 and 2 of Table 1, hold for all three rules and are robust to specifications of quadratic loss functions that put greater weight on either inflation or unemployment loss and to a specification that puts all weight on inflation loss.

While economic performance is always better in rules-based eras than in discretionary eras, the effects of the deviations differ systematically among the rules. The ratio of the loss during discretionary eras to the loss during rules-based eras is reported in Column 3 of Table 1. The loss ratio is largest for the original Taylor rule, next largest for the modified Taylor rule, and smallest for the estimated Taylor rule. The results in Table 1 are robust to deleting the periods when Paul Volcker raised the federal funds rate more than two percentage points above the Taylor rule benchmark in order to bring down inflation and restore Fed credibility, which arguably should not be classified as part of the discretionary eras. Using the original Taylor rule as a benchmark provides the sharpest evidence of the negative effects of deviating from policy rules.

How does this relate to the proposed legislation? Our evidence that, regardless of the policy rule or the loss function, economic performance in rules-based eras is always better than economic performance in discretionary eras supports the concept of a Directive Policy Rule chosen by the Fed. But our results go further. The original Taylor rule provides the strongest delineation between rules-based and discretionary eras, making it, at least according to our metric and class of policy rules, the best choice for the Reference Policy Rule.

In the current political climate, the proposed legislation will inevitably be interpreted in partisan terms because it was introduced in the House Financial Services Committee by two Republican Congressman. Not surprisingly, the first reporting on the legislation by Reuters was entirely political. This is both unfortunate and misleading. We divided our rules-based and discretionary eras with the original Taylor rule between Republican and Democratic Presidents. If we delete the Volcker disinflationary period, out of the 94 quarters with Republican Presidents, 54 were rules-based and 40 were discretionary while, among the 81 quarters with Democratic Presidents, 46 were rules-based and 35 were discretionary. Remarkably, monetary policy over the past 50 years has been rules-based 57 percent of the time and discretionary 43 percent of the time under both Democratic and Republican Presidents. Choosing the original Taylor rule as the Reference Policy Rule is neither a Democratic nor a Republican proposal. It is simply good policy.

This post written by Alex Nikolsko-Rzhevskyy, David Papell and Ruxandra Prodan.

The Fed has to work in the future economy, because of lags in the adjustment process. Moreover, there are positive and negative shocks to the system in the short-run that require adjustments in the money supply, e.g. in recent years, technology shocks, Y2K, 9-11, oil shocks (or commodities in general), the creative-destruction process (mostly from 2000-02), the financial crisis, etc..

Also, I may add, it seems, Friedman believed Greenspan was an excellent Fed chairman:

AN INTERVIEW WITH

MILTON FRIEDMAN

Interviewed by John B. Taylor

Stanford University

May 2, 2000

Taylor: Well, whatever the break point is, why do you think things have changed? Why, as you put it, does the Fed seem to be operating the monetary-policy thermostatic regulator so much better now? What do you think the reason is?

Friedman: I’m baffled. I find it hard to believe. They haven’t learned anything they didn’t know before. There’s no additional knowledge. Literally, I’m baffled.

Taylor: What about the idea that they have learned that inflation was really much worse than they thought in the late 1970’s, and they therefore put in place an interest-rate policy that kept inflation in check and reduced the boom/bust cycle?

Friedman: I believe that there are two different changes. One is a change in the relative value put on inflation control and economic stability and that did come in the eighties. The other is the breakdown in the relation between money and GDP. That came in the early nineties, when there was a dramatic reduction in the variability of GDP. What I’m puzzled about is whether, and if so how, they suddenly learned how to regulate the economy. Does Alan Greenspan have an insight into the movements in the economy and the shocks that other people don’t have?

Taylor: Well, it’s possible.

Folks: correlation != causality.

All you have achieved is you have shown is that good economic times are compatible with the Taylor rule. That is, you have shown that the Taylor rule does not prevent prosperity. There is no evidence in this post that had we followed the Taylor rule during tough economic times that things would have been better, yet that is the policy implication you want us to take away. This feels deceitful / manipulative.

You should be clear about the policy implications of this work:

1) the Fed has often not followed the Taylor rule during tough economic times;

2) there is no reason to think that following the Taylor rule would have made things better, so there is no evidence here supporting the proposed legislation.

Kenneth Duda

Menlo Park, CA

kjd@duda.org

This. I thought I was taking crazy pills. Was this abuse of econometrics really worthy of crafting into a paper?

Even though it’s a good point, it could be applied to pretty much every single empirical result out there; we can never be sure we are indeed getting a causal effect. The correlation that we found does not lead to the conclusion that there is no causality. In order to find evidence of causality we would need a model. As John Cochrane discussed in his blog (http://johnhcochrane.blogspot.com/2014/06/taylor-rules.html) there is no model of the economy that policy people use to think about how monetary policy affects the economy.

Also, to some extend, we tried not to “encourage” reverse causality. One usually thinks that during good times, shocks are small. In a previous study, using a Markov Switching model, we have also allowed the mean and variance to switch independently. Hence, we made sure that our state distributions are not driven by good times/bad times. That didn’t change our findings.

Asset price bubble 2000. Shock to economy. Asset price bubble 2007. Bigger shock to economy. Asset price bubble emerging again 2014. Quick, sacred priesthood, all together now, one, two, three, count number of angels on pinhead of our new version of Taylor rule … and let’s do it all again!

LOL! Careful, JBH, with that pin around all the bubbles The Chair is unable to see floating in front of her face.

Perhaps we could all pitch in for an eye exam and new prescription for her eyeglasses.

But, seriously, similar to the desire to be the POTUS, who would want her job? As a politician charged with having to constantly run political cover for an int’l criminal banking syndicate, whenever she opens her mouth we know she’s lying about something to cover the banksters.

But the banksters chose The Chair, as they did Bubble Ben Shalom Zimbabwe, to present a benign, professorial, kinder, and gentler political cover for their license to acquire the gov’t and to persist in their colossal plunder. Sir Greenscam was arguably the biggest fraud the banksters perpetrated on humanity in the Fed’s history, yet he has been canonized while still among the living as an irreproachable saint.

My response: http://worthwhile.typepad.com/worthwhile_canadian_initi/2014/07/taylor-rules-again.html

I took 5 minutes to glance through the paper, so I’m not conversant with it, but my reaction was correlation of loss functions to discretionary periods showed mostly that there were reasons for the discretionary periods.

First, I agree with Nick Rowe’s analysis (from his link, read it). But, what does this, from the guests, mean;

‘The “Directive Policy Rule” would be chosen by the Fed, and would describe how the Fed’s policy instrument, such as the federal funds rate, would respond to a change in the intermediate policy inputs, presumably inflation and one or more measures of real economic activity such as the output gap, the unemployment rate, and real GDP growth. ‘

Inflation is an ‘intermediate policy input’?

Patrick: The normal words for “intermediate policy input” (in my experience) are “monetary policy indicator”. For an inflation targeting central bank, inflation is both an indicator and a target. The Bank looks at past inflation (along with other data) as an indicator, before choosing where to set its interest rate instrument, to hit its future inflation target.

That quoted passage, in normal language, means the Fed must specify its instrument reaction function in advance, and stick to it, so it becomes a de facto instrument rule, and explain why it’s not the same as the Taylor Rule.

Why don’t they just require the Fed to specify its target rule, and justify it, like all other sensible countries do? And then hold the Fed accountable for hitting its target rule. Does Congress care about the instrument, or the target?

The Fed follows the dictates and reserve needs of the TBTE bankster owners of the Fed, not the converse; that’s the rule.

If this were conceded and internalized, it would follow that markets, politicians, and the public would then require scrutiny of the values, objectives, desires, and expectations of the TBTE bankster owners of the Fed, as well as full transparency and disclosure of the banksters’ communications with, and influence on, Fed governors, bank presidents, and The Chair of the central bank they own.

This would, of course, end the Fed’s “independence”, which is another way of saying the Fed’s statutory privilege granted by the gov’t they own to run political cover for the TBTE banks’ owners license to plunder labor product, profits, and gov’t receipts for social goods in perpetuity.

Were even a small plurality of the public to understand fully the Fed’s role, motives, actions, and true purpose, the Fed’s credibility and legitimacy would evaporate and the institution would cease to exist along with the Fed’s owners’ privilege to plunder.

Let’s not dictate to the doctors on how the treat the patient.

Steven, it’s arguably more like taking care not to pi$$ off the banking syndicate’s organized crime capos by exposing their machinations, or risk being reported to the godfathers of the bankster syndicate who will promptly have delivered a severed horse’s head for one’s pillow.

That the TBTE int’l banking syndicate has been demonstrated to be involved in money laundering, fixing markets, defrauding borrowers, their clients, and the gov’t, arms and drug trafficking, political coups, murder for hire, white sex slavery and child porn, bribing of political officials, and who knows what else, it is not hyperbole or a misplaced description to describe the enterprise as a criminal syndicate. And these guys own the gov’t; therefore, by extension, the gov’t operates as a kind of enabler, facilitator, and protector of the criminal banking syndicate.

These guys are now so above the law and untouchable that they are likely not threatened by such revelations or “accusations”. They might even get the occasional good knee-slapping laugh that a growing share of the public is learning about their activities but can do next to nothing about it, making most of us either witting or unwitting criminal conspirators or unwilling marks or victims of the syndicate.

BC: Why has not one Tier I bank official been indicted for fraudulent activity contributing to the 2008 collapse, while hundreds of Tier II banks have been shut down by the regulators? Why have no government regulators themselves been publicly called on the carpet and/or indicted? Why has not one politician been brought up on ethics charges in the House or Senate for sanctioning the shabby work of regulators and setting up the very framework that led to the crisis starting as far back as 1995 with the Homeownership Act? Why have governors and presidents of the Fed itself gotten off Scott Free? Greenspan, Bernanke, and many other FOMC members recklessly created massive liquidity from around 2000 on, a necessary condition for the credit bubble to gain traction, ignoring internal Fed advice including that of a since deceased Fed governor who published a book about the danger of these very excesses including subprime. Lastly, the vast silence of money, banking, and macro economists in academia. They who were culpable in teaching Greenspan and entire generations this bad economics, including Congressmen who, based on what they’d learned at the university, were responsible for overseeing regulators and thus Wall Street.

Your comment points the way to a tentative answer! When will readers including academics open their minds – open-mindedness being the key requisite of science – and awaken to what is really going on?

JBH, those are the right questions.

It is no revelation that establishment academe and the sycophantic financial media influentials are in their positions of legitimacy, credibility, and status because they have internalized the rentier-parasitic mindset and are content to be paid well to perpetuate the system in their self-interest on behalf of the rentier Power Elite.

Of course, some are true believers, whereas I suspect most simply go along to get along to earn a good living to pay the mortgage on the McMansion in the gated enclave, the payments for the European luxury vehicles, the private school tuition for their offspring, the holidays in the tropics and Europe, their wives’ cosmetic improvements, and the like. Take away those bourgeois trappings and inducements, and they will likely squeal.

The art of sophistry pays much better than truth telling, and it arguably always has.

It has been said that one cannot cheat an honest man, and if a man were paid what he is worth for telling the truth, then he increases the value of all other honest men who can then live an authentic life with trust. But a dishonest man (or group or society) gains his advantage by lying, which reduces most every other man to being dishonest merely to compete. When virtually everyone one encounters is conditioned to deceive, dissemble, and obfuscate in order to gain a social, financial, economic, or political advantage, one is at a great disadvantage if one does not learn such social skills.

The rentier-parasitic zeitgeist now dominates the English-speaking world, having in the past 10-20 years spread to China and the Asian city-states. Now the rentier-parasitic caste has virtually 100% claim on all wages, profits, and gov’t receipts in perpetuity via imputed compounding interest on total credit market debt and other financial assets they disproportionately own. When the rentier-parasites are small in number and influence, their ambitions are checked by competing forces. However, when they achieve dominance, the society is overcome by the parasitic affliction and risks the parasitic disease destroying the host society. As the host society dies, the parasites often turn on one another to survive.

The world has experienced countless episodes throughout history when an infinitesimally small rentier-parasite group/caste gained overwhelmingly disproportionate influence, credibility, legitimacy, power, and control, and it has happened yet again with a similar outcome. The question now is how the rentier-parasites will be singled out, blamed/held accountable, and brought to justice/injustice by the aggrieved bourgeois caste and then the masses this time around, and when.

https://www.youtube.com/watch?v=vjY5Y-eQZTw

The Taylor Rule seems to suggest the economy is accelerating right now. I would laugh my butt off if Taylor came on the news and said the economy is surging right now and if we don’t slow it down, it will develope into a investment bubble. Corporate profits turning down is another sign, of course this can last for awhile to they are depleted, then the bubble pops.

Rage, oil and gas extraction is growing at 3-5 times the rate of mfg., which is skewing the IP figure much higher than otherwise.

Were oil and gas extraction to be growing at the rate of overall mfg. and IP, the rate of IP would be at 1-1.25% instead of 3-3.5%.

Peak Oil is causing the shale (and energy-related transport) boom/bubble to fool many into believing that the US economy is stronger than it is, even as real wages/incomes are not growing q-q annualized.

The most important thing that the “Federal Reserve Accountability and Transparency Act of 2014″ tells us is that there is broad recognition that the current micro-managing of the economy is not working. This was admitted by Ben Bernanke as he constantly sought new ways to implement QE and it has been admitted every timg Janet Yellen has testified before congress as she repeats that the economy is still struggling. The “recession” has been over for around 5 years and yet nothing the congress and the FED has done has bought recovery.

But what is also amusing about the “Federal Reserve Accountability and Transparency Act of 2014″ is that it is a move toward the real solution but is still far from the optimal action. We need not a rules based economy but an economy with a currency with a firm anchor. But as the debate above tells us we are still looking at a slippery, manipulated system even with a Talor Rule. Is it the original Taylor Rule, or is it the modified Taylor Rule, or is it the estimated Talor rule, or do we simply flip from one to the other based on the whims of the FED chair? Wouldn’t it be amazing if our “philosopher kings” were to actually heed Adam Smith: “Little else is requisite to carry a state to the highest degree of opulence from the lowest barbarism, but peace, easy taxes, and a tolerable administration of justice; all the rest being brought about the natural course of things. All governments which thwart this natural course, which force things into another channel or which endeavor to arrest the progress of society at a particular point, are unnatural, and to support themselves are obliged to be oppressive and tyrannical.

We would be wise to stop playing with rules based manipulation and actually anchor our currency to gold, then get the FED out of all the other meddling it does..

Ricardo, we have had a “recovery” . . . from a Great Depression-like contraction in 2008-10. However, what’s missing is the “expansion” phase of the business cycle.

And, yes, the massive reserve printing and crediting banks’ balance sheets with book entry profits at a record to total profits and as a share of GDP not only have not resulted in a typical reflationary expansionary business cycle effect, but cumulative compounding interest to total credit market det outstanding to average term is at 100% of GDP in perpetuity, and net annual claims to the financial sector exceed growth of annual nominal GDP.

Add to that the effects of oil consumption to final sales at the recessionary level and Boomer demographic drag effects on consumer spending, and real final sales per capita cannot grow. Period.

Ricardo nails it again. Essentially, activist, unpredictable monetary policy, responding to political winds, simply adds more uncertainty to an already complicated global economy. It might get lucky some time, but, as we have seen so severely, it might lead to horribly destructive asset bubbles. We are now trading the Yellen put.

No Ricardo is wrong. “The “recession” has been over for around 5 years and yet nothing the congress and the FED has done has bought recovery.”

Congress and the Fed need to do more seeing as the private sector is stagnating. The only way the private sector won’t stagnate is for the banks to push bad loans like they did during the housing bubble. To the extent that the economy has improved it is because of help from the government: Obama’s stimulus and Fed policy. But Congress has forced austerity on Obama and the Fed exited from QE too soon. To call it the Yellen “put” is just another way of saying that the free market isn’t working.

You guys are just distorting historical facts. Policy has moved to the right since the Reagan era and today’s economy is the result.

http://online.wsj.com/articles/alan-s-blinder-an-unnecessary-fix-for-the-fed-1405639582

Blinder on why the Taylor rule is a bad idea.

Question about the discretionary era, 1974 – 1984, Especially the period form 1974 to when Volker came in. Was the problem discretion as suggested by Taylor in 1999 ((A Historical Analysis of Monetary Policy Rules) or was it a problem with overestimating productivity as suggested by Orphanides? Would the proposed legislation inhibit something like the latter from happening again?

smg

There are three possibilities: sound money backed by something tangible, fiat money guided by a Taylor rule or equivalent, and pure discretion. Sound money took wings in 1971. Discretion complimented by the Taylor rule began guiding policy sometime in the 80s even before the publication of John Taylor’s rule, but since the crisis the policy of ZIRP and QE are again guided completely by discretion.

The primary economic problem is in seeing that the natural economic cycle unfolds so that the path of long-term potential growth is maximized in a sustainable way. Most of the rest of the economic problem devolves on the schools of business and business management to scientifically inform society on how to increase productivity at the micro level. The micro always happens within the macro framework. The macro environment has lashed the micro by cycles of unnecessary amplitude and length. The singular cause of this has been unsound money, where credit and debt is subsumed in this definition. That is, if money were truly sound the banking system could not increase credit beyond its natural healthy limit. Credit crunches and credit bubbles would be insignificant froth on top of the healthy natural cycle.

Taylor proposed a rule to guide policy in this fiat environment. This rule is sadly deficient because there is no third variable in the Taylor equation to account for asset prices. The proposed legislation is therefore just as sadly deficient. The immensely powerful Federal Reserve, in any case, is never going to be bound by such rules. If you will but inform yourself by reading von Mises, Hayek, Rothbard, Fekete (Pillars of Money and Credit), you will eventually conclude there is no substitute for sound money. It will take considerable effort on your part to fully grasp this, because in the process you will also have to truly understand the business cycle. And that is not going to happen until you emptied your mind of much of what mainstream economics has to say about the cycle. The mainstream was pig ignorant and blind going into the Great Recession, if that helps any.

As someone who visits this site, you yourself likely have as much knowledge on this matter as the average member of Congress. If you are in the dark, they as a body are too. No help from this quarter.

Two events are on the horizon. I cannot at this point predict which one will win out nor the timing. One, some form of sound money will arise in the non-Anglosphere to eventually displace this sphere’s pure fiat money. The second is a crisis so catastrophic that the emperor will be revealed to have no clothes and the public will revolt.

Labor force, population, and real labor productivity imply a potential real GDP hereafter at closer to 1.4% and less than 1% per capita, so the 3% and 2.6% potential rates through 2020 and 2024 respectively estimated by the CBO are highly unlikely.

And how to justify a 2% real funds rate during a debt-deflationary regime with no growth of bank lending and deposits after bank cash assets/reserves?

The IGM forum (Chicago Booth School) asked its panel of experts whether enacting the Taylor rule legislation “would improve monetary policy outcomes in the U.S.” Not one of these economists agreed with this proposition.

http://www.igmchicago.org/igm-economic-experts-panel/poll-results?SurveyID=SV_doNZ9FbNq7tDi97

Asset booms and busts are unimportant.

What’s important is sustainable growth, of goods & services, which is optimal growth.

The Fed has done an increasingly better job at smoothing-out both long-wave and short-term business cycles, particularly since the U.S. went off the gold standard, causing faster growth.

Economic boom/bust cycles are inefficient, both in the boom and bust phases, because of periods of strain and slack.

PeakTrader, Growth rate 20 years prior to going off gold August 1971 – 3.6%. Growth 40-some years since – 2.8%. Growth latest 10 years – 1.5%.

Peak, since the 1970s, the US has become deindustrialized and hyper-financialized, experiencing one financial and commodity price bubble and bust after another, with real wages no higher than 40-45 years ago, and debt to wages and GDP at a record high. The economy is so financialized that net annual flows to the financial sector exceed annual nominal GDP growth, and total imputed interest to total debt is now 100% of GDP in perpetuity.

The Fed has done no such thing as you describe, which remains a persistent fallacy incessantly promoted by sycophants and shills of the Fed, TBTE banks, and Wall St. We don’t need more of them, for goodness sake.

In fact, the Fed has facilitated the obscene wealth and income inequality, massive asset bubbles, and the associated financialization and hopelessly debilitating debt service burden.

Your entire statement is misleading or incorrect.

The Fed reduces income inequality by smoothing-out business cycles, to maintain sustainable growth, and keeping the country near full employment, ceteris paribus.

Per capita real income, real compensation, and even median real income are much higher.

For example, real median household income doesn’t rise steadily over time. There was a steep rise over five years in the 1990s, including when actual output exceeded potential output, when the Baby Boomers were at their prime, rising from $49,000 to $56,000.

However, it generally maintained that steep 1990s rise, falling to $54,000 and almost rising to $56,000 again in 2007.

It has declined from about $56,000 in 2007 to $51,000 today, over this unnecessary depression.

Chart: http://research.stlouisfed.org/fred2/graph/?g=qHy

Peak: https://www.youtube.com/watch?v=vjY5Y-eQZTw

The U.S. had a long-wave bust cycle from 1973-82, a long-boom from 1982-07, and a recession/depression after the economy peaked in 2007.

Average annual per capita real GDP growth:

1973-82: 0.99%

1982-07: 2.30%

2007-12: -0.03%

Source: BEA

And, there are many factors that influence growth.

Economic booms & busts, feasts & famines, floods & droughts, etc. are suboptimal to a larger extent.

And, it should be noted, U.S. average annual per capita real GDP growth in the “long-boom” doesn’t fully capture the vast improvements in living standards, labor standards (or working conditions), and environmental standards, since the U.S. consumed up to $750 billion a year more than it produced in the global economy.

The U.S. has been a “black hole” in the global economy, attracting imports and capital, and even attracting the owners of that capital themselves.

Peak, most US “imports” are from US supranational firms’ foreign subsidiaries’ production and their contract producers.

If one accurately accounted for US firms’ foreign neo-imperial production structure, the US trade deficit is virtually non-existent ex oil, with some of that coming from US oil companies’ extraction and processing abroad.

Wall Street and Corporate America created enormous value, in the U.S. economy, through efficiencies in production and “gains-in-trade” during the height of the Information Revolution, from 1982-07.

More output, with more market power, was produced with fewer inputs; older industries, with declining prices, were offshored and those goods were imported at lower prices and higher profits; and our trading partners exchanged valuable goods for worth less dollars (rather than for U.S. goods).

Enormous resources (e.g. labor and capital) were freed-up and flowed into emerging industries and high-end manufacturing. Consequently, the U.S. not only leads the world in the Information and Biotech Revolutions (in both revenue and profit), it leads the rest of the world combined, while U.S. manufacturing as a share of world output remained roughly constant at 20%, although huge trade deficits raised our trading partner’s output.

The only way to move from one economic revolution into the next is through employing limited resources more efficiently, including through specialization and trade.

Here is an interesting commentary that makes many of the same points that I made in my post above. Those who believe our policies will lead to recovery almost to a man say that the reason the recovery is sluggish is because the FED has not done enough blood-leting. More and moe people are seeing that the actions of the FED are actually preventing recovery and the US economy on the same path as the Japanese economy.