Conventional wisdom (sovereign debt crisis and austerity measures) or oil as cause? Steven Kopits says oil:

The cause of a brutal recession in Europe during Q4 2011 – Q1 2013 remains unexplained in policy circles. Or more precisely, the proposed explanation is less than compelling. … oil prices once again returned to high levels, with Brent regularly in the $100 – 115 range. With this, oil consumption in both the US and Europe began to decline, and such declines in oil consumption due to high prices — normally characterized as an oil shock — invariably leads to recession. … to suggest a Greek financial crisis could cause a recession in Europe is not entirely convincing. Greece’s GDP is all of 2% of that of the EU. It would be like a financial crisis in Indiana taking down the US economy. Conceivable, but it does not jump out at you.

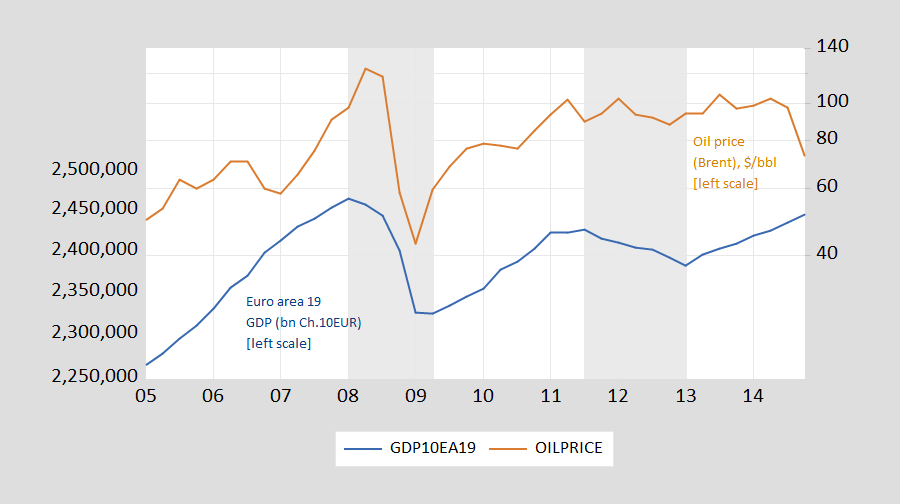

Here’s a picture of Euro area real GDP against nominal oil prices (Brent):

Figure 1: Euro Area 19 GDP in mn Ch.2010EUR (blue, left log scale), price of oil (Brent), $/bbl (brown, right log scale). CEPR defined peak-to-trough recession dates shaded gray. Source: EuroStat via FRED, EIA, CEPR.

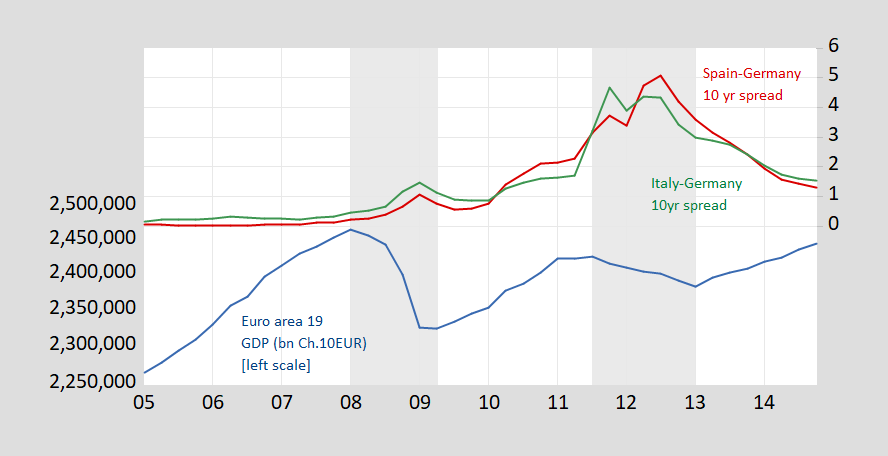

And here’s a picture of sovereign spreads for Spain and Italy (of the GIIPS). Notice, I’m not including Greek spreads.

Figure 2: Euro Area 19 GDP in mn Ch.2010EUR (blue, left log scale), Spain-Germany 10 year sovereign bond yield spread (red, right scale), Italy-Germany spread (green, right scale), both in %. CEPR defined peak-to-trough recession dates shaded gray. Source: EuroStat via FRED, OECD via FRED, CEPR.

My interpretation of Figure 2: with concerns about debt unsustainability, austerity was forced onto GIIPS, resulting in higher default risk premia, that then made debt sustainability even less plausible. In the end, austerity proved contractionary (there was no expansionary fiscal contraction). Only when the ECB intervened to cap yields did growth resume. Oil does not figure in as a primary factor in any interpretation I’m aware of (save Mr. Koptis’s). In other words, I would say the cause of the 2011-13 Euro area recession is not unexplained in policy circles.

More discussion here.

https://www.statista.com/statistics/695882/number-of-car-shipments-made-by-the-italian-sports-car-company-ferrari/

Vroom! Vroom!

Car shipments made by the Italian sports car company Ferrari from 2011 to 2021

This is your measure of EU GDP? Ferraris? OK – apologies to Princeton Steve as he is only the 2nd dumbest troll here.

PaGLiacci,

You might have the slightest clue of why I provided that link, but ONLY if you were capable of keeping up with the discussion. Alas, here we are (yet again) with PaGLiacci showing up to the discussion with egg running down their face. The tragic clown has struck yet again. HonkHonkHonkHonk

Did Mommy buy little Econned a new car? Your little comment added nothing to the discussion – as usual. But if you think you had a point to make – then try doing so. This should be fun.

At least you’re now admitting that you haven’t a clue what’s going on. But it’s not like anyone required your buying-in to the painfully obvious fact of your obliviousness. And per usual, you’re so completely unaware of your surroundings that you actually expect others to do the lifting for you. Your routine is quite comical. Tragic but comical!

pgl,

Now now, don’t you know that Ferrari is the fundamental driving force of the entire EU economy???????

Econned

May 2, 2022 at 3:09 pm

Yep – never had a point as usual. You are just a dumb angry troll. Do you spam other economist blogs as well? Oh wait – they banned your worthless rear end. Never mind.

“Barkley Rosser”,

Now now, don’t you know that “academics” should be better than making ridiculous and unfounded assumptions of another’s comments?????? That the fundamental driving force of being an “academic” is the ability to…. research before making idiotic comments??????

“Barkley Rosser” hahahaha yeah right.

PaGLiacci

May 3, 2022 at 12:52 am

Tell me who am I “trolling” and wtf are you doing in your reply?

Econned,

In 2021 Ferrari earnings were 1.7 billion euros, while the GDP of the Eu was 17.1 trillion euros. So, Ferrari is about one thousandth of the EU economy. Yeah, it sure drives that economy. Wow, you are sooooo brilliant.

“Barkley Rosser”,

I never once even hinted that Ferrari drives the EU economy. Nothing even close. You are (again) suggesting things that are untrue. Please keep up with the conversation or don’t say anything at all. Your ignorance is not very becoming. You certainly do not act nor apply critical reasoning like one would expect an academic to do.

Ooooops! 1.7 billion is one then thousandth of 17.1 trillion, not one thousandth, even more trivially miniscule.

“Barkley Rosser”,

So not only is your online identity representative of a faux academic who makes ridiculous and unfounded assumptions, but you also fail at basic arithmetic. Another great showing at embarrassing yourself.

“Econned

May 3, 2022 at 5:50 am

“Barkley Rosser”,

Now now, don’t you know that “academics” should be better than making ridiculous and unfounded assumptions of another’s comments?????? That the fundamental driving force of being an “academic” is the ability to…. research before making idiotic comments??????”

Glad to see you admit you are no academic as your research skills are nonexistent and all of your comments are truly idiotic. Vroom! Vroom!

Holy sh*t, please enlighten me oh tragic clown.

It is truly amazing how Princeton Steve goes on and on with his declarative statements without a shred of empirical support for them. Damn it – only oil matters so do not bother him with any other plausible story. Damn it – only oil matters so do not bother him with empirical evidence.

Look – he has been doubling down on his incessant BS for years. Why stop now?

BTW – I suspect Stevie will triple down on his old comments and then provide us with a link to his blog post.

DO NOT WASTE YOUR TIME reading his incessant babble as it is the same old discredited nonsense over and over.

Stevie tried to dismiss tight monetary policy from the ECB as he claimed interest rates rose by a mere 0.5%. First of all any increase in interest rates can lead to a recession if other demand factors are weak. But check out the 10-year German government bond rate (which of course Stevie did not provide maybe because he is too stupid to do so):

https://fred.stlouisfed.org/series/IRLTLT01DEM156N

Interest rates from 2.3% to 3.3%. Now my preK teacher told me that represents a 1.0% increase not a 0.5% increase. So I have to wonder WTF Stevie learned during preK arithmetic classes.

https://english.news.cn/20220502/221bea0b61534546b39a8f493fdd72a5/c.html

May 2, 2022

Chinese EVs gaining popularity in Israel with green vision

Chinese automakers have gained more and more popularity in the Israeli market with electric vehicles (EVs) amid the Israeli government’s ambitions to gradually phase out fossil fuel vehicles.

In a showroom of China’s automaker Geely Auto Group in the central Israeli city of Tel Aviv, Segal Yafa, a buyer from the south of the city, has signed a contract for three China-manufactured Geometry C electric vehicles.

“One for my husband, one for myself, and one for my friend,” Yafa told Xinhua.

Most Israelis began to know about the Chinese brand Geely since its launch of Geometry C EV in November 2021. With dashing looks and affordable prices, Geometry C has achieved a strong market share here quickly, becoming the winner in the “Best Buy of the Year” category for 2022 nominated by Israel’s major car magazine Auto.

“Good price, strong power and less pollution… it gains a good reputation,” Yafa explained the reason for her choice.

Ronan Yablon, CEO of Geely Israel, told Xinhua that they have received more than 8,000 orders in less than five months.

Geely is a good example of the Chinese EVs in the Israeli market over recent years amid an ambitious green vision of the country.

According to a plan initiated by the Israeli Ministry of Energy in 2018, the import of vehicles powered by polluting fuels will be banned as of 2030, which makes EVs an irreplaceable choice for the public.

“The plan affects the welfare of all, and should not be delayed,” read a statement from the ministry about the plan.

Yablon noted that “one of the most important goals with electric vehicles is to lower pollution.”

To encourage the import and purchase of EVs, the Israeli government has offered tax incentives and free registration for EVs. Until 2023, Israel plans to tax EVs at a significantly lower rate of 10 percent, compared with regular vehicles at 83 percent.

In addition, a total of 30 million new shekels (9.11 million U.S. dollars) have been allocated for the public EV charging infrastructure across the country.

“Most consumers in Israel are the middle class who value price advantages. We do have European EV makers, but they are more expensive, and Chinese EVs are good value for money,” Tomer Hadar, an automotive editor for Calcalist, Israel’s largest financial newspaper, told Xinhua….

Anyone trained in international macroeconomics would note that tight ECB policy would tend to appreciate the Euro which would lower EU net exports. Note at the beginning of the period Stevie choose to discuss, the Euro’s value rose from $1.22 to $1.44:

https://fred.stlouisfed.org/series/EXUSEU/

But Stevie has dismissed the role of monetary policy here. I’m sorry but Stevie is so an incredible level of ignorance and incompetence.

https://fred.stlouisfed.org/graph/?g=ONbd

January 15, 2018

Government gross debt as a share of Gross Domestic Product for Greece and Italy, 2000-2020

https://fred.stlouisfed.org/graph/?g=ONbA

January 15, 2018

Government debt as a share of Gross Domestic Product for Ireland, Portugal, Spain, Italy and Greece, 2000-2020

Stevie asserts that the U.S. cannot go into recession due to an oil shock because of high domestic production of oil, while Europe went into recession because of high reliance on oil imports. This is pure magical structural thinking. Magical because it relies on belief rather than on empirical evidence. We don’t need to follow the oil price shock through the data. He just says it and we should believe it. Stevie is pretending his view is received wisdom (“less than compelling”), a comical pose that he indulges in regularly; Stevie’s the High Priest of Oil.

But let us not forget, Stevie wants us to believe that Europe shouldn’t be messing with Putin because Putin has oil. Stevie’s magical structural belief may predate Russia’s latest invasion of Ukraine, but he dragged it out now to support his view that Putin is god-like because Putin has oil.

Starting from one’s biases and working backward to causes is a poor way to do analysis.

“Magical because it relies on belief rather than on empirical evidence. We don’t need to follow the oil price shock through the data. He just says it and we should believe it. Stevie is pretending his view is received wisdom (“less than compelling”), a comical pose that he indulges in regularly; Stevie’s the High Priest of Oil.”

Well said. Remember those dogmatic monetarists who declared ONLY MONEY MATTERS. In Steve’s world, ONLY OIL MATTERS. Which means he can dismiss the role of monetary policy entirely. When I was taking courses, we called these dogmatic views junk science.

On paper, that’s right, the US should be immune to an oil shock. Of course, the elasticities of the various sectors matter, but the 2011-2013 experience suggests that high oil prices would revive ‘secular stagnation’, but not necessarily outright recession (bearing in mind that there are other material distortions in the economy).

As for Putin, let me quote myself since I published on the matter prior to the war (Feb. 12th)

Biden should have been clear upfront: The US would not abide re-writing Europe’s borders in this fashion and would meet the Russians in the field. That might have prevented Putin from investing so much of his and Russia’s prestige into this perilous venture.

Imagine, if Biden had asked for lend-lease and $33 bn in military and economic aid for Ukraine on Feb. 15th; if he had offered 100 Howitzers. Imagine if, on Feb. 15th, Defense Secretary Lloyd Austin had said Washington was “going to keep moving heaven and earth so that we can meet” Kyiv’s needs, that the US would “help Ukraine win the fight against Russia’s unjust invasion and to build up Ukraine’s defences for tomorrow’s challenges.” Imagine if Austin had said, “Ukraine clearly believes that it can win and so does everyone here.”

Imagine that German Defence Minister Christine Lambrecht gave the go-ahead to the delivery of used Gepard anti-aircraft tanks, instead of helmets, to Ukraine.

Do you think Putin might have been deterred? Do you think Putin would have invaded knowing what he knows now? I have written time and time again, mostly for ltr’s benefit, that democracies routinely sucker punch dictators by greenlighting invasions which those same democracies later resist. The Biden Doctrine (see the piece here: https://www.americanthinker.com/blog/2022/03/the_biden_doctrine_abandons_americas_common_welfare.html) unilaterally withdrew the US from the theatre even as German Chancellor Scholz flipped the middle finger to the Ukrainians with the helmet stunt. My take on Biden and Scholz was the same as Putin’s: They had written off Ukraine and greenlighted Putin’s invasion.

Now Putin is really getting pushed into a corner. Will he use tactical nukes? My view: Yes, 2:1 odds. And we need absolutely clear, merciless deterrence (yet another article) for Putin. Will we provide it, or again sucker punch Putin into trying his hands with tactical nukes? (Ltr, you will remember when I raised the issue of super powers going to war and how it sooner or later turns to nukes. You see what I mean.)

Btw, if Putin uses nukes, Xi is finished, because the Communist leadership will freak out, as that is where Xi’s policies are also driving China.

As for oil, if the Germans actually embargo Russian oil and, say, 4 mbpd disappears from the market, you bet, we’ll see a recession. Xi may not survive that, either.

So, don’t lecture me, Duckie. I was out front on Putin on paper in public.

https://www.americanthinker.com/articles/2022/02/it_is_possible_for_putin_to_get_crimea_without_force.html

“let me quote myself”. You are one arrogant moron. Look Stevie – repeating intellectual garbage does not make it wisdom.

high oil prices would revive ‘secular stagnation’

You have no clue what Secular Stagnation even means. We have asked you before to stop using terms where you have no clue what they mean. Your writing is sheer gibberish but for some reason you think it is analysis? LORD!

BTW anything published in American Thinking is good for only lining the bird cage.

” I was out front on Putin on paper in public.”

you had no additional insight that others did not have. people understood the threat of putin. but some people will need to take responsibility for actions taken. pundits do not have that responsibility. or to be clear, you were advocating putting nato boots on the ground in ukraine, at the border, daring russia to invade? steven, i am simply glad you are nowhere near being responsible for such decision making. it would probably be on par with trump outcomes.

Stevie actually thought there was some economic deal that would keep Putin happy. Of course Putin is a madman bent on killing an entire country so Stevie never had a clue. But will this arrogant idiot ever admit it? Of course not – he is too busy quoting himself.

Baffs –

I was responding specifically to Macroduck’s assertion:

“Stevie wants us to believe that Europe shouldn’t be messing with Putin because Putin has oil.”

I have never stated this, nor do I believe it. I refuted Duckie’s assertion by reference to a published document demonstrating that fact.

I do believe that Russia should be allowed to produce and sell oil and gas freely, in part due to the dependence on both Europe and the global economy on Russian oil exports (a whopping 20% of global oil and refined product exports) but that approximately 40% of such revenues should be diverted into a ‘Compensation Fund’ to defray Ukraine’s losses and expenses. This might be budgeted at $90 bn / year, or approximately 60% of Ukraine’s pre-war GDP. I currently put Ukraine’s losses, all in, somewhere in the $300 bn range. A steady flow of $90 bn / year would go a long way to restoring Ukraine’s economy and compensating the losses of its citizens.

“I do believe that Russia should be allowed to produce and sell oil and gas freely, in part due to the dependence on both Europe and the global economy on Russian oil exports”

Which was Macroduck’s point. OK you did not write the precise words he used but the message is the same. Stop being such a two faced bozo.

No, you’re incorrect.

I called for a military response to the invasion of Crimea (in the comments section on Econbrowser, no less); I called for deterrence by threat of military force, as referenced in the comments here; I called for a no-fly zone. All of these constitute “messing with Putin”, indeed, the hardline version of that.

Moreover, if you think taking half of Russia’s oil revenues does not constitute “messing with Putin”, well, I think Putin would disagree.

Ukraine must win the peace, as well as the war. Winning the peace involves securing massive funding to rebuild the country, stabilize and strengthen its economy, and pay for its defense. There are limited options to achieve this objective, among them 1) seizing Russian central banks assets, which I find problematic barring a declaration of war (and possibly even then); 2) becoming a ward of the US and EU, with no guarantee that the funding will be sufficient; or 3) bootstrapping for the next thirty years from internal resources. For me, the obvious source of funding is a part of Russian oil revenues.

“I called for a no-fly zone.”

and I remember commenting on this previously. that is a direct conflict with Russia. that will be us forces on the ground and in the line of fire. that is an escalation to ww3. now maybe that is where we end up. but it should not be part of the first action taken. that is why Biden has actually been the responsible party here. he actually understands what we would be getting into. it is not that he is afraid to do so. but it is more of a last resort rather than a preemptive action.

“I do believe that Russia should be allowed to produce and sell oil and gas freely,”

then you are willing to sacrifice more of Ukraine than Biden.

Oh, I think I’ll go ahead and lecture you. I haven’t lumped you in with Putin sympathizers. I’ve lumped you in with Putin aggrandizers. Your misguided belief that Oil is All has you thinking he is more powerful than he is. Quoting yourself (as you are so prone to do) about what Biden should do doesn’t address the issue I’ve raised.

And while I’m lecturing, here’s more. You don’t know enough about international relations to be all cock-sure about Xi’s future. The idea that you can usefully inform anyone about Putin’s threatened use of nukes is laughable. You are pretending wisdom you don’t have…again.

Posing for the Bannon channel is one thing. He doesn’t care if you prance around without a stitch on. The rest of the world doesn’t need to see you expose yourself:

https://andersen.sdu.dk/vaerk/hersholt/TheEmperorsNewClothes_e.html

Do I think Putin is all powerful? Again, let’s see what the written record says:

Friedman writes: “Putin is the most powerful, unchecked Russian leader since Stalin.” Really? This is factually untrue. Before the breakup of the Soviet Union in the early 1990s, its population exceeded 290 million. The current population of Russia is less than half that, 144 million. Russia’s area is 2 million square miles, or about one quarter smaller than was the Soviet Union’s, and its position relative to the U.S. is commensurately weaker. In 1965, the Soviet economy was estimated at near 40% that of the U.S. The Russian economy, depending on the measure used, is 7–17% of the U.S. economy today, one third of its relative strength in Soviet days.

To call Putin the most powerful Russian leader since Stalin is pure fantasy. Indeed, the entire thrust of Putin’s reasoning is to recover the power and standing of Russia during Soviet and imperial times.

Goodness, Duckie, you could read what I write before making assertions about my positions on various matters.

https://www.americanthinker.com/blog/2022/02/the_new_york_times_thomas_friedman_russian_apologist.html

Thomas Friedman is an utter moron – sort of like you. Macroduck is neither Thomas Friedman nor an utter idiot. Damn Stevie – you do remind me of a dog catching its own tail.

I don’t think Putin’s threat of nuclear weapons is laughable by any means.

I have been clear about the failure of deterrence of the current invasion by both Biden (the ‘Biden Doctrine’) and by Scholz.

To date, the US has not been clear about its response to a nuclear attack on Ukraine. I feel that Putin may still like his odds at using a tactical nuke, giving his other options and his rapidly dimming horizon.

So when Putin threatens nukes – you would back down? Thank God no one in the State Department is as much of a wuss as you are.

“To date, the US has not been clear about its response to a nuclear attack on Ukraine.”

So we should play our hand before the extremely unlikely event that Putin goes nuke. Can we play poker as I know how to bluff. And you are so dumb I would take your money in the 1st two hours.

Again – do not go to work for the State Department as you are more incompetent than Trump.

You have to follow through with deterrence. If Putin uses a nuke, the Ukrainians use a (US) nuke.

That’s the essence of deterrence: a credible promise to follow through with an action.

Steven,

I at least recognize that you are more anti-Putin than Orban. Your buyout proposal was not all that bad, just completely unrealistic.

Easy to poke at Biden and Scholze now for not offering all those weapons upfront, but even though US intel was accurately forecasting the invasion, most observers did not believe it, including the Germans and the Ukrainian leadership. The political support for such moves simply was not there until after Putin did his invasion. I think you know that.

As for Putin using tacktical nukes, the big joke is that I think they would not help him all that much. He is already using a lot of very powerful conventional bombs, and what are they getting him? Oh, maybe he could use one to finally just destroy the Azovstal plant and all the remaining Ukrainian forces inside it. But aside from that, or maybe just massively destroying some large chunk of some other city, just how useful will they be? Seriously overrated, although him using them would indeed totally destroy Russia’s international standing, including probably with China.

BTW, I just saw a rumor on part of the internet, probably false, that Putin informed Orban ahead of time of the invasion and has offered to turn part of Ukraine over to Hungary, presumably part of or all of Transcaptho-Ukraine where there are some Hungarians along with all those Rusyns.

I am not sure I would characterize my views as pro or anti anybody. I am more interested in policy than personalities.

Let me again refer to what I have actually written:

It is important to emphasize that the US interest is not anti-Russian or pro-Ukrainian, or vice versa. America’s and NATO’s interest is in stability, normalcy, and peace. The intent is not only to integrate Ukraine into Europe but also to integrate Russia as well, such that its people should enjoy a status similar to that of, say, Hungarians or Poles. Gradual, steady progress towards prosperity in both Russia and Ukraine is the western interest, just as it is the interest of the Russian and Ukrainian people.

That properly represents my long term views.

I continue to believe Orban is among the most talented of European politicians, but the man has gotten into bed with the Russians and created a kind of soft mafia state in Hungary. It’s time for him to go, and frankly, the Hungarians missed an opportunity at the elections to turn the page. I expect the EU to continue to increase the pressure on the Hungarian prime minister and his FIDESZ party.

As for Putin, his decision to enter this war was absolutely catastrophic on virtually every level. While he rules Russia, it will remain in a black hole of sanctions, much as was Saddam Hussein’s Iraq. (Iraq seems the right precedent for Russia on several fronts.) All he had to do was nothing, just let Russian middle class society find its feet for the first time in history. Instead, he chose to go all-in on a Ukraine war.

Had he won — as most westerns observers expected — it would indeed have been a brilliant, if costly, play. But again, as I wrote:

Successfully invading Ukraine, therefore, requires either speed to conclusion or passivity from NATO and, most importantly, the United States. Like it or not, Russia cannot move without US acquiescence, not unless Putin is willing to risk unmitigated disaster. Moreover, the US and NATO do not have to win for Russia to lose. NATO can bankrupt Russia out of petty cash merely by keeping the Russians in the field. In such an event, gas and oil sales will prove problematic and, of course, Russia will be unable to borrow from international capital markets.

…

For Putin, this risks the worst of all worlds: A war in the west where Russia not only fails to secure Ukraine, but that also sees earlier gains in Crimea and Donbas reversed…

I think Russia is now looking at some version of a worst case scenario.

https://www.americanthinker.com/articles/2022/02/it_is_possible_for_putin_to_get_crimea_without_force.html

“Successfully invading Ukraine, therefore, requires either speed to conclusion or passivity from NATO and, most importantly, the United States.”

Man – you are so self absorbed with your dumb writings that you have not noticed what has been happening. NATO has not be passive. But you do have the vision of Mr. Magoo. Speed to conclusion? Seriously? Russia is bogged down and far from achieving even the slightest of Putin’s goals.

Come on Stevie – no one gives a damn about what you write as what you write has zero resemblance to the real world.

So far Biden and NATO are winning this proxy war against Putin – and the risk of Chemical or Nuclear weapons has been kept low. The Biden administration has been absolutely brilliant at this. Once again, competence matters.

Putin is getting ready to declare he annexed the Donbas and his “land bridge” area (probably on Victory day). His declarations are not going to make the Ukrainians stop fighting to defend or regain that territory. We know where it has to end, but the longer the fighting before the compromise, the more Russia’s military will be degraded. For US/NATO to induce this level of harm to Russias conventional forces without destructive war on NATO territory – or an escalation to nuclear war – was not even imagined before now. Furthermore, collateral benefits included half a dozen major strategic goals that seemed decades away, if ever, before this war.

At the beginning we expressed worry about the collapse of the Ukrainian forces. Now we have to be more concerned about the collapse of Russian forces.

You have no idea what the risk of nuclear war is.

And you have no idea of anything. Anything at all.

That is a good summary. That Princeton Steve does not agree shows how utterly right you are. Stevie has a lot of bombastic views each of which are dumber than rocks.

I will stay with the oil interpretation. If I understand your reasoning, you are arguing that “only when the ECB intervened to cap yields did growth resume.” Well, the ECB certainly took its time didn’t it? The whole problem, for some mysterious reason, sprung up with the return of high oil prices in 2011. The question of debt sustainability was certainly an issue. But what caused the problem in 2011? It was not internal debt. It was external debt, ie, we’re talking about the capital account and by implication the current account. And we’re back to oil.

In any event, interest spreads subsequently declined, but they declined with falling oil prices. If it was the ECB, well, they figured they would wait for three years to cap those spreads, you know, just when oil prices fell.

A country which 1) imports all its oil; 2) is highly dependent on industries sensitive to the price of oil (including air tourism); and 3) is structurally mispriced in a currency union will be absolutely hammered in an oil shock. And they were. GDP in Greece, measured in constant local currency, was in 2021 at 76% of 2008 levels; Italy was at 94%; and Spain was at 100%. All of them should have left the currency union. The Euro has impoverished these countries. Hungary (+25%), Poland (+51%) and Slovakia (+25%) all did better. A lot better. (Slovakia, is of course, in the EZ, but it joined in 2009.)

Frankly, Germany and France are no great shakes either. Since 2008, France’s growth rate is 0.7% and Germany’s is 0.9%.

So, yes, an oil shock can lead to a debt crisis. As I have stated, the current account, and by extension, the capital account become the disciplining tools. Without devaluation, though, adjustment becomes a brutal slog, really with no end in sight at this point.

“I will stay with the oil interpretation.”

Well – that is all you know. Your comments on ECB policy are so stupid they make Stephen Moore look smart. Then again you never bothered to learn even basic macroeconomics. And it shows!

The currency union was a problem but not because of oil shocks. Try German productivity growth with really low inflation targets. Smart people like Bernanke and Krugman were noting this back in 2006. But they wrote in basic economics which we know you are incapable of understanding.

Steve – not only are your long winded comment pompous as heck but they also seriously lower the IQ of anyone who takes your stupidity seriously.

“In any event, interest spreads subsequently declined, but they declined with falling oil prices. If it was the ECB, well, they figured they would wait for three years to cap those spreads, you know, just when oil prices fell.”

Interest rates declined ONLY BECAUSE Draghi announced that he would support the financial system by any means necessary. You don’t need fancy break tests to see it in real time.

Paul de Grauwe has explained this stuff very clearly. There was a panic, sending all sovereign rates soaring. This is the nature of panics. Market participants can’t tell the good from the bad.

I don’t know what “policy circles” you are referring to when you say people in them are uncertain about the causes of the euro crisis, but they’re not people who understand it. This is a well-studied subject.

The Kremlin has been pushing this line that Zelensky is a Nazi incredibly hard to the point that Israel has had to strongly object:

https://www.msn.com/en-us/news/world/israel-blasts-russia-e2-80-99s-e2-80-98unforgivable-e2-80-99-comments-about-holocaust/ar-AAWPhkp?ocid=uxbndlbing

Israel tried hard to remain neutral but may be joining us in terms of sanctions against Russia. One has to wonder if the folks in the Putin government have truly gone insane.

There are lots of Jews in Russia, and Bennett (not my favorite politician) is no fool and knows some history. Saying the wrong thing could put people’s lives in jeopardy.

Setting aside magical structural thinking for a moment, let’s have a look at what Stevie identifies as his reason to doubt that the Greek debt crisis led to recession in Europe. His reason for doubt is that Greece represents only 2% of Eurozone GDP. Limiting one’s attention to production as a transmission mechanism for shocks is, well, it’s shocking in this day and age. It’s downright baffling when talking about a debt crisis, what with it’s being all about debt. Europe was hit with repeated financial shocks as a result of the Geek debt crisis, as anyone who paid attention at the time will recall. For instance:

https://www.reuters.com/article/us-europe-banks/europes-banks-bleed-from-greek-debt-crisis-idUSTRE81M0LT20120223

The size and quality of bank assets determine banks’…do I really need to go through this? Really? Money and Banking T-account exercises? Bank runs?

Greek GDP was the wrong thing to bring up, Stevie. It’s a clear sign you ain’t runnin’ with the big dogs. You belong on the porch.

Speaking of financial shocks, this is from the ECB’s Q1 bank survey:

“Banks tightened their approval criteria for loans to firms, as risks were perceived to have increased. Banks expect a considerably stronger net tightening in the second quarter of 2022.”

https://www.ecb.europa.eu/stats/ecb_surveys/bank_lending_survey/html/index.en.html

Not a good sign, especially since European firms rely more heavily on bank lending than on bond markets for finance, relative to what we in the U.S. do.

But in Steve’s world, money and banking do not matter. Only oil matters. So when Ben Bernanke fretted over the financial crisis back in 2007 – Stevie pooh would argue he was barking up the wrong tree. Yes only oil matters Stevie is THAT DUMB.

Thank you for making this very obvious point clear. Also, Paul de Grauwe showed that sovereign bond rates up to Drahgi’s big statement of commitment were unrelated to state finances. In other words, it was a huge panic, triggered by Greece (actually bad) state finances and spread through the euro system by the euro. Nothing to do with oil. Everything to do with bad government decisions, especially the ECB.

Paul de Grauwe is a capable economist. A link to his paper on this if you have one would be most appreciated.

Link?

Panic-driven austerity in the Eurozone and its implications

Paul De Grauwe, Yuemei Ji 21 February 2013

https://voxeu.org/article/panic-driven-austerity-eurozone-and-its-implications

Not an academic article but a VoxEU piece.

I think this was it:

De Grauwe, P and Ji Y, (2012), “Self-fulfilling crises in the Eurozone: an empirical test” Journal of International Money and Finance, vol. e-pub.

International Monetary Fund, (2012), World Economic Outlook, Chapter 3, October, Washington, DC.

But I don’t have the PDF which suggests to me my memory was from the VoxEU posts.

Many thanks!

Southern Eurozone countries have been forced to introduce severe austerity programs since 2011. Where did the forces that led these countries into austerity come from? Are these forces the result of deteriorating economic fundamentals that made austerity inevitable? Or could it be that the austerity dynamics were forced by fear and panic that erupted in the financial markets and then gripped policymakers. Furthermore, what are the implications of these severe austerity programs for the countries involved?

Financial markets leading to austerity as Dr. Chinn noted. Huh – no mention of oil after all.

One big issue is the euro. Under the gold standard, when gold club members had their exchange rates fixed to each other through pegging their currencies to gold, a country could leave the gold standard in a time of crisis (so long as the crisis wasn’t caused by them!), run some expansionary monetary policy, then re-join the gold standard when things were better, sometimes at a lower peg. It’s particularly useful when a country needs a lender of last resort (though ideas on that were not very clear through much of history). This is part of the rules of the game, and gold members in good standing (the ones who had the best monetary/fiscal policy in good times) were the ones that could most easily take advantage.

The euro doesn’t have this escape plan. So money flooded Spain over the years, then when the crisis hit, it flew back out (to Germany). Spain didn’t do anything wrong (they had good fiscal fundamentals), but couldn’t temporarily leave or halt the hot money flowing out. So they had to suffer. And because their debts were in euro, they had to pay them in euros, not a depreciated peso (which would imply a short-term haircut for lenders, but long-term both sovereign borrower and lender would be better off). So they were stuck paying these huge bills.

Arguably, Spain and others *still* could have avoided such strict austerity measures. But the thing is, giving the middle finger to your creditors, who are in the core euro countries, may risk your being in the euro area entirely.

Note that Mundell, who helped design the euro, knew this very well. The existence of this straitjacket was by design. Unfortunately, it punished bad debtors (like Greece) and good ones (like Spain) alike.

https://fred.stlouisfed.org/graph/?g=oKU3

January 15, 2018

Interest Rates on German, Italian and Euro Area Government Bonds, 2007-2022

https://fred.stlouisfed.org/graph/?g=ONsJ

January 15, 2018

Interest Rates on German, Italian, Greek and Euro Area Government Bonds, 2007-2022

Interesting graphs. Germany, Greece, and Italy all have Euro denominated financial instruments so one would expect these yields to be the same in the absence of sovereign debt risk. The fact that Greek rates were so incredibly high sort of illustrates Dr. Chinn’s point – not that Only Oil Princeton Steve will ever get this basic point.

https://www.msn.com/en-us/news/opinion/russian-generals-extremely-frustrated-as-they-fail-all-of-putin-s-strategic-objectives-cnn-military-analyst/ar-AAWQ9ba?ocid=msedgntp&cvid=a85a305b52ab471982b9b15e88c1caf9

Interesting story on how the Russian generals are frustrated with Putin’s failures. Hey fellows – here is an idea. Overthrown this incompetent war criminal and ship his sorry rear end off to the Hague. Russia will greatly benefit if you do that and end this stupid invasion.

I agree with the large group here who argue that it was the Greek financial crisis that pushed the Eu into recession. However, it should be recognized that the high oil prices at that time made those economies more vulnerable to any sort of shock, such as this financial shock that came out of Greece, and had an impact far beyond the relatively small size of the Greek economy itself.

Oil may have been a contributing factor but Stevie is arguing only oil matters. Yea it is a stupid argument but we are talking about Princeton Steve.

high oil prices may have made them more vulnerable, but it was not an very important factor. I would posit the greek financial crisis and eu recession would have occurred even if oil prices were not elevated. there were financial issues in Europe that needed to be resolved, regardless of oil. not sure if they have really solved the problem, even today, however.

Kopits is arguing that

a) “policy circles” are unsure about the nature of the crisis, and

b) oil triggered the crisis.

Neither of these claims are true. They’re actually kind of crazy.

Steven Kopitz, I admire your ability to play the ball and not the man despite constant provocation.

The below may contribute to the discussion 🙂

James Hamilton 16 June 2009 https://voxeu.org/article/did-rising-oil-prices-trigger-current-recession

Past oil price spikes associated with Middle East conflicts and OPEC embargos were each followed by a global economic recession. This column argues that the onset of the current economic downturn is also partly attributable to a sharp increase in the price of oil. Moreover, the interaction of high oil prices and housing problems contributed to the severity of the downturn.

Nice work Steven !

It is obvious oil is key in macroeconomics ! It was and still is.

A deep analysis of the 1970s macroeconomics is enlightening.

But monetary policy has had its impact, through oil production, as I tried to show in :

IS MONETARY POLICY (CARBON) NEUTRAL ?

https://theshiftproject.org/en/article/is-monetary-policy-carbon-neutral/

As for 2022, US O&G CAPEX is now moving according to the oil price signal. But US monetary policy will not be disinflationary, as it has been from 2010 to 2019, any longer …