17 thoughts on “September Real Median Household Income Estimated”

pgl

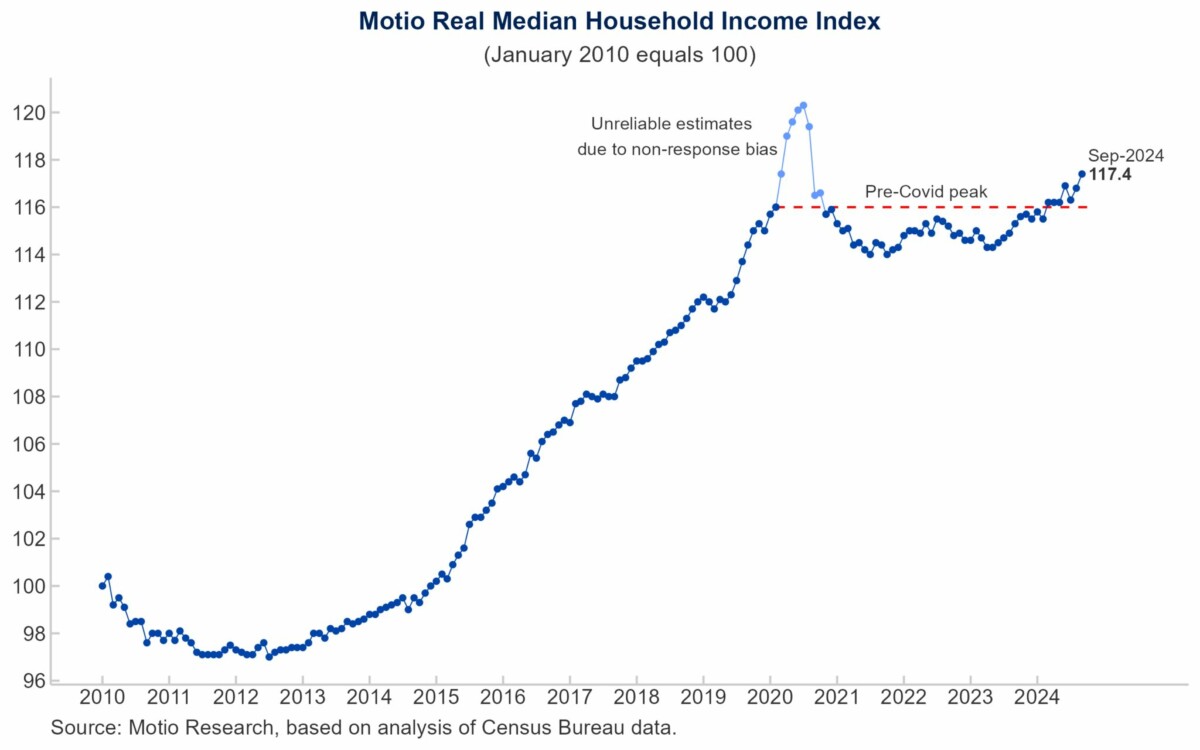

“Above Pre-Covid peak.”

Something the readers of EJ Antoni will never hear. I bet EJ is asking Trump to throw Motio Research in jail.

Moses Herzog

Selling bullshit is a business “And business is good Congrats EJ

pgl

Their charts shows that this series initially dipped a bit during the first months of the Biden Administration but by early 2022 had gone back to where it was a year earlier, And yet lying fake Ph.D. EJ Antoni’s sole contribution to Project 2025 was a claim that real household income had declined by $6000. He never documented how the eff he came up with this figure. Of course little EJ makes a lot of claims which he never bothers to document.

James

To me – our recent bout of inflation primarily caused by the U.S. having a massive supply chain disruption and switch to goods from services and then back to services while many companies took advantage to increase prices while housing remains in short supply (hence proposals by Harris to increase supply) – however – I will go back to view the discussion on inflation that Menzie references in an earlier post.

Stephen Miller thought Trump’s sit down with Bloomberg at the Chicago Economic Club was the greatest economic discussion ever. “Period”. Kevin Drum has a different view backed by the facts!

John Authers, in an effort to explain the emotional salience of inflation to the average Joe/Jo, assigned some Bloomberg data jugglers to create what he calls an “anti-core inflation index”. This is just an index made from food and fuel price components of CPI, twiddle a bit for weightings. I haven’t bothered with weightings because statistical accuracy isn’t really the point and I’m lazy. Here’s a 50/50 food/fuel index along with core CPI:

The point made by the picture isn’t profound to anyone who regularly reads this blog. Food and fuel prices rose much more during the Covid inflation spike than did core prices. We buy food and fuel more often than most other things, and count them as necessities, so leaving them out does miss some of our daily experience.

Among the reasons for excluding food and fuel prices is that they are traditionally more volatile than other prices, and so obscure underlying price trends. That’s certainly true during the Covid spike and also in earlier periods, though take a look at 2017 through till just after the recession – pretty calm.

I don’t think this is the entire story of the recent disparity between public perception of inflation and measured inflation. Price levels are up, straining budgets, and that really matters. But regularly seeing egg prices noticeably higher than the last time you bought them, regularly seeing a $135 basket of groceries that you remember costing just $100, makes for a frequent reminder of the prices that rose most.

The good news, as shown above, is that budgets are now less strained, but the reminders are still there.

joseph

The Chicago Economic Club describes itself on their web site:

“The Economic Club of Chicago membership is a curated group of business and civic leaders” Curated? I think they mean “rich”.

” The Club spotlights thought leaders, with varying perspectives” By varying perspectives they mean all the way from multi-millionaires to multi-billionaires. That’s three orders of magnitude!

“They guide us to deliver the most timely, relevant programming and member engagement options – targeted squarely at our c-suite membership.” So they get right to the point — their membership is curated rich C-suite folks — with varying perspectives, to be sure.

pgl

You would think Trump would do well there but even these richy riches saw threw Trump’s BS!

pgl

Another episode of Uncle Tom Byron Donalds lying on behalf of his master Donald Trump:

Fact check: Did Black wages in the US rise ‘massively’ under Donald Trump?

“The big stat — and this happened during the first Trump administration, nobody likes to talk about it: Wages adjusted for inflation were massively up under Donald Trump for Black men, for Black families, [and] for all Americans,” Donalds said on October 13 on the CNN programme State of the Union. “The wage gap that Democrats love to lecture about — the wage gap in 2019 was actually shrinking under Donald Trump’s administration, his economic policies, his energy policies, and his regulatory policies.” Wages for Black Americans and Black men did rise under Trump, but Donalds ignored that they rose three times faster under Trump’s successor, President Joe Biden, even after adjusting for a period of 40-year-high inflation on Biden’s watch. Rather than narrowing under Trump, the Black-white wage gap widened. “I can’t find any way that suggests that [Donalds] is right,” said Douglas Holtz-Eakin, president of the American Action Forum, a centre-right think tank. “No economist is pointing to this.” Donalds’s office did not respond to an inquiry for this article.

The story continues with the facts that Uncle Tom distorted. Uncle Tom loves to talk as if he is some big bold person but it seems he ducked the person who put together this discussion.

Macroduck

Remember when a well-regarded Republican economist was somebody like Holtz-Eakin? Thank goodness we have the likes of Kudlow to set the record straight.

pgl

Add to Kudlow the likes of Laffer, Moore, and of course EJ Antoni!

pgl

Trump wants Helene victims to fear and doubt FEMA. Their experience is contradicting him

The lies people were told by Trump et. alia versus the reality on the ground. FEMA is doing its job even as Trump is desperately trying to undermine it.

Steven Kopits

This is a very interesting graph. It suggests a prolonged downturn subsequent to the covid pandemic. Unlike ordinary downturns, however, it was accompanied by high inflation and soaring assets prices. So again, recession v suppression.

The straight-forward interpretation, it seems to me, is not one of a pending downturn, but rather an incipient recovery which started in 2023, with median income reaching new highs in the last half year or so. On the face of it, therefore, we might expect a stretch similar to that of 2015-2019, that is, of basically solid secular growth for the next several years. However, this will be occurring paradoxically in the context of normalizing inflation and asset prices, thus retracing the distortions of fiscal and monetary policy, as well as from supply chain disruptions, during and following the pandemic.

I had earlier added an analysis of construction, WIP and completed new homes. New private home starts are all but normal, coming in around 110,000 in the last reporting month. Normal is about 100,000, so new starts are perhaps 10% higher than normal. From 2004-2006, however, new starts averaged 162,000 / month, thus creating a massive inventory overhang. There does not appear to be a need to massively scale back new home construction prospectively.

We are seeing, however, that completions are outpacing starts by cc 40,000 / month; that is, supply bottlenecks are resolving, and they should be fully resolved by latest Q1 2026, basically during the course of 2025. This implies the completion of an additional 400,000 new homes above normal which the market must absorb in 2025, with that 400k representing about 20 days of inventory. That’s enough to depress prices, but unlikely to result in some catastrophic meltdown, it seems to me.

In any event, the Motio graph above suggests we are exiting, not entering, a recession.

One can have some sympathy for Antoni here. Ordinarily, falling asset prices are harbingers of recession, but in this case, they are merely signs of normalization. Once again, we are faced with the suppression v recession issue. The Motio graph speaks to recovery after four pretty dismal years in terms of median income.

Given that, what is the next challenge? I think Lindsay Jacobs lays it out quite clearly in the Econbrowser post but a few before this one. I think Kamala Harris (I am assuming she will win) really faces a rebalancing of the budget, and key to that is transfer payments and other support, principally to seniors. I think that could be packaged as some combination of increased corporate taxes and spending placed on a lower trajectory. I think it just as well that she is avoiding making too many promises.

So once again, “suppression” is just something you made up. It’s a vanity project for you, annoying for everybody else.

Do you really have nothing to add to the discussion?

Macroduck

Social Security is on its own budget. The Treasury budget is a different issue, expecting that SS invests its surplus in Treasury debt.

If by “corporate taxes” you mean a FICA increase for employers, better to say that. If by “spending cuts” you mean reduced benefits, say that. If not, you’ve lost the thread pretty completely.

pgl

Macroduck has already called out your “suppression” BS.

‘The straight-forward interpretation, it seems to me, is not one of a pending downturn, but rather an incipient recovery which started in 2023’

Still trying to slip in your trash about a 2022 recession it seems. Dude – you are one worthless troll. Go away,

pgl

“I think Lindsay Jacobs lays it out quite clearly”.

He did but based on what you wrote there – you had no clue what he said!

“Above Pre-Covid peak.”

Something the readers of EJ Antoni will never hear. I bet EJ is asking Trump to throw Motio Research in jail.

Selling bullshit is a business “And business is good Congrats EJ

Their charts shows that this series initially dipped a bit during the first months of the Biden Administration but by early 2022 had gone back to where it was a year earlier, And yet lying fake Ph.D. EJ Antoni’s sole contribution to Project 2025 was a claim that real household income had declined by $6000. He never documented how the eff he came up with this figure. Of course little EJ makes a lot of claims which he never bothers to document.

To me – our recent bout of inflation primarily caused by the U.S. having a massive supply chain disruption and switch to goods from services and then back to services while many companies took advantage to increase prices while housing remains in short supply (hence proposals by Harris to increase supply) – however – I will go back to view the discussion on inflation that Menzie references in an earlier post.

I don’t think we should just pass over Trump’s increasingly bizarre and unhinged behavior as just funny – clearly Trump should be in long-term care with supervision. Standing on stage and swaying to music for almost 40 minutes until his sycophants finally lead him off as audience has already left – https://www.msn.com/en-us/news/other/donald-trump-sways-to-music-for-39-minutes-at-bizarre-pa-town-hall-who-the-hell-wants-to-hear-questions-right/ar-AA1sjTKJ

The legacy/corporate media needs to be shouting Trump can not/should not be the President/Commander-in-Chief. As Trump’s former Chair of the Joint Chiefs of Staff General Mark Milley has said, Trump is a “fascist to the core” and “the most dangerous person to this country.” https://www.msn.com/en-us/news/other/i-know-mark-milley-we-should-take-his-trump-warning-seriously/ar-AA1sjRQ1

Stephen Miller thought Trump’s sit down with Bloomberg at the Chicago Economic Club was the greatest economic discussion ever. “Period”. Kevin Drum has a different view backed by the facts!

Notes on Trump’s Bloomberg interview

https://jabberwocking.com/notes-on-trumps-bloomberg-interview/

John Authers, in an effort to explain the emotional salience of inflation to the average Joe/Jo, assigned some Bloomberg data jugglers to create what he calls an “anti-core inflation index”. This is just an index made from food and fuel price components of CPI, twiddle a bit for weightings. I haven’t bothered with weightings because statistical accuracy isn’t really the point and I’m lazy. Here’s a 50/50 food/fuel index along with core CPI:

https://fred.stlouisfed.org/graph/?g=1w7M0

The point made by the picture isn’t profound to anyone who regularly reads this blog. Food and fuel prices rose much more during the Covid inflation spike than did core prices. We buy food and fuel more often than most other things, and count them as necessities, so leaving them out does miss some of our daily experience.

Among the reasons for excluding food and fuel prices is that they are traditionally more volatile than other prices, and so obscure underlying price trends. That’s certainly true during the Covid spike and also in earlier periods, though take a look at 2017 through till just after the recession – pretty calm.

I don’t think this is the entire story of the recent disparity between public perception of inflation and measured inflation. Price levels are up, straining budgets, and that really matters. But regularly seeing egg prices noticeably higher than the last time you bought them, regularly seeing a $135 basket of groceries that you remember costing just $100, makes for a frequent reminder of the prices that rose most.

The good news, as shown above, is that budgets are now less strained, but the reminders are still there.

The Chicago Economic Club describes itself on their web site:

“The Economic Club of Chicago membership is a curated group of business and civic leaders” Curated? I think they mean “rich”.

” The Club spotlights thought leaders, with varying perspectives” By varying perspectives they mean all the way from multi-millionaires to multi-billionaires. That’s three orders of magnitude!

“They guide us to deliver the most timely, relevant programming and member engagement options – targeted squarely at our c-suite membership.” So they get right to the point — their membership is curated rich C-suite folks — with varying perspectives, to be sure.

You would think Trump would do well there but even these richy riches saw threw Trump’s BS!

Another episode of Uncle Tom Byron Donalds lying on behalf of his master Donald Trump:

https://www.msn.com/en-us/news/world/fact-check-did-black-wages-in-the-us-rise-massively-under-donald-trump/ar-AA1snxfd?ocid=msedgdhp&pc=U531&cvid=7f0474852df94f92862fbd6ccfed630c&ei=12

Fact check: Did Black wages in the US rise ‘massively’ under Donald Trump?

“The big stat — and this happened during the first Trump administration, nobody likes to talk about it: Wages adjusted for inflation were massively up under Donald Trump for Black men, for Black families, [and] for all Americans,” Donalds said on October 13 on the CNN programme State of the Union. “The wage gap that Democrats love to lecture about — the wage gap in 2019 was actually shrinking under Donald Trump’s administration, his economic policies, his energy policies, and his regulatory policies.” Wages for Black Americans and Black men did rise under Trump, but Donalds ignored that they rose three times faster under Trump’s successor, President Joe Biden, even after adjusting for a period of 40-year-high inflation on Biden’s watch. Rather than narrowing under Trump, the Black-white wage gap widened. “I can’t find any way that suggests that [Donalds] is right,” said Douglas Holtz-Eakin, president of the American Action Forum, a centre-right think tank. “No economist is pointing to this.” Donalds’s office did not respond to an inquiry for this article.

The story continues with the facts that Uncle Tom distorted. Uncle Tom loves to talk as if he is some big bold person but it seems he ducked the person who put together this discussion.

Remember when a well-regarded Republican economist was somebody like Holtz-Eakin? Thank goodness we have the likes of Kudlow to set the record straight.

Add to Kudlow the likes of Laffer, Moore, and of course EJ Antoni!

Trump wants Helene victims to fear and doubt FEMA. Their experience is contradicting him

https://www.msn.com/en-us/news/us/abcarian-trump-wants-helene-victims-to-fear-and-doubt-fema-their-experience-is-contradicting-him/ar-AA1smw1q?ocid=msedgdhp&pc=U531&cvid=d239f0c840564543bfe4b6b7a599f15a&ei=18

The lies people were told by Trump et. alia versus the reality on the ground. FEMA is doing its job even as Trump is desperately trying to undermine it.

This is a very interesting graph. It suggests a prolonged downturn subsequent to the covid pandemic. Unlike ordinary downturns, however, it was accompanied by high inflation and soaring assets prices. So again, recession v suppression.

The straight-forward interpretation, it seems to me, is not one of a pending downturn, but rather an incipient recovery which started in 2023, with median income reaching new highs in the last half year or so. On the face of it, therefore, we might expect a stretch similar to that of 2015-2019, that is, of basically solid secular growth for the next several years. However, this will be occurring paradoxically in the context of normalizing inflation and asset prices, thus retracing the distortions of fiscal and monetary policy, as well as from supply chain disruptions, during and following the pandemic.

I had earlier added an analysis of construction, WIP and completed new homes. New private home starts are all but normal, coming in around 110,000 in the last reporting month. Normal is about 100,000, so new starts are perhaps 10% higher than normal. From 2004-2006, however, new starts averaged 162,000 / month, thus creating a massive inventory overhang. There does not appear to be a need to massively scale back new home construction prospectively.

We are seeing, however, that completions are outpacing starts by cc 40,000 / month; that is, supply bottlenecks are resolving, and they should be fully resolved by latest Q1 2026, basically during the course of 2025. This implies the completion of an additional 400,000 new homes above normal which the market must absorb in 2025, with that 400k representing about 20 days of inventory. That’s enough to depress prices, but unlikely to result in some catastrophic meltdown, it seems to me.

In any event, the Motio graph above suggests we are exiting, not entering, a recession.

One can have some sympathy for Antoni here. Ordinarily, falling asset prices are harbingers of recession, but in this case, they are merely signs of normalization. Once again, we are faced with the suppression v recession issue. The Motio graph speaks to recovery after four pretty dismal years in terms of median income.

Given that, what is the next challenge? I think Lindsay Jacobs lays it out quite clearly in the Econbrowser post but a few before this one. I think Kamala Harris (I am assuming she will win) really faces a rebalancing of the budget, and key to that is transfer payments and other support, principally to seniors. I think that could be packaged as some combination of increased corporate taxes and spending placed on a lower trajectory. I think it just as well that she is avoiding making too many promises.

https://econbrowser.com/archives/2024/10/guest-contribution-social-security-reform-between-a-cliff-and-a-hard-place

“So again, recession v suppression.”

So once again, “suppression” is just something you made up. It’s a vanity project for you, annoying for everybody else.

Do you really have nothing to add to the discussion?

Social Security is on its own budget. The Treasury budget is a different issue, expecting that SS invests its surplus in Treasury debt.

If by “corporate taxes” you mean a FICA increase for employers, better to say that. If by “spending cuts” you mean reduced benefits, say that. If not, you’ve lost the thread pretty completely.

Macroduck has already called out your “suppression” BS.

‘The straight-forward interpretation, it seems to me, is not one of a pending downturn, but rather an incipient recovery which started in 2023’

Still trying to slip in your trash about a 2022 recession it seems. Dude – you are one worthless troll. Go away,

“I think Lindsay Jacobs lays it out quite clearly”.

He did but based on what you wrote there – you had no clue what he said!