Here are some key indicators followed by the NBER Business Cycle Dating Committee. I’ve added civilian employment to the set of indicators. Below are the trends over the recession and recovery to date, with some guesses for June consumption, May & June sales (since numbers are released on 7/29) and July employment (released on 8/5).

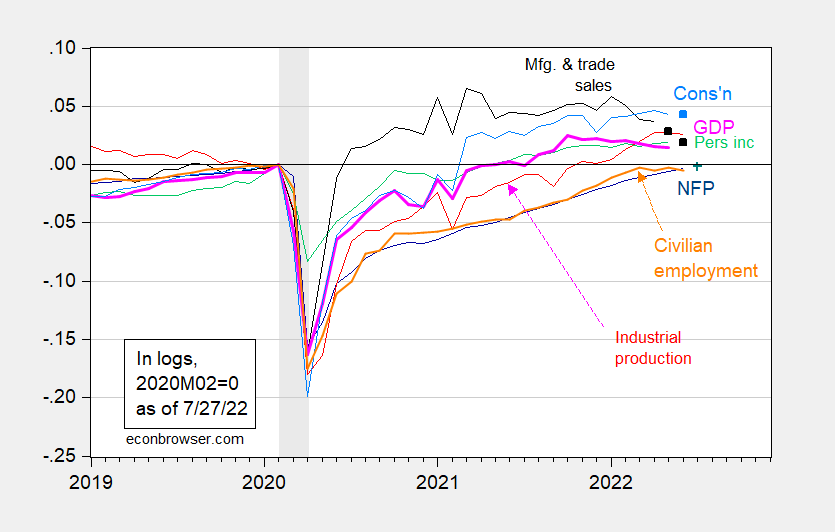

Figure 1: Nonfarm payroll employment (dark blue), Bloomberg consensus as of 7/27 (blue +) industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), projected sales based on retail sales (black squares), consumption in Ch.2012$ (light blue), projected consumption based on retail and food sales (light blue squares), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. NBER defined recession dates, peak-to-trough, shaded gray. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (7/1/2022 release), NBER, and author’s calculations.

Since we have manufacturing and trade sales only through April, and consumption through May, I have forecasted these based on a log first differences regression 2021M04 onward. For consumption, the adjusted R2 is 72%, for sales, it’s 43%.

Manufacturing and trade sales continue their decline, as might be expected as consumption shifts away from goods toward services. Consumption essentially stabilizes, growing at 0.6% annualized. Bloomberg consensus for NFP indicates +255 K, so continued recovery in the labor market.

https://www.aap.org/en/pages/2019-novel-coronavirus-covid-19-infections/children-and-covid-19-state-level-data-report/

July 21, 2022

Over 14 million children are reported to have tested positive for COVID-19 since the onset of the pandemic according to available state reports; over 311,000 of these cases have been added in the past 4 weeks. Approximately 6.1 million reported cases have been added in 2022….

https://news.cgtn.com/news/2022-07-27/Chinese-mainland-records-120-new-confirmed-COVID-19-cases-1c0a7I9z1WU/index.html

July 27, 2022

Chinese mainland records 120 new confirmed COVID-19 cases

The Chinese mainland recorded 120 confirmed COVID-19 cases on Tuesday, with 79 attributed to local transmissions and 41 from overseas, data from the National Health Commission showed on Wednesday.

A total of 583 asymptomatic cases were also recorded on Tuesday, and 7,197 asymptomatic patients remain under medical observation.

The cumulative number of confirmed cases on the Chinese mainland is 229,066, with the death toll from COVID-19 standing at 5,226.

Chinese mainland new locally transmitted cases

https://news.cgtn.com/news/2022-07-27/Chinese-mainland-records-120-new-confirmed-COVID-19-cases-1c0a7I9z1WU/img/55ee19d8703745d0b37176ad019ddb90/55ee19d8703745d0b37176ad019ddb90.jpeg

Chinese mainland new imported cases

https://news.cgtn.com/news/2022-07-27/Chinese-mainland-records-120-new-confirmed-COVID-19-cases-1c0a7I9z1WU/img/f23e57a5d31c41698168339ba3bf752e/f23e57a5d31c41698168339ba3bf752e.jpeg

Chinese mainland new asymptomatic cases

https://news.cgtn.com/news/2022-07-27/Chinese-mainland-records-120-new-confirmed-COVID-19-cases-1c0a7I9z1WU/img/41d99dd16161410dbb165873223415a9/41d99dd16161410dbb165873223415a9.jpeg

Amazing what can be accomplished when the government has the ability to restrict people to their own residences for many weeks. Fortunately, there was no impact on those people.

https://news.yahoo.com/video-shanghai-residents-screaming-windows-010552050.html

https://www.reuters.com/world/china/china-reports-598-new-covid-cases-july-17-vs-691-day-earlier-2022-07-18/

It would seem that there is some reasonable alternative to either locking up everyone or putting infected elderly back into nursing homes.

“Amazing what can be accomplished when the government has the ability to restrict people to their own residences for many weeks.”

What – you still have not left your mommy’s basement? Dude that Communist governor of yours is not about to arrest you. Then again she might beat you up just for kicks!

https://www.worldometers.info/coronavirus/

July 26, 2022

Coronavirus

United States

Cases ( 92,494,018)

Deaths ( 1,052,935)

Deaths per million ( 3,168)

China

Cases ( 229,066)

Deaths ( 5,226)

Deaths per million ( 4)

https://fred.stlouisfed.org/graph/?g=PkXW

January 15, 2018

Life Expectancy at Birth for United States, Canada, France, Germany, Italy, Japan and United Kingdom, 2000-2020

https://fred.stlouisfed.org/graph/?g=MnBT

January 30, 2018

Infant Mortality Rate for United States, Canada, France, Germany, Italy, Japan and United Kingdom, 2000-2020

Manchin and Schumer reach another “deal”?

https://www.msn.com/en-us/news/politics/manchin-and-schumer-announce-a-deal-that-includes-energy-taxes/ar-AA102rpN

Joe Manchin and Senate Majority Leader Chuck Schumer on Wednesday reached a deal on a bill that includes energy and tax policy, a turnaround after the two deadlocked earlier this month in talks on Democrats’ marquee party-line agenda. In a joint statement, the two Democrats said the legislation will be on the Senate floor next week. It includes roughly $370 billion in energy and climate spending, $300 billion in deficit reduction, three years of subsidies for Affordable Care Act premiums, prescription drug reform and significant tax changes. The duo said their bill, dubbed “The Inflation Reduction Act of 2022,” would “fight inflation, invest in domestic energy production and manufacturing, and reduce carbon emissions by roughly 40 percent by 2030.” Moreover, as part of the agreement announced Wednesday, Schumer and Speaker Nancy Pelosi agreed to pass legislation governing energy permits.

This would be great except Manchin has this habit of pulling the plug on alleged deals. I’ll start cheering when the bill passes both House and ends up on Biden’s desk for his signature.

Couple of Fed things:

After today’s FOMC policy announcement, priced in odds favor a 50 basis point rate hike in September (65%), rather than 75 bps (35%). Yesterday, odds were 51%/41%, with 8% for a full 1% hike. The 10y/3m yield spread widened by 16 basis points to 35 bps as a result.

The other thing is that China has been trying to spy on the Fed:

https://www.axios.com/2022/07/26/china-attempt-infiltrate-federal-reserve

Oddly, naturally, Axios reports this violation of U.S. law as mostly a struggle between the Fed and the FBI, while mostly ignoring China’s multiple criminal acts.

“ China has been trying to spy on the Fed.” How unconscionable!!! We would NEVER do something so dastardly to China…and if we did macroduck would be the last to notice or complain about it…

The usual double standards…

There are no double standards. Everybody spies. Just think it of that

Ehxactly…everybody does it, but only some get called out for it…and those are countries on the US’ blacklist du jour.

Not fair! Not fair! JohnH cries.

Unless everyone is punished, no one should be.

Twelve year olds cheer him.

Poor neglected Johnny. Did your parents not give you enough attention? Johnny, these outbursts won’t fill up that empty place.

Maybe he can sign up for Hulu on the hopes that they carry Spy v. Spy. After all – Hulu is not carrying those progressive ads that would just set Johnny off.

https://english.news.cn/20220727/9792f4364eb542459989188b9b59b673/c.html

July 27, 2022

China capable of achieving carbon peaking despite challenges: energy regulator

BEIJING — China is capable and confident of achieving the goal of carbon peaking before 2030, the country’s energy regulator said Wednesday.

Despite global energy strains and the reopening of coal-fired power plants in several European countries, China’s development of non-fossil energy has continued unabated, said Zhang Jianhua, head of the National Energy Administration.

Last year, the share of non-fossil energy in China’s total energy consumption expanded from 15.9 percent to 16.6 percent, Zhang said, adding the figure is expected to grow at an average rate of one percentage point a year from now to 2030.

Official data showed that installed capacity of renewables in the country increased by about 130 million kilowatts last year.

As part of efforts to expedite a low-carbon transition of the energy sector, China is ramping up efforts to promote the clean and efficient use of coal and improve clean energy heating, according to Zhang.

The official also highlighted the progress China achieved in constructing charging facilities for new energy vehicles, saying that it has put in place the world’s largest network of charging facilities, with a total of 3.92 million charging piles built as of June this year.

By 2025, China will be able to meet the charging demand of over 20 million electric vehicles, Zhang said.

Princeton Steve says he is a fan of Hungary’s Victor Orban. I bet this is why:

https://www.thetimes.co.uk/article/b5efcfaa-0d93-11ed-a4af-79eb4b98fc31?shareToken=8c6ec6027111f533c38dfd7583a08c5d

Viktor Orban, Hungary’s populist and anti-immigrant leader, has been accused by one of his longest-serving advisers of making a “pure Nazi speech” worthy of Adolf Hitler’s propaganda chief. Zsusza Hegedus, who is Jewish, accused Orban of going beyond anti-Islamic rhetoric into open racism. “The speech you delivered is a purely Nazi diatribe worthy of Joseph Goebbels,” she wrote in a resignation letter after advising Orban on social inclusion policy for 20 years. Hegedus, whose letter noted that she was born a year after the end of the Holocaust, wrote that she was breaking with her past defence of Orban as not being either “racist or far-right”.

“The prime minister is promoting an openly racist policy that is now unacceptable even for the far-right in western Europe,” she said, warning that “too many were silent when the kind of hatred that the Nazis built on was being born”.

CPAC must be a fan of Orban because they have invited him to speech before their meetings in Dallas.

pgl,

Oh, I may be wrong and even if I am right will probably annoy a bunch of people here. But, it is my impression that Steven has never been a big fan of Orban’s. He has described him as a smart politician and he has also noted that there is an opposition party in Hungary, Jobbik, that is further to the right and even more fascistic than Orban, hard as that may be to believe. I note that one can do business with a government, even if one does not agree with it.

I do not know if Steven will clarify this or not, but this is my impression of his position: that he is not a supporter of Orban, despite praising his political skills.

https://www.bea.gov/sites/default/files/2022-07/gdp2q22_adv.pdf

Real gross domestic product (GDP) decreased at an annual rate of 0.9 percent in the second quarter of 2022 (table 1), according to the “advance” estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 1.6 percent.

Before those disgusting RECESSION cheerleaders start doing high fives, a couple of more notes:

The GDP estimate released today is based on source data that are incomplete or subject to further revision by the source agency (refer to “Source Data for the Advance Estimate” on page 3). The “second” estimate for the second quarter, based on more complete data, will be released on August 25, 2022.

I’m sure our host will have some sensible things for these cheerleaders to consider but let’s also note:

The decrease in private inventory investment was led by a decrease in retail trade (mainly general merchandise stores as well as motor vehicle dealers). The decrease in residential fixed investment was led by a decrease in “other” structures (specifically brokers’ commissions). The decrease in federal government spending reflected a decrease in nondefense spending that was partly offset by an increase in defense spending. The decrease in nondefense spending reflected the sale of crude oil from the Strategic Petroleum Reserve, which results in a corresponding decrease in consumption expenditures. Because the oil sold by the government enters private inventories, there is no direct net effect on GDP. The decrease in state and local government spending was led by a decrease in investment in structures.

The decrease in nonresidential fixed investment reflected decreases in structures and equipment that were mostly offset by an increase in intellectual property products.

The decline in measured real GDP did not come from lower real consumption as the disgusting cheerleaders had predicted. No it came the same kind of fiscal restraint and tight money these same disgusting cheerleaders claim was good policy. Now I would argue we need more government investment and we should tell the FED to lighten up.

I am curious if anyone knows the magnitude of the Strategic Petroleum Reserve effect.

Funny thing is that the Biden partisans here, in trying to disprove the idea that we might be in a recession, are only highlighting “recession” in people’s mind.

George Lakoff demonstrated this phenomenon by saying to people, “Don’t think of an elephant.” And what did people think of? An elephant!!!

So good job, pgl. You and your Democratic handlers sure know how to convince people that we’re not in a recession!

Now if only we could find some economists to give an honest assessment like The NY Times: “ the data released on Thursday left little doubt that the recovery is losing momentum amid high inflation and rising interest rates.…” and a recession may not be that far off.

I just listened to Dr. Yellen speak. Clear, honest, and well informed. The antithesis of your rants.

it was a good sleep aid…sure to become a YouTube hit.

Perhaps the smartest economist on the planet and Johnny boy tosses out a sexist insult. You are a very disgusting little boy.

Johnny, Johnny, Johnny,

What an odd sentence: If only economists believed what most economists believe? This manufactured outrage thing you do – you really need to do better. You keep expressing outrage over a little fantasy world rather than the real one.

Of course the economy is slowing. Growth of 6% was unsustainable, the product of a ton of unused potential and policy aimed at getting that unused potential back into production. It worked. Anybody with eyes and a brain understands’ this. CoVid and war have combined to generate inflation and central banks are raising rates to try to fight that inflation. All you have to do is read the news (or this blog) to know that.

What on earth makes you think economists think otherwise? Calm down, Johnny.

Instead of emphasizing the obvious…that the economy is on the brink of recession or not all that far from going into recession, an amazing amount of time and energy has been spent here showing that the economy is not in recession, at least not technically if not in the commonly understood shorthand version of two quarters of negative GDP. If not in support of Biden administration spin, does such hair splitting really serve any constructive function? To me it sure looks to be a diversion, encouraging people to not believe their lying eyes.

Ironically, the more you use the word recession to disprove that we’re in one, the more people think about being in a recession!

Johnny, Johnny, Johnny,

You claimed economists aren’t aware f a slowing coming, inflation and rising rates. I pointed out what nonsense that is. No, you want to change the subject. Net like when you claimed western economists know nothing about Russia’s economy when they sad it like suffer under sanctions, and when it turns out Russia’s economy is in the toil, you are nowhere to be found.

This bit about saying recession being a “win” for recession cheerleaders? You think recession is like Beetlejuice? You’ve made clear that you think is important; you think talk matters more than reality. That’s what propagandists and lunch-room debating heros think, so I’m not surprised. Go have your debate with the other teenagers. Enjoy.

pgl,

I saw that personal income and disposable income are up by amounts only slightly less than Q1. I am not sure iif the first of these is the same as GDI, but if it is, then it looks that GDI grew more than GDP declined, same as Q1. That means gross domestic output, their average, rose both quarters, but I have seen no reporting of that.

Weirdest thing in the numbers is the decline in inventories. I do not know how this reconciles with all the news reports of increased inventories and how all kinds of sectors are trying to unload them. I continue to be struck by how unreliable and unpredicatable various parts of our current data are. This is just plain weird.

Anyway, even though I warned we might get a surprise with it going the other way, I said probably GDI would look a lot better than GDP again, and it looks that this is the case, although I am not sure.

pce read tomorrow at 0830 same site as the initial gdp read….

it shows 5 months so we can see what went in and out.

much of it is nominal, but a couple of lines are chained to 2012 (iirc).

gasoline, food and rents hurt retail sales which met unwinding supply chain backlogs.

and the stimmy wound down as well.

good thing the pentagon signed off on more dd250’s than usual.

Well, I got the GDP thing wrong it looks like. I don’t think even the revised numbers will put it where I would end up being correct (and that would have been grabbing for straws anyway on my part). I guess that’s what I get for betting against IHS Markit, which is pretty much the fastest gun in the wild west right now. My one rationalization for being wrong is I get to stand alongside Jeffrey Frankel in being wrong about 2ndQ GDP. So hey, if I get to be in Jeffrey Frankel’s group while being wrong, that ain’t bad. [ Professor Frankel is reading this going “What the hell is it with this middle-aged punk throwing me under the bus!?!?!” ]

Moses Herzog: Jeff Frankel didn’t write that Q2 GDP would be positive. He just wrote that — as I and others have noted — a 2nd quarter negative reading would not be definitive for constituting recession.

Exactly right. But i fully expect (alas) a lot of hype from our RECESSION cheerleaders. Then again – we get another BEA release in about 4 weeks.

Here’s what Frankel wrote:

“The chain of reasoning is probably wrong, however, as is likely to become clear in the future. There are three flaws. First, growth is as likely to turn out positive in the second quarter as negative. Second, even if the number indeed comes out negative July 28, a US recession is not defined as two consecutive quarters of negative growth…”

Clearly, he was well wide of the mark asserting that “growth is as likely to turn out positive in the second quarter as negative”.

Steven Kopits: Are you a Bayesian?

It was clearly not as likely to turn out positive as negative. IHS was at -2%, AF was at -1.6%. The Fed News Index is all over the place, and clearly, Goldman Sachs doesn’t have as articulated a forecasting model. And of course, the result was -0.9%, clearly not a close call. Indeed, I had called the under weeks before Frankel published, and clearly I got it right, at least wrt to the sign.

Steven Kopits: Bloomberg consensus was +0.4% SAAR on the eve of the release.

Menzie ChinnPost author

July 28, 2022 at 11:22 am

Steven Kopits: Bloomberg consensus was +0.4% SAAR on the eve of the release.

When do we know what happened to GDI? Or GDPPlus? Given the role of inventories (per Dean Baker and Dr. Yellen) maybe Bloomberg’s consensus was “technically” correct. OK I just tortured technically but not as badly as any statistic will do Princeton Steve.

Sine inventory – real GDP rose. So Frankel was spot on. Speaking of spots – pull down your cheerleader skirt as they are ugly spots on your panties.

Steven,

So, congratulations on accurately callling a negative Q@ GDP move. I note that personal income rose by more than GDP declined, which may or may not amount to a similar move for GDI. I note that I called you out to make a forecast of GDI, but you simply ignored it. I called that GDI would do better than GDP, and it looks to be the case.

If indeed GDI moves as personal income does, then we shall have a repeat of Q1 where GDI grew more than GDP declined, meaning that the gross domestic output measure rose again as it did in Q1. not much of a recession, especially given how hot the job market remains.

The odd thing in the report I do not understand is the decline again in inventories. I did say that they would be driving the outcome. I noted that it looked like they might increase, given all the news stories about excessive inventories having appeared. But, instead, they are reported to have declined, which certainly is consistent with GDP declining, but not necessarily income. I have no explanation of why the data and the news stories are so out of synch, and I await somebody coming up with any kind of explanation that makes any sense.

Barkley –

I suspect the inventories and net exports categories, which are the big movers since Q3 last year, were driven by the stimulus. So the non-recession recession of H1 2022 looks primarily about the run-off of the stimulus. Hence, no major unemployment (yet) and why solid analysts like Bill McBride were not even on recession watch when the US experienced a technical recession. They are focusing on business cycle stuff, rather than a historically unusual end of an over-sized stimulus.

I think we need to put H1 behind us and now start looking at H2, which probably (has the stimulus effect entirely processed through the system?) has more typical business cycle dynamics. We still have IUCs indicating a recessionary turn from March 19th, but that is only one data point to consider.

Steven,

I am going to go out on a limb and be at least a third of S Real Man. I am going to predict that Q3 will also see a decline of GDP for the US. I am not going to make a forecast about other major macro variables that the NBER committee looks at, such as employment or income. I do not know what they will do for the quarter, although it appears that at least employment has continued to grow through at least July.

Why am I making this forecast for official GDP? It is indeed our inventories matter. They have continued to rise, although at a decelerating rate that has been a major reason for the negative GDP movements in the last two quarters. But, as I have noted several times, there are lots of news reports that inventories have now become excessive in many parts of the economy, so it looks like there will be a serious effort to unload them. Moving from rising inventories as we have had for the last two qaurters to outright declining inventories, possibly by a large amount, will involve a much larger negative change in the change in inventories than we saw for the first two quarters.

So, even if consjumption continues to grow and net exports hold up, and maybe even local government grows rather than declines, there will probably be a much more substantial negative change in the change of inventories for Q3 that will overwhelm pretty much everything else and give us another quarter of negative GDP growth, even if enough other variables hold up so that when the NBER committee finally decides on all this they may still decide that Q3 is not a recession.

4th paragraph down:

Some economists, including me, would guess that growth was more likely positive in the second quarter than negative.”

https://econbrowser.com/archives/2022/07/guest-contribution-the-us-q2-gdp-announcement-will-not-mean-recession

You can say a “guess” is not a “prediction”, but that sentence to me is indicating pretty well were someone is “casting their lots”. I’m not exactly implicating the man. I made the bad prediction.

As, yes, and this per Moses.

Moses even in his most crazed comments is 1000 times more honest and informative than the most incompetent consultant ever.

” I had called the under weeks before Frankel published, and clearly I got it right, at least wrt to the sign.”

Tell you what. Write a letter to JASA about this and see if they give you forecaster of the year. The editor needs a laugh and I bet you letter will have him laughing for weeks.

You now enjoy agreeing with me just because you’ve figured out it annoys the hell out of me, don’t you?? Professor Frankel clearly stated it was a guess. So, I don’t think he was really wrong. I don’t think you hold someone’s feet to the fire when they clearly state it was an educated guess. As is one of my character weaknesses, I was trying to make myself feel better by dragging in Professor Frankel on my 1%+ off prediction. It’s not very fair since Professor Frankel was not making a definitive statement.

Well, apparently I am a good bit more competent than Frankel, 46 of 47 macro economists polled, or Goldman Sachs, at least as far as Q2 was concerned.

But you’re right, Moses either has a better memory or better research skills on this one.

It’s the quality of the comments, Moses, not the person. If you can’t distinguish the substance from the source, then you’re pretty much doomed, a la pgl.

I personally prefer civilized dialogue, because without it, it’s all about intimidation and reducing the information flow. You end up like Putin, where those with differing views flee or are banished. What’s left is a sterile echo chamber. That’s pgl’s world, and unfortunately, one which Menzie implicitly endorses.

Steven Kopits: Civilized dialogue is one where you, without evidence, accuse me of being intimidated by the Chinese government (and backhandedly suggest I might not be a China apologist)? Civilized dialogue is you using the inflammatory term “China virus”? And wondering who wrote “What the hell do you teach your students, Menzie?” Civilized apparently is if you say something insulting and inflammatory, but not if somebody else who characterizes your remarks (mostly correctly) as idiotic.

Steven Kopits

July 28, 2022 at 11:52 am

Well, apparently I am a good bit more competent than Frankel

Seriously? An incompetent boob v. someone who has served as an economic advisor to Presidents. OK then I’m the tallest person ever to play basketball.

@ BlueStateKopits

But see, I think this may be part of your problem, because “the source” as you call it, is often a major major contributor in identifying the quality or as you refer to it, “the substance” of the data. I can give you a terrific example of this. Here is a very poor choice of source, and the garbage which results from quoting such sources:

“At the year horizon, excess deaths seem likely to settle in the 200-400 range.”

https://www.princetonpolicy.com/ppa-blog/2018/5/30/reports-of-death-in-puerto-rico-are-wildly-exaggerated

And here, although maybe not a “perfect source”, but a much better example of sourcing of quality data, and the better, more substantive, more empirical data one can get from better quality sourcing of data or information:

“Total excess mortality post-hurricane using the migration displacement scenario is estimated to be 2,975 (95% CI: 2,658-3,290) for the total study period of September 2017 through February 2018.”

https://publichealth.gwu.edu/sites/default/files/downloads/projects/PRstudy/Acertainment%20of%20the%20Estimated%20Excess%20Mortality%20from%20Hurricane%20Maria%20in%20Puerto%20Rico.pdf

Sourcing is often the first step in getting good data. For if a person only chooses based on “substance” they may already be “locked into” their own demented, highly misguided, and preconceived notions of what “substance” is. i.e. hunting down the sources which give them the answers they desire, rather than reality, or often, as is in your case, letting the tail wag the dog.

BlueStateKopits, You’re the type person/”source” who falsely claims that multiple vertebrae in his back are broken, and goes searching through 15 different doctors looking for someone to agree your perfectly healthy spine has multiple broken vertebrae, and that 15th/last doctor, Dr. Will Lye Forcash tells you your spine is irreparable, and you go around telling everyone you meet that Dr. Will Lye Forcash is the only good doctor left in existence.

Do you permit students to abuse each other in your classes as pgl does many commenters here? Are those your values? Do you permit that in your home? Would you permit pgl to use his ad hominem attacks on your wife as he does on commenters? If not, why do you condone it here? Is that your values, because you surely condone his abusive behavior.

If you want to end it, that’s simple. Force him to use his real name. I have little doubt that if you did so, he would be shown to have a long history of abusive behavior towards his coworkers, women, children and others. There’s no such thing as a guy who is abusive in this context only. His is abusive generally in his life and you are his enabler. That’s the way it is.

Steven Kopits: Er, you’ve not answered my question. This is a blog. If you’d said the things you’ve said on this blog, about a fellow student (not about me, I’m the instructor) in my class, you’d be out. If you want me to apply this standard to you, I would be happy to oblige.

Moses, I am agreeing with you because I thought you were right. If you side with someone purely because they are on your team, or against them if they are not on your team, then dialogue is nothing but a cover for pre-determined outcomes. It is then all about whether your side wins or loses, and there are no commons as such. There is no justice in that system, only patronage. It is all about warfare, which makes you understand why so many in red states are expecting civil war and want secession. You may want to live in a world like that — there are many countries around the world where politics is reduced to this sort of zero sum game — but I don’t. In fact, neither do you.

Menzie –

Do you have any idea how bad a war between the US and China over Taiwan could be? It is really end of the Roman Empire start of the Dark Ages stuff. China is a hegemon scale country. If it attacks other countries, then the world will fear China, not for the duration of the war, but for the next hundred years. Security policy all over the world will be about keeping China down, because a rising China is a mortal threat to everyone, and that will have incredible and lasting implications for the world economy and society in general. And that’s assuming no nukes!

China desperately — desperately — needs democracy, and it needs it now. That is an order of magnitude bigger issue than everything else you’re writing about combined. I have had to prod you over and over to even write modestly about democracy in China and the need for leadership (and increasingly regime) change there. Do you think Xi needs to go? I do. If you think so, then why don’t you write a post entitled: “Xi needs to go.” That would certainly demonstrate that you’re not intimidated.

Steven Kopits: I suspect I’ve read more documents pertaining to the military balance in Asia Pacific than you have (probably have a better reading of WW II, Korean and Vietnam wars than you do, given my off-economics interests). So, I have an idea of the stakes. By the way, are you aware of the number of long range nuclear weapons China is estimated (who know exactly how many) to have, relative to the US? Then compare against how many the Russians (are estimated to) have.

So, I take it you continue to believe I’m intimidated by Xi and the CCP? What is this – if one is an ethnic Chinese person (born in the USA, unlike you), one has to write a post demonstrating that one is not in the thrall of the CCP? It certainly sounds like a loyalty test. Strangely, you haven’t asked me to write a “Putin has to go” post.

PLA’s post ‘Preparing for war’ draws wide support from netizens ahead of Army Day

https://www.globaltimes.cn/page/202207/1271742.shtml

Well, Menzie, you clearly do not feel that Xi has to go. And moreover, you are taking that Barkleyesque view that, well, China would never go to war over Taiwan. Or do you feel differently? Is Xi okay? Are you happy with him? What’s your view, Dr. Courage?

If you think Xi is fine and China will not go to war, maybe you have better make that case explicitly, because war certainly looks in the cards to me.

The best “take” I have ever seen on this, and I think it was YT video, and I think I may have attempted to put it up in this blog in a comment, but because of the strong content of the YT video, Menzie kind of decided it was in poor taste to put it up on the blog. But it was an Asian gentleman (I want to say he was Japanese, but am mildly ashamed to say I can’t remember now) who worked on a city council of some medium sized suburban town. And there was some kind of racism involved. And this Japanese gentleman (and I mean that, he was a very civilized refined gentleman, but he had finally reached his limits the straw on the camel’s back. He slowly unbuttoned his shirt as he talked about his service during one of the wars (I assumed it was probably the Korean or Vietnam war). and when he had finally taken his white long-sleeve dress shirt off, it exposed some grotesque scars all around his torso, front and back. It was obvious torture he had received as an American soldier in one of the wars. and he was not “yelling” per se, but in a loud voice looked around the city council room slowly and said something like “How about it!?!?!?! Is this ENOUGH!!??!?!!? IS this enough to prove my allegiance!?!??! Is this ENOUGH to prove my Americanism!?!?!?!”

I am sure many of his colleagues and the towns people thought this gentleman had gone “too far”. I didn’t, I found it very emotionally moving and to this day I wish I could buy that man 2–3 beers or whatever the hell he wanted at the bar. And I would listen to whatever he wanted to say while we drank, or maybe if he liked, we could drink in silence. It really wouldn’t matter to me just so long as I could buy him some drinks.

Steven,

Now you are coming on like Moses Herzog, attributing things to me I never said.

You claim that it is a “Barkleyesque view” that China will never invade Taiwan. I do not believe I have ever expressed an opinion one way or the other on the matter, and in fact I worry they might and have for a long time. Really, you are off on this, pretty badly, Steven.

As for demanding that Menzie or anybody else declare that “Xi must go” or any other nasty world leader for that matter, how silly can you get? Look, lots of us would prefer China were a democracy, and that somebody other than Xi was in charge there. But us calling for this, either once in a long while or every other time we post, is not going to bring it about, any more than posting “Putin must go” will get him out of office, or for that matter, “Orban must go.”

As it is, frankly, it is not obvious to me that introducing democracy into China will necessarily reduce the threat to Taiwan all that much. Nationalism has become deeply entrenched in China, and the narrative that Taiwan belongs to China and an invasion to take it would be justified I think is widely believed and accepted in the population. A democratically elected government might feel even more strongly that they must invade Taiwan to take it. Have you considered that possibility?

As it is, I am surprised that Moses is not stepping forth to denounce Pelosi for her likely trip to Taiwan. I have very mixed feelings about this, but it is clear the Biden admin would prefer she not do it, with the Chinese clearly quite worked up about it. Really, with the war in Ukraine going full blast, having China invade Taiwan, or otherwise cause it a lot of trouble is about the last thing we need right now. This is clearly much more dangerous than her eating fancy ice cream, and is clearly appealing to her very local constituency, possibly very irresponsibly, although I strongly support the autonomy of Taiwan and am for showing them some support. But this trip at this time may not be the best way to do it.

Bur, a serious bottom line here is that I think some of your comments to Menzie, a Chinese American, have really been seriously out of line.

“GDP declined at a 0.9 percent annual rate in the second quarter, as a slower pace of inventory accumulation subtracted 2.01 percentage points from the quarter’s growth.” Dean Baker. Also what Dr. Yellen noted.

OK – Stevie still does not get this even after Macroduck patiently explained it to him.

Moses,

You should not have played this third rate macho game of making precise forecasts, but I at least know that you are really into that sort of thing, probably even more so than Steven.

But I’m so exceptionally good at third rate macho.

It seems George Washington University has decided Clarence Thomas is not fit to teach Constitutional Law:

https://www.gwhatchet.com/2022/07/27/supreme-court-justice-wont-teach-gw-law-seminar/

Supreme Court Justice Clarence Thomas will not teach a Constitutional Law Seminar this fall, according to an email addressed to students in the seminar that was obtained by The Hatchet. Gregory Maggs, who has co-taught the course with Thomas since 2011, stated in an email addressed to the class that Thomas is “unavailable” to co-teach the course in the fall, and Thomas is no longer listed as a lecturer on GW Law’s course list. Thomas’ withdrawal from the course comes a month after more than 11,000 community members signed a petition demanding his removal from GW, but officials declined to remove him from his role after he voted to overturn Roe v. Wade.

Passing along this email from the great Dean Baker:

Recession-fearing households increased spending on hotels and restaurants at a 13.5 percent annual rate in Q2.

GDP declined at a 0.9 percent annual rate in the second quarter, as a slower pace of inventory accumulation subtracted 2.01 percentage points from the quarter’s growth. A 14.0 percent rate of decline in residential construction subtracted 0.71 percentage points from GDP growth. Final sales of domestic products to domestic purchasers fell at a 0.3 percent rate, after rising at a 2.0 percent rate in the first quarter.

Even with Slower Growth, Inventories Still Accumulated at a Healthy Pace

Inventories still rose at a $81.6 billion annual rate, somewhat faster than pre-pandemic normal. This was nonetheless a drag on growth, since they grew at a $188.5 billion rate in the first quarter. This healthy rate of accumulation is a positive going forward, since it means stores are, for the most part, well-stocked after the pandemic supply chain problems. This will put downward pressure on prices.

Farm inventories are an exception. They fell at a $44.6 billion annual rate, continuing a downward trend that has been in place since the third quarter of 2015.

Consumption Grew at a Modest 1.0 Percent Rate, as the Switch Back to Services Continues

Consumption of services rose at a 4.1 percent annual rate in the second quarter, while consumption of goods fell at a 4.4 percent rate. Goods consumption as a share of nominal spending is still 3.6 percent higher than its pre-pandemic share, with service spending down by the same amount. The goods share in real terms is 3.2 percentage points higher, with services down by 2.4 percentage points (real shares won’t sum to 100 percent).

Spending on a wide range of goods is still considerably higher than its pre-pandemic level. The biggest drop in nominal shares on the service side are in health care services, down 1.4 percentage points, recreational services down 0.6 percentage points, housing down 0.5 percentage points, and transportation services (much of this is commuting) down 0.4 percentage points.

The Saving Rate is Holding Up

The inflation hawks have been raising the alarm that people are spending down pandemic savings, leading to an overheated economy. They cite the reported saving rate, which was 5.2 percent in the second quarter, down from an average 7.5 percent in the three years preceding the pandemic.

This is misleading. Saving was lower in the last two quarters because tax payments have risen. Since there was not an increase in tax rates in 2022, this is presumably because people are paying capital gains taxes on recent stock sales.

The sum of savings plus taxes as a share of personal income was 18.9 percent in the second quarter. This is higher than the 18.5 percent figure in 2018 and the 18.7 percent share in 2019.

In short, there is no story of excessive levels of consumption overheating the economy. On the other side, hotel and restaurant spending rose at a 13.5 percent annual rate in the second quarter. This is not consistent with the widely expressed recession fears reported by the media.

Inflation Slows Sharply in Quarter

Inflation, as measured by the core Personal Consumption Expenditures (PCE) deflator (the Fed’s main inflation gauge), fell to a 4.4 percent annual rate in the second quarter from a 5.2 percent rate in the first quarter. This is still considerably higher than the Fed’s target of a 2.0 percent average rate, but it should help to alleviate concerns of a 1970s-type wage-price spiral. While it is just a single quarter’s data — and these numbers have been especially erratic in the pandemic — the pace of inflation looks to be slowing rather than increasing.

Investment Remains Healthy

Nonresidential investment fell at a 0.1 percent annual rate in the quarter, driven mostly by an 11.7 percent rate of decline in structure investment. Structure investment has been falling sharply throughout the pandemic and recovery as there is less need for office space and traditional retail space. It was 24.7 percent below its pre-pandemic level in the second quarter.

Investment in intellectual products remains solid, rising at 9.2 percent rate in the quarter, putting it 20.0 percent above its level in the fourth quarter of 2019. Equipment investment fell at a 2.7 percent rate, but is still 9.0 percent higher than in the fourth quarter of 2019

Dean says inventories rose, and that they rose in Q1. However, when I look at some data sources, I see just the opposite. I admit that I am completely mystified and confused as to what the heck is going on with inventories.

Barkley Rosser: Inventory investment is the *change* in the stock of inventories, so the change (which is the contribution to GDP growth) in the change was negative.

@ Professor Chinn

This is the same number over on FRED??

https://fred.stlouisfed.org/series/CBI

I guess I need to read the BEA lesson notes closer (no joke) because it’s easy for me to get confused looking at the BEA tables. For example I’m stupid enough to think if I type in “CIPI” or inventory investments in a BEA website search it will give me the number to find it in the actual BEA tables, but of course it does not:

use this: https://www.bea.gov/sites/default/files/2022-07/gdp2q22_adv.pdf

and this: https://www.bea.gov/sites/default/files/2022-07/GDPKeySource_2q22_adv.xlsx

inventories are always the last line item (items) under the investment category. no searching necessary.

@ rjs

Much appreciated and very grateful. May God bless you and your family. Your dog. Whoever your “crew” is, seriously.

Got it, Menzie, finally. Equilibirum would be zero changes in inventories. But, yeah, it looks that we have a decline in GDP because we have a decline in the rate of growth of inventories. Really not surprising then that it looks we have a major disjuncture between GDP and GDI probably.

Menzie,

Now that I am looking at it again, I am newly confused. Is it the change in inventories or the change in the change of inventories? I had always thought it was the change in inventories, and I remind that in equilibrium that number is zero. But what I am seeing here is that inventories rose. The change in inventories was positive. If indeed it is the change in inventories that counts, that should have been a positive number, pushing GDP up.

But now I have all sorts of people saying that it is the second derivative that counts, the change in the change of inventories. So, inventories continued to rise, but the rate of increase of inventories slowed, so, wow, GDP declines! Looking at this does not make sense.

I have to say that this is the first time I have ever seen it claimed that what goes into the measure of GDP is the second derivative of inventories, the change in the change of them.

Barkley: real private inventories grew at an inflation adjusted $81.6 billion rate in the 2nd quarter, after growing at an inflation adjusted $188.5 billion in the first quarter, and as a result the $106.9 billion reduction in real inventory growth subtracted 2.01 percentage points from the 2nd quarter’s growth rate, after an inflation adjusted $4.7 billion decrease in inventory growth in the 1st quarter had subtracted 0.35 percentage points from that quarter’s GDP growth rate..

that also means we have to beat $81.6 billion in inventory growth in the 3rd quarter for it to be a positive for GDP…

the problem began in the 4th quarter, when inventories added 590 basis points to GDP….we’re just giving some of that back…

@ rjs

I found where they list this on “tradingeconomics”, so I guess I can find it again in future, but can you tell me where these numbers are in the BEA tables?? The number they have on the far left part of the BEA tables to cross reference??

Moses; table 3, line 40 here: https://www.bea.gov/sites/default/files/2022-07/gdp2q22_adv.pdf

the percentage point effect on GDP is table 2, also line 40

where, btw, i see i have to correct my above statement to “inventories added 532 basis points to 4th quarter GDP”

i should know better to rely on my memory for a revised figure like that

470 bps then?? for the 4th Q?? Yeah, again I appreciate it. This has actually been quite educational for me, because I knew very well inventories effected the GDP number a lot in certain contexts, like now. But I think it didn’t quite register in my brain how it’s not exactly a “face value” number, and there’s a certain kind of “boomerang effect” from recent prior quarters’ inventory numbers. I was trying to think of a metaphor for it?? Kind of like small waves of water in a bathtub or pool. If the numbers were “extreme” or “unusual” they can effect the next batch of quarterly inventory numbers or effects on GDP. It could be a pretty “big hint” on the final GDP number.

GDP is a waste. It’s impossible to know based on a couple months of research what real GDP was. A piece of poor data can mislead. Don’t forget the 2007 GDP estimate disaster. They were way off with over and then underestimation. We, for

My view is they are underestimating exports/inventory. Overestimating inflation. Revised out it will be.

Let’s benchmark these wise words for when Princeton Steve starts more of his absurd bloviating.

June construction, June trade in services, and non-durables inventory data have yet to be reported, and that the BEA assumed a $5.7 billion increase in exports of services, a $4.2 billion increase in imports of services, a $10.1 billion decrease in residential construction, a $1.3 billion decrease in non-residential construction, a $1.2 billion increase in public construction, and a $1.2 billion increase in nondurable manufacturing inventories for June before they estimated 2nd quarter output (see the Key source data and assumptions excel file that accompanies this report for more specific details)..

my sense is that their estimates for June, at least for construction, are based on the trends of April and May…since June data has been surprising to the downside, my guess is that those figures will be revised downward….we’ll have the hard data on construction on Monday, so we’ll know for sure soon…

I’m listening to Janet Yellen who really gets it and knows how to explain the data and the issues. An incredible breath of fresh air for anyone who has had to endure the bombastic stupid bloviating from Princeton Steve. Dr. Yellen noted how that inventory issue distorted the reported data. Without this decline, measured output would have been up 1% on an annualized data. An important fact that liars like Princeton Steve will just gloss over.

Hey, are you going to call Goldman Sachs to sue me? Let’s see, you defended their call on July 1 — after the close of the quarter — at +1.9%. Advance Q2 is -0.9%. They were only off by 2.8%!. That’s accuracy!

You think you got the forecast right. Of course, your gloating only proves my point about you being the most arrogant moron ever. Keep it up troll as I’m laughing my rear end off.

BTW – we know why you never record your forecasts. If you did – people could check how incredibly wrong most of them are. So you’re not just dumb and arrogant. You are also a coward.

This was the advanced estimate for real GDP in 2022Q2. The victory lap being taken by Princeton Steve reminds me of Canadian track fans during the 1988 Olympic men’s 100 meters. Yes Ben Johnson seemed to have clocked a 9:86 while Carl Lewis ran 9:92, But after further review, Johnson’s time was disqualified and Lewis got the gold.

Now I felt bad for Johnson as he was sort of duped into cheating. But when the news comes out on August 25, 2022 that real GDP grew slightly – any abuse you care to levy on the arrogant know nothing jerk was call Princeton Steve will be well deserved. Of course we know he will whine until the cows come home. That is what he does as he sings MACHO MACHO MAN!

pgl,

Let him have his “victory lap.” It looks like income rose more than GDP fell, so posiitive GDO, which looks to be more tied to employment, which we know NBER really looks at closely. The labor market simply remains too hot for Q1 and Q2 to constitute a recession when NBER gets around to clearly deciding evrentually.

BTW, to those who want to claim NBER committee is a bunch of Dems, I have known its permanent chair, Bob Hall of the Hoover INstitution, for over a half century. He is a GOP, served on Reagan’s economic transition team. In WaPo today, Allan Sloan interviewed him, and he made it clear the committee looks at all these other things. He noted part of what is going on now is the news media likes to report recessions because they make for more exciting news than growth, which is “smooth and boring.”

Robert Hall is a very competent economist. Yea he leans right. So does Martin Feldstein.

When Janet Yellen speaks, smart people listen:

https://www.msn.com/en-us/money/markets/yellen-says-us-economy-is-not-seeing-recession-conditions-now/ar-AA104OEw?ocid=msedgdhp&pc=U531&cvid=817452e21a7a45e0b6c6d2d3464dbc3f

Treasury Secretary Janet Yellen said the US economy is seeing an economic slowdown — something vital to bringing down inflation — but isn’t currently in a recession. “We do see a significant slowdown in growth,” Yellen said at a press conference on Thursday. But a true recession is a “broad-based weakening of the economy,” she said. “That is not what we’re seeing right now.”

Oh yes – the most incompetent consultant ever will disagree. Then again no one in the history of time has ever considered Princeton Steve as being smart.

Inventories accounted for more than the entire decline in GDP:

https://fred.stlouisfed.org/graph/?g=SfOl

Meanwhile, final sales returned to growth, thanks to an improvement in net exports:

https://fred.stlouisfed.org/graph/?g=SfQw

I still think overall the numbers look quite good. But if Georgetown Jerome keeps taking his marching orders from Republicans the numbers won’t be good for much longer.

What Dean Baker noted. What Janet Yellen noted. But also note that both JohnH and Princeton Steve are running around claiming they are smarter than Dr. Yellen. Yea – they are kind of dumb.

MD,

So why is Dean Baker saying they rose? I am completely confused. Really.

And if they declined, how is it that all those news stories about them piling up to excessive levels were repoted? Did they just look at a few sectors? Was it a decline of farmer inventories that did it? I sure as heck do not know.

They rose, but they rose by a lesser amount than in the prior quarter. You’re making this much more complicated than it has to be.

This has been explained to you already, twice, by commenters who said it much more articulately than I just did.

@ Rosser

You see after the link jump the last two blue bars on the far right??

https://tradingeconomics.com/united-states/changes-in-inventories

They are both blue (positive number), correct?? (that’s rhetorical Q sh*thead). Not beige (beige is negative) i.e. they are both positive, but the drop in the amount is what is whacking the GDP. What I’d just like to know from anyone is where the damned number is in the BEA tables.

Yes, I have double checked on it. While it is not labeled as such, it really is the second derivative of inventories that counts, the change in the change of inventories.

The second derivative test. Now I would insist I get all the credit for this but my ego is not nearly the size of Princeton Steve’s.

Inflation data from today’s GDP release contain an oddity:

https://fred.stlouisfed.org/graph/?g=SfS8

Despite the strength of the dollar in FX markets, import prices are rising a lot faster than domestic prices. I don’t have import quantities worked out, but my impression is that U.S. imports of energy products are fairly small relative to the total. If so, then this is more than a reflection of high energy prices. Anyhow, the data show that U.S. inflation is being pulled up by imports, and has been in several recent quarters.

Does anyone WHO HAS ACTUALLY DONE THE MATH (no chin-stroking posers, please) have any wisdom to impact?

Maybe I’m confusing gross with net imports.

MD,

I do not have the answer, but note that oil and gasoline prices peaked in mid-June, so June does not show the decline in those prices that has been happening seriously. Will need to see July numbers for that part of it to show up.

There are a lot of odd things in some of these numbers, with me elsewhere noting confusion and weirdness about the inventories numbers.

MD

Don’t know about volumes, but I looked at the FRED series Imports of goods (implicit price deflator) (A255RD3Q086SBEA).

It looks like the implicit deflator for import goods jumped from about 2.4% Y/Y to about 9.8% Y/Y from 2021Q1 to 2021Q2 and continues at that approximate Y/Y rate.

The M/M 2022Q1 to 2022Q2 percent change is about 3.0% and the current compound annualized rate is about 12.6%.

A simple second difference log ARIMA MA (1) model forecasts for 2022Q3 an increase in the import goods deflator index from 99.2 to 102.0 or an increase of about 2.8% M/M and about a 12.0% compound annualized increase.

My import prices problem is a gross vs net problem. Petroleum imports are well down from their peak as a share of the total, but stop asking for 28%.

…still account for…

My observation is consistent with what Yellen said. It’s from a pure anecdotal and local level, but because it’s so similar, it’s a data point of sorts. Real estate is off. It needed to be since it was overheated pretty badly. Construction is off, but that’s inevitable when materials are hard to get and so is labor. I don’t know for sure if the cooling of real estate is the reason for construction being off a bit or vice-versa. The help wanted signs sure aren’t going away. My own work is accelerating, not declining. I don’t know anybody who is either out of work or needs two jobs to get by, both common when we are in a recession. It’s an odd set of signals when you consider the usual non-technical signals I observe point to a recession being underway now. But, really, I just don’t see a recession.

So there’s the final word from the non-technical magic 8-ball prediction side of things. It works as well as any, so far as I can tell.

Willie,

Are you in a position to know how unfinished housing inventory is affecting builders activity or planned activity?

One thing to note about inventories – the odds of a third quarter of inventory drag on GDP are not great, though it could happen. The inventory-to-sales ratio as of May is up from April, but still low by pre-recession standards:

https://fred.stlouisfed.org/graph/?g=Sg0l

We need all three months’ data from Q2 to make a reasonable guess about inventories’ effect on Q3 GDP. That said, the Atlanta Fed’s first GDPNow estimate for Q3 will probably show up tomorrow. The inventory contribution to that estimate won’t have more inputs than the rest of us, but will offer a look at how the GDP math for Q3 inventories is shaping up, based on the little we have. Dig up the recent exchange between AS and Menzie in comments for background.

An inventory to sales ratio = 1.5 is absurdly high. Of course we should expect GDP growth to trail final sales growth. DUH. But hey – do not let reality get in the way of Princeton Steve doing his little cheerleader dance as he actually claims that he is smarter than Jeff Frankel.

Not to agree with Econned but this place has become a cease pool thanks to the Three Stooges – CoRev, Bruce Hall, and especially the arrogant incompetent consultant Princeton Steve.

Why not mention that the margin of error on jobs is twice the prediction?

Poor little Stevie – we are not treating him in a civilized manner. That after this clown said he was smarter than Jeff Frankel. Excuse me?

BTW I have been noting the points made by Dean Baker and Janet Yellen about how final sales rose. Of course Stevie is too blind to see it so maybe he should check off the graphs here:

Macroduck

July 28, 2022 at 11:55 am

Of course even if he did – he would never acknowledge the simple point. No – Princeton Steve is as dishonest as it gets. Oh wait – that may not be civilized. But it is true.

The US Economy in Q-2: First Look

In the second quarter of 2022, the US economy grew 1.6% in real terms, from a year earlier. That was down from +3.5% in January-March, and +5.5% in the final three months of 2021. However, tomorrow’s headlines will say that we are now in recession, since the economy has contracted two quarters in a row (-1.6% in Q-1 and -0.9% in the April-June period), when calculated on a seasonally adjusted quarter-to-quarter annualized basis.

Both are accurate, but the actual definition of a recession has nothing to do with growth rates. Rather, it is determined by the National Bureau of Economic Research’s (NBER) analysts, on the basis of a host of factors.

One thing we do know: the economy is slowing down. Private consumption expanded +1.8% year-on-year (YoY), down from +4.5% in Q-1. Capital investment grew +8.7%, after a strong, +11.6% run in the first quarter.

Pricing are rising, too, which should surprise no one but a hermit. The broadest measure, the GDP deflator, covers all prices in the economy, including both household, corporate, and governmental. That measure was +7.5% higher than in the first three months of 2021, up from a +6.9% pace in Q-1. However, the Federal Reserve Board of Governors (Fed) is known to favor the PCE deflator – which is broader than the Consumer Price Index (CPI), but narrower (household spending only) than its GDP counterpart. The PCE deflator rose +6.5% YoY, up a tad from +6.3% in Q-1 and +5.5% in 2021’s Q-4.

The price of imported petroleum and its byproducts rose +66.2% in April-June, from the same 2021 period, up from a blistering +55.6% pace in January-March. On the consumer side, durable goods imports cost +3.4% more than a year earlier, and non-durables just +0.5% more.

The M-2 money supply has been skidding, rather than slowing. From +20-25% in the 12 months ended March 2021, in slowed to +10-15% in the following year, and just +6.7% in Q-2 2022.