The Bureau of Economic Analysis announced yesterday that U.S. real GDP grew at a 2.6% annual rate in the fourth quarter of 2018. That’s below the 3.1% average for the U.S. economy over the last 70 years, but better than the 2.2% average rate since the recovery from the Great Recession began in 2009:Q3.

Real GDP growth at an annual rate, 1947:Q2-2018:Q4, with the 1947-2018 historical average (3.1%) in blue and post-Great-Recession average (2.2%) in red.

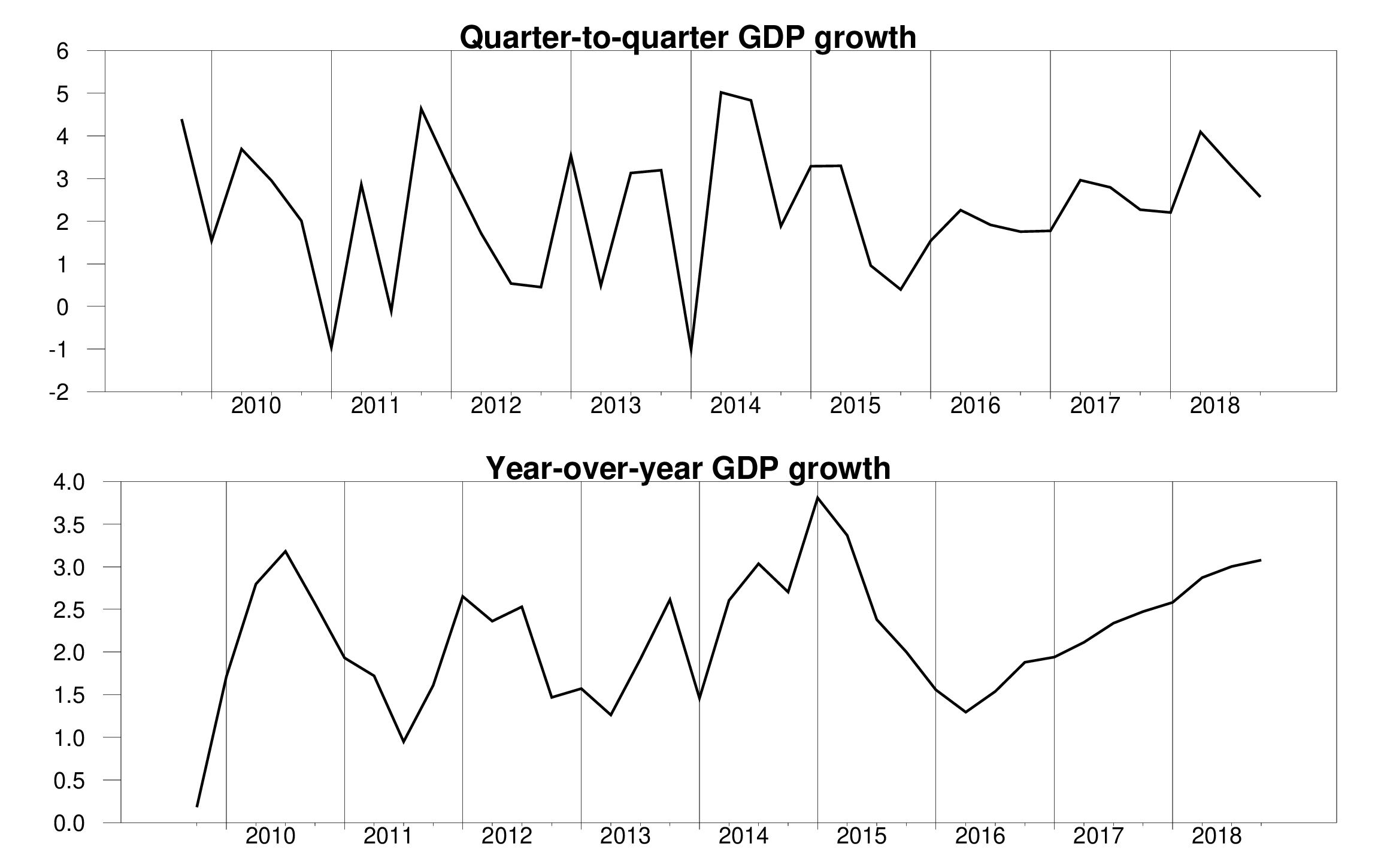

One can also look at the year-over-year growth rate, which smoothes out some of the measurement error in the quarterly growth numbers. This climbed throughout 2018, and we ended the year with the highest year-over-year growth rate since 2015:Q2.

Top panel: quarter-to-quarter real GDP growth, quoted at an annual rate, 2009:Q4 to 2018:Q4. Bottom panel: year-over-year real GDP growth. Vertical lines denote first-quarter observations.

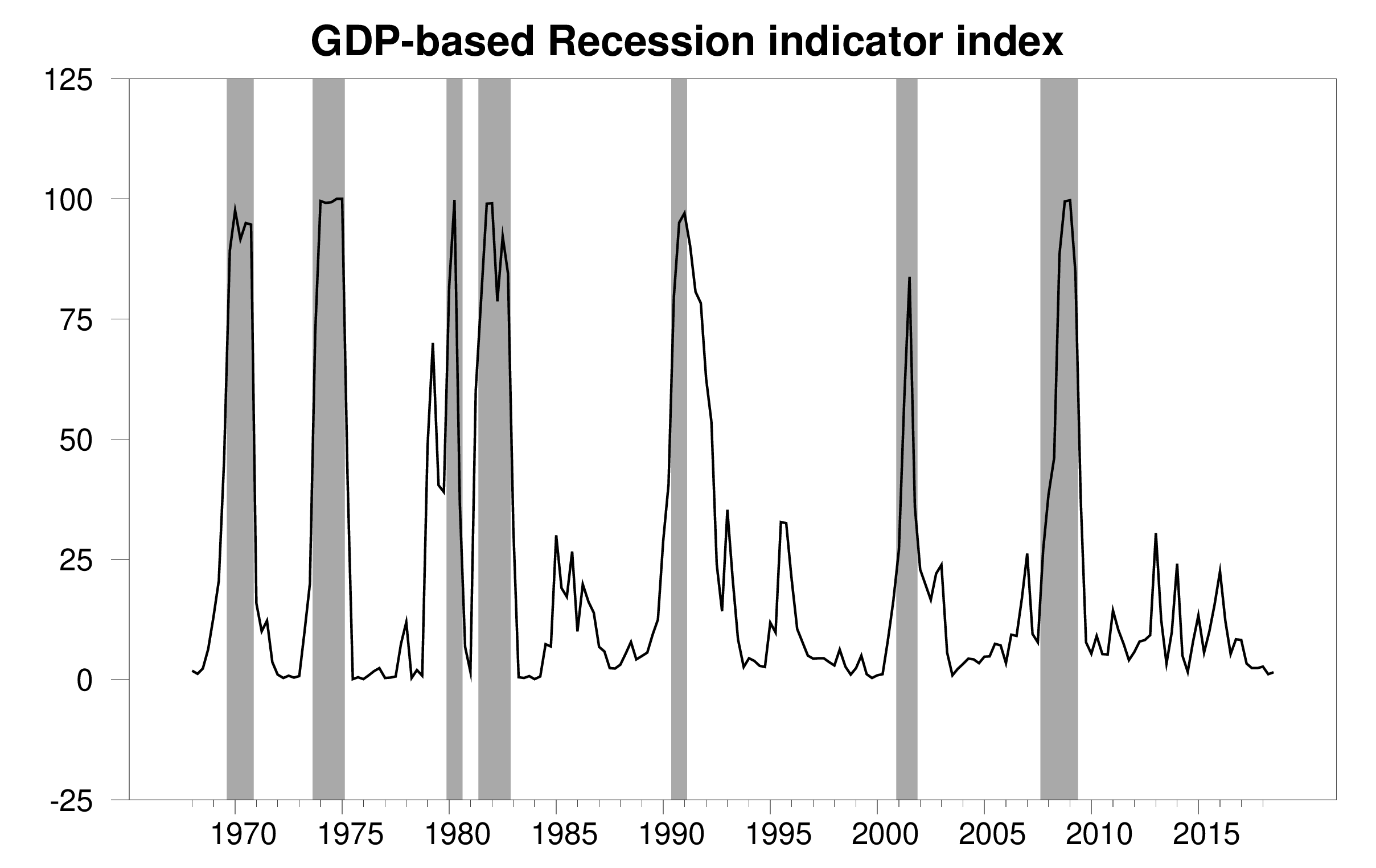

The solid growth numbers kept the Econbrowser Recession Indicator Index at 1.5%, among the lowest levels we ever see. That means the U.S. economic expansion has now been under way for 9-1/2 years, 2 quarters shy of the longest expansion on record (1991:Q2-2001:Q1).

GDP-based recession indicator index. The plotted value for each date is based solely on information as it would have been publicly available and reported as of one quarter after the indicated date, with 2018:Q3 the last date shown on the graph. Shaded regions represent the NBER’s dates for recessions, which dates were not used in any way in constructing the index, and which were sometimes not reported until two years after the date.

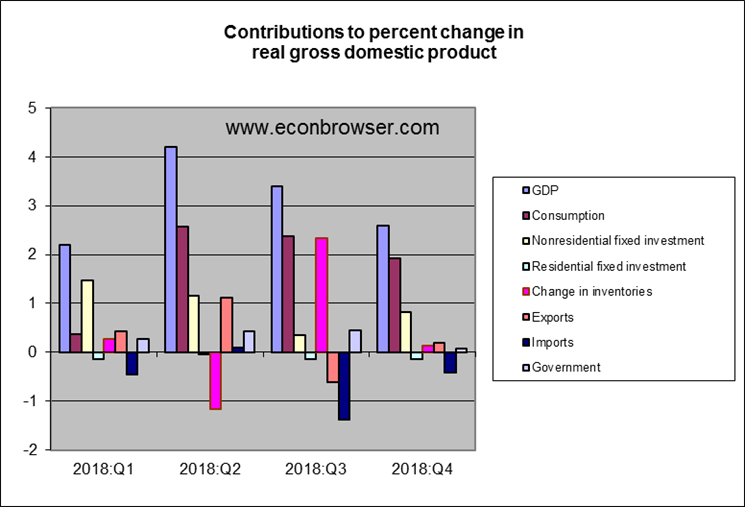

It was encouraging to see nonresidential fixed investment make a positive contribution to both Q4 and year-over-year growth. That’s a key cyclical contributor in a typical expansion and also provides the basis for future productivity growth.

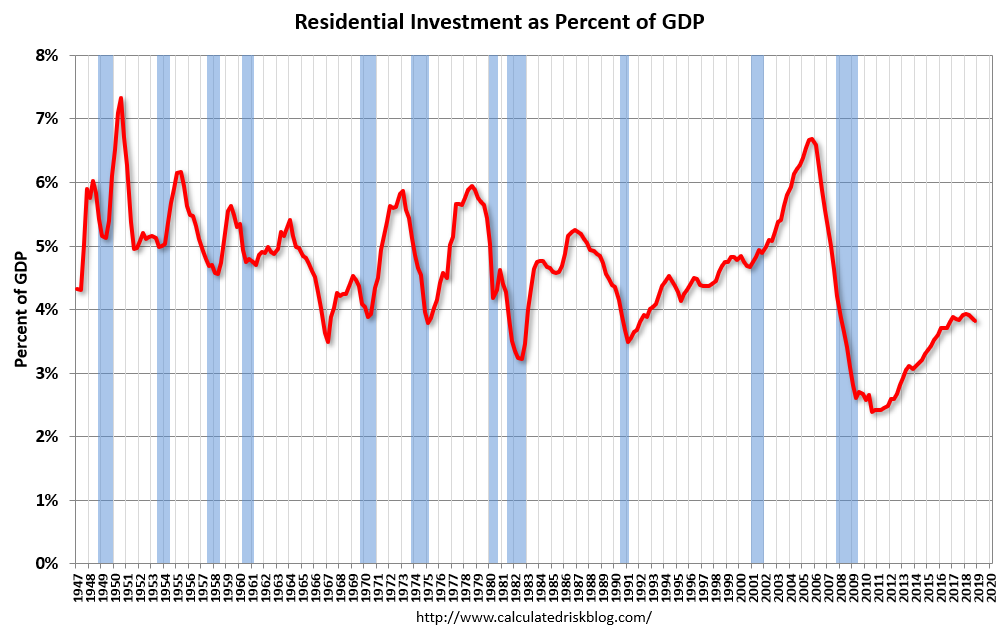

On the other hand, residential fixed investment is another variable that usually helps power a cyclical expansion. But housing was a slight drag on GDP throughout 2018.

Residential fixed investment as a percent of GDP. Source: Calculated Risk.

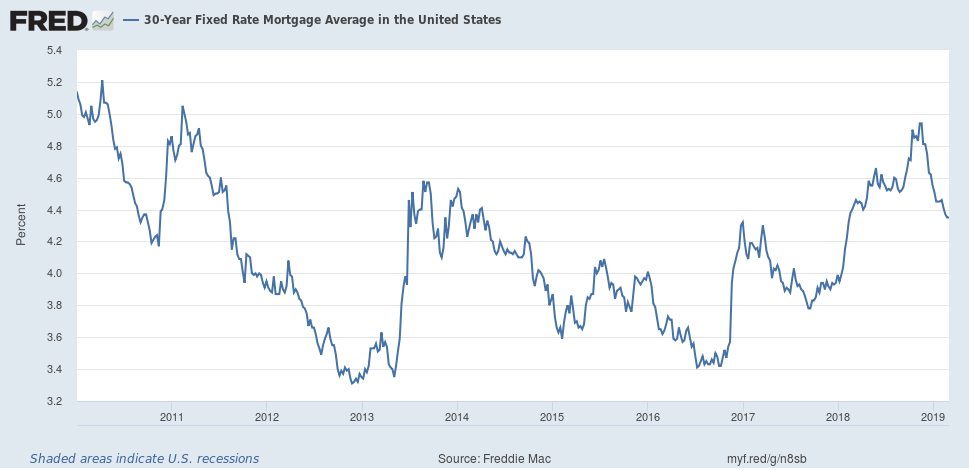

Interest rates may have been one factor holding back housing. The 30-year mortgage rate rose from 3.5% in the fall of 2016 to close to 5% last November. The rate has come back down significantly since then, though historically new home sales take several months to respond to changes in interest rates. Perhaps limits on tax-deductibility of mortgage payments implemented in 2018 were another factor.

Thirty-year fixed mortgage rate, Jan 1 2010 to Feb 28, 2019, from FRED.

The GDP data were a month late being released due to the government shutdown. That event may also show up in the level of GDP when we see the numbers for 2019:Q1.

Doesn’t look too bad overall.

Menzie! You are saying things that our Usual Suspects must be thinking to be “fake news” starting with your title “the long expansion continues”. OK PeakTrader used the same term but he claims the long expansion was 1982-2007. But you define it as 2009-2019 not Peaky’s time frame. And then you dare inform us that NBER disagrees with Peaky by noting we had recessions in both 1990/91 and 2001. Who to believe – Peaky or NBER?!

Then there is this statement which I sort of also said:

“On the other hand, residential fixed investment is another variable that usually helps power a cyclical expansion. But housing was a slight drag on GDP throughout 2018.”

Yes a slight drag. But Bruce Hall has all sorts of “data” (data he routinely misrepresents mind you) that residential investment is about to plunge us into a recession. In TrumpWorld, Bruce’s fake data must triumph over more reasonable presentation of the facts!

There were business cycles, including recessions, in the long boom.

In the long boom, we had the Reagan expansion in 1982-90, the Bush 41 expansion in 1991-01, and the Bush 43 expansion in 2001-07.

“There were business cycles, including recessions, in the long boom.”

Lord Peaky – don’t you ever get bored writing such stupid drivel? We get bored reading it!

And the boom of the late 90s under Clinton that beat all of those you mentioned conveniently only when GOPs were president. A serious bottom line that Jim Hamilton I am reasonably sure agrees with is that presidents have fairly small influence on the macroeconomy. Menzie would probably agree.

It wasn’t called the Clinton expansion, because it began under Bush 41.

A pragmatic and moderate Democrat President and an activist GOP Congress at least didn’t impede the demographic wave.

They most likely facilitated it, along with the Greenspan Fed.

No, PT. The Bush recession had ended by the time Clinton came in, but Clinton got in party because the economy was only growing very slowly. The 1992 election was the one that saw “it’s the economy, stupid” from his adviser, James Carville.

He then passed a tax inccrease, supported by Greenspan, but voted agaiinst by every Republican in Congress, withmany of them such as Gingrich forecasting a recession that absolutely was going to happen because that is what happens when taxes are increased. You are right that Greenspan played a role, because after the tax increase went through he loosened monetary policy. The GOP took Congress running against the tax increase, but there was no recession after all, not that a single one of those who made those erroneous forecasts has admitted that they were wrong.

To get to the bottom line it was only after 1995 that the growth rate of GDP really took off, several years after Bush left office, with the biggest part of the boom coming in Clinton’s second term, long after Bush was out. Really, PT, can’t you stop looking at data through a totally partisan lens, ever?

The 1995-00 Gingrich House and Dole Senate were further to the right than Bush “no new taxes” (and he voted for Hillary in 2016).

And, of course, President Clinton was no Obama.

This sounds like a 3AM Trump twitter rage. The perfect combination of pointless anger and sheer stupidity. Of course most of your rants fit this description.

Peaky replied with this:

“It wasn’t called the Clinton expansion, because it began under Bush 41.”

And that’s why Bush41 won reelection. How wait. BTW Peaky – the recovery was weak even through 1994 in large part because was not exactly cooperating with a recovering economy. The ICT boom did not began under Reagan or Bush41 or Clinton’s first term. It occurred during his 2nd term. So Peaky once again either proves he is the dumbest troll ever or a serial liar.

I make the same mistake, because I get where I hardly look at that part of the post, but it’s Professor Hamilton posting. My perception is that Prof Hamilton has a more positive outlook on the general economy than Menzie, but I may be playing my favorite board game “Badly Mistaken Mind Reader” again.

Not Menzie!!!!

pgl,

This was not Menzie, but the originator of the blog, Jim Hamilton.

pgl, do you work for CNN? You’re really good at misrepresenting what others say. If “about to” is the one or two years ahead where there might be a downturn is “about to plunge”, I guess your parsed interpretation of English is correct. https://econbrowser.com/archives/2019/02/is-california-in-recession-part-xv#comment-221737

Bruce – you clearly have anger management issues. But do rant on as your stupidity and childish rants are actually really funny.

Anon, thank you for you insightful addition to the discussion and the exchange of perspectives. I don’t know what we’d do without your contribution.

We do know what we would do without your “contributions”. Spend our time more productively!

Anon, no one is forcing you to consider my comments or the links of supporting sources. I’ll skip over yours and pgl’s if they are simply personal attacks. I’ll read them and the links if you wish to provide supported perspective. See how easy that is? Glad to be of help providing time efficiency.

“Interest rates may have been one factor holding back housing. The 30-year mortgage rate rose from 3.5% in the fall of 2016 to close to 5% last November. The rate has come back down significantly since then, though historically new home sales take several months to respond to changes in interest rates.”

Interesting point and more interesting graph. I knew this rate fell below 3.5% in 2012/13 only to rise again. I forgot that it fell to 3.5% by the end of Obama’s 2nd term. Trump’s fiscal stimulus which the Usual Suspects often praise (bowing to their master) induced the FED and markets to drive up interest rates. In my view – we likely should have had a modest increase in interest rates but the FED may have overdone this. Which is why a partial retreat in interest rates may be a good thing. But shhh – let’s not mess up Bruce Hall’s recession panic by informing him of the reality that the recent reduction in mortgage rates might help the housing market!

Where was the Econbrowser Recession Indicator Index when the crisis pretty much hit full steam in late September 2008??? Asking for a friend……

*What decisions would a person have made (assuming rational expectations) based on that Econbrowser index number??

*Bonus question, not required to answer but worth an extra 8% credit to all of our Berkeley Phd’s (or as my father jokingly called them “Puh-huds”) taking this exam.

Per Capita Real GDP growth in the fourth quarter annualized was 1.92%. Not as good as in the 1982-2007 long boom when it averaged 2.30%, but better than the average of 1.41% in 2009-17.

https://www.advisorperspectives.com/dshort/updates/2019/02/28/q4-real-gdp-per-capita-1-92-versus-the-2-59-headline-real-gdp

Real GDP growth from Q4 2017 to Q4 2018 was 3.1%.

My income would dispute your idea that 1982 to 2007 was a long boom. There were a couple Reagan recessions that put me on the street, a Bush I recession that put me on the street, and the first Bush II recession that put me on the street. It sure wasn’t an unbroken boom time for me or anybody else who didn’t have a trust fund or some kind of cushy job that wasn’t subject to market forces.

Willie, upward income mobility was uneven, although living standards for tens of millions of poor immigrants and their children were much better than if they stayed in their home countries.

Microsoft, for example, created 10,000 millionaire workers and a few billionaires by the year 2000. Also, the enormous prosperity at the height of the American Information Revolution allowed substantial improvements in environmental standards, since the 1970s.

Rising riches: 1 in 5 in U.S. reaches affluence

December 6, 2013

“New research suggests that affluent Americans are more numerous than government data depict, encompassing 21% of working-age adults for at least a year by the time they turn 60. That proportion has more than doubled since 1979.

Sometimes referred to by marketers as the “mass affluent,” the new rich make up roughly 25 million U.S. households and account for nearly 40% of total U.S. consumer spending.

In 2012, the top 20% of U.S. households took home a record 51% of the nation’s income. The median income of this group is more than $150,000.”

“Also, the enormous prosperity at the height of the American Information Revolution allowed substantial improvements in environmental standards, since the 1970s.”

the american information revolution of the 90’s is not what led to improvements in the environment. it was the clean air and clean water acts of the 1970’s that resulted in a much cleaner environment. it would be more logical to assume a clean environment led to the american information revolution, than to take your argument that the american information revolution led to improvements in environmental standards, peak.

Baffling, using your “logic,” if China imposed similar environmental regulations, it would have even stronger GDP growth.

China’s high GDP growth is a result of exploiting labor and the environment.

However, I’ve cited before, the health impacts reduce labor productivity, particularly as the limited labor force becomes less expendable.

Wow – we know PeakStupidity says a lot of batshit insane nonsense but is he seriously saying all that money made by the Koch Brothers has led to a cleaner environment? If he really believes this – we in Brooklyn have a bridge to sell to this fool.

i said nothing about china, only the us. try again peak. this does not change the fact that in the us, the information revolution occurred after stronger environmental standards were imposed. your statement was factually incorrect.

The American Information Revolution, with higher productivity, was a result of the Baby-Boomers entering their peak productive years and the pro-business policies by Reagan.

Western Europe’s Information Revolution was weak in comparison.

baffling, you are correct that the original EPA mission of cleaning up the air and water mess of the Industrial Age was quite effective. I remember entering the Los Angeles area for the first time in 1968 on a KC-135 and being astounded at the demarcation of the atmosphere above and below about 10,000 ft. The LA area was shrouded in brown fog. Then when I drove through the area, I had to keep the windows up and recirculate the air inside the vehicle because my eyes were stinging with the windows open. Pittsburgh was another example of EPA success. The measure taken were direct and focused on local and regional issues. The implementation was often less than stellar, especially in the automotive arena where cobbled “fixes” led to poorly running engines and significant product dissatisfaction until technology eventually lead to feasibility.

Now, however, the EPA has moved a large part of its effort to “solving” a more nebulous and global condition which may or may not be fully warranted. No, don’t run off with the “denier” bit. CO2, the primary target of EPA’s modern efforts, has been classified a pollutant with the EPA’s backing on the presumption that it is the primary driver of … let’s say it … global warming, However, the evidence in the form of computer models (ah, the Information Age) leaves much to be desired in terms of quality of predictions versus observations. Additionally, the assumptions that a greener and warmer environment is bad is debatable. At this point, climate science is closer to astrology than physics in many ways… or perhaps closer to political science than physics.

Regardless, the EPA’s successes in removing poisons from our environment is clearly a benefit for our economy at many levels. Likewise, the data-driven economy has allowed the U.S. to capitalize on the better environment without threatening it with additional poisons again (sure there are elements of computer manufacturing that could be quite harmful if not closely supervised). The movement away from coal to natural gas has been a major factor in the reduction of poisons and CO2 within the U.S while computerized engines have become much more efficient and far less polluting.

Eventually, based on technologies yet to be developed (including better batteries using a non-lithium base), electrification using wind, solar, nuclear, and geothermal sources may be sufficient to power the needs of this country without creating the massive costs and energy shortfalls inherent in the New Green Deal, But placing political mandates ahead of available technology is highly risky for our economic future. I could envision an economic catastrophe for the U.S. if the NGD were actually implemented … which it won’t for at least two more years and hopefully not in the manner envisioned.

“The American Information Revolution, with higher productivity, was a result of the Baby-Boomers entering their peak productive years and the pro-business policies by Reagan.”

so rather than admit your statement was false, you simply create another argument peak. but lets be clear, the information revolution was started and continues to impact the world in a positive way through the best educational system the world has ever seen. your reagan idoltry notwithstanding, high tech and stem education have been and will continue to be the reason we grow economically. you think fedex grew to be the company it is today because of reagan’s policies, or the insight that optimization and technology brought to the table from academia? come on peak, take a day and quit being a political hack in all of your worldviews.

bruce, “Now, however, the EPA has moved a large part of its effort to “solving” a more nebulous and global condition which may or may not be fully warranted. …” most of your comment makes sense. however, your description of carbon and the new green deal simply replays the same arguments we heard years ago about pollution and acid rain. and yet, as you yourself acknowledge, we did solve the problem and thrived. you are underestimating the ability of us technology to develop and solve a problem. the engineers of the world will develop the technology and solutions needed for the next phase in environmental pollution and climate change-that is what they are good at. what inhibits them from creating those solutions, is when certain segments of society intentionally deny and mislead the public on the importance of these issues. it is much easier to prevent a catastrophe than to try and clean up the mess afterwards. bruce, let technology do its thing and push us to a green, electric and renewable world. can you just imagine where renewables would be today if we had invested a trillion dollars in clean energy research rather than bombs on iraq, afghanistan and syria? it is simply madness that we spent over a trillion dollars to preserve the dirty fossil fuel way of life. what a sh!++y legacy you have left for your children and grandchildren, simply because you are too lazy to embrace a new way of life. renewables are not only cleaner, strategically they remove us from war torn areas fueled by oil riches. why would you not embrace that future?

baffling, there is no doubt that without Kuwait attacks and subsequent series of U.S. incursions and 9/11 attacks, that more money could have been spent on domestic issues. I never liked the whole Afghanistan “nation building” approach to military actions. Either fight a war or provide foreign aid; the two occurring simultaneously is stupid and wasteful. The U.S. role in the Middle East has been completely reactionary whether it was the Bushes, Obama, or Trump. The only true ally the U.S. has in the Middle East is Israel along with, perhaps, the Kurds. We don’t need Saudi oil (although the fearful-of-Russians would not want Europe to be more reliant on the Russians). There is enough wealth among the Islamic nations to fix their own social issues … if they are so inclined.

So, yes, there could have been more technological effort expended beyond the many billions of dollars dumped on the Solyndras and other political favorites. My issue is, after having government push clean air regulation on the automotive industry before technology had been reasonably developed, that mandating results without capabilities always results in enormous waste and poor implementation. A further issue is that the U.S. has been the leader in reducing CO2 output without carbon taxes or onerous economic burdens on its citizens, but the NGD as currently envisioned would change that dramatically. I wouldn’t mind owning a $30k, 5-passenger SUV, with a 350-mile all-electric range and having 10-minute charging stations every 5 miles along my route. But if I were in charge and mandated that, what do you think the result would be? Implemented in 5-years? 10-years? 20-years? 50-years? And what would the economic disruption be for a 5-year or 10-year mandate?

We all love our flat-screen LED televisions. Suppose the government had mandated that everyone had to purchase those after 2000? Remember that the 50-inch plasma cost $20,000 then. Would that mandate have been a problem? Yeah, well, the technology wasn’t ready then! Okay, my point exactly. Somehow the marketplace worked without massive government intervention. Why, because those bigger, better, less expensive sets eventually made both performance and economic sense to the masses of consumers… without huge tax burdens and market disruptions.

Your last paragraph says more than you probably intended. The “boom” has been great for well connected, well funded people. People with an insulated job or a trust fund. The rest of us get to scrounge. And the top 20% are dominated by the top 10%. The top 10% are dominated by the top 1%, etc. At this point, God help our young people, at least those who were not born with a way to gain a useful education without going disastrously into debt. So, your last paragraph is both revealing and a bit deceptive. Which isn’t much of a surprise.

PeakTrader the 1982-2007 long boom

Didn’t you forget about a couple of recessions during that timeframe? Or do you have your own solipsistic language?

solipsistic language it is! I wonder how reading this is going to mess with PeakBot’s simplistic programming!

Seems to me, reading for entertainment the ad homs and the abuse toward antagonists here, that the “narratives” abide, bringing a solipsistic attitude for any “narrative” but one’s own.

Amusement while awaiting the snow arriving in Boston area tonight……..

The MSNBC teams versus the Fox News teams.

I will use solipsistic in a sentence next time I speak to an old friend from the South!

JDH: Regarding your Recession Indicator Index. Even though the values on the vertical axis go beyond 100, I believe this axis plots probability. If I am mistaken in this, please let me know.

Assuming that the vertical scale numbers are probabilities, one look at the last two recessions alone tells the reader that this index is of little value. It is not a leading index. So perhaps a qualifying note at the bottom of the chart would be helpful to clear things up for the bulk of readers who may be misinterpreting this index as a leader.

Per your original paper or variant thereof, there’s a claim that this index is useful for ascertaining that a recession has begun before the NBER dating committee does so. That may be. However, there is a far better method for this purpose. The dating committee uses four coincident indicators and GDP – these overwhelmingly – to make its official decision on marking the starting and ending dates of recession. One merely need construct an index of the four monthlies, and then watch it. I myself have such an index. Using percent changes smoothed over three months gives razor sharp demarcation of the first month of recession with, in effect, only a one month lag. And it does so recession after recession after recession.

What I am getting at is this. Your site could be improved if you regularly posted your own well thought out leading indicator index along with a coincident index like the above. Not only do I find your vaunted Recession Indicator Index of no use, I believe for many if not most readers it is in fact misleading.

As for misleading. The venerable institution founded by G. Moore morphed into today’s ECRI shows that the risk of recession is currently quite elevated. As well other sources say the same. Even the consensus has recession risk in the neighborhood of 20%. Yet this is hardly the impression you give your readers by saying “the Econbrowser Recession Indicator Index at 1.5%, among the lowest levels we ever see.”

JBH: Quite right, this is an assessment tool, not a predictive tool. Your logic would force you to say that the NBER designations of recession are useless as well, which may be your position. The question that interested me was whether you can describe a recession as an objective statistcal event as opposed to somebody’s opinion. The real-time track record is good evidence that you can.

As for ECRI, they were predicting a recession in 2011 and stuck with that forecast for years. There is always a market for some analyst who predicts that a recession is right around the corner, because sooner or later one of them is going to be right and everyone will say ex post they’re a genius. Given the abundance of shamans predicting doom out there, I think there is value in offering a purely objective (albeit backward-looking) assessment to help keep perspective.

And as for my personal assessment of where we’re headed, I’ve been providing that for years in the form of the Econbrowser emoticon. That went negative Jan 8, 2008, back to neutral Aug 30, 2009, and has been positive since Oct 30, 2014.

Again I think we’ve been a useful source on that call as well.

Certainly there will be another recession some time. I personally see no evidence that it’s on the horizon just yet.

JDH: Thanks for your response.

I wasn’t disputing the dating committee’s official dates. I take them as given. I learn now that you were looking over the committee’s shoulder to see if their final opinion was objectively verifiable. That’s a reasonable question, and evidently the answer you found was satisfactory to everyone.

My point was a different one. I’d looked into the committee’s methodology and replicated it for the purpose of being able to make a statement about whether or not a recession had begun long before the official word came out. This I have done to my satisfaction as is implicit in my wording “razor sharp demarcation.” We both approached the same subject matter with different objectives, came up with different methodologies, and each accomplished our respective goals.

Now what’s interesting, I realized in the process of doing this work, is that GDP at quarterly frequency is something of a 5th wheel. The business cycle dating frequency is monthly, not quarterly. It must therefore be that monthly data series carry all the water. Indeed the dating committee uses monthly GDP and monthly GDI when making its decision. The committee must be extremely careful in its work as its end result is official. I have no such restraint. I’m simply trying to get as close as possible to what the committee will say is the initial month of recession (recovery) far before they actually say it. For this I was willing to construct a Procrustean bed of monthlies that with simplicity and in real time is demonstrably able to claim that the initial recession month has in fact occurred within plus or minus a month, and well over 50 percent of the time to the exact month per the final dating.

In pointing out the embarrassing and greatly prolonged wrong recession call made by the ECRI in 2011, you of all people will see that having an indicator constructed from the self-same bricks that the NBER committee uses to make its official call, made it easy to see in real time the ECRI’s ongoing error. For that matter, able to see a similar error made by anyone, then or at anytime in the future. Moreover, with my simple Procrustean coincident model, I can triangulate into the future so to speak. The numeric value of the 3-month rate of change to which this indicator has fallen is (as of January) where it was ahead of the past three recessions by 3-mos, 10-mos, and 10-mos respectively. The triangulation comes in having two other (leading indicator) models with which to get a bead on things. Interestingly, the modal 10-month lead of the coincident model, the just over 50% probability of recession within nine months of February per model two, and the model three central tendency of November all fall on the same month. This planetary alignment, though it be coincidence, gives confidence that recession will more than likely arrive before the end of calendar 2019. Obviously ongoing data can change this, and if so I will then on that basis change my view.

However I would not throw out the baby of ECRI with the bathwater of 2011. The ECRI really does have a pretty good record over time. Very few others do.

Ah ha! A possible disagreement between Jim and Menzie. While the latter is rumbling about a possible recession in 2020, the former tells us he sees “no evidence that it’s on the horizon just yet.” True enough, but as sd everal of these threads have reminded us, it is very hard to forecast the specific time of the arrival of a recession. They tend to appear often with little immmediate warning, drop the economy sharply for a short period, and then just quietly disappear, their turnaround point also not all that easily foreast, although easier than precisely predicting the inital downturn.

Menzie is cearly politically biased, and Trumps powerplay is not in his favour.

Jim’s right, there is no recession at the horizon, and this is good news for Trump and the country. Bill McBride even thinks the good days (economically speaking) are just beginning. 5G, electric cars, IoT and other new technology will be a boost for our economy, the question is what’s going to happen in China.

Kroogman? Oh boy – another troll misrepresenting what Paul Krugman really said.

@ “Kroogman”

You are either misrepresenting what Menzie said or flat out lying. Menzie has made it very clear he leans towards a recession happening after December 31, 2019, or months after that. That’s basically 10+ months from now. Many people have been “making calls” on a possible recession related to the inversion of the yield curve, with some other stats thrown in for good measure, allowing themselves a relatively wide time margin on the timing of the recession. Such as the overvaluation of the USA stock market and the overvaluation of the China stock market, and both the overvaluation of American real estate and real estate in China. The inversion of the yield curve has nothing to do with politics nor do the other stats. No less a “dirty liberal” and Jeffrey Gundlach has discussed the amount of junk rated corporate debt and the amount of corporate debt that should be rated as junk. Then you have the over-proliferation of CDOs, CLOs, and MBS etc. Many of these type credit instruments are not accounted for in James Hamilton’s or most economists’ recession risk measurements (or frankly I should be surprised as hell if Professor Hamilton has these in his index). That’s no knock against Professor Hamilton, most economists do not have this as an “input” in their more formal models.

JBH One merely need construct an index of the four monthlies, and then watch it. I myself have such an index. Using percent changes smoothed over three months gives razor sharp demarcation of the first month of recession with, in effect, only a one month lag.

That cannot be right. GDP is reported quarterly, not monthly. That fact also makes it unclear what you mean when you refer to smoothing GDP over three months.

JBH Or perhaps I’m misunderstanding you and you’re saying that you only need to look at four of the five elements used by the NBER committee; i.e., only the monthly reports excluding GDP. If that’s what you’re saying, then aren’t you effectively telling the NBER committee that they might as well ignore real GDP when the make their final determination? In other words, if you get the same answer using just four variables, then why add a fifth?

Bill McBride surveys the forecasts for 2019QI growth:

https://www.calculatedriskblog.com/2019/03/q1-gdp-forecasts-starting-low.html

Early forecasts seems to be predicting a mere 1% growth rate. At least no prediction of an early recession – at least for now.But this is a FAR cry from what Team Trump told us would happen.

The political effect of slower growth will be telling. It’s also going to be interesting to see how it gets spun, because it will get spun. Even if we have a so-called soft landing, slowing economic growth has it’s effect, at least from what I can see. Bill McBride still isn’t on recession watch, so far as I know, but it may not matter whether there’s technically a recession or not.

JBH,

Regarding recession indicators, what four indicators do you use, if not proprietary? From my understanding of a Professor Chinn entry July 28, 2007, NBER consistently uses real personal income less transfer payments and employment, but I am not certain of what the other two consistent indicators may be even after looking quickly at the NBER website.

AS The four monthly frequency indicators are:

(1) real income

(2) employment

(3) industrial production

(4) wholesale-retail sales

Two of the four monthly indicators reflect activity in the goods related sector of the economy. I wonder if the NBER committee has given any thought to looking at other indicators closely related to the service sector, which now makes up about two-thirds of personal consumption expenditures.

AS: In addition the two you mention, the core indicators are industrial production and manufacturing and trade sales, along with the Macroeconomic Advisers monthly GDP series. More recently, as of the last NBER BCDC release, the key indicators had expanded:

Macroeconomic Advisers’ monthly GDP (June)

The Stock-Watson index of monthly GDP (June)

Their index of monthly GDI (July)

An average of their two indexes of monthly GDP and GDI (June)

Real manufacturing and trade sales (June)

Index of Industrial Production (June)

Real personal income less transfers (October)

Aggregate hours of work in the total economy (October)

Payroll survey employment (December)

Household survey employment (December)

Professor Chinn and 2Slugs,

Thanks for the response.

What confused me was NBER’s comment on its website concerning indicators used. https://www.nber.org/cycles/jan08bcdc_memo.html

“The committee places particular emphasis on two monthly measures of activity across the entire economy: (1) personal income less transfer payments, in real terms and (2) employment. In addition, we refer to two indicators with coverage primarily of manufacturing and goods: (3) industrial production and (4) the volume of sales of the manufacturing and wholesale-retail sectors adjusted for price changes. We also look at monthly estimates of real GDP such as those prepared by Macroeconomic Advisers (see http://www.macroadvisers.com). Although these indicators are the most important measures considered by the NBER in developing its business cycle chronology, there is no fixed rule about which other measures contribute information to the process.”

The comment , “Although these indicators ae the most important measures considered by the NBER in developing its business cycle chronology, there is no fixed rule about which other measures contribute information to the process.”

Your comments are very welcome to remove my confusion. Seems like quite a task to attempt “to date recessions at home”.

Thanks again

AS: Household employment. Payroll employment. Real personal Y less transfers. Real trade sales. Industrial production. Note: Using the two employment series and counting income twice gives double weight to the two economy-wide variables, employment and income. Trade sales and industrial production get single weight. In effect this is four series expanded into six by having two employment series and double counting the lone income series. Each of these six then get equal weight in the final composite. Calculate symmetric percent changes. Take absolute values of these to then arrive at standardized percent changes. The six averages of the absolutes from February 1959 to present are used to do the standardization, a necessary step for meaningful summing. Sum the six standardized percent changes to get the composite in percent change form. Then observe the trailing 3-month average of the standardized percent changes to see the leading edge of this composite from month to month. I do extrapolate the badly lagging income series by a month. As of this Friday’s employment report, this composite could be extending into February territory. You would of course have to extrapolate the other three series to get a February number.

All this is easily done in an Excel spreadsheet with URLs in FRED pointing to each of the data series making regular updating a no brainer. Working backwards by initial recession month, this composite hits a value of .0003 in December 2007. It missed the official January 2008 by one month. The composite went negative precisely in April 2001, an exact hit. Similarly an exact hit at the start of the 1990 recession. This close accuracy fades for the 1980 and 1982 recessions, but once again is an exact hit for the 1974 recession. On my part, I am only interested in the three most recent recessions. This because the economy was in a different era prior to 1985. That year was the dividing line between the era of manageable debt and the current era of beyond optimal debt. Optimal debt is a separate issue which is nowhere treated in the literature. That there is an optimal for every aspect of the universe is prima facia evident.

The current 3-month percentage of the January value of this composite – a clearly different composite than that of the Conference Board due to series selection and weighting – is .0056. Which brings up another function of having an index like this – in real time! With each new monthly value in the late stage of the cycle, you can scan back and see how many months before the initial month of recession this value occurred – before the last three recessions especially. You then have an objective first estimate, on the basis of this indicator alone, as to how long it will be before recession arrives. Of course carefully constructed leading indicators are even more potent, so you may want have your own leading indicator index too.

I’m posting this because you seem genuinely interested. This is perfectly replicable to every jot and tittle. Posting it this way – though it is proprietary – also gives me a chance to demonstrate that I do this kind of work with many other models just as carefully constructed for virtually every post I make here.

Thorough knowledge of the literature, ability to ferret out and shed the baggage of what you were taught in graduate school that was wrong, and creative imagination to extend what you’ve learned into fruitful new space is what it takes to be at the cutting edge of the economy in real time.

Nothing in economics is of more value to business decision makers and many households than being able to advise them of the turning points of the cycle in advance. Forecasting is the sine qua non of all science. Accurately forecasting interest rates is even more challenging. It requires knowledge of the entire economic sphere – which is constantly evolving – along with key causal vectors emanating from the larger socio-cultural-political-geopolitical sphere that’s wrapped around the economy and impinges on it with a fair degree of frequency. The Paris Accord, for example, was the exogenous hit that gestated nine months and then birthed the Crash of ’87. So deep knowledge of economic history is also essential. There is no substitute for understanding the broad context at any historic moment.

JBH,

Thanks for the post and sharing. Do I understand your comment responding to Professor Hamilton, that your calculations show a 50% chance of recession within the next nine months as of February?

Thanks again.

AS: You understand that correctly. And you are welcome. My indicator was designed specifically to call cycle peaks. It peaked 21 months before the last recession. 15 months before the previous recession. And 19 months before the recession before that. The average of these is 18 months, pointing to next March from last September’s peak. Taking account of the magnitude of decline from its September top, though, translates into just over a 50 prob of recession by November. Consumer spending is what’s propping the economy up. The main wild cards are possible joint central bank easing like in February 2016, and how Trump’s next move against the deep state affects the public.

Jim, thanks for your post. Long time no hear from you. Hope everything is going well with you and your family. Are you already looking forward to enjoy retirement ? Is it 2 more years ? Good luck !

I love it, a basically anonymous troll parading a supposedly personal connection to Jim. Tacky. iif you are going to pull that one, “Kroogman,” you should probably say your real name, otherwise it is a joke, although perhaps Jim knows your real identity by this moniker.

As it is, I know both him and Menzie personally, but then, I go by my real name here, which does lead to some who disagree with me to drag bits of my personal history and connections into discussions pointlessly.

So where exactly is the demand coming from that is driving the expansion?

The federal budget deficit has increased significantly since 2015. https://fred.stlouisfed.org/series/FYFSD

Over $340 billion of additional fiscal stimulus in 2018 versus 2015 is a lot money pumped into the economy.

we have the greatest economy the country has ever seen, according to potus, and this has been built upon tax cuts and fiscal stimulus. and now we see the last quarter of 2018 was underperforming. in order to continue “growing” the economy, we need to continue to drop rates, according to “potus”. unfortunately, this does not appear to be a strong and self sustaining economy poised for long term growth without additional government support. so exactly what kind of economic policy are conservatives running out of the white house today? it is possible trump economic policy will crack the economy in his first term.

Conservatives are running a Keynesian policy of low interest rates and strong fiscal stimulus. Keynes said it best:

“Thus the remedy for the boom is not a higher rate of interest but a lower rate of interest! For that may enable the so-called boom to last. The right remedy for the trade cycle is not to be found in abolishing booms and thus keeping us permanently in a semi-slump; but in abolishing slumps and thus keeping us permanently in a quasi-boom.” The General Theory of Employment, Interest and Money, p. 322.

The Dems, OTOH, embrace PAYGO and have no plan for infrastructure funding with deficit spending. They have learned nothing from the 2016 debacle and are heading into 2020 with no economic plan that makes sense. No wonder a majority approves Trump’s handling of the economy according to Gallup. If Dems blow 2020, they will be the stupid party.

Paul: Your prior comment asking about the source of demand implies you are not on sure footing about the inner workings of the economy. How then do you have such assurance about the validity of this quote from the GT? On this, Keynes had it upside down. The virtually only cause of slumps is the boom that precedes the slump. The booms are driven by excess credit. Steve Keen created a monthly series on credit going back into the mid-1800s. If you will hunt for a copy and study it against recession episodes you will learn that what I say here is what the data say. All booms since 1913 have been sourced by the Fed. The Fed then had to unwind the resulting inflation which led to all recessions since 1913. The sole exception was the steel strike of 1960. Keen was the economist most correct about the Great Recession well in advance of nearly all others who got it right in advance too. Keynes was one of the notable economists who got the Great Depression the most wrong in advance. Those who get the big events right ahead of time know something that others do not, and are worthy of study.

Paul: One of Keynes’s more insightful terms was effective demand. Effective demand has two sources: consumer income and incremental credit. Obviously there is bi-causality, but the preponderance of causality is on the income side. Credit then boosts the month-to-month or Q-to-Q increments of income.

I like to “archive” predictions about the economy. Here is one:

“The Dow Jones Industrial Average surged 670 points on Monday, but it will hit bottom on Mar. 4, 2019, at 18,328.27.” That was written on March 26, 2018.

https://finance.yahoo.com/news/dow-may-already-bear-market-185419194.html

Unfortunately, the linked source is no longer available from Yahoo. Embarrassment? I don’t have that problem. I can predict with 100% certainty what happened a year ago.

Paul Mathis The Dems, OTOH, embrace PAYGO and have no plan for infrastructure funding with deficit spending.

Have you been living on the planet Triskelion? While you were away the GOP fought tooth and nail against Obama’s plans for deeper infrastructure spending. And only a few weeks ago the Democrats proposed something called the Green New Deal. Have you heard of it since your return to planet Earth? It says things like this:

to invest in the infrastructure and industry of the United States to sustainably meet the challenges of the 21st century

The Republican response has been to ask how to fund (PAYGO?) the GND. The only infrastructure project coming from Team Trump is his big, beautiful wall…and that’s only coming at the expense of other infrastructure spending from the MC&H appropriations. Republicans are comfortable with deficits, but only deficits from tax cuts. As a general rule Republicans don’t like public infrastructure spending because they see it as a lost opportunity to capture private rents.

Obviously the GOP fought against Obama’s infrastructure spending. Throughout the Obama presidency, Republicans in Congress were deliberately sabotaging the economy with government shut downs, debt ceiling crises and austerity in fiscal policy. Their goal was stated by Senate Majority Leader Mitch McConnell: make Obama a one-term president.

Yes, the GOP is comfortable with deficits which has been true since Reagan tripled the debt. Republicans know that deficit spending is fuel for the economy and at this point, their only hope of holding the WH and Senate is a good economy next year. No GOPer is going to propose a balanced budget for obvious reasons.

The Dems, however, have completely forgotten about how FDR financed the original New Deal and they have no plans to finance the GND except by increasing taxes, which is clearly a non-starter. Dems have NO economic plan for 2020 that makes any sense.

Paul Mathis I don’t think today’s economic problems are comparable to what FDR faced in the Great Recession. As to the Democrats having no economic plan, I think the bigger problem is that they have a couple of not entirely consistent plans. The GND is associated with an MMT approach to financing government spending. Call me skeptical. Then there are the timid red state Democrats who are pretty much clueless. Somewhere in the middle between the GND Dems and the red state Dems are the Old Left Dems. The intellectuals behind this group would include folks like Larry Summers, Paul Krugman, Jason Furman, Brad DeLong and Jared Bernstein. I think Prof. Frankel’s recent guest post would fall into that category as well. The politicians would include Biden, Klobuchar, Pelosi and probably Kamala Harris. I would summarize their views as GND without MMT. GND initiatives would prioritize R&D (and a lot of it). Funding it would be via somewhat higher tax rates on the rich, less defense spending, and a carbon tax rebate. Deficits funding of GND capital investment and GND R&D spending makes sense because the social returns are likely to be higher than private returns. It’s also a plan that has more than a snowball’s chance in hell of getting passed in a Democratic Congress. And it’s a plan that voters would likely find economically painless, although I think a lot of the perceived painlessness would be illusory. Funding GND initiatives would require significant savings, which would mean less consumption, but voters might not notice that if employment is high and GDP is growing. Some of the savings could come from overseas (which would justify making the R&D research freely available).

“Funding it would be via somewhat higher tax rates”

So Dems have learned nothing since 1984: on July 19, 1984, Democratic presidential candidate Walter Mondale pledged to raise taxes if he defeated the White House incumbent, Ronald Reagan. Mondale lost in a landslide.

Read my lips: No New Taxes!

How many times do Dems have to face plant on tax increases? They act as if deficit spending is the plague when in fact it is fuel for the economy as everyone in the econ business knows.