In a previous post, I documented the fact that the Fama puzzle had transformed post-global financial crisis, so that for most currency pairs, interest rate differentials pointed in the right direction for subsequent exchange rate depreciation, from 2006 through end-2015 (Bussiere, Chinn, Ferrara, Heipertz (2018)). Here I show that the new puzzle persists through the end of 2017, a period when US interest rates were rising.

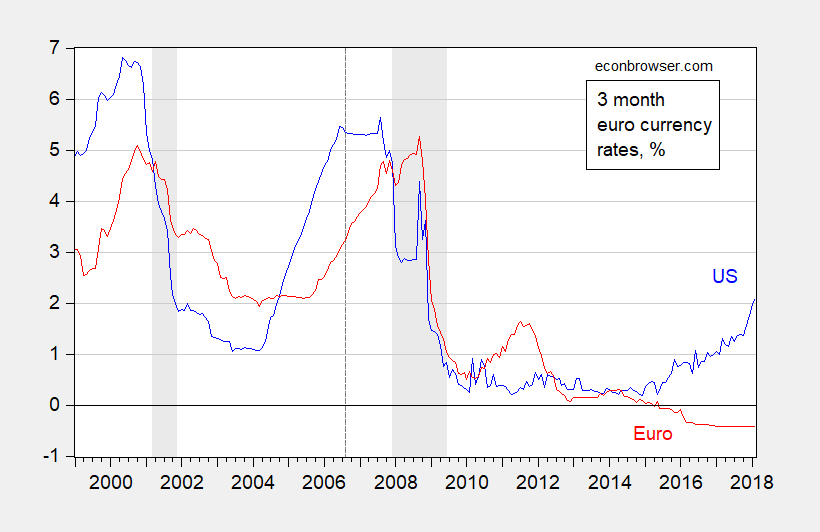

First consider three month euro-currency interest differentials (eurodeposit data from 2016M02 onward from BoE and National Bank of Belgium).

Figure 1: Three month euro-currency rates for US (blue), for euro area (red). NBER defined recession dates shaded gray. Source: Thomson Reuters thru 2016M02, Bank of England and National Bank of Belgium thereafter.

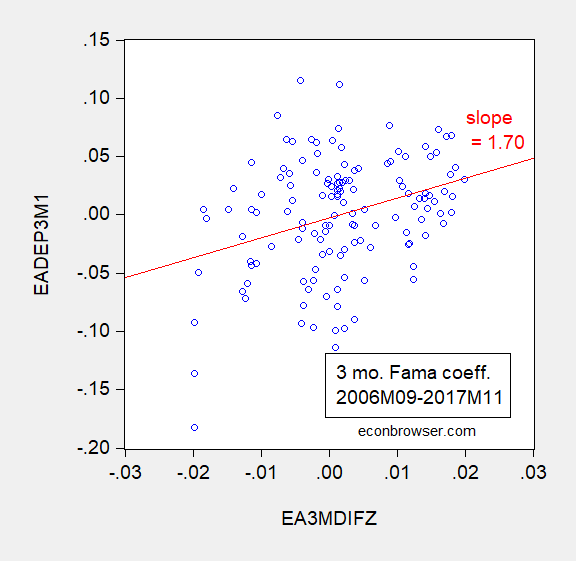

If one estimates the Fama regression,

s+1 – s = α’ + β'(i-i*) + error

breaking the sample into that up to 2006M08, and that from 2006M09 to 2017M11, one obtains the following slope estimates.

Figure 2: Three month ex post depreciation euro-dollar annualized against three month US-euro area euro-deposit interest differential, 1999M01-2006M08 (blue circle) and OLS regression line (red).

Figure 3: Three month ex post depreciation euro-dollar annualized against three month US-euro area euro-deposit interest differential, 2006M09-2017M11 (blue circle) and OLS regression line (red).

In the latter period, the slope coefficient is statistically significantly different from zero, but not unity. One salient question is whether the puzzle has persisted in the post-ZLB period. As we noted in our paper:

… a formal decomposition of deviations from the posited value of unity in the Fama regression indicates that the switch in signs from pre- to post-crisis can be attributed to a large extent to the switch in the nature of the co-movement between expectations errors and interest differentials. This finding implies that the change in the Fama coefficients is not necessarily a durable one.

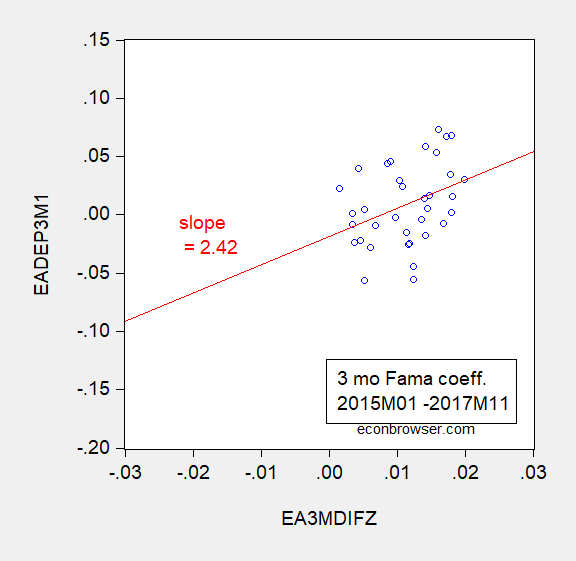

To answer this question, I truncate the sample to start with 2015M01. This results in the following figure.

Figure 4: Three month ex post depreciation euro-dollar annualized against three month US-euro area euro-deposit interest differential, 2015M01-2017M11 (blue circle) and OLS regression line (red).

The point estimate is again positive, and not significantly different from unity. In other words, the new Fama puzzle has persisted into to the post-ZLB period. Whether the durability of the new puzzle is due to the persistence of the switch in the correlation between forecast errors and interest differentials, as documented in our paper, remains to be seen, as that requires extended data on market expectations as proxied by survey data.

This is not an area of my expertise, but is it possible, the positive coefficient means the ECB kept the money supply tighter than the Fed and the U.S. had relatively stronger growth than the E.U.?

Or, the Euro depreciated, since more Euros were exchanged for dollars, that required higher interest rates in the U.S..

Let’s see – the Euro is expected to lose value over time so borrowing in Euros can award one with lower not higher interest rates. Irving Fisher is now rolling in his grave. Why? He could make a ton of money if he could rise from the grave and short sell whatever Bottom Feeder is holding long! Even Rudi Dornbusch is appalled at your ignorance!

An honest opening – it is not your area of expertise.

The issue is actually quite simple: the international Fisher equivalent predicts that nominal interest rate differentials capture expected exchange rate changes. Even the Keynesian Dornbusch overshooting model (what you allude to without realizing it) assumes as much. If expectations are always formed rationally and if there is no premium for bearing exchange rate risk – we would predict that the relationship would hold. But it does not do so in all periods for reasons that have been discussed for the past 45 years.

Ah but BottomFeeder has no clue what the actual literature over this period has noted. Trump needs a better troll!

You know – Menzie has written a lot on these issues. Time for some folks to read his contributions!

Pgl, the #1 negative name caller, it’s not your area of expertise either. And, currency traders don’t understand it well. It seems, the ECB didn’t ease the money supply enough and I wonder if that added to uncertainty. Anyway, I was looking for causes of the systematic error or change. The structural break may have something to do with the unusual economic situation after the recession.

Assuming PeakyBoo ever takes the time to read actual financial research, John Cochrane makes it easy by noting the incredible research of Gene Fama:

https://johnhcochrane.blogspot.com/2018/03/fama-portfolio.html

@ pgi

I guess my eyes kind of floated over this earlier, and I should have noticed, this is actually a great link you put up–both for the book reference and Cochrane being kind enough to share his essays. I strongly disagree with a lot of Cochrane’s politics, and he strikes me as pretty damned arrogant–but he is one of the few conservatives I will check up on and read because you can learn a lot about investing from him, conceptually and philosophically—I do find myself learning from him, unlike say, a Jim Rogers of commodities fame or a Marc Faber for example. I used to stop and listen to Jim Rogers go on his inflation tirades (which I think were and are insincere on his part) on CNBC and then after maybe the 5th one it just kind of dawned on me “Why am I listening to this grumpy A-hole??—because I never get anything out of it”

@ pgi

Sometimes I just wander around and find these things, and then you find like 15-20 similar videos. I don’t know how other people think of these guys, but in my mind, it’s almost like they’re already dead—but then you find this guy and find out is still a very vibrant human being, and not the stuffy type we usual imagine that gets a Nobel. I’m also becoming an Andrew Lo fan recently so, it’s even cooler to see the two of them together:

https://www.youtube.com/watch?v=dj-RO4mh-wA

It never ceases to amaze me the high percentage of these guys that are Jewish. He’s Catholic it looks like, but it’s a good wager a lot of his teachers at Chicago were Jewish. Can you imagine this guy, college age, thinking he was going to be a damned sports coach??

PeakTrader: Actually, pgl has displayed in his comments a much greater understanding of international finance than you have in yours. I have no reason to believe that this is not his area of expertise.

Menzie Chinn, I don’t disagree with Pgl’s statement. I was wondering why the parity condition doesn’t hold or what causes trader’s incorrect forecasts.

PeakTrader: As noted in the earlier posts on the Fama puzzle, biased forecasts drive the bulk of the new Fama puzzle (as long as you believe survey data). Expected returns in a common currency seem to be close to equalized on average.

I can’t really tell what Menzie is getting at here. Is it an “open ended” question on if/will the “new Fama puzzle” will continue?? Is it a half-prediction that “No folks, the new Fama puzzle will not continue”?? Is it a “Does anyone know the REAL reason why the new Fama puzzle is happening other than ZLB??

I can’t tell if Menzie is making an “enquiry” a “statement” or both?? or…… ???

Moses Herzog: Mechanically, the new Fama puzzle is due to the pattern of forecast errors post-crisis, and the correlation with interest differentials. Why the forecast errors have altered their behavior is the open question. The point is the Fama coefficient is a non-structural parameter (i.e., it’s not like the coefficient of relative risk aversion, which is supposed to be a deep structural parameter), so as expectations formations processes change, one would anticipate a corresponding change in the Fama coefficient.

@ Menzie

When you give these type explanations, (and no, it is not expected all the time) it is much appreciated. Appreciated probably more than you imagine. I do aim to get this stuff clear in my brain someday, but when you add these things, it’s kind of like searching for a deer I shot, not knowing where the hell it ran to die, and finding a sprinkling of blood on the ground (if that metaphor makes any damned sense at all).

@ Menzie

Is this related to monetary policy???—- because I’m looking for any excuse to ask you a burning question I have related to that.

I have no idea whether this is related or not, but the chart on page 2 looks eerily similar to figure 1, especially since 2009.

https://www.ecb.europa.eu/pub/pdf/other/ecb.sfafinancialstabilityreview201705.en.pdf?b8bc042e0590acfbec37353280a9e3ba

@ Menzie

The question I wanted to ask, related to monetary policy (if that’s not going way off topic here), is there have been at least one guy I respect pretty well on finance knowledge, Mike Konczal, and another guy I would say is a “minor figure” in the blogging world, Edward Harrison, who have been talking about how it’s basically illegal for the Fed to purchase municipal bonds in QE, and that maybe, as another “tool in the toolkit” for the Fed that this law should be changed, and that buying municipal bonds could be a real helpful factor, with ZLB limiting choices, to save things (asset prices, rates etc) when the next crisis hits. I was wondering your thoughts on multiple facets of this.

1) Do you think it would be effective, and how much would it help relative to more traditional QE bond purchases

2) Do you think it is morally sound?? (i.e. would it be morally or ethically wrong for the Fed to get involved in municipal bond purchases, inside of a QE operation, and would it create “moral hazard”). Similar to the overly generous Timothy Geithner “haircut” to AIG (pennies on the dollar).

3) Are you aware of anyone inside the Fed (or recently part of the Fed hierarchy) who has been pushing/lobbying on this idea, such as Bernanke, Yellen, Alan Blinder, etc??

4) Would this only benefit “fat cats” since so many wealthy individuals purchased municipal bonds to lessen their “tax burden”??

5) Flat out would you be for or against it, or is it at least worth putting a “trial balloon” up??

6) About 10 other questions I had which seem to have escaped my feeble brain at the moment.

Moses Herzog:

1) Probably more effective in helping out municipalities, but since munis aren’t as central to determining overall economywide interest rates, I doubt overall effectiveness would be greater.

2) Rather than speaking to the issue of morality, I’ll just note that the greater the risk taken onboard by the Fed in purchasing securities that can take on capital losses/default losses, the more quasi-fiscal the measure. To the extent that we delegate to the executive/legislative branches fiscal policies, QE on munis is more problematic than what was undertaken under credit easing measures implemented by the Fed. That being said, when one is in a crisis, hard-and-fast rules are not always plausible, so I wouldn’t rule out in extreme circumstances.

3) I don’t know of anybody in the Fed (Board, FOMC) who has suggested such a measure. Could be some working paper exists somewhere in the system that has discussed it, though.

4) I think in principle purchasing munis would drive down the cost of borrowing for municipalities, so would benefit some people at lower incomes to the extent that such borrowing benefits lower income households. But the distribution of gains surely depends on the incidence of both benefits, and tax burdens.

5) Without studying at some lenght, I wouldn’t have any opinion.

@ Menzie

Appreciate the response and your thoughtful take on it.

Konczal wrote a relatively long paper on it, I have only basically read his Intro to the paper—-the PDF paper is a short scroll down in this link on the small chance you would be interested in reading it:

http://rooseveltinstitute.org/expanding-monetary-policy-toolkit/

I have contested on this blog before, that there is more intentional leaking of both Fed policy, AND more intentional leaking of Fed data than many people perceive to be the case. The Fed data is intentionally leaked to favored parties (who bribe the Fed leakers??) before the data is made available to the general public. I first started having a strong feeling about this when the Jeffrey Lacker story finally broke. These two links basically support what I have been arguing for awhile now.

https://promarket.org/what-insights-do-taxi-rides-offer-into-federal-reserve-leakage/

http://faculty.haas.berkeley.edu/vissing/cycle_paper_cieslak_morse_vissingjorgensen.pdf

……. the [intentional] leaks therefor can be profitably traded on (and therefor effecting interest rate expectations, depending on the type of data released early) ahead of the eventual market move that will occur when the data become public. For those of you who forgot the Jeffrey Lacker story, which was a relatively big deal at the time—but since treated by Fed Res members, economists, and Uni profs as if discussing what Lacker did out-loud is equivalent to “dropping an F-bomb”—here is the link to the story.

https://theintercept.com/2017/04/07/a-federal-reserve-bank-ignored-insider-trading-investigation-when-reappointing-its-president/