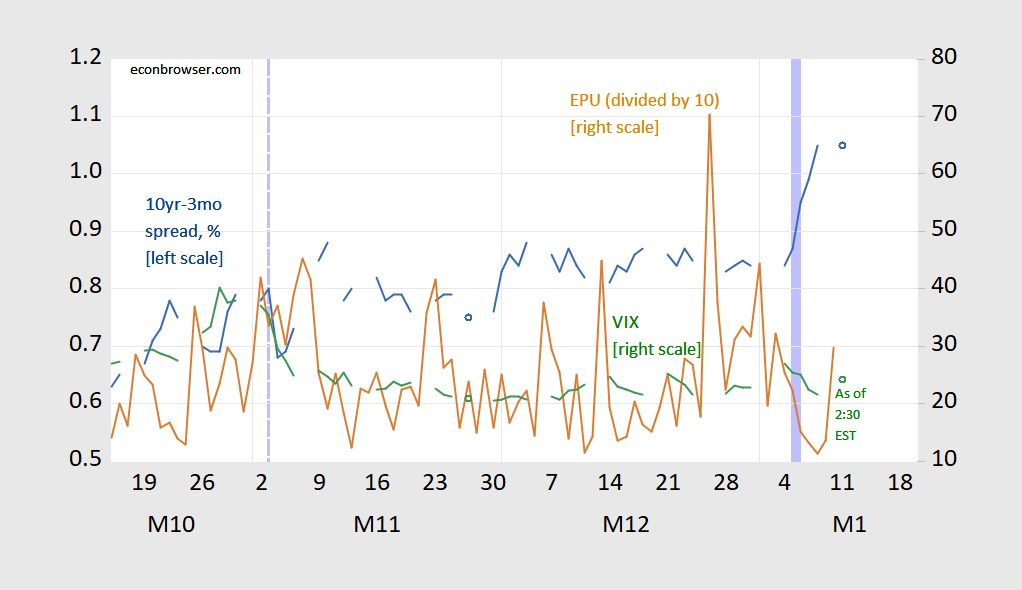

I’ve been amazed at how little the last week’s political turmoil has shown up in financial markets. The only thing that seems to have moved anything is the apparent control of the Senate moving to the Democrats.

Figure 1: 10yr-3mo Treasury spread, % (blue, left scale), VIX (green, right scale), and Economic Policy Uncertainty (EPU) index divided by 10 (brown, right scale). 1/11 observation for 2/30 EST. Light blue dashed line at 11/3 (election day); light blue shading at 1/5-1/6 (Georgia election, insurrection at Capitol).

You would think with the president of the United States inciting an insurrection against the legislative branch, there would be heightened perceived risk (VIX) and/or heightened uncertainty regarding the course of economic policy (EPU), but no pattern is apparent to my eyes.

The term spread on Treasury’s has increased. This outcome could be attributed to the expectations of either more fiscal stimulus and hence larger expected deficits, more vigorous anticipated growth, or both. These are the most commonly cited reasons for yield curve steepening.

Torsten Slok (Apollo) argues (not online) that a good portion of the steepening pre-Georgia (from August onward) is due to a rising term premium on ten year bonds:

“the entire reason why [ten year Treasury] rates have been going up since August is that the term premium is moving up, and it is now close to zero.”

The Christensen-Rudebusch estimates he bases this argument on only extends up to 1/4/2021, so we’ll have to wait to get a look at what portion of the post-Georgia steepening — which is qualitatively different from the August-December steepening — is due to changes in the term premium.

Addendum:

Let me be more explicit about the cause of the steepening.

If the level of the long term bond is given by:

then the 10 year- 3 month term spread is:

![]()

And the change in the 10yr-3mo spread, from one moment to another moment is:

![]()

With the three month Treasury yield pretty much constant, then the change in the spread can come from the change in the EHTS component, or change in the term premium.

My guess is that the markets are belatedly reflecting the instability that Trump and Moscow Mitch created, and that the Democrats will tame some of the instability. A Biden administration will be consistent and rational. That’s good for business. Apparently the market doesn’t think the MAGA insurrection will amount to much. Biden may raise taxes, but a better business climate will increase commerce. Paying taxes on money you have is better than having no money.

Another part of it is that the Biden administration will be competent when it comes to dealing with the pandemic. diaper donnie played golf. Biden will get on it. There will be glitches, no doubt, but things will start to happen. Until the pandemic is under control, the economy is on hold anyway.

Ockham says:

Fiscal policy matters a great deal, and can be priced in very quickly. Pure politics doesn’t allow for easy discounting. Thinking things through takes time, during which time political news changes.

Shorter Ockham:

It’s hard to price in what has never been priced in before.

Ockham would also like to point out that short-term trade is dominated by machines. If machines aren’t told to respond to “insurrection”, then most of the money ain’t gonna notice when a bunch of mindless drones attack democracy.

@ Macroduck

It appears you’ve completely confused our two resident know it alls. I kind of assumed you were speaking, at least in part, in a philosophical sense and about our “Madness of Crowds” folks at the U.S. Capitol. Maybe our two, “like….. geniuses and stuff”, never heard of Algorithmic programs for financial trading.

Next time use footnotes or prepare to be insulted and condescended to by Tweedledee in NYC and Tweedledum in Harrisonburg.

It is no longer a surprise that discussions of fact devolve into rude nonsense. That’s the internet. One adapts.

BTW, macroduck, you usually make smart and well-informed comments here. This one was garbled in various ways unfortunately. I observe that a nearly sure sign that you have messed up is when you have “Moses Herzog” rushing to your rescue.

Two questions: who is your Ockham.

And pray tell WTF does your little gibberish even mean? We have never seen change in fiscal policy? Sorry dude but you are making no sense here. None.

pgl,

He might be thinking about the guy with the razor, although the preferred spelling of that name is “Occam..”

Barkes you are RAZOR sharp

I believe he is referring to Gillette.

Tell you what. You learn some civility, then I’ll explain to you what you missed.

macroduck (and Moses Herzog),

Was noting that probably were probably referring to Occam rather than Ockham “uncivil”? How so? Both of you seem to be overreacting rather substantially with inappropriate self-righteousness.

Actually on looking at this more closely, heck, Moses, you are right. I am confused. I do not know what the heck point macroduck was trying to make with this peculiar set of claims. Can you elucidate?

On checking he must have had William of Occam (or “Ockham” if you prefer) in mind as there seems to be nobody else called “Ockham” out there. I thought possibly there was some current blogger or commentator using that moniker, but this does not seem to be the case. On googling in search of such a person all I got was an unpublished paper by my friend Giandomecha Becchia on a dual implication for economics of Occam’s Razor, Logic and Heuristics. Her argument is that Samuelson was an example of somebody invoking Occam’s Razor (her spelling, no “Ockham”) to support his version of neoclassical economics for its logical simplicity, while Herbert Simon’s bounded rationality was an invocation of it on heuristic grounds for simplifying based on a minimal set of realistic behavioral assumptions. But I do not see anything in macroduck’s rather confusing comments that fits any of this.

As it is, he wrote as if he was referring to something Occam wrote about fiscal policy in economics, but Occam never wrote anything about economics, which is what makes this so silly. And, needless to say, there is nothing in the comments that seems to invoke the idea of Occam’s Razor, which, just in case you do not know what it is (and sure as heck is not obvious that macroduck does either) is that if one has two competing explanations for a phenomenon, the simpler one is to be preferred. I see nothing referencing such a view in his garbled comments. Which is what brought on all the joking comments. Ockham? Ockham who? I mean, really. What a farce.

Some correction. The paper I mentioned has been published by the World Economic Association, and the name of the author, which I botched, is Giandomenica Becchio. She is at the University of Torino in Italy. The title of the paper is “The Blades of Occam’s Razor in Economics: Logical and Heuristic,” for anybody who wants to check it out.

Oh, and there is a sort of more direct connection between Occam and “economy.” His famous principle, Occam’s Razor, is sometimes called “the law of economy” or “the law of parsimony” due to it invoking a sort of intellectual cost minimization in its preference for the simplest, possibly measured to some degree by shortest, explanations for things.

Anyway, I frankly do not see how any of that has to do with what macroduck posted here. Usually you make more sense, md.

Until now, my response had nothing to do with you. pgl decided to dismiss what he did not understand, resorting to the language of a teenage MIW.

Now, however, you have self-righteously decided that I was self-righteous. Seems you have lapsed back into your old, vile self.

Gloves off? Happy to oblige.

macroduck

“old vile self”? Oh, this is your dark Moses Herzog imitator side coming out.

Your comment is incomprehensible and stupid. You and “Moses Herzog” have both been asked to elucidate your comments, and neither of you has obliged. Instead we get this singularly inappropriate and stupid scheiss, you whining about people being “uncivil” and “vile.” All I did was point out in detail how ridiculous your “Ockham says” bit was, which you have also never explained, and I am pretty sure you can’t, it was so silly and ridiculous.

If you want to hang out in a toilet with “Moses Herzog” be my guest, but very few here will respect you at all for it, given his vile misogyny and tendency to hateful sadism. Really. Deal with it.

But what’s the risk? Does anyone seriously believe at this point that there will be some successful coup?

Have the insurgents even declared an intent to take over the government, much less change economic arrangements? I just don’t see the relevance at this point.

Steven Kopits: In the asset pricing literature, the term premium has to do with the risk of unexpected inflation which causes capital losses on bonds. It might be useful to consult a money & banking textbook when venturing into finance. I recommend Schoenholtz and Cecchetti (which I used in my financial system course).

Menzie –

You write:

“I’ve been amazed at how little the last week’s political turmoil has shown up in financial markets. The only thing that seems to have moved anything is the apparent control of the Senate moving to the Democrats.

“You would think with the president of the United States inciting an insurrection against the legislative branch, there would be heightened perceived risk (VIX) and/or heightened uncertainty regarding the course of economic policy (EPU), but no pattern is apparent to my eyes.”

I am literally responding to your topic sentence. I am asking, why you would be ‘amazed’? An increased risk premium would be warranted if 1) you thought Joe Bide would not be sworn into office; or 2) a subsequent insurrection could succeed and result in a change fiscal or monetary policy, or 3) Biden would be compelled to change fiscal or influence monetary policy contrary to current expectations in response to an actual or threatened insurrection. None of these seem within the realm of possibility at the moment. Therefore, I see no reason to be ‘amazed’ that risk premia did not change with the storming of the Capitol.

My MBA was in finance and accounting.

So what’s the risk?

Trump is gone in nine days. Neither fiscal nor monetary policy is likely to change in the interval. No new legislation will be passed as the Senate is not in session and will not be again until the 20th.

So, again, what’s the risk? That Trump will start a war? Theoretically possible, but I doubt the bureaucracy would let him do it.

There could be the risk of a coup. But does anyone really think that’s likely at this point? And even if it happened, would fiscal or monetary policy change?

I suppose we could have a civil war, but at present that seems pretty unlikely.

Or perhaps Biden would need to change fiscal or monetary policy to accommodate Trumpian insurgents.

None of this looks particularly plausible.

Instead, the last event of note was the Democrats’ victory in Georgia, which may in fact prove material in outcome over time. And if I understand correctly, that’s what your post above indicates.

But otherwise, what is the risk, in your opinion?

Steven Kopits: As I indicated, in asset pricing referring to the US Treasury market, the term premium arises from the variability (and covariability) of inflation with wealth (or with consumption if using the consumption CAPM). Default risk is usually assumed away. Well, I guess I have to do a post on this…

If he’s not going to read the SF Fed link, do you really think he’ll read it?? It could still be educational for the rest of us, but, just saying……..

Wait – the term structure has steepened but it seems you think there is no rational explanation for this market observation. So I guess your finance textbook preached the gospel of irrationality? Please pay attention to the market before spouting off your next chirping.

Waving a degree around to assert understanding is commonly known a “credentialism”. It is a way or those who do not have a valid argument to excuse themselves from offering one.

You asked “what’s the risk?” Menzie answered not by identifying the risk directly, but by pointing to a point in his original text which narrowed the range of possible risks to one – an increase in uncertainty regarding inflation. And the best you have is to repeat your question?

It looks like what’s going on is that Menzie is raising a technical issue regarding risk spreads, but you want to talk about your political views. Oh, goody! Your point, if I understand you, is to trivialize the mob attack on the Capitol Building.

Menzie tries to prompt a discussion of financial market pricing. You insist on making the discussion about you political views. In the broader context of our country’s troubles, looks like you’re part of the problem.

I am not trivializing the storming of the Capitol.

I am asking a specific question related to the capital markets reaction thereto. In what sense would the riot at the Capitol affect interest rates? You are suggesting purely through sentiment, but I do not think the events there would make me or less likely to think my bonds would be repaid. If anything, it might suggest easier monetary policy.

“Have the insurgents even declared an intent to take over the government, much less change economic arrangements?”

Yes they have. We all hope they fail but you really do need to take your chirping to your own blog (where we can just ignore you).

Torsten Slok (Apollo) argues (not online) that a good portion of the steepening pre-Georgia (from August onward) is due to a rising term premium on ten year bonds:

“the entire reason why [ten year Treasury] rates have been going up since August is that the term premium is moving up, and it is now close to zero.”

Wait, 1-year government bond rates have been close to 10 basis points this whole time. 10-year rates were 0.5% and are now 1.1%. Not sure what close to zero means here but 10-year rates are still really low.

Slok uses an estimate of term premium not available beyond January 4. I’m on my phone, which cannot open spreadsheet files, so I can’t check, but I believe ACM term premium estimates are available on a more current basis. For anyone who cares to check:

https://www.newyorkfed.org/research/data_indicators/term_premia.html

Long ago and far away when I did a stint at outre risk analysis for a reinsurance company, the general assumption was that short of expropriation or monetary collapse, dangerous politics was a rounding error in terms of loss.

When folk bring up risk, I tell them to read up on what Swiss Re is saying…

By the way, your former industry has a role in the shape of the curve. Menzie has explained that term premium reflects uncertainty over future inflation. When looking at treasury yields as a simple adding up of expected funding costs, expected inflation and term premium, term premium is a catch-all for everthing but point estimates of funding costs and inflation. Any change in safe-haven demand, liquidity needs, central bank reserves or (recalling Menzie’s point about treasury default risk) default risk will show up as a change in term premium. If insurance portfolio duration needs change, the curve shows it. Banks’ tier 1 capital requirements helped drive down term premium.

Which is, of course, why Menzie raised the issue of spread stability in the face of political risk.

I would note that this rather sudden jump in the 10-year rate in the last week and a half or so is probably what Jim Bullard was looking at when he made his comments on Jan. 7 that had Moses unhappy on another thread. Bullard may be overly optimistic about what will happen on the output front, and possibly overly concerned by how much the rate of inflation will go up, but this sudden noticeable jump in the 10-year rate is consistent with both a faster rate of growth and some modest increase in the rate of inflation. After all, we are talking about something on the order of 200-300 basis points in the increase in the 10-year rate.

I would also note that in his comments on this Bullard did not call for a tightening of monetary policy, most precisely any slowdown in the current program of asset purchases that has been expanding the monetary base. This rise in the 10-year rate has happened despite that basically expansionary monetary policy continuing, so it reflects a market perception, however justified or not.

I also remind everybody that early last year it was Bullard who at the Fed first foresaw how hard the economy would plunge due to the pandemic and wisely pushed the Fed to adopt the strongly expansionary monetary policy that it did and basically continues. He supports that continuation and also in his talk warned that there is a great deal of uncertainty regarding the future impact on the economy of the pandemic, even as he expressed optimism that a rapid rollout of vaccines may well lay the groundwork for more rapid growth later this year, which would be consistent with the recent change in 10-year rates.

I shall add here that it is important that even though Bullard is forecasting some increase in the rate of inflation later this year, along with an increase in the rate of growth, he is not calling for a tightening of monetary policy. This may well be due to the Fed having a 2% inflation target, which has not been being met. So in fact he may welcome this forecasted increase in the rate of inflation if in fact it moves us close to that targeted rate of inflation.

January 11, 2021

Coronavirus

US

Cases ( 23,143,197)

Deaths ( 385,249)

India

Cases ( 10,479,879)

Deaths ( 151,364)

UK

Cases ( 3,118,518)

Deaths ( 81,960)

France

Cases ( 2,786,838)

Deaths ( 68,060)

Germany

Cases ( 1,941,119)

Deaths ( 42,097)

Mexico

Cases ( 1,534,039)

Deaths ( 133,706)

Canada

Cases ( 668,193)

Deaths ( 17,086)

China

Cases ( 87,536)

Deaths ( 4,634)

January 11, 2021

Coronavirus (Deaths per million)

UK ( 1,204)

US ( 1,159)

France ( 1,041)

Mexico ( 1,031)

Germany ( 497)

Canada ( 449)

India ( 109)

China ( 3)

Notice the ratios of deaths to coronavirus cases are 8.7%, 2.6% and 2.4% for Mexico, the United Kingdom and France respectively.

https://news.cgtn.com/news/2021-01-12/Chinese-mainland-reports-55-new-COVID-19-cases-WYZ7v5Ui08/index.html

January 12, 2021

Chinese mainland reports 55 new COVID-19 cases

The Chinese mainland on Monday recorded 55 new COVID-19 cases – 42 of local transmission and 13 from overseas, the National Health Commission said on Tuesday.

The domestic cases were reported in north and northeast China: 40 in Hebei Province, 1 in Heilongjiang Province and 1 in Beijing.

Eighty-one new asymptomatic COVID-19 cases were recorded, while 565 asymptomatic patients remain under medical observation. No deaths related to COVID-19 were registered on Monday, while 31 patients were discharged from hospitals.

The total number of confirmed COVID-19 cases on the Chinese mainland has reached 87,591, and the death toll stands at 4,634.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2021-01-12/Chinese-mainland-reports-55-new-COVID-19-cases-WYZ7v5Ui08/img/c55a7c3edc2347e19073429521330ff2/c55a7c3edc2347e19073429521330ff2.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2021-01-12/Chinese-mainland-reports-55-new-COVID-19-cases-WYZ7v5Ui08/img/ef57ed518a3c4fbe99e3859e3a1338e5/ef57ed518a3c4fbe99e3859e3a1338e5.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2021-01-12/Chinese-mainland-reports-55-new-COVID-19-cases-WYZ7v5Ui08/img/c09ae9b8d6024301950f02129b091713/c09ae9b8d6024301950f02129b091713.jpeg

[ There has been no coronavirus death on the Chinese mainland since the beginning of last May. Since the beginning of last June there have been only limited community clusters of infections, each of which was an immediate focus of mass testing, contact tracing and quarantine, with each outbreak having been contained. Symptomatic and asymptomatic cases are all contact traced and quarantined.

Imported coronavirus cases are caught at entry points with required testing and immediate quarantine. Cold-chain imported food products are all checked and tracked through distribution. The flow of imported cases to China is low, but has been persistent.

There are now 697 active coronavirus cases in all on the Chinese mainland, 18 of which cases are classed as serious or critical. ]

If they don’t build a statue in this man’s honor, this country has certainly gone down the crapper:

https://twitter.com/TheViewFromLL2/status/1348134679132647426

January 11, 2021

Coronavirus

Massachusetts

Cases ( 437,042)

Deaths ( 13,206)

Deaths per million ( 1,916)

————————————–

January 11, 2021

Coronavirus

New York

Cases ( 1,182,351)

Deaths ( 39,808)

Deaths per million ( 2,046)

[ Apparent public health failings that have to be examined and understood. ]

https://www.nytimes.com/2021/01/11/us/politics/cuba-terrorism-trump-pompeo.html

January 11, 2021

Pompeo Returns Cuba to Terrorism Sponsor List, Constraining Biden’s Plans

In announcing the move, Secretary of State Mike Pompeo cited Cuba’s hosting of American fugitives and Colombian rebels and its support for Venezuela’s authoritarian leader.

By Michael Crowley, Ed Augustin and Kirk Semple

WASHINGTON — The State Department designated Cuba a state sponsor of terrorism on Monday in a last-minute foreign policy stroke that will complicate the incoming Biden administration’s plans to restore friendlier relations with Havana.

In a statement, Secretary of State Mike Pompeo cited Cuba’s hosting of 10 Colombian rebel leaders, along with a handful of American fugitives wanted for crimes committed in the 1970s, and Cuba’s support for the authoritarian leader of Venezuela, Nicolás Maduro.

Mr. Pompeo said the action sent the message that “the Castro regime must end its support for international terrorism and subversion of U.S. justice.”

The New York Times reported last month Mr. Pompeo was weighing the move and had a plan to do so on his desk.

The action, announced with just days remaining in the Trump administration, reverses a step taken in 2015 after President Barack Obama restored diplomatic relations with Cuba, calling its decades of political and economic isolation a relic of the Cold War….

January 12, 2021

Coronavirus

Dominican Republic

Cases ( 184,788)

Deaths ( 2,427)

Deaths per million ( 223)

Cuba

Cases ( 15,494)

Deaths ( 155)

Deaths per million ( 14)

[ The Dominican Republic has had the fastest per capita growth in Latin American these last 50 years and has fared relatively well this last year, but Cuba for all the United States sanctions has fared remarkably well seemingly a reflection of a fine public health system. ]

https://fred.stlouisfed.org/graph/?g=zoHl

January 15, 2018

Life Expectancy at Birth for Cuba and Dominican Republic, 1971-2018

https://fred.stlouisfed.org/graph/?g=zoK8

January 30, 2018

Infant Mortality Rate for Cuba and Dominican Republic, 1971-2019

Latin American countries have recorded 4 of the 13 highest and 6 of the 25 highest number of coronavirus cases among all countries. Brazil, Colombia, Argentina, Mexico, Peru and Chile.

Mexico, with more than 1.5 million cases recorded, has the 4th highest number of cases among Latin American countries and the 13th highest number of cases among all countries. Peru, with more than 1 million cases, has the 5th highest number of cases among Latin American countries and the 18th highest number among all countries. Mexico was the 4th among all countries to have recorded more than 100,000 and 130,000 coronavirus deaths.

January 11, 2021

Coronavirus (Deaths per million)

US ( 1,160) *

Brazil ( 954)

Colombia ( 908)

Argentina ( 983)

Mexico ( 1,031)

Peru ( 1,154)

Chile ( 894)

Ecuador ( 798)

Bolivia ( 797)

* Descending number of cases

My guess is, and it is only a guess, that the mass of corporations now moving to withdraw PAC money from those legislators who voted not to recognize the popular vote and electoral college vote for President-Elect Biden, is what is now moving/driving this. Whether that is indeed the case or not, this is positive news:

https://www.nytimes.com/live/2021/01/12/us/impeachment-trump-25th-amendment

Of course IF Republican legislators were sane (I said IF they were sane) the fact that their lives were under threat after donald trump encouraging sedition and treason and that donald trump ordered that the National Guard not protect them from harm of death~~one might reasonably assume that would be a solid reason to impeach donald trump.

Of course Mike Pence thinks donald trump is an awesome person for attempting to have Pence hanged from the rafters of the U.S. nation’s Capitol. So really assuming sanity among Republicans who love “a president” who would hang all Republican legislators at the first advantageous opportunity given, is a quite challenging game of mental gymnastics. I wish anyone attempting that mental gymnastics~~good luck

Apparently some Republicans “get” donald trump endangered (and STILL endangers) their lives.

https://www.koin.com/news/washington/herrera-beutler-i-will-vote-to-impeach-trump/

I wish I could say I expect the same behavior from all Republicans after their own lives were endangered. But I’ve seen enough of the likes of cowards like James Lankford and Rod Rosenstein to know differently. Obviously Luke Letlow isn’t the only Republican with a self-destructive bent, if it means he can wear the MAGA hat of Fascism.

I don’t like the desecration and misrepresentation of the image of Jesus. Yet, put in its proper context, as the true target being not Jesus, but those who are grossly hypocritical and falsely labeling themselves “Christian”, this meme seems dead on accurate to me:

https://i.redd.it/0gqw5c84c1b61.jpg

It is the same as the MAGA crowd self-professing themselves “Blue Lives Matter” and then beating to death a Capitol policeman. And then MAGA folks claiming they are “Christian”. They claim these fraternity memberships whenever the immediate convenience presents itself, but their actions show what they truly are.

The historic Jesus was probably named Jeshua and probably looked like an Arab, not a white guy. So, it a way, a spoof like that isn’t all that bad. The idea that some of these people who wave religion around in support of violence and prejudice are even remotely Christian is laughable.

A different topic (international trade) but maybe Menzie might comment on the latest from Forbes who has been talking to a couple of people who know nothing about international trade:

https://www.forbes.com/sites/edgarsten/2020/12/21/catastrophe-predicted-if-no-uk-eu-free-trade-agreement-reached-by-deadline/?sh=3e45806b69ac

The issue here is what will be the consequences of Brexit for the UK based automobile sector. The know nothings use alarmist words like catastrophe. But what are people who actually understand this issue saying?

Thought this was a well written story. It’s no wonder Republican legislators always sound so certain “Government doesn’t work”. They lean their elbow on the scale everyday to make certain it doesn’t—even if it’s their won constituents. But you watch those toothless illiterates in Kentucky. Just like in Oklahoma they’ll go out and vote in droves for the same Rand Pauls and Mitch McConnells that work overtime to see that everyday of their lives is spent in penniless and in never-ending financial debts:

https://www.nytimes.com/2020/12/28/business/economy/kentucky-economy.html