That is a decided shift from the last four years. Like the U.S. economy, U.S. equities had out-performed the rest of the world over the last few years.

Aside from the obvious problem for the U.S. highlighted in the sharp rise in policy uncertainty, Europe and China are on course for fiscal and monetary expansion. The U.S. appears to be on course for fiscal expansion, but with a low (negative?) multiplier and damaging effects on employment. The U.S. is also in the unpleasant situation of maybe a recession, or alternatively no further rate cuts. There’s obvious middle ground, but the economic outlook is a bit of a mess. Hard to know where to invest when fundamentals are so unclear.

Meanwhile, Challenger reports more job cuts last month than in any February since 2009 and the highest for any month since July 2020:

Those were two terrible months. Announcements don’t need represent cuts in he same month. The announcement of 172,017 job cuts doesn’t mean a goose egg from BLS tomorrow, but it certainly points to a weak Q1/H1 pace of net job creation.

Challenger reports government led in job-cut announcements: “Challenger tracked 62,242 announced job cuts by the Federal Government from 17 different agencies last month. So far this year, the Government has cut 62,530, an increase of 41,311% from the 151 cuts announced through February 2024.”

Challenger excluded from it’s count the 200,000 firings of probationary workers which had been overturned by the courts.

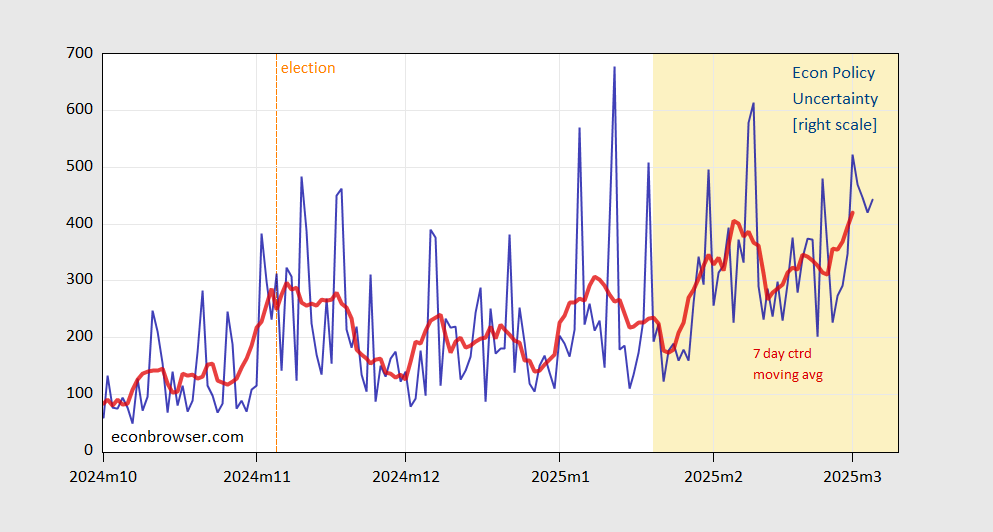

When policy is bound by law, it is more certain: there are limits to the possible change in policy without a change in law. Law changes slowly.

Policy is now being made without reference to law. Courts provide only a partial bulwark against unlawful policy. Policy uncertainty is high.

On a related point, U.S. equities are underperforming major overseas markets so far this year:

https://www.moneycontrol.com/markets/global-indices/

That is a decided shift from the last four years. Like the U.S. economy, U.S. equities had out-performed the rest of the world over the last few years.

Aside from the obvious problem for the U.S. highlighted in the sharp rise in policy uncertainty, Europe and China are on course for fiscal and monetary expansion. The U.S. appears to be on course for fiscal expansion, but with a low (negative?) multiplier and damaging effects on employment. The U.S. is also in the unpleasant situation of maybe a recession, or alternatively no further rate cuts. There’s obvious middle ground, but the economic outlook is a bit of a mess. Hard to know where to invest when fundamentals are so unclear.

Meanwhile, Challenger reports more job cuts last month than in any February since 2009 and the highest for any month since July 2020:

https://www.challengergray.com/blog/job-cuts-surge-on-doge-actions-retail-woes-highest-monthly-total-since-july-2020/

Those were two terrible months. Announcements don’t need represent cuts in he same month. The announcement of 172,017 job cuts doesn’t mean a goose egg from BLS tomorrow, but it certainly points to a weak Q1/H1 pace of net job creation.

Challenger reports government led in job-cut announcements: “Challenger tracked 62,242 announced job cuts by the Federal Government from 17 different agencies last month. So far this year, the Government has cut 62,530, an increase of 41,311% from the 151 cuts announced through February 2024.”

Challenger excluded from it’s count the 200,000 firings of probationary workers which had been overturned by the courts.