Today, we’re fortunate to have Willem Thorbecke, Senior Fellow at Japan’s Research Institute of Economy, Trade and Industry (RIETI) as a guest contributor. The views expressed represent those of the author himself, and do not necessarily represent those of RIETI, or any other institutions the author is affiliated with.

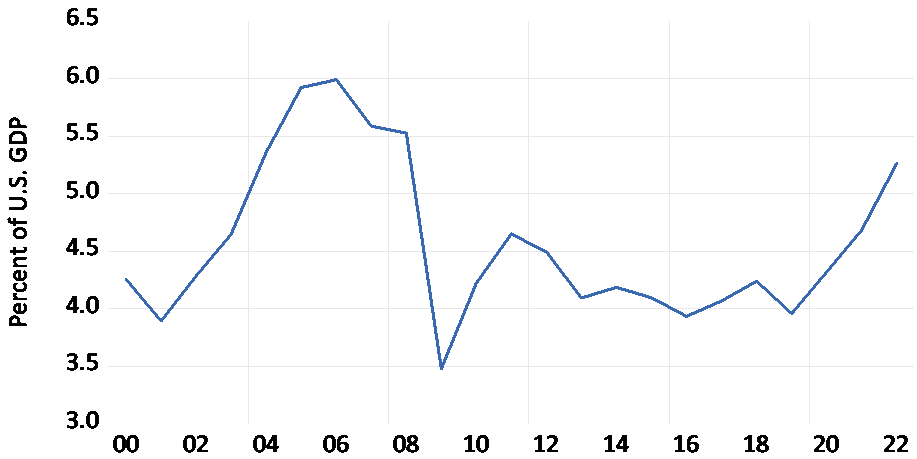

The U.S. current account deficit has increased from 2.1% of GDP in 2019 to 3.7% of GDP in 2020 to 4.8% of GDP in the first quarter of 2022. The Bureau of Economic Analysis reported that this increase is driven by a growing deficit in goods trade. Figure 1 plots the U.S trade deficit in goods.

Figure 1. U.S. Trade Deficit over the 2000-2022 Period. Source: U.S. Census Bureau.

Recent trade and current account deficits emerged in the context of large U.S. budget deficits, rising interest rates in the U.S. relative to its trading partners, and an appreciating U.S. dollar. In the 1980s the U.S. also had large budget deficits, higher interest rates relative to its trading partners, and an appreciating dollar. In the 1980s the strong dollar caused U.S. exporting and import-competing firms to lose price competitiveness. In 1985 the U.S. ran trade and current account deficits of 3% of GDP.

The G-5 countries (France, Germany, Japan, the UK, and the U.S.) were alarmed by these imbalances. To resolve them they reached the Plaza Accord in September 1985. The U.S. agreed to reduce its budget deficit, America’s trading partners implemented stimulative policies, the five countries worked together to reduce the value of the dollar, and all agreed to fight protectionism. The dollar did depreciate and the U.S. current account reached balance in 1991.

Estimating Trade Elasticities

Exchange rate adjustments seemed to help rebalance trade after the Plaza Accord. To investigate whether they would have this effect now I estimate U.S. import and export elasticities. In previous work, Chinn used dynamic ordinary least squares (DOLS) techniques to estimate trade elasticities for U.S. imports and exports over the 1975Q1-2010Q1 period. In his baseline specification, he reported an exchange rate elasticity of -0.45 and an income elasticity of 2.6 for goods imports excluding oil. For goods exports excluding agriculture he found an exchange rate elasticity of 0.6 and an income elasticity of 1.9.

I estimate aggregate import and export elasticities using data on goods imports excluding oil and goods exports from the U.S. Census Bureau and the U.S. International Trade Commission. These are deflated using import and export price data obtained from the U.S. Bureau of Labor Statistics. Following the imperfect substitutes model, imports are assumed to depend on the real exchange rate and GDP in the U.S. and exports on the real exchange rate and GDP in the rest of the world. Data on the broad consumer price index deflated real effective exchange rate are obtained from the Bank for International Settlements and data on U.S. GDP from the OECD. Data on GDP in the rest of the world are calculated as a geometrically weighted average of GDP in 15 leading trading partners, where the GDP data come again from the OECD. The model is estimated using DOLS and data extending from 1994Q1 to 2019Q4. Four lags and two leads of the first differenced right-hand side variables, quarterly dummies, a time trend, and dummies for the Global Financial Crisis are also included in the model.

The resulting import function is:

Sample Period = 1995Q2-2019Q4, Adjusted R-squared = 0.991, Heteroskedasticity and autocorrelation corrected standard errors in parentheses, *** denotes significance at the 1% level.

In equation (1) IM represents U.S. real imports excluding oil, RER represents the real effective exchange rate, and USGDP represents U.S. real GDP. The results indicate that a 10 percent dollar appreciation would increase imports by 5.0% and that a 10% increase in U.S. GDP would increase imports by 21.0%.

The corresponding results for exports are:

Sample Period = 1995Q2-2019Q4, Adjusted R-squared = 0.991, Heteroskedasticity and autocorrelation corrected standard errors in parentheses, *** denotes significance at the 1% level.

In equation (2) EX represents U.S. real exports, RER represents the real effective exchange rate, and ROWGDP represents real GDP in the rest of the world. The results indicate that a 10 percent dollar appreciation would reduce exports by 5.2% and that a 10% increase in rest of the world GDP would increase exports by 31.7%.

Implications

The Marshall–Lerner condition states that, beginning from balanced trade, a currency depreciation will improve a country’s trade balance if the sum of the absolute values of the export and import elasticities exceeds one. The price elasticities in equations (1) and (2) just meet this condition. This suggests that a dollar depreciation would help to improve the trade balance

Between 2000 and 2021, the U.S. current account deficit averaged 3.4% of U.S. GDP. So far the rest of the world has been willing to finance these U.S. deficits. If the rest of the world grows unwilling to continue accumulating U.S. assets on this scale, the dollar will depreciate. The results above indicate that the depreciation will help to improve the trade balance. However, the price elasticities are not large. This implies that a depreciation alone will not be enough to rebalance trade. This would force some of the adjustment to come through a fall in U.S. GDP. Such an adjustment would prove painful for U.S. workers, consumers, and firms.

The U.S. budget deficit has averaged 6.6% of GDP over the last 12 years. This fiscal stimulus increases U.S. GDP and thus the U.S. current account deficit. The U.S budget deficit that caused consternation in 1985 was below 5% of GDP. So the U.S. budget and current account deficits that led to urgent action in the Plaza Accord are now exceeded year after year. Both to help reduce the current account deficit and to help fight inflation, the U.S. should reduce its budget deficit.

This post written by Willem Thorbecke.

The crux of the argument: “If the rest of the world grows unwilling to continue accumulating U.S. assets on this scale, the dollar will depreciate.”

And, here I am thinking it’s currency traders that dominate the exchange rate markets, and that there’s still no good substitute for the US dollar!

Silly me.

‘If the rest of the wrold grows unwilling to continue accumulating U.S. assets on this scale at a given interest rate, then interest rates will rise, and the dollar will appreciate, or depreciate, depending on which effect is stronger.’

I’m always surprised when scholars go beyond 101 in some parts of a paper or article, then fall back to 101 in another. There are a fair number of self-regulating mechanisms in an economy. They interact. There’s no reason to present one self-regulating mechanism but ignore another.

Meanwhile, a substantial driver of U.S. asset accumulation is likely to strengthen in the short-to-medium term:

https://asiatimes.com/2022/09/falling-fx-reserves-herald-asia-financial-crisis-2-0/

FX reserves are shrinking due to exchange-rate defense in Thailand, Malaysia and India, among others.

Biden again does the “competent President” thing:

https://www.cnn.com/2022/09/15/politics/biden-white-house-railroad-strike/index.html

Not that hard if you know what you are doing.

this is a big deal. a railroad strike would have been, politically, a huge defeat. it would have been very bad for inflation via the logistics issue. not sure how it would have impacted jobs. but it is a complication that was, and should have been, avoided. good job President Biden.

“The U.S. current account deficit has increased from 2.1% of GDP in 2019 to 3.7% of GDP in 2020 to 4.8% of GDP in the first quarter of 2022.”

One reason why our trade deficit has risen as our recovery from the pandemic has been stronger than that of our trading partners. His estimated import and export functions give us a means for estimating this Keynesian income effect.

Of course Economic Know Nothing Princeton Steve sees our trade deficit as a weakness with impending doom. Of course he always runs around like Chicken Little.

The analogy to what policy makers did in the 1980’s is instructive. Yes we need to be careful with our macroeconomic policies but our trading partners could use a bit more stimulus. And yes – let the dollar devalue.

“The results above indicate that the depreciation will help to improve the trade balance. However, the price elasticities are not large. This implies that a depreciation alone will not be enough to rebalance trade. This would force some of the adjustment to come through a fall in U.S. GDP. Such an adjustment would prove painful for U.S. workers, consumers, and firms.”

[ Goes into my very poorly done imitation voice of Randy “Macho Man” Savage ] Ooooooh yeeeeeeah!!!! Ooooooohh Yeeeeah!!!! Well, a Merry Christmas to you too Mr. Thorbecke, Merry Christmas to you too!!!! [ Exits mental space where tiny “Macho Man” Savage lives in my weird mind ]

As someone who just visited Europe for the first time in three years, it was a pleasure to do so with the exchange rate at nearly one to one between the euro and the USD. Don’t know how long that will last.

Shouldn’t you propagate the error from GDP to trade measures? Or is it just simpler to assume you have the actual true values of output and trade?

If you are building a bridge, can you afford to ignore margins of error?

Studying the margin of error in this case is like arguing about the color of the bridge … it is related to the subject at hand, but not in an interesting way.