What else would one expect from expectations of expanded budget deficits, higher incipient inflation in the context of a Taylor rule reaction function, when the currency is a safe haven asset?

From Bloomberg:

“We see a good chance of substantial dollar strength through next calendar year and potentially into 2026 as well,” said Helen Given, a foreign-exchange trader at Monex. “A Trump administration changes the calculus on forecasting in a very material way as domestic policy points to a big spending spree and international policy is likely to be quite protectionist.”

…

JPMorgan says the sentiment shock around Trump’s win is enough to boost the greenback, even with no official tariff announcement. While the dollar’s path is unlikely to be a straight line given the lack of visibility about the timing of Trump’s policies, Chandan sees the gauge of the greenback strengthening as much as 7% in coming months. That will send the euro toward parity with the greenback and the yuan nearing 7.40 per dollar.

Globally, this will have severe consequences for Europe (recession says one bank), and for emerging market economies, given that dollar appreciation induces more stress than higher US interest rates.

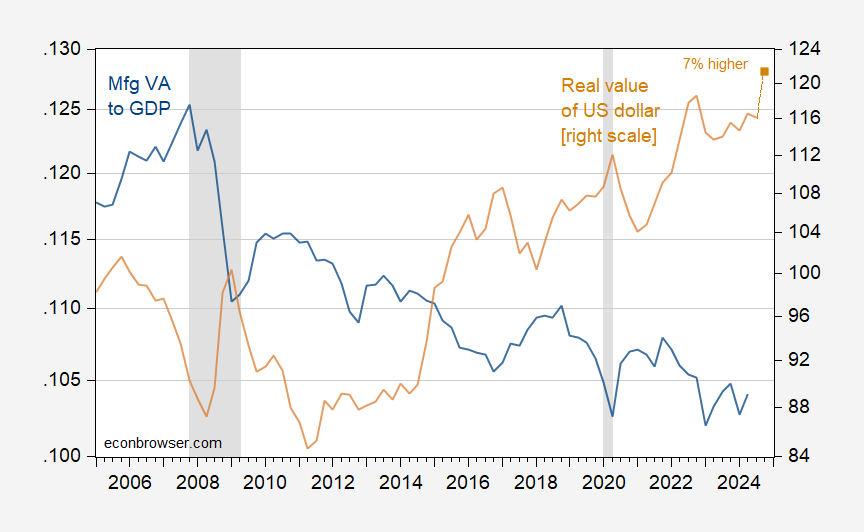

For the US, this is going to make more difficult any attempt to reverse the trend toward lower US activity share in manufacturing (particularly since tariffs will likely make manufacturing overall less competitive even in the absence of dollar appreciation– see Cox and Russ).

Figure 1: Value added in manufacturing to real GDP in Ch.2017$ (blue, left log scale), and real value of US dollar (tan, right log scale), and assuming 7% appreciation from October to December (tan square, right log scale). NBER defined peak-to-trough recession dates shaded gray. Source: BEA, Federal Reserve via FRED, NBER, and author’s calculations.

Visual inspection of the two series suggests a deviation from trend arising from the 2014, 2018 and 2022 appreciation episodes of the dollar.

If we can take history as a guide, implementing a trade war in the likely to be chaotic policy process of the Trump 2.0 era is likely to elevate economic policy uncertainty. This in turn is likely to exacerbate dollar appreciation. From this post:

Suppose you thought a hybrid real interest differential/Taylor fundamentals model worked for explaining the real trade weighted dollar. One might estimate over the 2001Q3-2019Q1 period the following:

rt = –0.81 – 0.74(πUSt – πRoWt) + 1.09(yUSt – yRoWt) + 10.6(iUSt – iRoWt) + 0.20epuGlobalt + ut

Adj-R2 = 0.65, SER = 0.0506, NOBS = 71, DW = 0.44. Bold denotes significance at 5% msl, using HAC robust standard errors.

Where r is the log real trade weighted value of the US dollar against a broad basket of currencies (r increase implies appreciation, 1973M03=0), π is one-year inflation, y is log real GDP, i is the 10 year nominal interest rate, and epuGlobal is the log Economic Policy Uncertainty global index, market GDP weighted from Baker, Bloom and Davis. RoW is the rest-of-the-world, all RoW data from Dallas Fed DGEI. Interest and inflation rates are in decimal form (10% = 0.10).

The coefficients match up roughly with theory — or at least a theory. Higher inflation relative to the rest-of-the-world weakens the dollar, higher relative US GDP and higher US long term interest rates appreciate the dollar. Most significantly, a greater degree of global economic policy uncertainty, as measured by the Baker, Bloom and Davis methodology, strengthens the dollar.