Today, we are pleased to present a guest post written by David Papell and Ruxandra Prodan, Professor and Instructional Associate Professor of Economics at the University of Houston.

As the June 2021 Federal Open Market Committee (FOMC or Committee) meeting approaches, the uncertain recovery of the economy from the effects of the Covid-19 pandemic has led to increased speculation regarding when the FOMC will raise the federal funds rate (FFR) from the current effective lower bound (ELB). In a new paper, Policy Rules and Forward Guidance Following the Covid-19 Recession, we compare the FFR prescribed by various policy rules with (1) the actual path of the FFR following the Great Recession and (2) the projected path of the FFR with FOMC forward guidance followed by the policy rule in Clarida (2020).

The FOMC adopted a far-reaching Revised Statement on Longer-Run Goals and Monetary Policy Strategy in August 2020. The framework contains two major changes from the original 2012 statement. First, policy decisions will attempt to mitigate shortfalls, rather than deviations, of employment from its maximum level. Second, the FOMC will implement Flexible Average Inflation Targeting where, “following periods when inflation has been running persistently below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.”

At its September 2020 meeting, the Committee approved outcome-based forward guidance, saying that it expects to maintain the target range of the FFR at the ELB of 0 to ¼ percent “until labor market conditions have reached levels consistent with the Committee’s assessment of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.” In the Summary of Economic Projections (SEP) released following the March 2021 meeting, the median projection of the members for the FFR was 0.1 percent through the end of 2023.

We consider six policy rules. The Taylor (1993) rule prescribes that the FFR equal the inflation rate plus 0.5 times the inflation gap, the difference between the inflation rate and the 2 percent inflation target, plus 1.0 times the unemployment gap, the difference between the rate of unemployment in the longer run and the realized unemployment rate, plus the neutral real interest rate. The balanced approach rule in Yellen (2012) raises the coefficient on the unemployment gap to 2.0 while maintaining the coefficient of 0.5 on the inflation gap. The Taylor and balanced approach (shortfalls) rules are identical to the original rules except that they don’t prescribe a rise in the FFR when unemployment falls below longer-run unemployment.

Neither the original nor the shortfalls rules are consistent with the revised statement. We introduce two new rules in accord with the revised statement that we call the Taylor and balanced (consistent) approach rules. First, we replace the rate of unemployment in the longer run with the unemployment rate consistent with maximum employment and base FFR prescriptions on shortfalls instead of deviations. Second, if inflation rises above 2 percent, the rule is amended to allow it to equal the inflation rate “moderately” above 2 percent that the FOMC is willing to tolerate “for some time” before raising rates in order to bring inflation down to the 2 percent target.

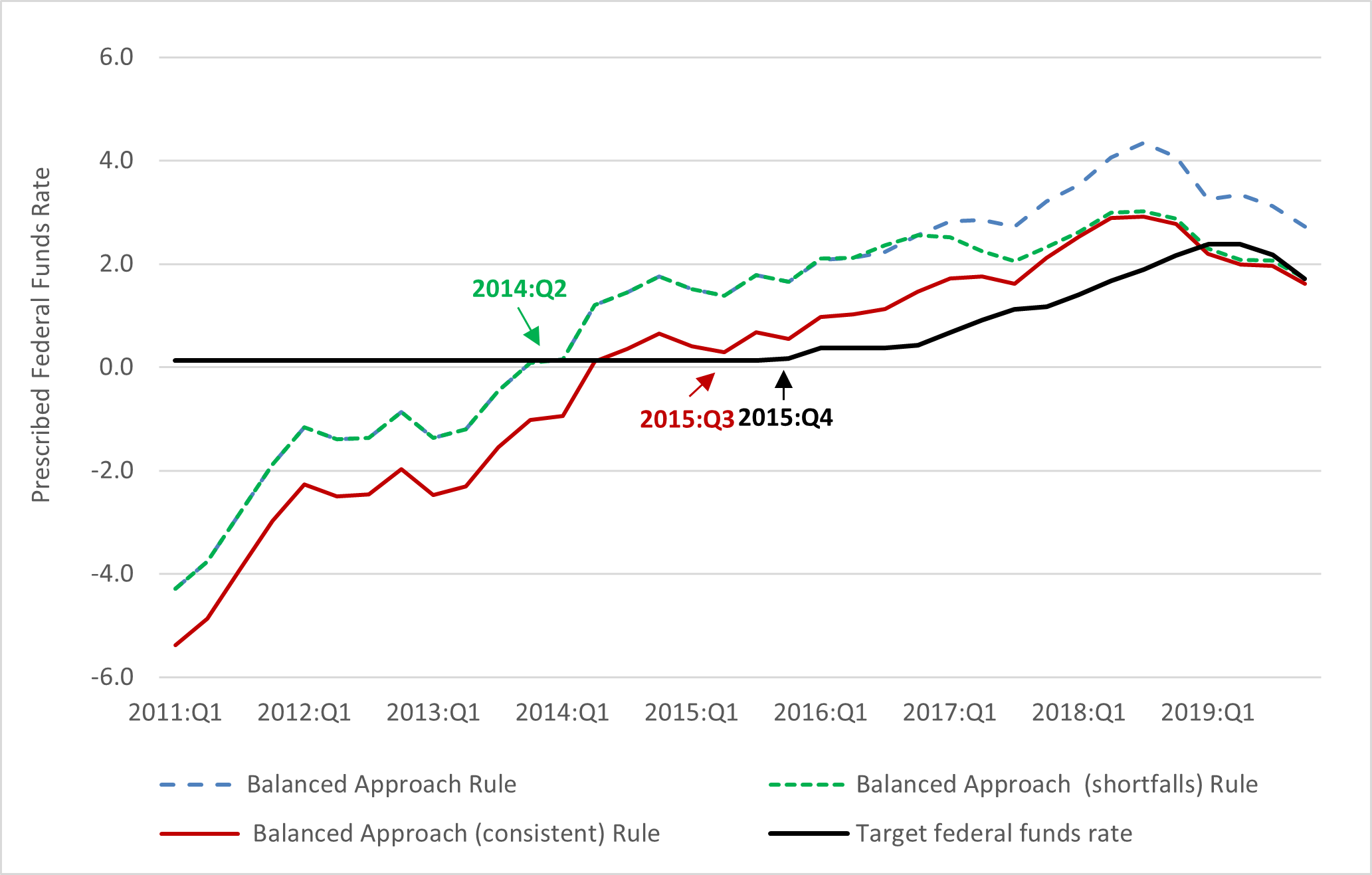

Figure 1 depicts the FFR prescribed by the original, shortfalls, and consistent balanced approach rules following the Great Recession, as well as the actual FFR. A similar diagram for the three Taylor rules is in the paper. The consistent rule prescribes a liftoff from the effective lower bound (ELB) that is very close to the actual liftoff with deviations between the prescribed and actual FFR’s that are smaller than with the original and the shortfalls rules. At the end of 2019, the prescriptions from the shortfalls and consistent rules are very close to actual policy.

Figure 1. Policy Rules Following the Great Recession

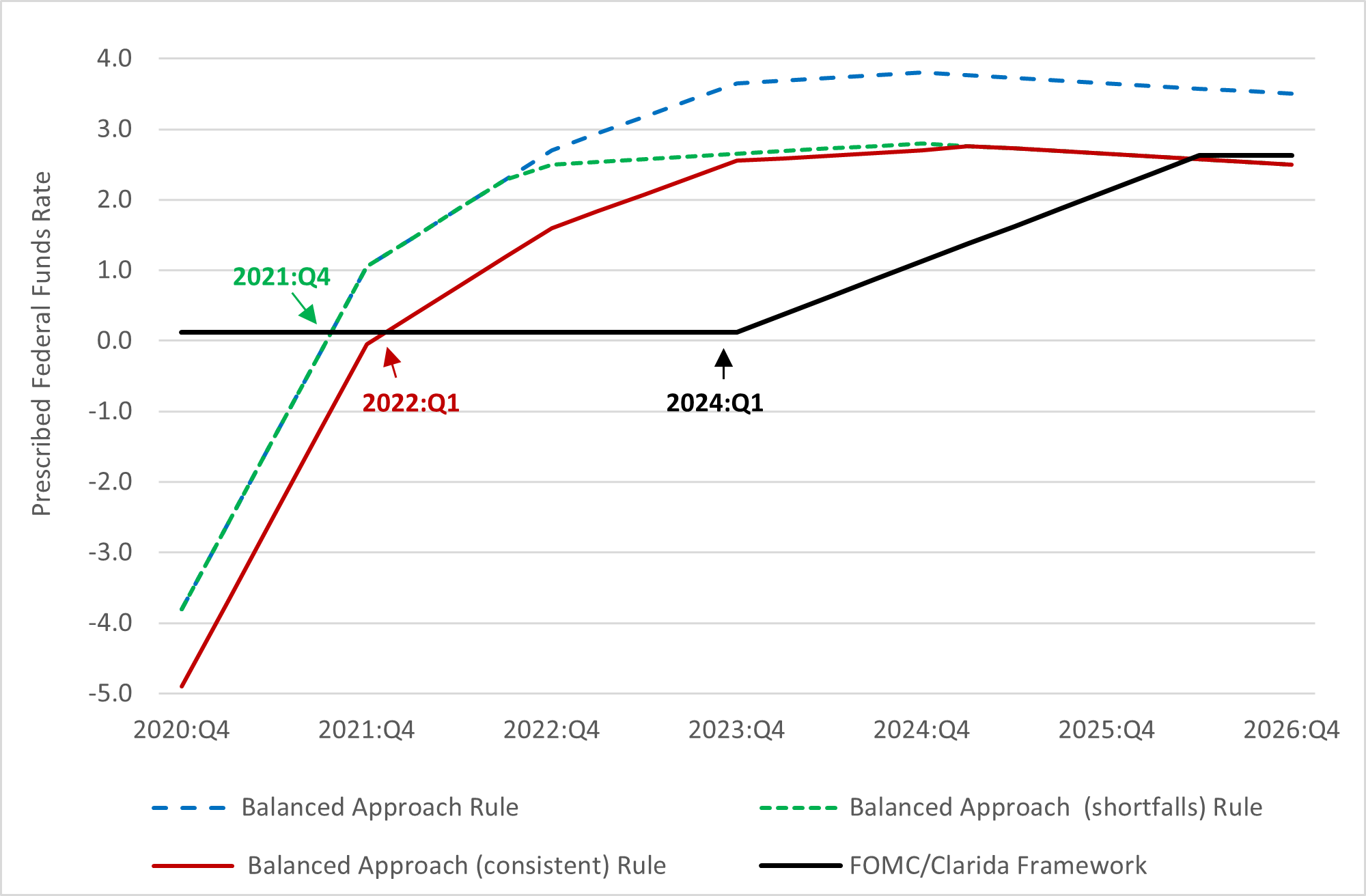

Figure 2 illustrates the FFR prescribed by the three balanced approach rules following the Covid-19 recession based on SEP inflation and unemployment projections through 2023 and our projections thereafter. The figure also shows the SEP projections that the FFR will remain at the ELB through the end of 2023 followed by the prescriptions from the policy rule in Clarida (2020). All three policy rules prescribe liftoff from the ELB before the SEP projections, there is a gap of at least 2.5 percent at the end of 2023 between the prescriptions from the policy rules and the ELB prescribed by the FOMC’s forward guidance, and the gap between the prescriptions with the shortfalls and consistent rules and the Clarida rule is eliminated by mid-2026. If inflation rises faster than our projections, the prescribed FFR will increase faster under both the policy rules and the FOMC/Clarida framework, but it will not change the relation between the two prescriptions.

Figure 2. Policy Rules Following the Covid-19 Recession

Policy rules are an important input for monetary policymaking. As described in the February 2021 Monetary Policy Report, “Policymakers consult policy rule prescriptions derived from a variety of policy rules as part of their monetary policy deliberations without mechanically following the prescriptions of any particular rule.” The prescriptions from the balanced approach (consistent) rule are in accord with the revised statement, very closely match the exit from the effective lower bound in December 2015, are almost identical to the federal funds rate at the end of 2019, prescribe a faster pace of normalization following the Covid-19 recession than the FOMC forward guidance, and converge to the FOMC/Clarida framework by 2026:Q2.

This post written by David Papell and Ruxandra Prodan.

https://www.hoover.org/sites/default/files/papell_paper-policy_rule_forward_guidance_11-09-2020.pdf

November 9, 2020

Policy Rule Forward Guidance Following the Covid-19 Recession

By David H. Papell and Ruxandra Prodan

Abstract

The Federal Open Market Committee recently adopted a far-reaching revised Statement on Longer-Run Goals and Monetary Policy Strategy. The two major changes are that the Committee will implement flexible average inflation targeting and will mitigate shortfalls, rather than deviations, of employment from its maximum level. At its September meeting, the Committee approved enhanced forward guidance, which maintains the federal funds rate at the effective lower bound until maximum employment is achieved and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. We first show how policy rules could be modified to be consistent with the revised statement and included in future Monetary Policy Reports. We then propose policy rule forward guidance as an alternative mechanism for the Committee to communicate the eventual exit from the effective lower bound and beyond which is consistent with both the revised statement and the Committee’s projections through 2023. In contrast with enhanced forward guidance, policy rule forward guidance removes accommodation as the economy improves. We describe scenarios with average, fast, and slow recoveries to illustrate how policy rule forward guidance could work in practice.

[ This and the new paper are interesting, but the Board of Governors expressly does not want to tie itself to a policy rule at this point since it is unclear what rule would suffice. This recession was seemingly unique and Fed caution as to what recovery is seems warranted. ]

So you try six rules and people are assumed to believe that each will last forever and ever. Hmm.

When you are John B. Taylor who wrote the original “rule” I guess you are given the right to declare your rule the only correct version. Never mind that the Wicksellian natural rate of interest has clearly declined since 1993 – we are talking about the sainted John B. Taylor.

When I read that second mention of “John B. Taylor,” I heard it a la “Randolph Scott.” I know pgl knows what I’m referring to.

It’s interesting to me that both the “consistent” and “shortfall” rules would have generated negative FFRs during the first part (the worst part) of the Great Recession when the target rate was zero. ISTR at least several macroeconomists calling for the Fed to explicitly target negative rates during that time, even though it would have been difficult to achieve.

Bob,

Clearly one should rely on a weighted average of the rules, although maybe some rules are more equal than others, as pgl suggests.

BLS payroll survey reports 559 thousand new jobs:

https://www.bls.gov/news.release/empsit.nr0.htm

Household survey reports employment to population ratio inches up to 58%.

I’m reading Dean Baker’s email on the BLS report and this caught my eye:

The private sector accounted for 492,000 of the May job growth, as state and local governments added back just 78,000 workers in the month (the federal government lost 11,000 jobs). State and local employment is still 1,191,000 below its pre-pandemic level, with the vast majority of this gap in education. With the end of the regular school year this month, pandemic closings will be less of an issue in June, but presumably all schools will be open again for in-class instruction in the fall.

The private sector is down 6,462,000 jobs since February 2020. At the May rate of job growth, it will take just over 13 months to make up the gap.

We are getting a rather steady diet of Chinese State Sponsored lies about Sinovac being 100% effective. I’m not the only one calling ltr out on this. I have asked her to produce even one credible statement on efficacy. She has refused to do so. This account notes in the various trials, efficacy is put at just over 50% to just under 84%. Not 100%.

https://www.nasdaq.com/articles/sinopharm-sinovac-covid-19-vaccine-data-show-efficacy-who-2021-03-31-0

Look it is great they have something and are producing it but can we please end this campaign of disinformation?

http://www.xinhuanet.com/english/2021-06/04/c_139989125.htm

June 4, 2021

Over 723 mln COVID-19 vaccine doses administered across China

BEIJING — Nearly 723.49 million doses of COVID-19 vaccines had been administered across China as of Thursday, the National Health Commission said Friday.

[ China has now administered more than 723 million doses of coronavirus vaccines domestically, and another 350 million vaccine doses have been distributed internationally. There are 5 Chinese developed vaccines being administered with approvals by the World Health Organization or a range of national health authorities. Domestically, 20 million vaccine doses are being administered daily. ]

chinese efficacy is around 50%. so it produces a coin flip for protection. better than nothing, but not going to get us to herd immunity.

Thank you as we know ltr will never mention this.

https://cepr.net/jobs-2021-06/

June 4, 2021

Economy Adds 559,000 Jobs in May; Unemployment Drops to 5.8 Percent

By DEAN BAKER

Black teen unemployment hit a record low of 12.1 percent in May.

The May employment report was somewhat weaker than had generally been expected, with the economy adding 559,000 jobs. On the household side, the unemployment rate fell by 0.3 percentage points to 5.8 percent. While this is still high by any reasonable measure, it is worth noting that the unemployment rate did not get this low following the Great Recession until October of 2014.

[Graph]

The employment-to-population ratio (EPOP) edged up to 58.0 percent, which is 3.1 percentage points below the pre-pandemic level. By this measure, the gender differences in the hit from the pandemic have largely disappeared, the women’s EPOP for May was 53.1 percent, down 2.3 percentage points from its average in 2019. For men the May EPOP was 63.4 percent, down 3.2 percentage points from its year-round average of 66.6 percent in 2019. However, in payroll employment, women’s share was 49.8 percent in May, compared with 50.0 percent before the pandemic.

(It is important to note that states that ended unemployment insurance supplements would not likely affect the May data. The termination did not take effect until June, the reference point for the survey is May 12th.)

Private Sector Performance Was Strong, as Governments Lag in Rehiring Workers

The private sector accounted for 492,000 of the May job growth, as state and local governments added back just 78,000 workers in the month (the federal government lost 11,000 jobs). State and local employment is still 1,191,000 below its pre-pandemic level, with the vast majority of this gap in education. With the end of the regular school year this month, pandemic closings will be less of an issue in June, but presumably all schools will be open again for in-class instruction in the fall.

The private sector is down 6,462,000 jobs since February 2020. At the May rate of job growth, it will take just over 13 months to make up the gap.

Restaurants Biggest Source of Job Gap

In absolute numbers, restaurants make up the largest chunk of this shortfall, with employment still down 1,480,000 from the pre-pandemic level, after adding 186,000 jobs in May. While many employers claim that they aren’t hiring because they can’t find workers, it’s not clear how much impact this shortage is having. Wages have been rising rapidly for nonsupervisory workers in the industry, a 22.2 percent annual rate comparing the average of the last three months (March, April, and May) with the prior three months (December, January, and February), but the average workweek actually fell slightly in May, from 25.3 hours to 25.1 hours.

On the plus side, the index of aggregate hours in the industry is still 12.4 percent below its pre-recession level. With restaurant sales likely passing their pre-pandemic level in May, this implies a huge gain in productivity. This is true more generally, as the overall index of aggregate hours for May stood 3.6 percent below the February level, even as output is virtually certain to pass pre-pandemic levels in the quarter.

Big Job Gains in Most Troubled Sectors

The health care sector, which is down 508,000 jobs from before the pandemic, added 22,500 jobs in May. Nursing care facilities, which are down 202,000 jobs, added back just 1,000 jobs in May, after losing 17,700 in April. This is a sector where low and poor working conditions may make it difficult to attract workers.

Hotels, which are down 526,000 jobs, added 34,600 jobs in May. The other services category, which includes sectors such as hair salons and dry cleaners and is down 353,000 jobs, added 10,000 jobs in May. The retail sector, which is down 411,000 jobs, actually lost 5,800 jobs in May. This is another sector where it seems there have been strong productivity gains. The motion picture sector, which is among the worst hit in percentage terms, down 157,000 jobs or 35.6 percent, added 13,900 jobs in May.

Construction and Manufacturing Coping with Shortages

Construction lost 20,000 jobs in May after losing 5,000 in April. This is likely due to temporary shortages of building material, most importantly lumber. Manufacturing added 23,000 jobs, reversing most of the job loss in April, as it seems auto manufacturers are finding ways to deal with the semiconductor shortage.

Recovery Continues to Benefit More Educated Workers

The unemployment rate for college grads fell 0.3 percentage points to 3.2 percent in May. It is down 0.8 percentage points from the start of the year. By contrast, the unemployment rate for high school grads dropped just 0.1 percentage points to 6.8 percent. It has fallen 0.3 percentage points since January.

Black Teen Unemployment Hits a Record Low

The unemployment rate for Black teens fell to 12.1 percent in May, by far the lowest level on record. These data are highly erratic, so we may see a big jump in future months, but it does seem to indicate they are doing relatively well in the current labor market.

The overall Black and Hispanic unemployment both dropped 0.6 percentage points in May, to 9.1 percent and 7.3 percent, respectively. The unemployment rate for Asian Americans is still somewhat higher than for whites, 5.5 percent compared to 5.1 percent for whites. It was slightly lower pre-recession….

https://www.nytimes.com/2021/06/04/opinion/jobs-report-labor-shortage-hiring.html

June 4, 2021

Wonking Out: Do hiring headaches imply a labor shortage?

By Paul Krugman

Don’t pay too much attention to today’s jobs report; it came in slightly below expectations, but given the noisiness of the data (and the extent to which the numbers are often revised), it told us very little that we didn’t already know.

The truth is that two things are clear about the U.S. economy right now. It’s growing very fast, and adding jobs at a rapid clip; but the pace of job creation is being crimped, at least a bit, because employers are having a hard time finding as many workers as they want to hire.

Sometimes complaints about a lack of willing workers just mean that companies don’t want to pay decent wages, and there’s no doubt some of that is going on. But this time that’s not the whole story. The latest Beige Book — the Fed’s informal survey of business conditions — suggests both that a number of companies really are having trouble adding workers as fast as they’d like, and that this is happening even though some are raising wages, offering signing bonuses, etc.

But what, if any, policy conclusion should we draw from this evidence? Republicans say that it means that we must cut benefits for the unemployed (and so many Republican-controlled states are now cutting aid, even though the federal government was actually bearing the cost). But they always say that, whatever is happening to the economy.

Many others point to lack of child care, with schools still closed in some states and normal day care crippled by the lingering effects of the pandemic. And fear of infection is still out there, despite a vaccination campaign that has proceeded faster than almost anyone expected.

There may be truth to all of these stories — yes, even some role for unemployment benefits, although the impact is probably modest. But are we just overthinking this? How much of the issue is simply that it takes some time to get the economy back up to speed from a standing start?

Thank you for your support. Want to share The New York Times? Friends and family can enjoy unlimited digital access to our journalism with this special offer.

I’ve been struck by reporting from Britain, which has been even more successful than the United States in achieving widespread vaccination (thank you, National Health Service). The thing is, Britain and America took very different approaches to supporting workers through lockdown. Where we relied mainly on enhanced unemployment benefits, Britain relied mainly on a “job retention” scheme — subsidizing earnings of workers placed on temporary leave by employers in locked-down sectors.

This scheme meant that Britain experienced much less of a rise in measured unemployment than we did, even though it suffered a deep economic slump:

https://static01.nyt.com/images/2021/06/04/opinion/krugman040621_1/krugman040621_1-articleLarge.png

The British did it differently.

You might think this would also make it easier for Britain to quickly restore its economy as the pandemic fades. Instead, the British press is full of reports about employers having a hard time finding workers.

So maybe the problem is simply that it’s hard to get the economy restarted in a few months.

One indicator many of us have been looking at during this weird economic period, in which facts on the ground change too quickly for standard statistics to keep up, is the number of diners reported by the reservation service OpenTable.com. OpenTable conveniently provides data on the number of seated diners during the pandemic relative to those on the corresponding date in 2019. Here’s what it looks like:

https://static01.nyt.com/images/2021/06/04/opinion/krugman040621_2/krugman040621_2-articleLarge.png

A dine-amic recovery.

Some automakers used to promise that their cars could go from zero to 60 in 16 seconds; well, the U.S. restaurant sector is trying to go from minus 60 — 60 percent below its prepandemic level — to zero in roughly 16 weeks. Why imagine that this could happen smoothly?

It’s true that some fairly old history might have made economists complacent.

Most forecasters expect U.S. economic growth this year to be the fastest since 1984, when the economy was going through the “morning in America” boom after the double-dip recession of 1979-82. Superficially, neither that recession nor the boom that followed looked anything like recent events. At a deeper level, however, there are some similarities.

In particular, the early ’80s slump, like the 2020 slump, was brought on by a sort of exogenous shock — in the earlier case, a huge rise in interest rates as the Fed tightened money to curb inflation. The impact of this shock, like that of Covid-19, fell especially hard on one sector — housing, rather than travel and leisure — which then sprang back rapidly as the headwinds abated:

https://static01.nyt.com/images/2021/06/04/opinion/krugman040621_3/krugman040621_3-articleLarge.png

Morning in construction….

https://fred.stlouisfed.org/graph/?g=Ev53

January 15, 2018

Unemployment Rates for United Kingdom and United States, 2017-2021

https://fred.stlouisfed.org/graph/?g=Ev86

January 30, 2018

Privately owned housing starts, 1978-1987

I am confused. What does this have to do with anything?

It helps those who want to find ways in which a government which kills tens of millions of its own people over the last 72 years and currently runs multiple concentration camps for minorities and federal prisons which equate to concentration camps is really a wonderful humanitarian outfit. If that’s supposed to make Americans and American corporations feel good about purchasing goods from those who manage those concentration camps and slave labor camps, I can’t say. Maybe/mostly you’re just supposed to shrug your shoulders and enjoy your cheap tech devices and cheap clothes.

https://xjdp.aspi.org.au/map/?