Today, we are pleased to present a guest post written by Charles Engel, Professor of Economics at the University of Wisconsin, Madison.

The academic economics literature on foreign exchange rate determination has not had much success linking exchange-rate movements to standard macroeconomic variables. This problem has come to be known as the “exchange-rate disconnect” puzzle, as coined by Obstfeld and Rogoff (2000). The problem is that, when examining the so-called G10 currencies (the U.S. dollar, the euro, the Japanese yen, the British pound, the Canadian dollar, the Swiss franc, the Australian dollar, the New Zealand dollar, the Swedish krona, and the Norwegian krone), standard macroeconomic explanatory variables such as interest rates, GDP, and inflation have very little power to account for exchange rate movements.

My recent paper co-authored with Steve Pak Yeung Wu (“Liquidity and Exchange Rates,” National Bureau of Economic Research working paper no.25397) examines the role of the liquidity return on government bonds in driving exchange rates. My earlier paper, Engel (2016), suggests that this return – the non-monetary return that government short-term bonds provide because of their safety, the ease with which they can be sold, and their value as collateral, which is sometimes referred to as the “convenience yield” – may be important in understanding exchange rate puzzles.

Our study uses measures of the liquidity yield on government bonds, as constructed by Du, et al. (2018). These measures take the difference between a riskless market rate and the government bond rate to quantify the implicit liquidity yield on the government bond. The idea is that government bonds typically pay a lower rate of interest than relatively safe assets such as interbank swaps (or LIBOR). This difference measures the liquidity return or convenience yield of government bonds.

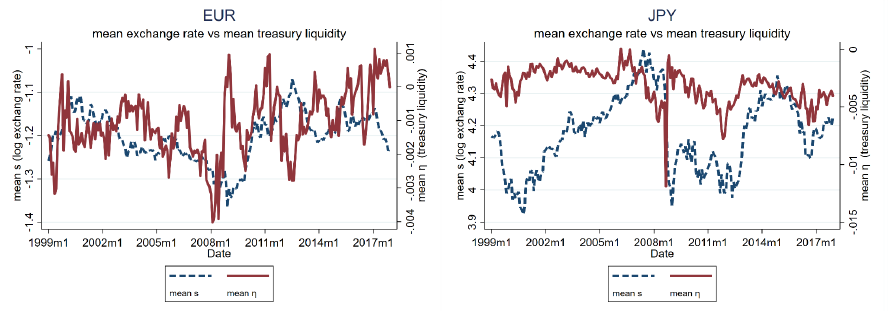

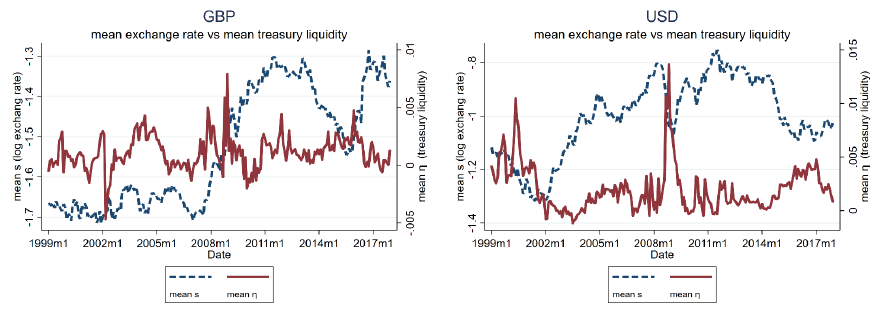

The liquidity returns and mean exchange rates for several currencies are illustrated below.

The intuition for why the government bond convenience yield influences the exchange rate is straightforward. The liquidity that these bonds provide is attractive to investors, and influences their investment decisions as if the bonds were paying an unobserved convenience dividend. The government bonds can pay a lower monetary return than other bonds with similar risk characteristics, and still be desirable. An increase in the liquidity yield, as measured by the difference between the private bond return and government bond return, will ceteris paribus lead to a currency appreciation much in the same way that an increase in the interest rate would affect the currency value. However, we note that in our equilibrium model, the liquidity return and the interest rate play somewhat different roles arising from the fact that the monetary policy instrument is the interest rate ex-convenience yield. Thus, the interest rate responds endogenously to inflation in a way that the convenience yield does not.

We find for each of the so-called G10 currencies that the relative liquidity yield (the home country yield relative to foreign country yields) has significant explanatory power for exchange rate movements. Moreover, using guidance from a standard New Keynesian model but augmented with a role for liquidity returns on government bonds, we find that the “standard” determinants of exchange rate movements are statistically and quantitatively important after controlling for the liquidity yields. In particular, interest rate differentials and a lagged adjustment term for the real exchange rate (as in Eichenbaum, et al. (2018)) are also important determinants of exchange rate movements. The real exchange rate is simply the relative consumer price levels between two countries, expressed in a common currency. This relative price level tends to move closely with the exchange rate because the exchange rate is used to convert price levels into the same currency. When exchange rate fluctuations are large, the relative cost of living measures can become misaligned, and the model predicts that subsequent nominal exchange rate movements will work to correct the misalignment.

We subject our results to a large number of robustness tests, but find the models perform consistently well in explaining exchange rate movements for all of the G10 currencies (relative, in each case, to the other 9 currencies.) Our baseline estimation looks at monthly changes from January 1999 to December 2017, but it is interesting to note that when we look at 1999-2007 and 2008-2017 subsamples, the model still performs well.

Du, et al. (2018a) propose decomposing the measure of the relative liquidity yield of government bonds into three components. The first component allows for fluctuations arising from the possibility of default on government debt as measured by credit default swap rates. While government default is not a very large problem for these countries, we do find that the small movements in the probability of default go in the direction that one would anticipate – higher default probability weakens the currency. The second component arises from a phenomenon that has arisen since the global financial crisis – that “covered interest parity” fails. Covered interest parity relates to arbitrage opportunities between spot rates for foreign exchange, forward rates for foreign exchange, and interest rates such as LIBOR. The failure developed during the crisis because of the possibility of bank failure, which made investors leery of receiving returns promised by many financial institutions. More recently, the failure has arisen perhaps because of balance sheet constraints faced by banks. In either case, the failure could point toward an increased liquidity demand for government securities, which would then increase the value of a country’s currency. That is what we find in the data. The third component of Du et al.’s (2018) decomposition is the remainder after correcting for the default risk and covered interest parity. It is perhaps the “true” measure of the convenience yield. Our study finds that all three components influence the exchange rate as the theory would predict.

It is also interesting that the “traditional” explanatory variables for exchange rates: interest rates, and currency misalignment as measured by the real exchange rate – affect the exchange rate in the way the theory predicts, but that this is apparent only after controlling for the convenience yield. Our study does not include inflation as a factor determining exchange rates, because during the period of 1999-2017, inflation was low and well under control in all ten of these countries.

An important point to note is that our study does not attempt to forecast exchange rates. It is simply trying to find the contemporaneous and past economic variables that are important in driving exchange movements. Indeed, an earlier paper of mine, Engel and West (2005), makes the case that the forecasting criterion is not a useful one for evaluating exchange-rate models. Most models actually have the implication that, under some assumptions that are likely to be valid, if the model is the “correct” model of exchange rates, then changes in the exchange rate should not be forecastable! We can understand better now, thanks to the new paper, what economic forces are important in determining exchange rates, but that still may not help us forecast future movements.

References

Du, Wenxin; Joanne Im; and Jesse Schreger. 2018. “US Treasury Premium.” Journal of International Economics 112, 167-181.

Eichenbaum, Martin; Benjamin K. Johannsen; and Sergio Rebelo. 2018. “Monetary Policy and the Predictability of Nominal Exchange Rates.” NBER Working Paper No.23158.

Engel, Charles, and Kenneth D. West, “Exchange Rates and Fundamentals.” Journal of Political Economy 113, 485-517.

Engel, Charles. 2016. “Interest Rates, Exchange Rates and the Risk Premium.” American Economic Review 106, 436-474.

Engel, Charles, and Steve Pak Yeung Wu. 2018. “Liquidity and Exchange Rates: An Empirical Investingation.” National Bureau of Economic Research working paper no. 25397.

Obstfeld, Maurice, and Kenneth Rogoff. 2000. “The Six Major Puzzles in International Macroeconomics: Is There a Common Cause?” NBER Macroeconomics Annual 2000, 339–390.

This post written by Charles Engel.

It’s certainly a fascinating topic. My theory on it has always kind of been, there are too many variables, or too many “moving parts” to make exchange rates predictable. At least as far as doing it in an “exact” way. Under extreme conditions, you might be able to predict a single currency’s general movement in comparison to one other single currency or predict a single currency’s movement to a basket of currencies (like an index). Outside of that it seems pretty damned hard. George Soros is kind of the master (and there were always rumors Soros was playing on inside information). I presume Eugene Fama has made some money there (although I don’t know that for a fact). Fama’s got a pretty strong/large ego, so you have to kind of assume he’s tried it a few times. That large of an ego is not going to be able to sit on the sideline on stuff he writes about and orates about all the time. I’ve often wondered how much college profs play around with these things. As far as I know, no University contract would prohibit or forbid this, so I don’t know why not. Keynes played the market some and David Ricardo made quite a bit of money—so why wouldn’t contemporary profs give it a whirl?? It has to tempt them certainly.

Thanks, Charlie, you always do good stuff. At least this variable is behaving reasonably well for forex market correlations, if not forecasting. You and Menzie try not to freeze too much there. Frozen Lake Mendota photo was inside front section of Washington Post today.

I’ve long believed that exchange rates were the hardest thing to forecast — behind interest rates, commodity prices, inflation, real growth and the stock market.

Not only do you have to forecast two or more interest rates correctly, but foreign exchange markets irregularly go off on some tangent and decide to focus on something else for some unknown period of time.