Analysis of current economic conditions and policy

IMF World Economic Outlook, October 2022: “Countering the Cost of Living Crisis”

Is out [link], along with forecasts. From Pierre Olivier Gourinchas’s blog post:

19 thoughts on “IMF World Economic Outlook, October 2022: “Countering the Cost of Living Crisis””

pgl

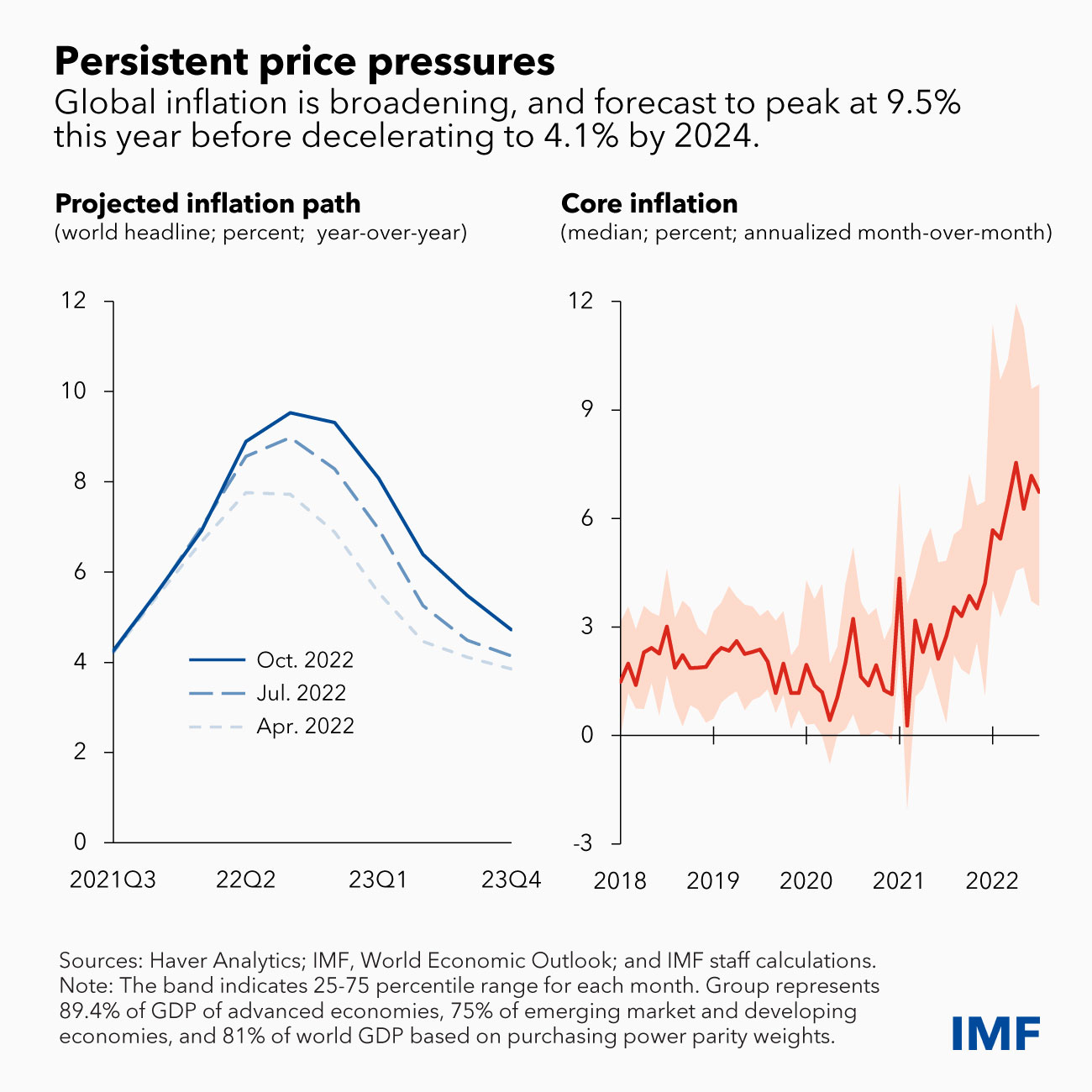

“Global inflation is forecast to rise from 4.7 percent in 2021 to 8.8 percent in 2022 but to decline to 6.5 percent in 2023 and to 4.1 percent by 2024. Monetary policy should stay the course to restore price stability, and fiscal policy should aim to alleviate the cost-of-living pressures while maintaining a sufficiently tight stance aligned with monetary policy. Structural reforms can further support the fight against inflation by improving productivity and easing supply constraints, while multilateral cooperation is necessary for fast-tracking the green energy transition and preventing fragmentation.”

Huh – this will disappoint the MAGA hatters like Bruce Hall and CoRev. Inflation to moderate as long as we continue the prudent steps emanating from the Biden White House. I guess this is why Bruce Hall’s latest rant ignored all of this as he lamented there were smart people in the workforce replacing dumb old men like him.

A prize for the economics of panic

By Paul Krugman

Do people still read Rudyard Kipling’s “If”? Even if you haven’t, you probably know how it begins: “If you can keep your head when all about you are losing theirs …” Refusing to panic, Kipling asserted, was a great virtue.

But during a bank run, refusing to panic can also be a way to lose all your money.

On Monday, the Nobel Prize in Economics was given to a household name, Ben Bernanke, and two economists’ economists, Douglas Diamond and Philip Dybvig, largely for papers they published almost 40 years ago. So let’s talk about their work and why, unfortunately, it remains all too relevant.

An aside: I sometimes encounter people who insist that the economics prize isn’t a “real” Nobel, because it’s just an award handed out by some Swedes, unlike the other prizes, which are … awards handed out by some Swedes. Yes, I may be talking my own book here, since I got one of these things myself in 2008, but it’s hard to deny the importance of the economics work the Swedes just honored.

Obviously, Bernanke, Diamond and Dybvig weren’t the first economists to notice that bank runs happen. But Diamond and Dybvig * provided the first really clear analysis of why they happen — and why, destructive as they are, they can represent rational behavior on the part of bank depositors. Their analysis was also full of implications for financial policy. At the same time, Bernanke ** provided evidence on why bank runs matter and, although he avoided saying so directly, why Milton Friedman was wrong about the causes of the Great Depression.

Diamond and Dybvig offered a stylized but insightful model of what banks do. They argued that there is always a tension between individuals’ desire for liquidity — ready access to funds — and the economy’s need to make long-term investments that can’t easily be converted into cash.

Banks square that circle by taking money from depositors who can withdraw their funds at will — making those deposits highly liquid — and investing most of that money in illiquid assets, such as business loans.

So banking is a productive activity that makes the economy richer by reconciling otherwise incompatible desires for liquidity and productive investment. And it normally works because only a fraction of a bank’s depositors want to withdraw their funds at any given time.

This does, however, make banks vulnerable to runs. Suppose that for some reason many depositors come to believe that many other depositors are about to cash out, and try to beat the pack by withdrawing their own funds. To meet these demands for liquidity, a bank will have to sell off its illiquid assets at fire sale prices, and doing so can drive an institution that should be solvent into bankruptcy. If that happens, people who didn’t withdraw their funds will be left with nothing. So during a panic, the rational thing to do is to panic along with everyone else.

There was, of course, a huge wave of banking panics in 1930-31. Many banks failed, and those that survived made far fewer business loans than before, holding cash instead, while many families shunned banks altogether, putting their cash in safes or under their mattresses. The result was a diversion of wealth into unproductive uses. In his 1983 paper, Bernanke offered evidence that this diversion played a large role in driving the economy into a depression and held back the subsequent recovery.

As I said, this was a tacit rejection of Milton Friedman….

Krugman’s OpEd is often good for a laugh. Great economist but he far too often writes in a horribly partisan and political voice. Anyone who knows the slightest about the economics of the Great Depression know that Bernanke’s non-monetary contributions were a compliment to Friedman & Schwartz’s A Monetary History. Same with other contributions including Econbrowser’s own Jim Hamilton who has stated monetary contraction as a driver behind the initial downturn (Hamilton 1987) but I suppose his views could have changed. Anyways, here’s Bernanke with what sounds to me to be an explicit endorsement of Friedman & Schwartz: “Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.”

pgl

First of all Bernanke himself noted he was following up on Friedman & Schwartz. Anyone who knew anything knows that – but not Econned. Secondly, you should be the last person to accuse someone else of being partisan.

But yea – way to keep up the jerk act. It is your only forte.

Barkley Rosser

pgl,

Actually on this one I think Econned has a point, although he overdoes it and does not correctly spell “complement.” I was myself thinking of posting on how Krugman was getting it wrong about Bernanke supposedly showing that Milton Friedman was “wrong” about the Great Depression. As you yourself say, Bernanke’s work clearly followed up on that of Friedman and Schwatz, complements it.

This is a surprising to me blunder by Krugman, whom I usually agree with.

Econned

“Barkley Rosser”,

Please expand on “overdoes it”.

Barkley Rosser

Econned,

Oh dear, you are now so stupid you do not get when you go over the line? There were so many items in your attempt to actually make a substantive comment, which ones were “overdoes it” is a long list. Not going to get into all of your stupid comments.

Oh, “Econned,” you want one? Oh, well try your opening remark: that somehow Krugman’s Op Ed is “often good for a laugh.” Listen, you worthless piece of scum. I have gone after Krugman, whom I know personally, very seriously here and elsewhere on deeply serious matters, with regulars here siding with him against me. But most of the time he is right on most things, as I have noted here, even when I have given him serious s**t. much to the disagreement of serioius regular commentators here, which you are not.

I could go on, but you are not worth it, utterly worthless garbage that you are.

Who the eff do you think you are putting quotation marks around my name? I am a very real and very serious person here, unlike you, you lying fraud.

Are you pretending to be CoRev on his ultimately and absolutely worst days declaring that my late father was not actually a super important person in the US space program? Check out “Mathematics of Space Flight,” 1945, J.B. Rosser, [Sr], still in print.

So, moment of super egomania by me, not Menzie. Earlier this day I hosted John A. List at JMU via zoom for a seminar. I shall not reproduce what he said precisely, but he said very complimentary remarks that I questioned, but, there is only so far one will argue with a near certain future visitant to Stockholm.

Econned

“Barkley Rosser”,

I see you’re still acting childish with the name calling. But I’ll indulge…

1) it’s obvious you answered emotionally and are unable to provide specific examples of me overdoing it. Aside from mentioing Krugman’s opeds being good for a laugh.

2) It’s laughable what Krugman wrote regarding Bernanke and Friedman. You agree Krugman wasn’t accurate and I find it laughable that an economist such as Krugman would print such an asinine comment when we all know he only did so because of his subjectiveness regarding Friedman. So, yes, laughable is a proper description.

3) Please stop obfuscating – it’s pointless for you to say “ But most of the time he is right on most things, as I have noted here, even when I have given him serious s**t” for a few reasons, a) it isn’t germane to the specific topic at hand b) I clearly stated Krugman is a “Great economist but he far too often writes in a horribly partisan and political voice”

4) I’ve been clear in the past why I continue to place quotations around your name. I am giving the real Barkley Rosser the benefit of the doubt that they wouldn’t be this blog-commenting entity. Their family, colleagues, and friends would likely do the same.

5) I’ve never once mentioned your “father” – real or pretend

6) Did you learn all about “super important people” from listening to DJT speeches?

7) you questioning List is wholly irrelevant here. Not at all related to the topic at hand of which you’ve provided a lot of words but minimal substance

pgl

I put up a discussion by TAP’s Robert Kuttner – some of which was OK but as my comment noted some of it I disagreed with.

At one point Kuttner took the position that Bernanke was giving a very different picture of the role of monetary policy than what one would get reading Friedman and Schwartz. While I get their book was much richer than the simpleton slogan Only Money Matters but I do see differences in what Bernanke offered.

Read Kuttner’s short discussion and comment please. I would have expected Econned to do so but as usual he cannot get past his own Anger Management issues.

AndrewG

Agree here with Rosser. Otherwise, great share by pgl and great read by Krugman.

AndrewG

Sorry, great share by *ltr*, not pgl (this time).

Bernanke on Friedman & Schwartz:

Remarks by Governor Ben S. Bernanke

At the Conference to Honor Milton Friedman, University of Chicago, Chicago, Illinois

November 8, 2002

On Milton Friedman’s Ninetieth Birthday https://www.federalreserve.gov/BOARDDOCS/SPEECHES/2002/20021108/

I can think of no greater honor than being invited to speak on the occasion of Milton Friedman’s ninetieth birthday. Among economic scholars, Friedman has no peer. His seminal contributions to economics are legion …

…

Conclusion

The brilliance of Friedman and Schwartz’s work on the Great Depression is not simply the texture of the discussion or the coherence of the point of view. Their work was among the first to use history to address seriously the issues of cause and effect in a complex economic system, the problem of identification. Perhaps no single one of their “natural experiments” alone is convincing; but together, and enhanced by the subsequent research of dozens of scholars, they make a powerful case indeed.

For practical central bankers, among which I now count myself, Friedman and Schwartz’s analysis leaves many lessons. What I take from their work is the idea that monetary forces, particularly if unleashed in a destabilizing direction, can be extremely powerful. The best thing that central bankers can do for the world is to avoid such crises by providing the economy with, in Milton Friedman’s words, a “stable monetary background”–for example as reflected in low and stable inflation.

Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.

Best wishes for your next ninety years.

Moses Herzog

Say what you will about Econned, I have to say his rejoinder to Barkley Junior here is one of the best lines typed over Econbrowser’s entire existence: Did you learn all about “super important people” from listening to DJT speeches?

Oh, never have I seen the essence of Barkley Junior’s soul stated so accurately. Thanks for the literal belly-laugh.

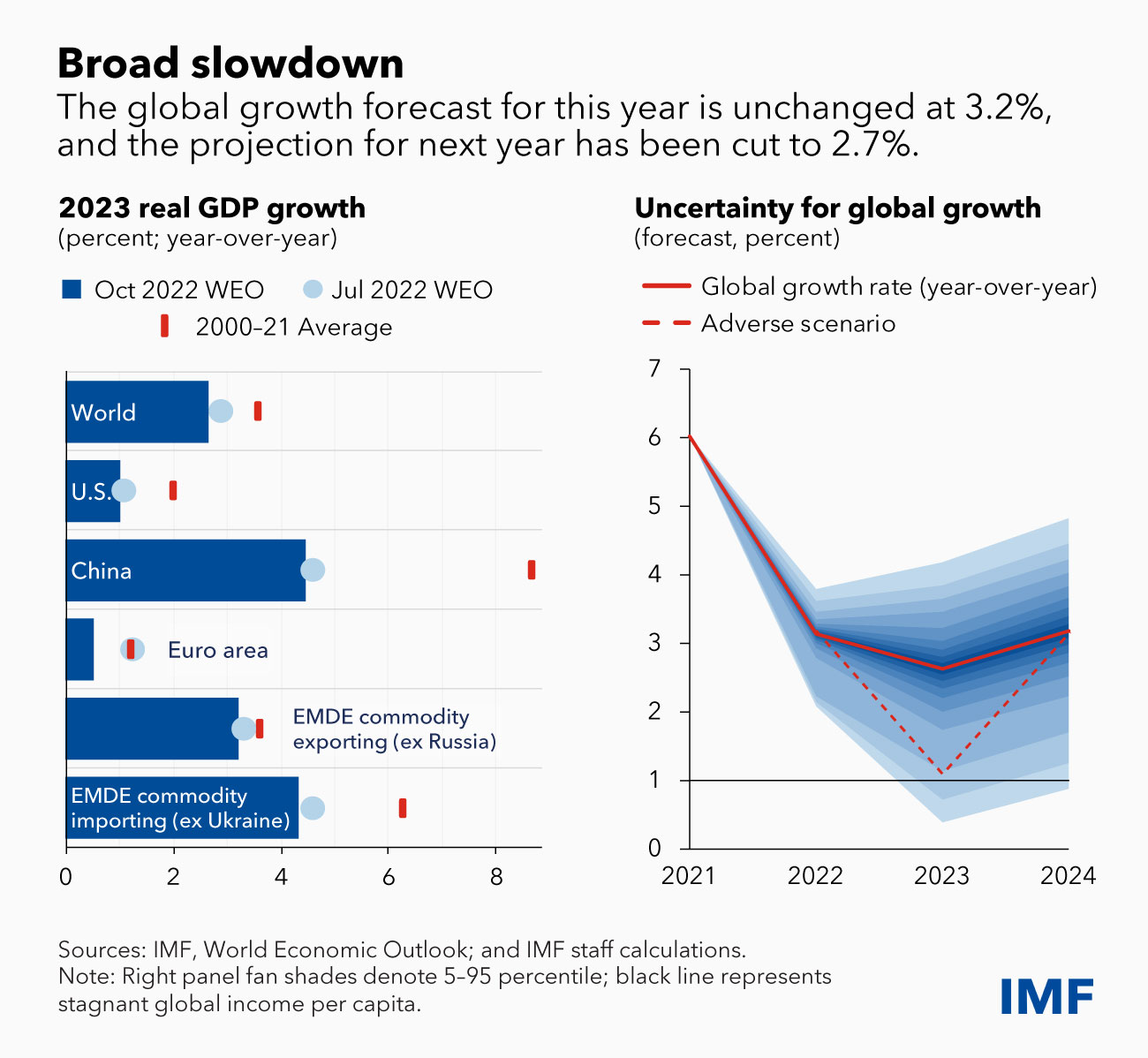

A 2.7% pace of growth for 2023 would be similar to 2019 and much of the 2000-teens. That’s mighty optimistic, given that there was no similar food-and-fuel supply disruption not a similarly contractionary monetary environment during the teens. Nor was China shutting down chunks of its economy in the teens.

The asymmetry of the forecast distribution looks more realistic than the central forecast. China, Japan and the UK all engaging in market intervention hints at one of the big downside risks to global growth. The IMF appears to be whistling in preparation to walk past the 2023 graveyard. It’s SOP, and well-intentioned, but should be seen for what it is.

Biden’s trade war against himself

By Anne O. Krueger

The contradiction between U.S. President Joe Biden’s major domestic and foreign-policy objectives and his administration’s trade policies has grown increasingly sharp. As Biden nears the midpoint of his electoral term, it is no exaggeration to say that he is waging war against his own agenda.

On the domestic front, the administration has emphasized the need to mitigate climate change, reduce inflation, fight poverty, and maintain productivity and growth. But its trade policies will do the opposite.

The same is true of U.S. foreign-policy objectives. Despite a clear bipartisan consensus on the need to strengthen U.S. alliances, the administration has raised tariffs on Canadian lumber, imposed stricter “Buy American” measures (which conflict with its World Trade Organization obligations), and taken other steps that harm U.S. allies.

Worse, these policies have raised (or at least failed to lower) costs and prices at a time when inflation is perched at a four-decade high….

Anne O. Krueger is Senior Research Professor of International Economics at the Johns Hopkins University School of Advanced International Studies and Senior Fellow at the Center for International Development at Stanford University.

ltr

That America has set out an array of seemingly forever and forever-growing economic sanctions, from Zimbabwe through Venezuela can not be an assist to growth really needs to be examined, though I imagine such an examination would come with considerable political calumny. After all, punishing Zimbabwe for fighting free of British rule and attempting land-reform after the British had taken as much of the land as possible, seems at least crudely unfairly limiting to actual Zimbabweans.

Macroduck

Speaking of Ben Bernanke, as everyone is doing just now, here’s a link to one of his (and Mark Gertler’s and Mark Watson’s) works nt honored by the Nobel committee:

Monetary policy and oil price shocks – wonder what that might tell us?

Among other things, it tells us the Fed’s response to oil price increases generally does more to reduce real output than does the oil price increase itself. Something like 2/3 to 3/4 of the contractionary impact of an oil price increase met with monetary tightening results from the monetary tightening. Given that difference, it’s no surprise that the contractionary effects of monetary tightening are also more persistent than those of oil price increases.

Seems like something to keep in mind.

The paper leans pretty heavily on work by one James Hamilton.

rsm

《Researchers recognize that they do not know the true function and seem to treat, usually implicitly, their results as a good-enough approximation. But there is no basis for the belief that the results of what is run in practice is anything close to the underlying phenomenon, even if there is an underlying phenomenon. This just seems to be wishful thinking. Most regression analysis research doesn’t even pay lip service to theoretical regularities. But you can’t just regress anything you want and expect the results to approximate reality. And even when researchers take somewhat seriously the need to have an underlying theoretical framework – as they have, at least to some extent, in the examples of studies of earnings, educational achievement, and GNP that I have used to illustrate my argument – they are so far from the conditions necessary for proper specification that one can have no confidence in the validity of the results.》

Why does this quotation from Steven J Klees call this blog to mind?

Why doesn’t the IMF include error bars for past measurements?

“Global inflation is forecast to rise from 4.7 percent in 2021 to 8.8 percent in 2022 but to decline to 6.5 percent in 2023 and to 4.1 percent by 2024. Monetary policy should stay the course to restore price stability, and fiscal policy should aim to alleviate the cost-of-living pressures while maintaining a sufficiently tight stance aligned with monetary policy. Structural reforms can further support the fight against inflation by improving productivity and easing supply constraints, while multilateral cooperation is necessary for fast-tracking the green energy transition and preventing fragmentation.”

Huh – this will disappoint the MAGA hatters like Bruce Hall and CoRev. Inflation to moderate as long as we continue the prudent steps emanating from the Biden White House. I guess this is why Bruce Hall’s latest rant ignored all of this as he lamented there were smart people in the workforce replacing dumb old men like him.

https://www.imf.org/en/Publications/WEO#:~:text=Global%20inflation%20is%20forecast%20to,to%204.1%20percent%20by%202024.

October 11, 2022

World Economic Outlook

https://www.nytimes.com/2022/10/11/opinion/nobel-economics-bernanke-diamond-dybvig.html

October 11, 2022

A prize for the economics of panic

By Paul Krugman

Do people still read Rudyard Kipling’s “If”? Even if you haven’t, you probably know how it begins: “If you can keep your head when all about you are losing theirs …” Refusing to panic, Kipling asserted, was a great virtue.

But during a bank run, refusing to panic can also be a way to lose all your money.

On Monday, the Nobel Prize in Economics was given to a household name, Ben Bernanke, and two economists’ economists, Douglas Diamond and Philip Dybvig, largely for papers they published almost 40 years ago. So let’s talk about their work and why, unfortunately, it remains all too relevant.

An aside: I sometimes encounter people who insist that the economics prize isn’t a “real” Nobel, because it’s just an award handed out by some Swedes, unlike the other prizes, which are … awards handed out by some Swedes. Yes, I may be talking my own book here, since I got one of these things myself in 2008, but it’s hard to deny the importance of the economics work the Swedes just honored.

Obviously, Bernanke, Diamond and Dybvig weren’t the first economists to notice that bank runs happen. But Diamond and Dybvig * provided the first really clear analysis of why they happen — and why, destructive as they are, they can represent rational behavior on the part of bank depositors. Their analysis was also full of implications for financial policy. At the same time, Bernanke ** provided evidence on why bank runs matter and, although he avoided saying so directly, why Milton Friedman was wrong about the causes of the Great Depression.

Diamond and Dybvig offered a stylized but insightful model of what banks do. They argued that there is always a tension between individuals’ desire for liquidity — ready access to funds — and the economy’s need to make long-term investments that can’t easily be converted into cash.

Banks square that circle by taking money from depositors who can withdraw their funds at will — making those deposits highly liquid — and investing most of that money in illiquid assets, such as business loans.

So banking is a productive activity that makes the economy richer by reconciling otherwise incompatible desires for liquidity and productive investment. And it normally works because only a fraction of a bank’s depositors want to withdraw their funds at any given time.

This does, however, make banks vulnerable to runs. Suppose that for some reason many depositors come to believe that many other depositors are about to cash out, and try to beat the pack by withdrawing their own funds. To meet these demands for liquidity, a bank will have to sell off its illiquid assets at fire sale prices, and doing so can drive an institution that should be solvent into bankruptcy. If that happens, people who didn’t withdraw their funds will be left with nothing. So during a panic, the rational thing to do is to panic along with everyone else.

There was, of course, a huge wave of banking panics in 1930-31. Many banks failed, and those that survived made far fewer business loans than before, holding cash instead, while many families shunned banks altogether, putting their cash in safes or under their mattresses. The result was a diversion of wealth into unproductive uses. In his 1983 paper, Bernanke offered evidence that this diversion played a large role in driving the economy into a depression and held back the subsequent recovery.

As I said, this was a tacit rejection of Milton Friedman….

* https://www.bu.edu/econ/files/2012/01/DD83jpe.pdf

** https://www.nber.org/system/files/working_papers/w1054/w1054.pdf

Krugman’s OpEd is often good for a laugh. Great economist but he far too often writes in a horribly partisan and political voice. Anyone who knows the slightest about the economics of the Great Depression know that Bernanke’s non-monetary contributions were a compliment to Friedman & Schwartz’s A Monetary History. Same with other contributions including Econbrowser’s own Jim Hamilton who has stated monetary contraction as a driver behind the initial downturn (Hamilton 1987) but I suppose his views could have changed. Anyways, here’s Bernanke with what sounds to me to be an explicit endorsement of Friedman & Schwartz: “Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.”

First of all Bernanke himself noted he was following up on Friedman & Schwartz. Anyone who knew anything knows that – but not Econned. Secondly, you should be the last person to accuse someone else of being partisan.

But yea – way to keep up the jerk act. It is your only forte.

pgl,

Actually on this one I think Econned has a point, although he overdoes it and does not correctly spell “complement.” I was myself thinking of posting on how Krugman was getting it wrong about Bernanke supposedly showing that Milton Friedman was “wrong” about the Great Depression. As you yourself say, Bernanke’s work clearly followed up on that of Friedman and Schwatz, complements it.

This is a surprising to me blunder by Krugman, whom I usually agree with.

“Barkley Rosser”,

Please expand on “overdoes it”.

Econned,

Oh dear, you are now so stupid you do not get when you go over the line? There were so many items in your attempt to actually make a substantive comment, which ones were “overdoes it” is a long list. Not going to get into all of your stupid comments.

Oh, “Econned,” you want one? Oh, well try your opening remark: that somehow Krugman’s Op Ed is “often good for a laugh.” Listen, you worthless piece of scum. I have gone after Krugman, whom I know personally, very seriously here and elsewhere on deeply serious matters, with regulars here siding with him against me. But most of the time he is right on most things, as I have noted here, even when I have given him serious s**t. much to the disagreement of serioius regular commentators here, which you are not.

I could go on, but you are not worth it, utterly worthless garbage that you are.

BTW, “”””””””””””Econned””””””””””””””””””””””””””””

Who the eff do you think you are putting quotation marks around my name? I am a very real and very serious person here, unlike you, you lying fraud.

Are you pretending to be CoRev on his ultimately and absolutely worst days declaring that my late father was not actually a super important person in the US space program? Check out “Mathematics of Space Flight,” 1945, J.B. Rosser, [Sr], still in print.

So, moment of super egomania by me, not Menzie. Earlier this day I hosted John A. List at JMU via zoom for a seminar. I shall not reproduce what he said precisely, but he said very complimentary remarks that I questioned, but, there is only so far one will argue with a near certain future visitant to Stockholm.

“Barkley Rosser”,

I see you’re still acting childish with the name calling. But I’ll indulge…

1) it’s obvious you answered emotionally and are unable to provide specific examples of me overdoing it. Aside from mentioing Krugman’s opeds being good for a laugh.

2) It’s laughable what Krugman wrote regarding Bernanke and Friedman. You agree Krugman wasn’t accurate and I find it laughable that an economist such as Krugman would print such an asinine comment when we all know he only did so because of his subjectiveness regarding Friedman. So, yes, laughable is a proper description.

3) Please stop obfuscating – it’s pointless for you to say “ But most of the time he is right on most things, as I have noted here, even when I have given him serious s**t” for a few reasons, a) it isn’t germane to the specific topic at hand b) I clearly stated Krugman is a “Great economist but he far too often writes in a horribly partisan and political voice”

4) I’ve been clear in the past why I continue to place quotations around your name. I am giving the real Barkley Rosser the benefit of the doubt that they wouldn’t be this blog-commenting entity. Their family, colleagues, and friends would likely do the same.

5) I’ve never once mentioned your “father” – real or pretend

6) Did you learn all about “super important people” from listening to DJT speeches?

7) you questioning List is wholly irrelevant here. Not at all related to the topic at hand of which you’ve provided a lot of words but minimal substance

I put up a discussion by TAP’s Robert Kuttner – some of which was OK but as my comment noted some of it I disagreed with.

At one point Kuttner took the position that Bernanke was giving a very different picture of the role of monetary policy than what one would get reading Friedman and Schwartz. While I get their book was much richer than the simpleton slogan Only Money Matters but I do see differences in what Bernanke offered.

Read Kuttner’s short discussion and comment please. I would have expected Econned to do so but as usual he cannot get past his own Anger Management issues.

Agree here with Rosser. Otherwise, great share by pgl and great read by Krugman.

Sorry, great share by *ltr*, not pgl (this time).

Bernanke on Friedman & Schwartz:

Remarks by Governor Ben S. Bernanke

At the Conference to Honor Milton Friedman, University of Chicago, Chicago, Illinois

November 8, 2002

On Milton Friedman’s Ninetieth Birthday

https://www.federalreserve.gov/BOARDDOCS/SPEECHES/2002/20021108/

I can think of no greater honor than being invited to speak on the occasion of Milton Friedman’s ninetieth birthday. Among economic scholars, Friedman has no peer. His seminal contributions to economics are legion …

…

Conclusion

The brilliance of Friedman and Schwartz’s work on the Great Depression is not simply the texture of the discussion or the coherence of the point of view. Their work was among the first to use history to address seriously the issues of cause and effect in a complex economic system, the problem of identification. Perhaps no single one of their “natural experiments” alone is convincing; but together, and enhanced by the subsequent research of dozens of scholars, they make a powerful case indeed.

For practical central bankers, among which I now count myself, Friedman and Schwartz’s analysis leaves many lessons. What I take from their work is the idea that monetary forces, particularly if unleashed in a destabilizing direction, can be extremely powerful. The best thing that central bankers can do for the world is to avoid such crises by providing the economy with, in Milton Friedman’s words, a “stable monetary background”–for example as reflected in low and stable inflation.

Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression. You’re right, we did it. We’re very sorry. But thanks to you, we won’t do it again.

Best wishes for your next ninety years.

Say what you will about Econned, I have to say his rejoinder to Barkley Junior here is one of the best lines typed over Econbrowser’s entire existence:

Did you learn all about “super important people” from listening to DJT speeches?

Oh, never have I seen the essence of Barkley Junior’s soul stated so accurately. Thanks for the literal belly-laugh.

Here’s the record of world GDP growth

https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?end=2021&locations=1W&start=1985

A 2.7% pace of growth for 2023 would be similar to 2019 and much of the 2000-teens. That’s mighty optimistic, given that there was no similar food-and-fuel supply disruption not a similarly contractionary monetary environment during the teens. Nor was China shutting down chunks of its economy in the teens.

The asymmetry of the forecast distribution looks more realistic than the central forecast. China, Japan and the UK all engaging in market intervention hints at one of the big downside risks to global growth. The IMF appears to be whistling in preparation to walk past the 2023 graveyard. It’s SOP, and well-intentioned, but should be seen for what it is.

https://news.cgtn.com/news/2022-09-22/Biden-s-trade-war-against-himself-1dxajteTQkg/index.html

September 22, 2022

Biden’s trade war against himself

By Anne O. Krueger

The contradiction between U.S. President Joe Biden’s major domestic and foreign-policy objectives and his administration’s trade policies has grown increasingly sharp. As Biden nears the midpoint of his electoral term, it is no exaggeration to say that he is waging war against his own agenda.

On the domestic front, the administration has emphasized the need to mitigate climate change, reduce inflation, fight poverty, and maintain productivity and growth. But its trade policies will do the opposite.

The same is true of U.S. foreign-policy objectives. Despite a clear bipartisan consensus on the need to strengthen U.S. alliances, the administration has raised tariffs on Canadian lumber, imposed stricter “Buy American” measures (which conflict with its World Trade Organization obligations), and taken other steps that harm U.S. allies.

Worse, these policies have raised (or at least failed to lower) costs and prices at a time when inflation is perched at a four-decade high….

Anne O. Krueger is Senior Research Professor of International Economics at the Johns Hopkins University School of Advanced International Studies and Senior Fellow at the Center for International Development at Stanford University.

That America has set out an array of seemingly forever and forever-growing economic sanctions, from Zimbabwe through Venezuela can not be an assist to growth really needs to be examined, though I imagine such an examination would come with considerable political calumny. After all, punishing Zimbabwe for fighting free of British rule and attempting land-reform after the British had taken as much of the land as possible, seems at least crudely unfairly limiting to actual Zimbabweans.

Speaking of Ben Bernanke, as everyone is doing just now, here’s a link to one of his (and Mark Gertler’s and Mark Watson’s) works nt honored by the Nobel committee:

https://www.brookings.edu/bpea-articles/systematic-monetary-policy-and-the-effects-of-oil-price-shocks/

Monetary policy and oil price shocks – wonder what that might tell us?

Among other things, it tells us the Fed’s response to oil price increases generally does more to reduce real output than does the oil price increase itself. Something like 2/3 to 3/4 of the contractionary impact of an oil price increase met with monetary tightening results from the monetary tightening. Given that difference, it’s no surprise that the contractionary effects of monetary tightening are also more persistent than those of oil price increases.

Seems like something to keep in mind.

The paper leans pretty heavily on work by one James Hamilton.

《Researchers recognize that they do not know the true function and seem to treat, usually implicitly, their results as a good-enough approximation. But there is no basis for the belief that the results of what is run in practice is anything close to the underlying phenomenon, even if there is an underlying phenomenon. This just seems to be wishful thinking. Most regression analysis research doesn’t even pay lip service to theoretical regularities. But you can’t just regress anything you want and expect the results to approximate reality. And even when researchers take somewhat seriously the need to have an underlying theoretical framework – as they have, at least to some extent, in the examples of studies of earnings, educational achievement, and GNP that I have used to illustrate my argument – they are so far from the conditions necessary for proper specification that one can have no confidence in the validity of the results.》

Why does this quotation from Steven J Klees call this blog to mind?

Why doesn’t the IMF include error bars for past measurements?