Today, we present a guest post written by David Papell and Ruxandra Prodan-Boul, Professor of Economics at the University of Houston and Economics Lecturer at Stanford University.

The Federal Open Market Committee (FOMC) maintained the target range for the federal funds rate (FFR) at 4.25 – 4.5 percent at its January 2025 meeting. In the Summary of Economic Projections (SEP) following the December 2024 meeting, it projected further decreases with a range for the FFR between 3.75 and 4.0 percent by the end of 2025, between 3.25 and 3.5 percent by the end of 2026, and between 3.0 and 3.25 percent by the end of 2027. Futures markets summarized by the CME FedWatch Tool after the December meeting predicted a slower path of rate cuts with a range for the FFR between 4.0 – 4.25 percent by the end of 2025 and, with additional inflation and unemployment data releases, predicted an even slower path of rate cuts at the time of the January meeting.

We compare the FOMC projections and CME predictions to prescriptions of non-inertial policy rules where the FOMC achieves the desired rate immediately and inertial policy rules where the FOMC smooths rate changes. The post is based on two of our papers. “Policy Rules and Forward Guidance Following the Covid-19 Recession,” published online in the Journal of Financial Stability, and “Alternative Policy Rules and Fed Policies,” which use data from the SEP’s for September 2020 to June 2024 to compare a wide variety of policy rule prescriptions with actual and FOMC projections of the FFR. In this post, we analyze four policy rules that are relevant for the future path of the FFR, update the policy rule prescriptions through December 2027 from the September 2024 SEP, and include futures market predictions.

The Taylor (1993) rule with an unemployment gap is as follows,

where is the level of the short-term federal funds interest rate prescribed by the rule, is the inflation rate, is the 2 percent target level of inflation, is the 4 percent rate of unemployment in the longer run, and is the current unemployment rate. is the neutral real interest rate from the SEP which equals 0.5 percent between September 2020 and December 2023, 0.6 percent in March 2024, 0.8 percent in June 2024, and 0.9 percent in September 2024.

Yellen (2012) analyzed the balanced approach rule where the coefficient on the inflation gap is 0.5 but the coefficient on the unemployment gap is raised to 2.0.

The balanced approach rule received considerable attention following the Great Recession and became the standard policy rule used by the Fed.

These rules are non-inertial because the FFR fully adjusts whenever the target FFR changes. This is not in accord with FOMC practice to smooth rate increases when inflation rises. We specify inertial versions of the rules based on Clarida, Gali, and Gertler (1999),

where is the degree of inertia and is the target level of the federal funds rate prescribed by Equations (1) and (2). We set as in Bernanke, Kiley, and Roberts (2019). equals the rate prescribed by the rule if it is positive and zero if the prescribed rate is negative.

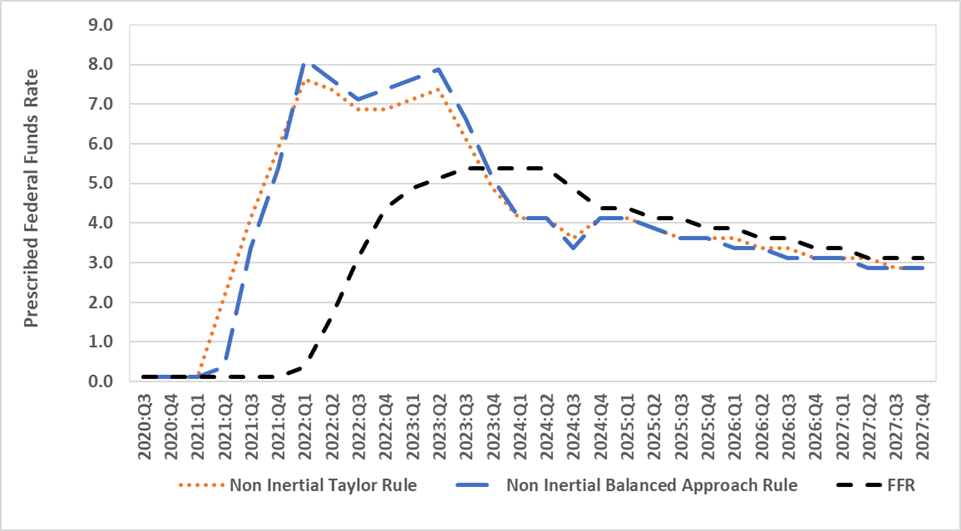

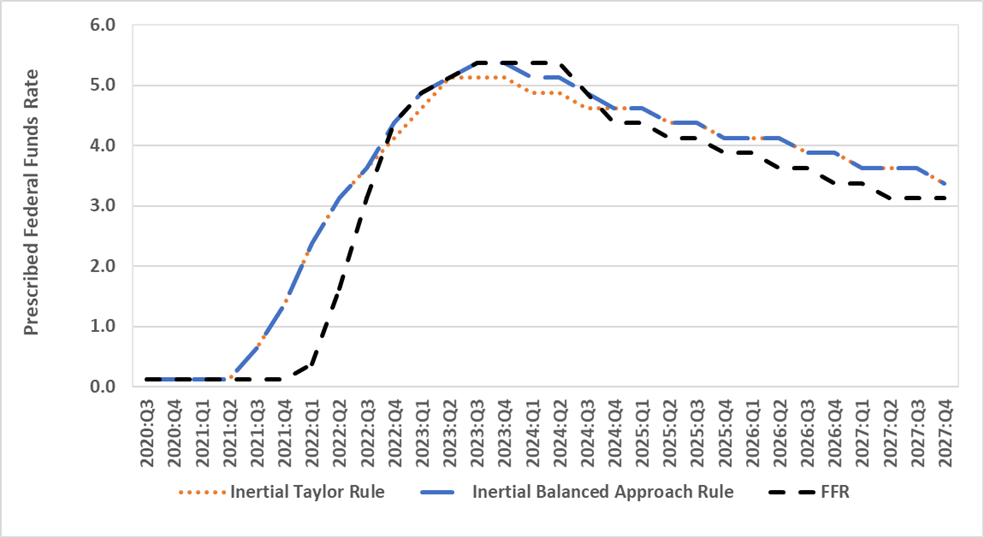

Figure 1 depicts the midpoint for the target range of the FFR for September 2020 to December 2024 and the projected FFR for March 2025 to December 2027 from the December 2024 SEP. Figure 1 also depicts policy rule prescriptions. Between September 2020 and December 2024, we use real-time inflation and unemployment data that was available at the time of the FOMC meetings. Between March 2025 and December 2027, we use inflation and unemployment projections from the December 2024 SEP. The differences in the prescribed FFR’s between the inertial and non-inertial rules are much larger than those between the Taylor and balanced approach rules.

Policy rule prescriptions are reported in Panel A for the non-inertial Taylor and balanced approach rules. They are much higher than the FFR in 2022 and 2023 and are not in accord with the FOMC’s practice of smoothing rate increases when inflation rises. In contrast, while the policy rule prescriptions for 2024 through 2027 from the December 2024 SEP are consistently lower than the FFR projections, the gap narrows considerably starting in 2025. The inertial rules in Panel B prescribe a much smoother path of rate increases in 2021 and 2022 than that adopted by the FOMC. Between December 2022 and September 2024, the policy rule prescriptions are close to the FOMC projections and, starting in December 2024, the prescriptions are higher than the projections.

Figure 1. The Federal Funds Rate and Policy Rule Prescriptions for December 2024

Panel A. Non-Inertial Rules

Panel B. Inertial Rules

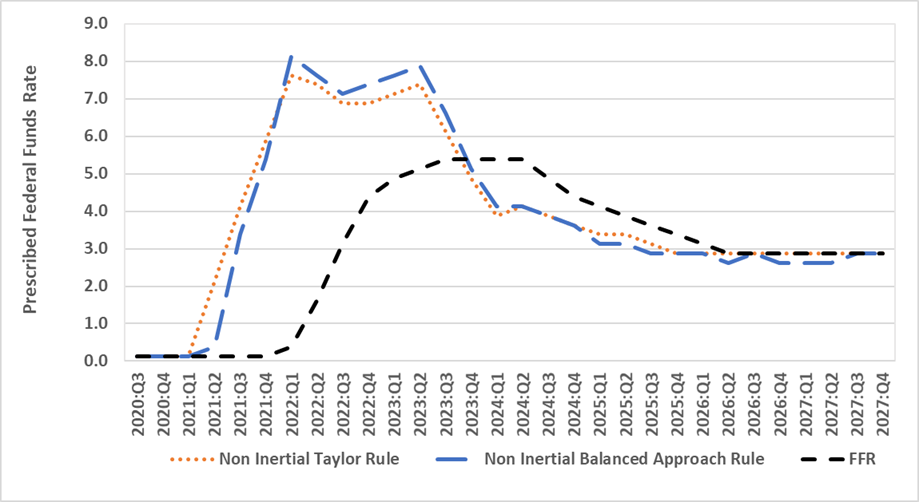

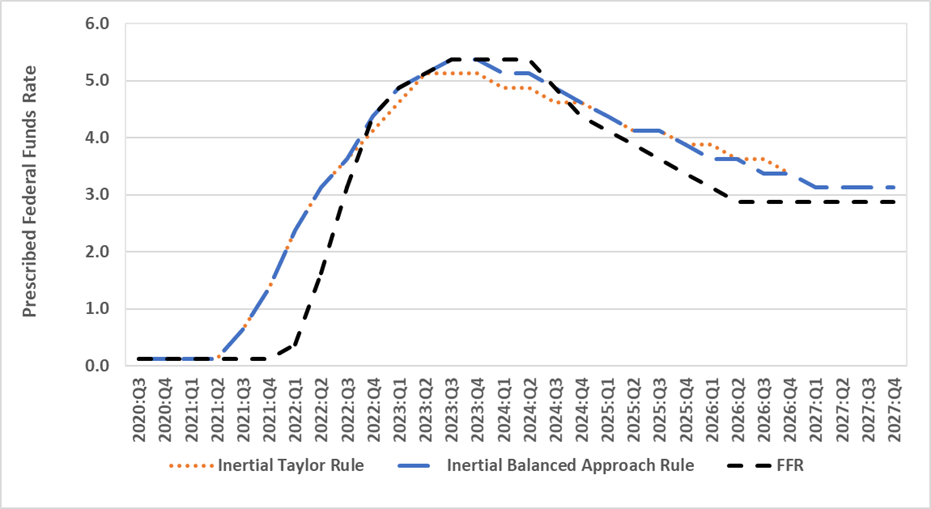

Figure 2 illustrates the federal funds rate projections and policy rule prescriptions from the September 2024 SEP to see how much has changed in the past three months. The speed of rate decreases slowed sharply, with the projected range of the FFR for December 2025 falling from the current 4.25 – 5.0 percent to 3.25 – 3.5 percent in the September SEP and 3.75 – 4.0 percent in the December SEP. Panel A depicts prescriptions from the non-inertial rules. Panel B depicts prescriptions from the inertial rules. The relation between prescriptions and projections is similar in the September and December 2004 SEP’s.

Figure 2. The Federal Funds Rate and Policy Rule Prescriptions for September 2024

Panel A. Non-Inertial Rules

Panel B. Inertial Rules

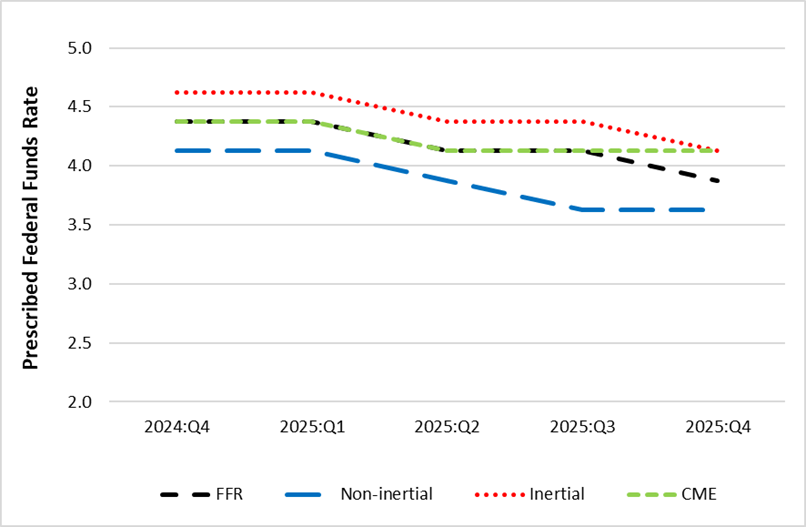

Figure 3 shows the median predictions from futures markets in the CME FedWatch Tool the day following the December 2024 FOMC meeting through the end of the CME prediction horizon in December 2025. The futures markets predict equal decreases in the FFR than the FOMC projections through September 2025 and a sharper decrease in December 2025. The prescriptions for Taylor and balanced approach rules are identical. The prescriptions from the non-inertial policy rules for December 2024 through December 2025 are below the futures market forecasts. For the inertial rules, the prescriptions are above the futures market predictions through September 2025 and equal in December 2025.

Figure 3: The Federal Funds Rate, CME FedWatch Tool and Policy Rule Prescriptions

Taylor and Balanced Approach Rules

This post written by David Papell and Ruxandra Prodan-Boul.