Analysis of current economic conditions and policy

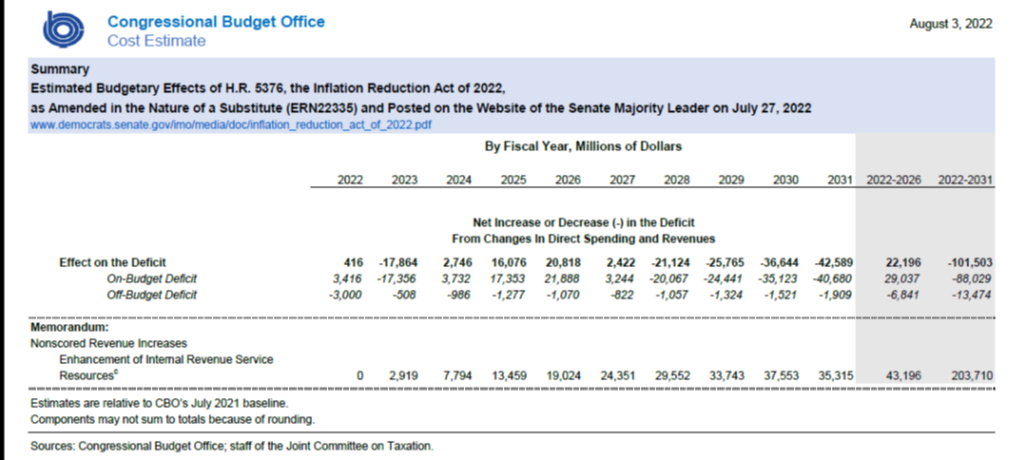

CBO Scored Inflation Reduction Act: 10 Year Deficit Reduction of $101.5 bn

As released by CBO today, decreased spending $131.5 bn, increased revenues $87.0 bn (not including expected revenues from enhanced IRS at $203.7 bn.

Penn Wharton Model evaluates macro effects here. Moody’s Analytics (Zandi) here.

35 thoughts on “CBO Scored Inflation Reduction Act: 10 Year Deficit Reduction of $101.5 bn”

pgl

“Broadly, the legislation will nudge the economy and inflation in the right direction, while meaningfully addressing climate change and reducing the government’s budget deficits” – Zandi. Penn Wharton said the bill will not impact real GDP growth.

Of course the liars in the Republican Party are saying it will cause a recession. Not even the conservative Tax Foundation is saying that.

BTW – the deficit reduction figures are for a decade time frame. Annually? Divide all numbers by 10.

Of course earlier Bruce Hall and his rabid pet dog CoRev tried to tell us government “spending” has risen under Biden. FRED provides the data on real government purchases and it seem it exploded under Trump but has come down under Biden.

Macroduck

So $335.2 billion in deficit reduction over a decade, counting both budget measures and improved tax collection.

But that’s not all the IRS could do if properly funded.

pgl

If the IRS actually enforced transfer pricing – the benefits would be considerable.

Steven Kopits

From my weekly report:

Recession Outlook Q3

–Some forecasters see positive US GDP growth in Q3

— For example, the Atlanta Fed is showing +1.3%, revised down from +2.1% on July 29

The coincident indicators we track suggest continued contraction in Q3

— Both US total product supplied (total oil products consumption) and gasoline supplied (consumption) are cratering

— Initial unemployment claims continue to rise

— The Michigan Consumer Sentiment Index for July remains just above record lows

— All of these suggest continuing recession

Those factors which saw a massive run-up during the US fiscal and monetary surge are likely to see a hard reset on the way down

– For example, job openings, which have been at historic highs by far, saw the largest monthly drop on record in June (bar March and April 2020, the depths of the pandemic shock).

— The graph below shows our forecast, suggesting job openings return to more normal levels over the next 6-12 months

— A hard reset suggests a deepening recession. Buckle up.

Steven Kopits: So you are sticking with the view we are *currently* in a recession? As of January 2022?

pgl

Let’s see:

‘Both US total product supplied (total oil products consumption) and gasoline supplied (consumption) are cratering’

Cratering is a “technical” term I guess.

‘Initial unemployment claims continue to rise’

He made this misleading claim before which has been thoroughly refuted by Barkley, by me, and the FRED graph of this series.

I’m sorry but a weekly report with such dishonesty is not worth reading.

Steven Kopits

Down 10%. That’s the technical standard for ‘cratering’.

pgl

I guess if it fell by 15% it would be suppression. I bet if you wrote a new dictionary, NO ONE would purchase it.

Steven Kopits

I appreciate you think none of my reports are reading, but I doubt anyone reads more of them than you do.

pgl

I read the Onion too. Everyone needs a good laugh and your BS is extremely funny.

Steven Kopits

So, I think Q2 is, in certain respects, an easier recession call than Q1. From March 19th, we see rising initial unemployment claims typical of a recession, and today’s IUCs at 260,000 continues that trend. So March 19 makes an organic starting point for a recession based on more traditional metrics.

However, clearly Q1 GDP was materially negative, oil consumption had begun to decline, and vmt also declined. These latter two metrics are ordinarily coincident indicators for the business cycle, so if you’re going to call a recession in Q2, it’s hard not to call it for Q1. The counter-argument rests principally on rising employment. However, if you have over-stimulated the economy on the fiscal side but were rolling this off, it seems to me that you could derive both rising employment and falling GDP, which is after all, what happened.

So, yes, thanks, I’ll stay with the standard of two declining quarters of GDP, which puts us into recession in H1.

pgl

“From March 19th, we see rising initial unemployment claims typical of a recession, and today’s IUCs at 260,000 continues that trend. So March 19 makes an organic starting point for a recession based on more traditional metrics.”

Let’ see. This series FEEL the week before, It went back up to where it was two weeks earlier. And it was 416 thousand a year ago. Of course a pathetic little liar like you can write the truth and you refuse to provide a link to FRED. Go figure.

Steven Kopits

Your linked graph shows exactly what I am saying.

pgl

“Steven Kopits

August 4, 2022 at 11:45 am

Your linked graph shows exactly what I am saying.”

I have read what you said. Have you read what I have said? Assuming you know how to read a graph – you would know you have lied. But hey – that is what you do. A LOT!

Barkley Rosser

Steven,

IUCs are not “typical of a recession.” They have been gradually rising, but they remain extremely low. This is a variable where it is the value, not the rate of change that matters. It continues to be the case that very few people are being laid off and there are way more jobs available than unemployed people. This is gradually changing, but that part of the picture remains very far from recessionary.

Steven Kopits

As for the ‘currently’ part.

If you take the view that Q1 and at least some of Q2 was a ‘technical’ recession driven by the roll off of stimulus, then you might expect the economy to right itself when the effect had passed through the system. So that’s how I drafted the initial summary slide of my weekly report.

Nevertheless, the total oil products and gasoline consumption (product supplied) numbers were really bad, down 10% below either 2019 or the beginning of the year. (See the link below.) Roll offs of this size are generally an indicator of recession, and this is high frequency data, ie, from the last four weeks, that is from Q3. Further, consumer confidence remains near record lows for July, again Q3 numbers. And IUCs continue to rise week after week, including today. All these are coincident indicators for recession, so that’s where I come out.

Finally, job openings are crashing down (see the link for my outlook), suggesting a hard reset on the way down mirroring the ballistic rise on the way up. Again, this is the reversal of the stimulus and M2 orgy going up. So we are seeing a hard reset on openings and, I think, on real estate as well. Do you think we can reset these metrics to pre-pandemic levels without a recession? I am inclined to think not.

Now, one month does not a quarter make. So let’s wait and see how it develops. But based on the indicators I track, yes, I think we are in continuing recession, and I expect a hard reset of the economy in H2.

double talk and circular logic. If those traits are ever missing that is when you’ll know it’s a Kopits imposter.

pgl

New post from Dr. Chinn noting how just an hour after this comment from Stevie that BLS showed a huge increase in employment!

pgl

I see you are still confusing changes in the deficit with fiscal policy. And repeating your lie about Initial unemployment claims. This is why NO ONE reads your BS.

Macroduck

Similar increases in initial claims occurred in 1971, 1972, 1977, 1984, 1996, 1998, 2003, 2005, 2017 with neither concurrent nor subsequent recession.

“Hard reset”? I don’t find anything in the index of any of my textbooks about “hard reset”. Confusing your cable box with economics, perhaps?

pgl

Well – Stevie really needs to be rehired as the Fox and Friends “chief economist” so he writes this nonsense to get their attention.

Steven Kopits

If job openings drop by 3 million in six months, does that qualify as a ‘hard reset’ in your mind?

pgl

Employment rose by 528 thousand last month per the BLS. Hard reset? You have a very soft excuse for a brain.

AndrewG

That’s down from huge historic highs.

Barkley Rosser

Steven,

I see nothing in your report about those fickle inventories changes, which played such an important role in the early reported GDP declines of the first two quarters. As I have noted elsewhere here, there certainly seems to be good reason to expect a strong decline in the change of changes in inventories this quarter, which would again push the economy towards a decline in GDP. Do you disagree with that? Do you avoid commenting on this matter because they are so volatile and unpredictable?

Steven Kopits

I am prepared to accept your comment on the face of it, Barkley. I am not really an expert in inventory movements, but related to that, I expect a ‘hard reset’ in the trade balance as well, and that seems to me might bump GDP up.

pgl

” I am not really an expert in inventory movements”

You are not an expert a lot of things including labor economics, basic finance, macroeconomics etc. But do not let that stop you from bloviating your usual BS.

Moses Herzog

The interview with Joe Manchin at FOX on this was classic. The word I have for the interviewer (Harris) I’m pretty certain Menzie wouldn’t let me put up here. But It won’t be too hard to find the interview on the web. One might have asked the hypothetical question anytime over the last 18 months, “If President Biden signed legislation lowering the federal deficit, surely Republicans wouldn’t criticize that??” But it’s NEVER been about deficit reduction to Republicans and “conservatives”. And only the very very very dumbest people in the room haven’t figured that out a long time ago.

Bruce Hall

Interesting… I wonder what it would have been without the ever-popular (in the Democratic Party) Sen. Manchin’s demands.

But I seen the bill as generally positive since it is supposed to be self-funded. The only issue I would have is the title. According to Moody’s Analytics chief economist Mark Zandi, the 725-page bill hammered out by Sens. Chuck Schumer (D-NY) and Joe Manchin (D-WV) would only lower the Consumer Price Index – a closely watched gauge that measures what consumers paid for goods and services –0.33% by 2031.

Moses Herzog

@ Brucey Baby

I Just phoned your township clerk. She sounded as excited as I was you’re changing your party affiliation. She said just visit here: https://mvic.sos.state.mi.us/RegisterVoter

Now remember Brucey, most Democrats are against tariffs on trade, which increases costs to consumers and can lower demand for products such as soybeans. So this will be a drastic change from your days at the hillbillies’ rallies with your MAGA dunce cap.

Bruce Hall

Go down, Moses. Way down into DC land. Tell old Uncle Joe. Let my people go.

BTW, soybeans are really not good for you. Basically pig food.

But the likelihood that it will do much of anything against inflation is purely smoke and mirrors which is pretty much what Zandi said. In fact, it probably will turn into another porkfest. So get those soybeans piled up.

pgl

Do you think eating bacon is a Communist plot? Of course Summers said in this piece that we are NOT in a recession. Gee – you forgot to mention that. Go figure!

Moses Herzog

So in essence what you’re saying is, you’re not interested in FACTS and you don’t want America to do well if it’s under a Democrat administration. Which proves what I just said above in this thread~~it’s NEVER been about deficit reduction to Republicans and “conservatives”. And only the very very very dumbest people in the room haven’t figured that out a long time ago.

pgl

Bruce Hall misses the elephant in the room. This bill will do two things MAGA Republicans like you said would cause massive economic disruptions – addressing climate change (OH NO SOCIALISM) and extending that COMMUNIST plot to give people decent health care. Odd – a small benefit to reducing inflation and a small benefit to long-term growth while lowering deficits. Of course a MAGA hat wearing moron like has to argue that all of this is BAD, BAD.

pgl

Counting pages? Oh that’s right – you cannot even read a 725 word op-ed so 725 pages must mean the bill is EVIL. Oh wait – how many pages was that 2017 tax cut for the rich? How much has it increased the Federal debt by now? And how dumb were its international tax complications like BEAT, FDII, and GILTI?

Oh wait – why am I asking Bruce Hall as he has no clue.

“Broadly, the legislation will nudge the economy and inflation in the right direction, while meaningfully addressing climate change and reducing the government’s budget deficits” – Zandi. Penn Wharton said the bill will not impact real GDP growth.

Of course the liars in the Republican Party are saying it will cause a recession. Not even the conservative Tax Foundation is saying that.

BTW – the deficit reduction figures are for a decade time frame. Annually? Divide all numbers by 10.

Of course earlier Bruce Hall and his rabid pet dog CoRev tried to tell us government “spending” has risen under Biden. FRED provides the data on real government purchases and it seem it exploded under Trump but has come down under Biden.

So $335.2 billion in deficit reduction over a decade, counting both budget measures and improved tax collection.

But that’s not all the IRS could do if properly funded.

If the IRS actually enforced transfer pricing – the benefits would be considerable.

From my weekly report:

Recession Outlook Q3

–Some forecasters see positive US GDP growth in Q3

— For example, the Atlanta Fed is showing +1.3%, revised down from +2.1% on July 29

The coincident indicators we track suggest continued contraction in Q3

— Both US total product supplied (total oil products consumption) and gasoline supplied (consumption) are cratering

— Initial unemployment claims continue to rise

— The Michigan Consumer Sentiment Index for July remains just above record lows

— All of these suggest continuing recession

Those factors which saw a massive run-up during the US fiscal and monetary surge are likely to see a hard reset on the way down

– For example, job openings, which have been at historic highs by far, saw the largest monthly drop on record in June (bar March and April 2020, the depths of the pandemic shock).

— The graph below shows our forecast, suggesting job openings return to more normal levels over the next 6-12 months

— A hard reset suggests a deepening recession. Buckle up.

Steven Kopits: So you are sticking with the view we are *currently* in a recession? As of January 2022?

Let’s see:

‘Both US total product supplied (total oil products consumption) and gasoline supplied (consumption) are cratering’

Cratering is a “technical” term I guess.

‘Initial unemployment claims continue to rise’

He made this misleading claim before which has been thoroughly refuted by Barkley, by me, and the FRED graph of this series.

I’m sorry but a weekly report with such dishonesty is not worth reading.

Down 10%. That’s the technical standard for ‘cratering’.

I guess if it fell by 15% it would be suppression. I bet if you wrote a new dictionary, NO ONE would purchase it.

I appreciate you think none of my reports are reading, but I doubt anyone reads more of them than you do.

I read the Onion too. Everyone needs a good laugh and your BS is extremely funny.

So, I think Q2 is, in certain respects, an easier recession call than Q1. From March 19th, we see rising initial unemployment claims typical of a recession, and today’s IUCs at 260,000 continues that trend. So March 19 makes an organic starting point for a recession based on more traditional metrics.

However, clearly Q1 GDP was materially negative, oil consumption had begun to decline, and vmt also declined. These latter two metrics are ordinarily coincident indicators for the business cycle, so if you’re going to call a recession in Q2, it’s hard not to call it for Q1. The counter-argument rests principally on rising employment. However, if you have over-stimulated the economy on the fiscal side but were rolling this off, it seems to me that you could derive both rising employment and falling GDP, which is after all, what happened.

So, yes, thanks, I’ll stay with the standard of two declining quarters of GDP, which puts us into recession in H1.

“From March 19th, we see rising initial unemployment claims typical of a recession, and today’s IUCs at 260,000 continues that trend. So March 19 makes an organic starting point for a recession based on more traditional metrics.”

You do lie a lot.

https://fred.stlouisfed.org/series/ICSA

Let’ see. This series FEEL the week before, It went back up to where it was two weeks earlier. And it was 416 thousand a year ago. Of course a pathetic little liar like you can write the truth and you refuse to provide a link to FRED. Go figure.

Your linked graph shows exactly what I am saying.

“Steven Kopits

August 4, 2022 at 11:45 am

Your linked graph shows exactly what I am saying.”

I have read what you said. Have you read what I have said? Assuming you know how to read a graph – you would know you have lied. But hey – that is what you do. A LOT!

Steven,

IUCs are not “typical of a recession.” They have been gradually rising, but they remain extremely low. This is a variable where it is the value, not the rate of change that matters. It continues to be the case that very few people are being laid off and there are way more jobs available than unemployed people. This is gradually changing, but that part of the picture remains very far from recessionary.

As for the ‘currently’ part.

If you take the view that Q1 and at least some of Q2 was a ‘technical’ recession driven by the roll off of stimulus, then you might expect the economy to right itself when the effect had passed through the system. So that’s how I drafted the initial summary slide of my weekly report.

Nevertheless, the total oil products and gasoline consumption (product supplied) numbers were really bad, down 10% below either 2019 or the beginning of the year. (See the link below.) Roll offs of this size are generally an indicator of recession, and this is high frequency data, ie, from the last four weeks, that is from Q3. Further, consumer confidence remains near record lows for July, again Q3 numbers. And IUCs continue to rise week after week, including today. All these are coincident indicators for recession, so that’s where I come out.

Finally, job openings are crashing down (see the link for my outlook), suggesting a hard reset on the way down mirroring the ballistic rise on the way up. Again, this is the reversal of the stimulus and M2 orgy going up. So we are seeing a hard reset on openings and, I think, on real estate as well. Do you think we can reset these metrics to pre-pandemic levels without a recession? I am inclined to think not.

Now, one month does not a quarter make. So let’s wait and see how it develops. But based on the indicators I track, yes, I think we are in continuing recession, and I expect a hard reset of the economy in H2.

(Here: http://www.prienga.com/blog/2022/8/4/10jvf9j44px0i2zt7qpcf3ptvi48fx)

double talk and circular logic. If those traits are ever missing that is when you’ll know it’s a Kopits imposter.

New post from Dr. Chinn noting how just an hour after this comment from Stevie that BLS showed a huge increase in employment!

I see you are still confusing changes in the deficit with fiscal policy. And repeating your lie about Initial unemployment claims. This is why NO ONE reads your BS.

Similar increases in initial claims occurred in 1971, 1972, 1977, 1984, 1996, 1998, 2003, 2005, 2017 with neither concurrent nor subsequent recession.

“Hard reset”? I don’t find anything in the index of any of my textbooks about “hard reset”. Confusing your cable box with economics, perhaps?

Well – Stevie really needs to be rehired as the Fox and Friends “chief economist” so he writes this nonsense to get their attention.

If job openings drop by 3 million in six months, does that qualify as a ‘hard reset’ in your mind?

Employment rose by 528 thousand last month per the BLS. Hard reset? You have a very soft excuse for a brain.

That’s down from huge historic highs.

Steven,

I see nothing in your report about those fickle inventories changes, which played such an important role in the early reported GDP declines of the first two quarters. As I have noted elsewhere here, there certainly seems to be good reason to expect a strong decline in the change of changes in inventories this quarter, which would again push the economy towards a decline in GDP. Do you disagree with that? Do you avoid commenting on this matter because they are so volatile and unpredictable?

I am prepared to accept your comment on the face of it, Barkley. I am not really an expert in inventory movements, but related to that, I expect a ‘hard reset’ in the trade balance as well, and that seems to me might bump GDP up.

” I am not really an expert in inventory movements”

You are not an expert a lot of things including labor economics, basic finance, macroeconomics etc. But do not let that stop you from bloviating your usual BS.

The interview with Joe Manchin at FOX on this was classic. The word I have for the interviewer (Harris) I’m pretty certain Menzie wouldn’t let me put up here. But It won’t be too hard to find the interview on the web. One might have asked the hypothetical question anytime over the last 18 months, “If President Biden signed legislation lowering the federal deficit, surely Republicans wouldn’t criticize that??” But it’s NEVER been about deficit reduction to Republicans and “conservatives”. And only the very very very dumbest people in the room haven’t figured that out a long time ago.

Interesting… I wonder what it would have been without the ever-popular (in the Democratic Party) Sen. Manchin’s demands.

But I seen the bill as generally positive since it is supposed to be self-funded. The only issue I would have is the title.

According to Moody’s Analytics chief economist Mark Zandi, the 725-page bill hammered out by Sens. Chuck Schumer (D-NY) and Joe Manchin (D-WV) would only lower the Consumer Price Index – a closely watched gauge that measures what consumers paid for goods and services –0.33% by 2031.

@ Brucey Baby

I Just phoned your township clerk. She sounded as excited as I was you’re changing your party affiliation. She said just visit here:

https://mvic.sos.state.mi.us/RegisterVoter

Now remember Brucey, most Democrats are against tariffs on trade, which increases costs to consumers and can lower demand for products such as soybeans. So this will be a drastic change from your days at the hillbillies’ rallies with your MAGA dunce cap.

Go down, Moses. Way down into DC land. Tell old Uncle Joe. Let my people go.

BTW, soybeans are really not good for you. Basically pig food.

I think Larry Summers had it right. Especially about the reasons for current inflation or containing future inflation.

https://finance.yahoo.com/news/larry-summers-recession-inflation-reduction-act-213052877.html

But the likelihood that it will do much of anything against inflation is purely smoke and mirrors which is pretty much what Zandi said. In fact, it probably will turn into another porkfest. So get those soybeans piled up.

Do you think eating bacon is a Communist plot? Of course Summers said in this piece that we are NOT in a recession. Gee – you forgot to mention that. Go figure!

So in essence what you’re saying is, you’re not interested in FACTS and you don’t want America to do well if it’s under a Democrat administration. Which proves what I just said above in this thread~~it’s NEVER been about deficit reduction to Republicans and “conservatives”. And only the very very very dumbest people in the room haven’t figured that out a long time ago.

Bruce Hall misses the elephant in the room. This bill will do two things MAGA Republicans like you said would cause massive economic disruptions – addressing climate change (OH NO SOCIALISM) and extending that COMMUNIST plot to give people decent health care. Odd – a small benefit to reducing inflation and a small benefit to long-term growth while lowering deficits. Of course a MAGA hat wearing moron like has to argue that all of this is BAD, BAD.

Counting pages? Oh that’s right – you cannot even read a 725 word op-ed so 725 pages must mean the bill is EVIL. Oh wait – how many pages was that 2017 tax cut for the rich? How much has it increased the Federal debt by now? And how dumb were its international tax complications like BEAT, FDII, and GILTI?

Oh wait – why am I asking Bruce Hall as he has no clue.