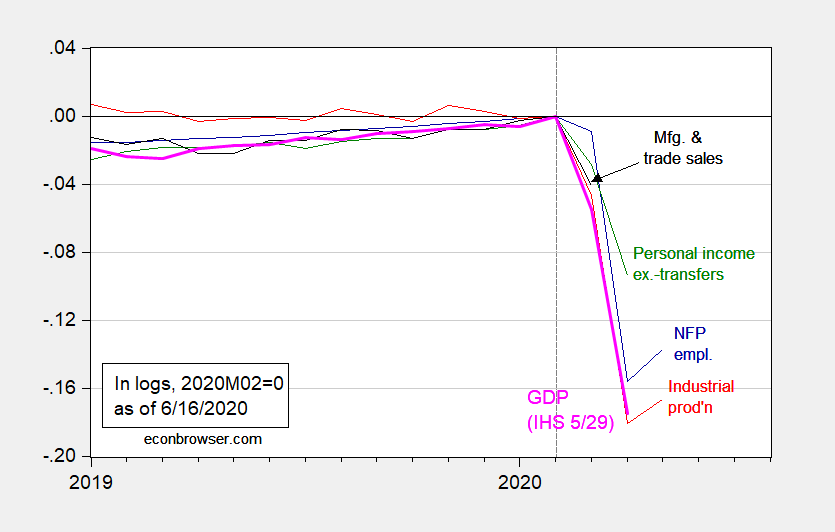

As of today, here are key monthly indicators followed by the NBER Business Cycle Dating Committee:

Figure 1: Nonfarm payroll employment (blue), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), and monthly GDP in Ch.2012$ (pink), all log normalized to 2019M02=0. Source: BLS, Federal Reserve, BEA, via FRED, Macroeconomic Advisers (5/29 release), Bloomberg, and author’s calculations.

The NBER Business cycle Dating Committee has dated the most recent peak at February 2020 for monthly data, and 2019Q4 for quarterly. Jeffrey Frankel describes the reasoning for this date.

Q2 nowcast from Atlanta Fed is -48.5% (6/9), from NY Fed is -25.9% (6/12), St. Louis Fed is -38.9%(6/12), all SAAR. IHS Markit is -37.4% as of today.

https://ourworldindata.org/grapher/daily-covid-cases-3-day-average?time=2020-02-24..&country=European%20Union~USA

Chart of the day! The EU has bent the curve downwards on new COVID 19 cases but the US has not. Of course the leaders in the EU are trying while Donald Trump is not.

I would also like to add something, according to my view an investor can become expert of market by making his own profit earning strategies and for this he has to follow those trader who are already performing outstanding in share market.This is best approach to be adopted by an investor.

https://www.indiratrade.com/

Could this be the shortest recession on record at only 3 months?

Alternatively, are we just seeing dead cat bounces?

Services are still contracting. I generally ignore the rest. Poor government sampling is sad.

It is likely a dead cat bounce. And if the cat catches COVID-19, it might end up dead.

It’s been documented that cats can be infected by SARS-CoV-2 but there is no evidence of transmission to humans or whether if poses a health risk to cats. This was one of the early studies coming out of Wuhan.

The only reported animal to human infections were in the Netherlands: Minks infected humans on fur farms.

The Chinese fur industry is the most likely origin of SARS-2 according to experts.

Continuing claims, though somewhat distorted, have come down. Philly Fed survey swung from -43.1 to 27.5. Hotel occupancy improving. (I’m reading all of this from the Calculated Risk front page – lazy man’s economics.) This is all for June, suggesting that may could be the near-term trough, so that Q3 will show growth.

NBER is unlikely to move as fast in calling an end to the recession as it did in calling the onset. The potential for another slide is high. If there is a long flat period far below the earlier peak, the business cycle committee may see the May trough as mere noise.

We are still in the thick of it. The wisdom of hindsight may be a long time in coming. Two massive economic shocks in just over a decade could lead to profound changes in business decision-making and financial risk-taking. Hope I’m not too tired to pay attention when the evidence comes in.

This recession may amount to only two months, March and April, although the declines in both those months so were so great they will offset the growth in the other two months of each quarter, thus giving us the favorite journalistic definition of a recession as at least two consecutive quarters of negative economic growth.

Of course, the NBER committee makes its own judgments based on a variety of variables, so we do not know yet how many months they will declare to have been recessionary officially. And for those who keep misunderstanding how that committee describes things, they are not counting February as a month of recession, although I keep seeing this claim repeated widely across the internet.

While we know first quarter was overall negative in its growth rate, that remains uncertain for the second quarter. The number I have not seen commented on here so far is the enormous increase in retail sales for April to May, 1.7%, more than offsetting the 14.4% decline for March to April, leaving retail sales only 8% below their peak in February. This is certainly an outburst of pent-up demand, partly goosed by fiscal stimulus of various kinds, some of which is disappearing. I may not have been surprised that employment grew, but this large increase has caught me by sueprise.

If this continues even somewhat, we may see what I had pompously dismissed numerous times here, that V-shaped recovery pattern, with most of the economics profession also being skeptical on this point. At the top of this surge are some sectors that may represent one-time buying, such as furniture. But other sectors may continue to see strong sales increases. This is the largest part of consumption, which is the largest part of GDP. It may well end up that growth in May and June will offset the sharp decline in April, leading to a situation of net positive GDP growth in the second quarter, and thus no recession in the journalistic sense of two consecutive quarters of net economic decline.

That doesn’t quite work. Revision samples will be large going forward.

The long wait for final revisions is among the reasons the business cycle committee is slower to declare recession ends than recession beginnings. This time, the beginning was unambiguous. The end may be highly ambiguous.

Recession dating has its fascination. Guessing dates and shapes is a sort of game. When it comes to putting recession stripes on charts and recession dummies into regressions, knowing the dates is useful. Beyond that, we are left with the tangle of interactions that make up the economy in the real world, and that tangle is much more interesting. We’ll be assessing the aftermath for the rest of our lives.

The drop and rebound in retail sales is a good example that the percent change in a rebound is generally larger than the percent drop.

A fall from 100 to 75 is a 25% fall. But the rebound from 75 to 100 is a 33% increase.

Barkley,

Since 4/25/2020 the NY Fed WEI has shown improvement each week. https://www.newyorkfed.org/research/policy/weekly-economic-index

Index

-11.48 on 4/25/2020

-11.35 on 5/2

-10.57 on 5/9

-10.47 on 5/16

-9.84 on 5/23

-9.58 on 5/30

-9.23 on 6/6

-8.39 on 6/13/2020

Question: How much of the stimulus payments made by the US will show-up in GDP statistics for 2020Q2? Is some or all of the stimulus considered transfer

payments?

Additional Comment: Based upon some humble forecasting, I think it is possible for real personal consumption to be down by about 35% annualized for 2020Q2. At about a 70% impact to GDP, this would be a negative GDP factor of about 25%. I used RSAFS as one element which would include the 17.7% increase in May.

Retail and services got thumped, and that was in the news. But the media did not fairly report that much of america has worked right through the pandemic. There are threats of future layoffs on government and education, but those layoffs have not yet materialized. The rightwing media has created the impression the shutdown closed everything, and that is simply not true. A strong rebound could have occurred if trump had done better at creating a well thought out plan to shut down, control the virus, implement protective steps for society and the medical community, and let the data dictate a smooth reopening. He failed at leadership. Now places like texas, which never pushed the curve down, has reopened into a rising curve which looks to be growing exponentially again. This will be much more costly than need be.

Whoops, that was a 17.7% increase in retail sales, April to May. and, yes, various forms of fiscal stimulus have aided this, with some of those already gone or set to disappear. There are a lot of moving parts to all this. But I am struck that an awful lot of economists and observers seem to be ignoring signs of possibly strong rebound.

Hey, I was not surprised by the positive net jobs report and said so here. There were an awful lot of economists who were surprised. Is this crowd on the verge of being surprised yet again? Sure, there are some signs one can point out that say recovery is slow, but then there are others, like the retails sales numbers, that should have anybody predicting some massive GDP decline for 2020 second quarter as a done deal to be a bit more cautious.

Maybe the most important economic news this week came out of China – a SinoVac vaccine is being readied for phase 3 trials. I can imagine Trump ordering the FDA to go slow in approving a vaccine developed in China. I cannot imagine Biden doing so.

Trump was interested in using access to a vaccine as a weapon. If china gets it first, will be an interesting development. What if china ships it to europe but not usa?

There is not enough popcorn for watching that noir pageant. Too bad it is so deadly serious.

City of houston just removed a confederate soldier statue from major park entrance. Confederates were traitors who attacked the republic. The deserve no public spaces. Black lives matter.

As a kid in Georgia in the early 1950s we use to get Robert E. Lee’s birthday off as an official state holiday.

I wonder how that compares to evacuation day in Boston.