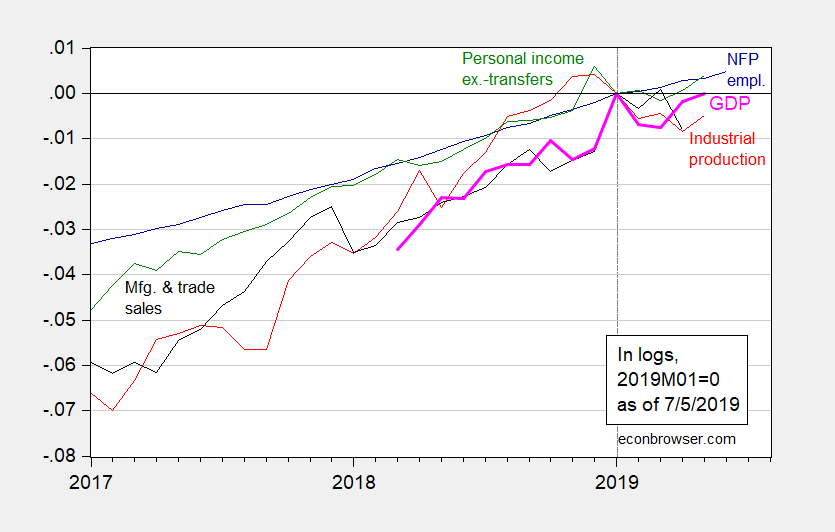

With the release of nonfarm payroll employment (NFP) numbers today, we have a new set of readings on indicators emphasized by the NBER BCDC (used in dating the end of the 2001 recession), since my last post on recession indicators. While NFP continues to trend upwards, industrial production, personal income excluding current transfers, manufacturing and trade industry sales are all below recent peaks. Monthly GDP has risen to match the last peak in January 2019.

Figure 1: Nonfarm payroll employment (blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), and monthly GDP in Ch.2012$ (pink bold), all log normalized to 2019M01=0. Source: BLS, Federal Reserve, BEA, via FRED, Macroeconomic Advisers (6/27 release), and author’s calculations.

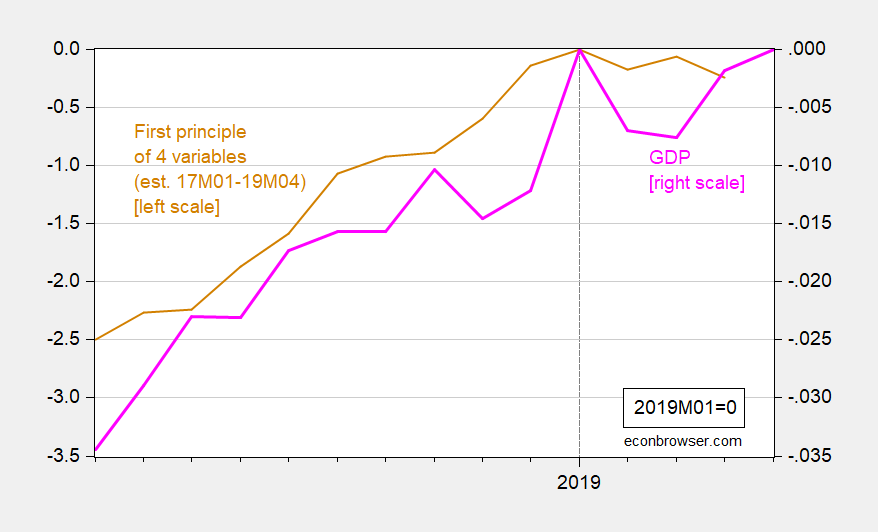

Industrial production, while rising, is 0.9% below recent peak. I computed the first principle component of the four variables (excl. monthly GDP) over the 2017M01-19M04 period, and plot this series and log GDP (both normalized to 2019M01=0). As a whole, the common component of the four variables has been essentially flat since 2019M01.

Figure 2: First principle component of nonfarm payroll employment, industrial production, personal income excluding transfers in Ch.2012$, manufacturing and trade sales in Ch.2012$, estimated over 2017M01-2019M04 (brown), and monthly GDP in Ch.2012$ (pink bold), all normalized to 2019M01=0. Source: BLS, Federal Reserve, BEA, via FRED, Macroeconomic Advisers (6/27 release), and author’s calculations.

In the name of honesty I will say I expected nonfarm payrolls to be much lower than today’s number. In fact I was half-tempted to make a prediction which no doubt would have gotten me egg all over my face. Not sure what to think of it exactly, although unemployment rising 0.1%. And a Fed Res rate cut looks less likely now?? That must make the broker/dealers so sad.

Last easter distortion. 2000 had the same effect. Many HR’s weren’t around for the BLS to sample in May which caused NFP to crash. Both months around it were typically strong. July will be weaker, noticeably. Jobless claims have essentially leveled off. No improvement has been made for months.

Some might note that the unemployment rate inched up but we should also note that the labor force participation rate inched up. Employment growth was just enough to keep the employment to population ratio at 60.4% where it seems to be stuck at for quite a while.

Error correction. The employment to population ratio is now 60.6% where it was as of October 2018:

https://fred.stlouisfed.org/series/EMRATIO

It was 60.4% last summer, but rose in the fall where it has been stuck since.

“Source: BLS, Federal Reserve, BEA, via FRED”.

Note to the incessant data source critics. FRED is a great way of accessing BEA, BLS, and Federal Reserve data. It provides the SAME data and is updated daily.

Now I realize that this data generally contradicts those Trump tweets. So believe who you choose to believe!

If these two SOBs think they can beat Uncle Moses at economics melodrama, well “step off!!!!!” dude!!!!!

https://www.coindesk.com/release-the-tape-nouriel-roubini-calls-for-bitmex-ceo-debate-video

https://www.youtube.com/watch?v=94dyikITfE0

I have stated before the battle/War is already lost for HK’ers. Still, somehow it is fun to root for or pull for lost causes sometimes. We all know Charlie Brown will go flying through the air when he tries to kick the football out of Lucy’s hands, but isn’t a small part of us still pulling for Charlie at the last millisecond there?? There are some minor grammar errors in this. It is extremely petty to focus on grammar errors when the underlying message is quite insightful, and shows clearly that mainland Chinese people can be very creative and inventive when the surrounding context provides them with an incentive to be just that:

https://medium.com/econ記者嘅寫膠網絡板/the-generation-leading-hong-kong-protests-doesnt-use-facebook-and-that-matters-f7b8a4adb9f

I’m wasting internal emotional energy pulling for these young people. Still I can’t seem to help myself from doing so.

LFPR was flat. Household was flat which was a YRY loss. This month was the final correction from the late easter which drove up April NFP and May NFP down. Total hiring is decaying. Sorta of think household employment as the leader and jobless claims as the secret follower and the U-series the dog on the sniff.

July will be weaker indeed, but its this fall where the Fed is worried about. That hiking cost of debt on corporations, driving down investment farther than it did late last year. That 4 trillion of debt turning into 8 trillion of interest rate hikes is bad, very bad. But debt booms end.

My guess January is the beginning of job loss.

Employment to population ratio was 60.6% – same as it was in October 2018. 9 months of no real progress despite all the cheerleading from the Trump trolls.

January is several months earlier than I expect things to come apart. I do not know if job losses coincide with onset of a recession or if they predate or lag.

https://www.youtube.com/watch?v=doYWURMek7g

Menzie, do you like to practice your “listening German”?? This film is pretty cool

https://www.youtube.com/watch?v=_5SZ7aiw6Zc