The Senate parliamentarian ruled the trigger to prevent a revenue shortfall as unacceptable, thereby temporarily stymieing the bill.

This is just as well, as the trigger would have been procyclical, raising tax rates if the economy hit a recession. The current working concept — to reduce the tax reduction by $350 billion — makes a lot more sense from a macroeconomic perspective.

That’s because we’re already at full employment. Cutting taxes in this situation risks overheating the economy if the Fed does not respond, and worsening trade deficits if the Fed does not.

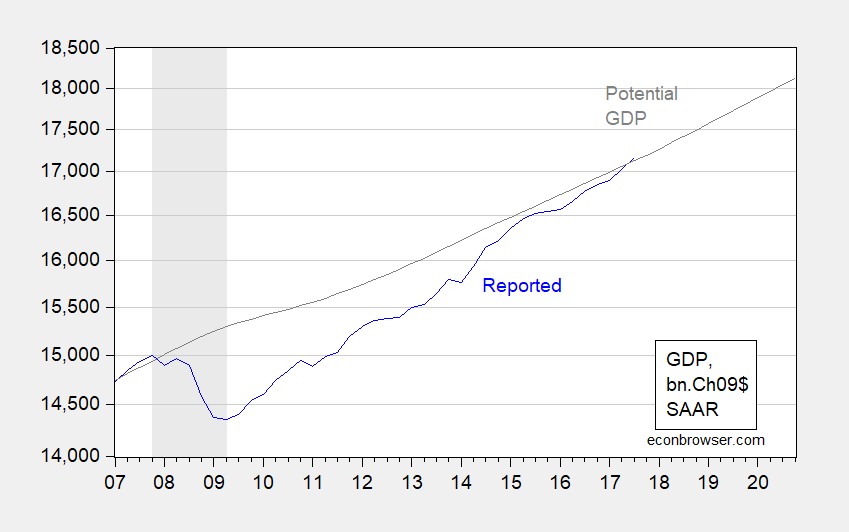

Figure 1: GDP (blue) and potential GDP (gray) in bn. Ch.2009$ SAAR, on log scale. NBER defined recession dates shaded gray. Source: BEA, 2017Q3 3rd release, and CBO (June 2017).

So, the smaller, the better. Of course, even better would be a revenue neutral, progressive, tax reform, but I don’t see anything like a middle-class friendly package coming from this group.

When the assumption is the output gap is closed or the country is at full employment, then lower corporate and income taxes designed for business start-ups and expansions, along with more foreign capital inflows, won’t have much of an effect on growth. However, if there’s substantial unproductive labor and capital, then we can expect a big boost in growth, e.g. employed labor, the capital stock, productivity, and wages.

The title “The Umpire Strikes Back” is appropriate. May the Force be with the GOP to fight the Dark Side – The Return of the Economy should be the next episode 🙂

I’ve stated before, although there has been some destruction of potential output from Baby-Boomers aging – the last of them will reach 65 in 2029 – it doesn’t explain the sudden, substantial, and sustained downshift in GDP:

https://www.advisorperspectives.com/dshort/updates/2017/11/29/q3-real-gdp-per-capita-2-53-versus-the-3-30-headline-real-gdp

And, it should be noted, older workers are working longer (the second most productive group is the 55 to 64 age group, based on education, training, and experience). Moreover, the children of the Baby-Boomers are reaching “prime-age” (35 to 54), similar to the Baby-Boomers in 1982-00.

the graph shows the output gap has closed. not sure how tax cuts would be appropriate under this condition? in addition, tax cuts coupled with tighter fed policy seem to be working against one another. as the output gap closes (and perhaps overheats), shouldn’t we be considering tax increases rather than cuts, to address the rising debt? there really seems to be no justification for a tax cut at this point in time, other than for ideological reasons. certainly not economic reasons.

Q4 GDP forecasts

NY Fed: 4.0% (+0.3% week on week) Wow!

Atlanta Fed: 3.5% (+0.8% week on week) Also wow!

You’re essentially putting your money on GDP growth.

I am running the numbers, and it is hard to overstate how bad the fundamental fiscal picture is.

…productivity growth…

i think you are referring to voodoo economics and the trick down theory?

Not necessarily. Peak is right about growth collapsing unnecessarily. But even if I put growth back at 2.5%, the budget is still a mess, and that’s without the tax bill.

I have to say, the Obama administration left the budget in truly execrable condition. Healthcare and related social spending is not slightly beyond the country’s means, but unaffordably so. Even with stiff tax increases, you’re still looking at nominal one-time cuts of 15% to Medicaid, Medicare and Other Mandatory, and after that, you have to hold the increases to less than nominal GDP growth. It’s really a mess.

And now we have the Republicans looking to pour some gasoline on the fire.

“Peak is right about growth collapsing unnecessarily.”

please explain.

See the link.

https://www.advisorperspectives.com/dshort/updates/2017/11/29/q3-real-gdp-per-capita-2-53-versus-the-3-30-headline-real-gdp

Steven, i am curious why it is unnecessarily? You may not want something to happen, but does that qualify it as unnecessarily? Especially within the context of that statement? The implication is we could stop it if we wanted, but chose not to do so. I do not believe that is true in any sense. Hence my request for explanation. As for the drop in GDP per capital, that probably has much to do with the demographics of who is entering and leaving the workforce. As boomers are forced into retirement, they are moving from (over) paid salary positions to much less retirement income. The up and coming millennial are paid much less, and this will result in a net drop in consumer spending. Looking at the output gap per capita rather than overall may be misleading without the context of baby boomer/millennial demographic shift.

PeakTrader Please, please, please ask Santa for a decent macro textbook. You’re hopelessly confused. For all practical purposes the economy is already at full employment. And whatever small gap there is will definitely be closed by the time the tax cuts kick in.

The first lesson you need to focus on is the difference between growth intended to close the gap between actual and potential GDP (i.e., an aggregate demand problem) and changes in the long run growth rate of potential GDP. Along a balanced growth path an increase in the capital stock results in a one time increase in the level of output but it does not result in a permanent increase in the growth rate. Got that? Levels versus rates. Over the long run there are only two factors that increase the growth rate along a balanced growth path: increases in the size of the labor force and multi-factor productivity (i.e., technology broadly understood). The growth rate of the labor force is a function of biology and immigration policies. Trump’s immigration policies will shrink that growth rate. So now we’re down to multi-factor productivity. And here the story isn’t good. It’s been falling. Trump’s war on technology and knowledge & research sectors (Trump University notwithstanding) will do nothing to improve things. And Trump’s stance on TPP, NAFTA and Brexit won’t help multi-factor productivity either. You’re living in a fantasy world of fake macro. Sometimes I wonder if you aren’t sitting by your keyboard while you’re fiddling with some free market ideology rosary beads. Your macro is purely faith based. Take some time to get up to speed.

2slugbaits, on my way to degrees in economics, I studied many undergrad and grad macroeconomics textbooks, which is a core course, like microeconomics. Your view of the macroeconomy is something like several incomplete jigsaw puzzles with the wrong pieces. Regarding, your statement, one variable, like the unemployment rate, doesn’t prove full employment, growth of the capital stock has slowed and aged, and output can increase through technology on inputs.

PeakTrader one variable, like the unemployment rate, doesn’t prove full employment

True but off point. Please refer to Menzie’s graph. It’s not just a low unemployment rate. The output gap relative to potential GDP has closed. We are at full employment.

and output can increase through technology on inputs.

Technology inputs do not increase output growth rates; they increase the growth rate of potential output. See the difference?

One consequence of this tax bill will be a severe cut in state and local spending on education…particularly higher education. Do you think that will lead to greater advances in technology?

If you have an NBER subscription you might have noticed the plethora of recent papers that have found a strong relationship between worker health and worker productivity. Do you think that eliminating the Obamacare mandate and cuts to Medicaid will result in a healthier, more productive workforce?

Do you think the elimination of personal exemptions will increase the growth rate of the labor force?

There is nothing in the GOP tax bills that increase potential GDP. Even the cut in the corporate tax rate, which at least in theory could have had a positive effect, ended up being botched so badly that it will do nothing but encourage rent seeking behavior…the very antithesis of productive activity.

Of course if we are below full employment. any fiscal stimulus would increase GDP. I would be going for more public infrastructure investment so those upper East Siders could actually get to work on time.

It has the makings of a Kansas fiasco.

The cuts, as envisioned yesterday afternoon (pre-$350 bn adjustment) puts the average deficit at 5% of GDP over the next decade, with net borrowing doubling in 2018 and 2019.

And it’s worse than this, because the CBO baseline assumes individual income taxes will increase by 1% of GDP (1 pp as a share of GDP) over the forecast horizon. Is that going to happen? I have my sincere doubts.

So that deficit is looking more like 6% of GDP.

Now, all this assumes that the potential GDP number above is better than useless–not a certainty at all. However, most of the upside has to come from more rapid productivity growth. Not at all impossible, but not in the bag, either.

Steven Kopits: “It has the makings of a Kansas fiasco.”

I don’t see why you are surprised at this. It is going exactly according to the plan.

The Republican plan has always been “starve the beast.” Republicans want to run up deficits so they can turn around and demand cuts to Social Security and Medicare.

They did it during the Bush administration and they are following exactly the same plan under Trump.

Ryan has already stated their their next budget reconciliation bill in January will be to address entitlement and welfare cuts.

I am not surprised by it. I predicted it, notably in my article on Japan and several times here in the comments section.

I am dismayed by it, nevertheless.

This is not a ‘starve the beast’ story. The Democrats have done that already. This is rather worse, and likely to lead to a big increase in either income taxes, or more probably, payroll taxes in the 2020-2022 timeframe. I think the experience in Kansas is likely to provide a precedent here.

Crowding out also becomes an issue. The Moody’s analysis Menzie linked earlier is well worth reading. When an economy is in depression mode, and the ZLB is effectively binding, then the ZLB is the de facto crowding out mechanism. However, as interest rates rise above the ZLB, the risk of crowding out by government spending once again becomes a real possibility. When the government is borrowing $1+ trillion per year, much depends on the willingness of US trading partners to buy additional US securities, and it is this question which Moody’s considers in some detail.

If interest rates start to rise quickly, it will affect both the business sector and the government deficit. A rise in the average interest rate of 0.7% (pp) is worth $100 bn in added interest costs to the Federal government.

It’s also a good bet that government borrowing funded by foreign lending will have a significant exchange rate effect. Probably not good news is you work in manufacturing or agriculture.