Today we learned that through March, the Federal budget deficit was 15% larger than the corresponding point in the last fiscal year — as expected given a not particularly stimulative tax cut (so much for tax cuts paying for themselves, as Stephen Moore claimed) and the ending of spending restraints. The dollar remains at elevated levels, as interest rates have risen. The trade deficit, excluding petroleum, continues to deteriorate. As I explained to my macro class today… it’s all textbook (notes).

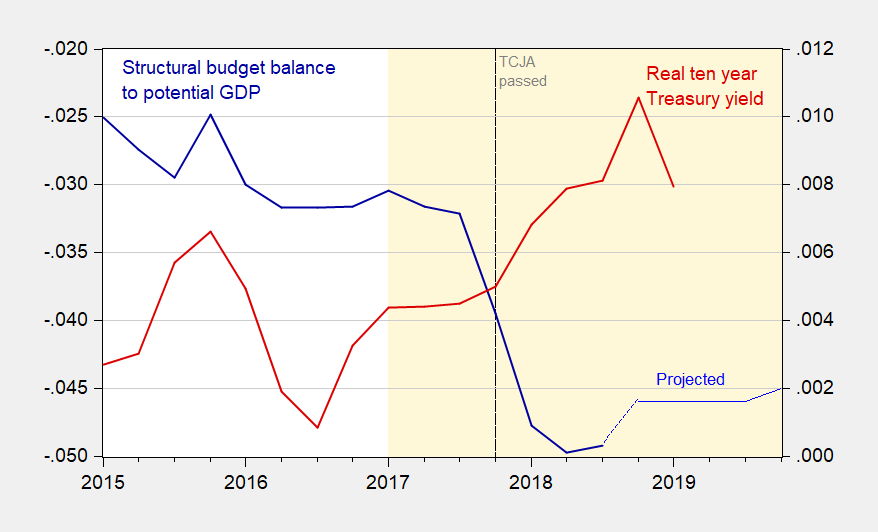

Figure 1: Federal structural budget balance as a share of potential GDP (dark blue, left scale), and projection (light blue), and ten year TIPS yield (red, right scale). Light orange shading denotes Trump administration, dashed line at passage of Tax Cut and Jobs Act. Source: CBO, Budget and Economic Outlook, January 2019, and Federal Reserve Board via FRED.

As the structural budget deficit deteriorated (1.4 ppts from 2017Q3-FY2019), real interest rates rose, roughly doubling.

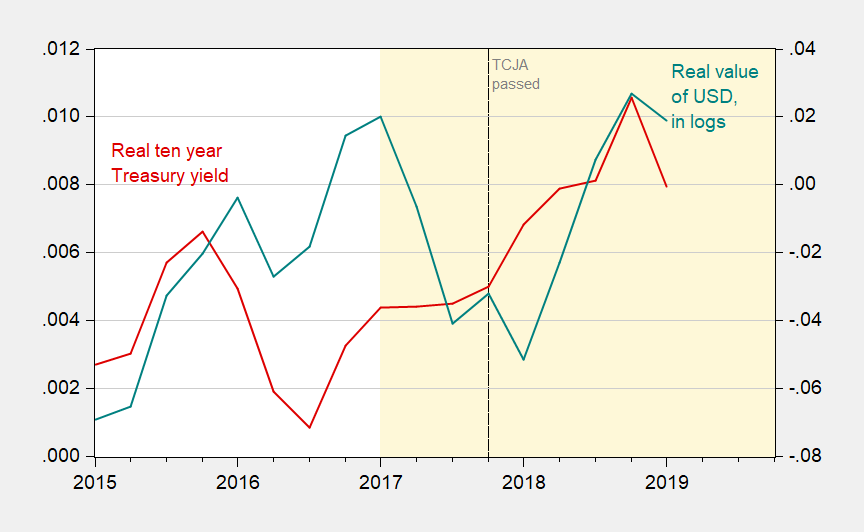

Figure 2: Ten year TIPS yield (red, left scale), and real value of US dollar against broad basket of currencies, in logs, 1973Q1=0 (teal, right scale). Light orange shading denotes Trump administration, dashed line at passage of Tax Cut and Jobs Act. Source: Federal Reserve Board via FRED.

Rising real rates in the US lead to a dollar appreciation of about 6%. What did the appreciated dollar do?

Figure 3: Real value of US dollar against broad basket of currencies, in logs, 1973Q1=0 (teal, left scale), and net exports excluding petroleum as a share of GDP (black, right scale). Light orange shading denotes Trump administration, dashed line at passage of Tax Cut and Jobs Act. Source: Federal Reserve Board via FRED, and BEA, 2018Q4 final, and author’s calculations.

The trade balance (excluding petroleum) has continued to decline, nearly a half of a percentage point from 2017Q3 to 2018Q4. This is true despite the imposition of anti-dumping, national security and 301 duties, which were intended to induce expenditure switching. In other words, macro dominates…

Pretty much as I predicted 2-1/2 years ago.

(Outside the textbook — Trump trade policy induced uncertainty has probably induced appreciation of the dollar as well, further worsening the trade deficit.)

If only the present Administration read textbooks. Can they read?

I should not talk we are about to have an election here

I bet the same message is presented in Mankiw’s textbook which is why the GOP “gurus” refuse to pay his nearly $300 per book price tag! You got this down to 5 pages of notes – nice! At Mankiw rates – these should sell for $60 a page! Alas even they are here online for free, I suspect the Usual Suspects will refuse to read them!

Hi,

My apologies for disturbing you. But I don’t see the orange line in figure 3. Is it supposed to be there?

Thanks,

Gene

Gene: No. There’s light orange shading…

The point that the large trade deficit in oil has almost disappeared without

any significant improvement in the total trade deficit makes a very good

argument that what drives the trade ( current account) deficit is the domestic

savings-investment , not any of the thing Trump is blaming. Actually, if his

policy are encouraging economic growth, they should be contributing to a

lager trade deficit.

You might want to check the spending side. That also appears out of control, last I checked.

When was the last time you checked? It looks to me like federal, state and local spending as percentages of GDP have been drifting downward. At least that’s the story in BEA’s Table 1.1.10

Anyone with an IQ above the teens and at least a shred of integrity (which of course excludes Princeton Steve) would check http://www.bea.gov especially Table 1.1.6. Real Gross Domestic Product, Chained Dollars

Since our incredibly inept and dishonest self styled expert at everything from Princeton could not do it, I have. Over the last decade, real state and local government spending fell in real terms only to recover to almost 2008 levels but not quite.

Real nondefense purchases has gone up by about 15.7% over the last decade but it is still less than 3% of GDP. So neither one of these categories is exactly out of control.

Defense spending? In real terms it was $791.5 billion in 2008 and is now only $738 billion.

Overall real government purchases in 2018 were approximately where they were a decade ago.

Yes once again Princeton Steve makes a completely bogus claim backed by no evidence and refuted by http://www.bea.gov. Is he really this incredible stupid and nothing more than your usual right wing liar!

BTW doing this in terms of % of GDP over the last decade is also cool. Total purchases fell from 20.3% to 17.2% of GDP. OUT OF CONTROL – Princeton Stevie is SO SCARED!!!

OK – back to the real world. Nondefense Federal purchases as a share of GDP fell from 2.7% to 2.6%.

Defense spending? Fell from 5.1% to 3.8% but the DONALD will fix that AND give us tax breaks (cough, cough).

State/local purchases as a share of GDP fell from 12.7% to 10.7% which may explain why New Jersey’s transportation system sucks. But I’m sure Princeton Stevie boy has the fix for that!

See next post.

I saw it – it does not change the fact that you are the most clueless babbling bafoon ever. http://www.bea.gov – try checking the facts next time – MORON!

Checked what? Oh yea – another one of your right wing authorities!

Since we’re treating the migrant labor as a black market, it is worthwhile to contemplate an analog, marijuana legalization.

Below are links from Colorado on the experience with cannabis legalization five years on. From the economics and public policy perspective, interesting, with some quite unexpected outcomes.

https://www.colorado.gov/pacific/publicsafety/news/colorado-division-criminal-justice-publishes-report-impacts-marijuana-legalization-colorado

http://cdpsdocs.state.co.us/ors/docs/reports/2018-SB13-283_Rpt.pdf

Well worth a discussion here.

I get it. You claimed government spending is out of control as you have been doing way too much marijuana. Sorry Stevie boy – discussing anything with someone who cannot get even basic facts right is a total waste of time.

“Princeton”Kopits comparing living breathing human beings from largely (no not all of them, but a significant portion) desperate situations/contexts to inanimate objects sold for profit. You know “Princeton”Kopits not only are you a good example of how some people waste the grand potential of the human mind, your morality ranks no higher than Nazi Stephen Miller’s.

https://www.politico.com/magazine/story/2018/08/13/stephen-miller-is-an-immigration-hypocrite-i-know-because-im-his-uncle-219351

Stephen Miller’s mother’s brother knows what anti-Semitism looks like, and probably never thought a Nazi would arise out of his own Jewish family.

I wonder if Miriam is proud of her Nazi son Stephen?? Does anyone know?? Her voice, similar to her brother’s, could be a powerful voice in the public dialogue. Women say they “want to be heard”, yes? Miriam—here is your chance to be heard as a female—your nation is waiting.

Other members of the Glosser family (somewhat bravely I might add) have spoken out.

https://www.buzzfeednews.com/article/ellievhall/stephen-millers-liberal-family-members-have-some

Although one wishes the hundreds (thousands??) of Mexican and Central American children being held in cages by ICE goons and not just men of stunted development with torches in Charlottesville got the Glosser family’s public rebuke. But speaking out in this environment is brave enough. It would be nice to see Miriam also type out (or pen if she prefers) an editorial, as I wager she’s way more articulate than her loser/weak son is.

Menzie: You were dead wrong in your prediction about employment flows 2½ years ago. Employment has done marvelously well under this president. And using the current account to measure your trade prediction, you were wrong as well! The current account as a % of GDP is precisely unchanged from 2016. Turning the corner on the hideous multi-decade trend in the trade deficit was always going to be a dicey, difficult proposition. Donald Trump had to fight Congress, academia, and the fake news media to get as far as he has on trade. Not to mention having to fight the big surpluses nations every step of the way, especially the communist dictatorship of China. Plus, the jury is still out on trade. The trade war is ongoing. Let’s see who wins the war. It ought to be obvious even to you that Trump is going to get a big piece of what he set out to get on trade. As for the unintended consequence of his policies in raising the value of the dollar. Big deal. The dollar doesn’t even appear directly as one of the 17 independent variables – count ‘em – you slather the rhs of the equation with to get a whopping 50% R-squared in your recent Chinn-Ito paper on the current account.

JBH: Run a regression of first log difference of nonfarm payroll employment 2010-2016. Dynamically forecast. Tell me what you see for actual vs. forecast for 2019M03. Is it still “marvelous”?

CA/GDP -24% in 2016Q4; -26% in 2018Q4.23.8% vs 26.2% if one uses potential GDP.

Re: CA regressions. Do you know the difference between a reduced form regression and a structural regression? I have a suspicion the answer is “no”.

Menzie: The data speaks for itself. Why would anyone need to do the dynamic forecast you suggest? Monthly gains in payroll employment averaged 199K during Trump’s 27 months. During the previous 27 months payroll gains averaged 217K per month. The difference is peanuts. Factor in the broader context that this lengthy expansion is now two years longer in the tooth under Trump, and that the higher fed funds rate and ramp up of QT have squeezed liquidity and hence buying power out of the system during Trump’s time in office. Yet employment hardly fell out of bed as you and many other liberal academics believed would happen. To date, Trump has actually done a fine job on the employment front.

I use actual GDP rather than potential GDP to ratio aggregates like the current account. Potential is not only a step away from actual and therefore more mystic. Who in fact knows what true potential really is? Based on hard data and that does not rely on a CBO model, the current account ratio was unchanged at 23% across the relevant time interval. And you waste time quibbling about it.

Of course I couldn’t possibly know anything about regression analysis. Never heard of it. But what I do know is that with a simple reduced form OLS model using a single independent variable that makes riveting economic sense I can explain 75% (!) of the quarterly variation in the US CA/GDP ratio from 1960 to the present. Moreover, that variable is causal with of course some bi-causality as well. And yet with a kitchen sink 17 variables, you and Ito explain only 2/3rds as much variation. Someday someone should write a paper about this kind of thing.

JBH: (1) Look…at…the…red…line. It’s just on pace, in a log-linear world. (2) OK. Tell CBO to stop dividing by potential GDP. (3) You should try to explain cross-country current account balances in panel setting without country fixed effects. Excuse me if I trust the judgment of referees that ok’d the model in the paper five or six times (as well as Maury Obstfeld) more than I trust your judgment. Call me silly!

(I *am* curious what one variable you are using to explain the time series of US current account balance).

JBH I would also like to know what single variable gets you an R-square of 0.75. A word of caution, in general a high R-square is usually a flashing red warning light of a misspecified model. And if your single variable is a time series in levels, then it’s almost certainly misspecified.

“The data speaks for itself.” WTF????

Seriously? No need to take statistics I guess. Just buy Alexa and hope Amazon is not spying on you!

The jury is still out on trade, JBH? That must be why Trump decided to wait another year to close the border that you said has led to out of control crime, drugs everywhere, disease spread by illegals, diluting the gene pool, etc. (Or it could just be that he understood the effect that would have on the Texas economy, and the tens of thousands of Texans–whose employment depends on trade with Mexico– who might not take kindly to such actions. He does understand that without those 36 electoral votes, there is no chance of a second term)

BTW, what’s the latest with those 293,009 indictments that will shake American civilization as it has never been shaken before? You were gayronteeing they were on their way…until–surprise!– you weren’t.

Steven Kopits doesn’t understand when you legalize something, particularly if it’s addictive, you get more of it.

https://www.denverpost.com/2017/05/18/marijuana-teenage-emergency-room-patients/

https://www.denverpost.com/2017/08/25/colorado-marijuana-traffic-fatalities/

A dollar of tax revenue is worth $10 in social costs, according to Steven Kopits math.

Happy to take you on counting the beans on this one, Peak.

I recommend you read the summary and peruse some of the text of the report. It’s actually pretty interesting.

Steven Kopits, you can start counting these beans:

Lost productivity, traffic & work injuries & fatalities, health problems & drug treatment, mental illness, unemployment, crime, domestic violence, child abuse, and other social services, including rehabilitation.

Two serial goof balls fighting in the kiddy’s sand box. LOL!

Pgl, you’re just jealous, since you were knocked out senseless from of the kiddy’s sandbox with ease.

Fortunately, you didn’t have much sense to begin with 🙂

At least HE knew Sonny Bono is dead. And has been for two decades.

Noneconomist, you must be Pgl’s mother.

You’re taking a big leap assuming Pgl knows much.

You must’ve taught him English comprehension or fake news.

You and Princeton Steven should go out on a date. Of course the waitress will probably insist on payment for food and drinks up front as she gets that both of you refuse to take up the check!

“Macro dominates”

Some young students may be confused by the highly technical and abstract term “dominates”.

Lesson #63 in Macroeconomics lexicon (See also Barry Switzer)

https://www.youtube.com/watch?v=JnQeCkgjszU

This visual tutorial on domination provided for some of the slower students: “Princeton”Kopits, Stephen Moore, Arthur Laffer, Sensitive Steven Mnuchin, Wilbur Sleepy Ross, Larry “I Love To Be Sauced During Interviews” Kudlow, Kevin “Half-Hour Comedy” Hassett……. damn, OK I’m tired typing these names—add any names you feel the list is inadequate without.

Hello Professor Chinn,

Thank you very much for the article on Trump Fiscal/Trade Regime.

I am still working my way through AP high school micro- and macroeconomics (Advanced Placement) on edX. I really like the micro econ instructor. He’s a professor at MIT. I am 58-years old and live in rural Georgia. It’s my responsibility to learn micro and macro econ.

For one third the price of one brand new Mankiw, I purchased a number of used econ textbooks: Mankiw Principles 6th, Case Fair Oster Principles 11th, Perloff Micro 6th, and Blanchard Johnson Macro 6th.

I was attempting to use my AP high school econ to see how close I could get.

I chose FY2018 to play with.

From the lecture notes, we have

Y = C + I + G – IM + X

and

Y = C + S + T

substituting for Y

C + S + T = C + I + G – IM + X

the C drops out and rearranging

(S – I) + (T – G) = X – IM

Using Mankiw (chapter 26) and Case Fair Oster (chapter 21 and 24), I am simplifying the equation. According to my intro text books, Savings equals Investment or S = I and the federal budget deficit/surplus equals T – G.

So, if I simplify S – I = 0.

(0) + (T – G) = (X – IM)

Finally, I get

federal budget deficit/surplus = trade deficit/surplus

Next, for fiscal year 2018, I went to the Treasury Dept for the federal budget numbers. I summed the monthly surplus/deficit for FY2018.

https://www.fiscal.treasury.gov/files/reports-statements/mts/mts.pdf

T – G = -779,174 for FY2018 Federal Budget Deficit

For the trade surplus/deficit, I used Census BOP, Seasonally Adjusted, and Seasonally Not Adjusted:

https://www.census.gov/foreign-trade/statistics/historical/exhibit_history.pdf

https://www.census.gov/foreign-trade/balance/c0004.html

https://www.census.gov/foreign-trade/balance/c0015.html

X – IM = -602,970 for the BOP method

X – IM = -859,094 for the Seasonally Adjusted method

X – IM = -854,217 for the Seasonally not Adjusted method

-779,174 == -602,970

-779,174 == -859,094

-779,174 == -854,217

Using my simple AP high school economics I am off by about about 10 percent and about 20 percent using the BOP method.

FY2018 was the only year I tried. It would be easy to do the other years.

There are about 10 million people in Georgia. I think it would be fantastic if several million could get up to AP high school economics speed.

Cheers,

Frank

Frank: I applaud your work. My warning is to use consistent data series; you need to use NIPA definitions of the trade balance (net exports) when you NIPA series. Also you have to be careful with S=I. This is true in a closed economy with *no govt* in equilibrium, where S is *planned* saving and I is *planned* investment. It’s always true (in a closed economy) when S and I are ex post (actual), since then it’s an identity (S≡I). But it all goes out in an open economy, with government. The identity is: (S-I) + (T-G) ≡ CA.

In my very arrogant personal opinion—one of the TOP 5 coolest comments/questions and coolest blog host answers I have ever seen on this blog (or for that matter, ANY blog).

Frank—- YOU ROCK SIR.

Hello Moses,

Thank you very much.

For the past almost 35 years, I have worked in agricultural research. I am just one of the dumb-dumb technicians.

All of my immediate supervisors have been PhD’s in a physical science.

One important thing I learned was to go to the data source(s) yourself and do, well attempt, the calculations yourself. And, check your work.

So, no, I just a dumb-dumb working my way through the econ models and trying to get the same answers as the econ PhD’s.

Professor Chinn is the main man. His work helps the millions of people (well, I hope there are millions of people who want to improve their economics knowledge) go the data source(s) and do the calculations and understand the economics.

Moses, thank you very much.

Cheers,

Frank

Menzie, I have a copy of the 2nd or 3rd most recent edition (I think published right after the derivatives crisis) of Blanchard’s book, by way of which “I am not currently at liberty to say”. Unfortunately I am not near as cool a person as Frank is (no sarcasm) and have barely skimmed the damned thing.

It’s all going perfectly, just as donald trump’s super MAGA plan was originally aimed:

https://twitter.com/Rover829/status/1116601511990026240

Courtesy of a link on Brit newspaper. Apparently this was better than they were expecting. Doesn’t look that great to me.

https://twitter.com/aila_mihr/status/1116630858645958657

This has been an “open secret” for a long time. Still important to hear it spoken out loud and the details more addressed—although American companies are still too cowardly to address this openly and call out names. A lot of button pushing analogies could be made here that would no doubt “trigger” some people, so, let’s just say it’s like getting your house robbed and then being afraid to call the local police. That’s certainly an analogy Mainland Chinese could relate to, not to mention some black neighborhoods in America. If you’re lazy like me or wanna rest your eyes from the computer monitor just hit the play button in the upper left and listen to the audio.

https://www.npr.org/2019/04/12/711779130/as-china-hacked-u-s-businesses-turned-a-blind-eye

The federal budget deficit increases are fueling GDP growth. That is macro as Keynes defined it. We will soon achieve the longest economic expansion in history after adding $11 trillion to the debt.

The trade deficit is reducing GDP growth. Keynes opposed countries running persistently high trade surpluses.

As long as inflation is subdued, the budget deficits are a positive for the economy. Why is there any argument about this?