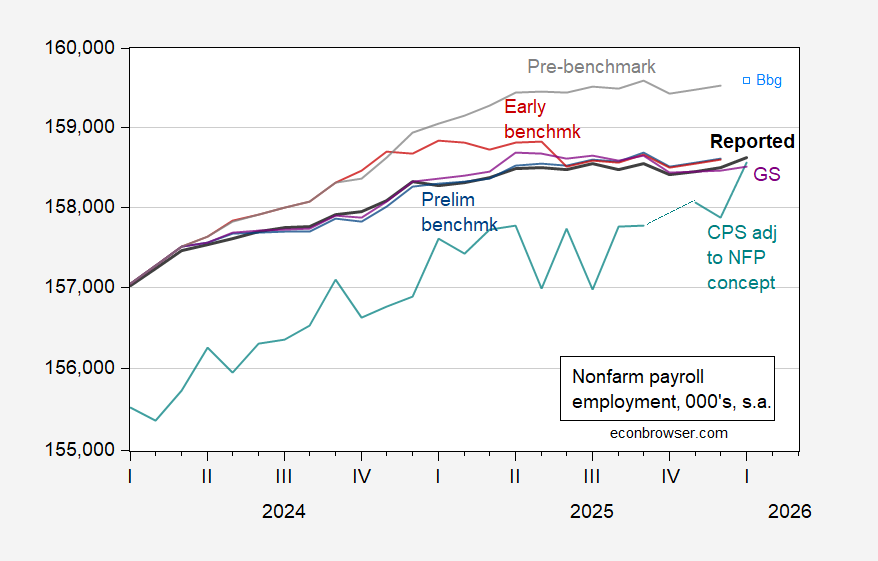

From today’s release, +133K v +66K Bloomberg consensus on NFP:

Figure 1: Reported (post-benchmark) nonfarm payroll employment (bold black), pre-benchmark NFP (gray), implied preliminary benchmark (blue), implied preliminary benchmark (red), implied Goldman Sachs (purple), CPS series adjusted to NFP concept (teal), all in 000’s, s.a. Source: BLS, BLS via FRED, Philadelphia Fed, Goldman Sachs, and author’s calculations.

The upside surprise to NFP in this graph does not alter the basic view of a slowdown in employment growth. It’s also important to keep in mind that the 1st-3rd mean absolute revision in 2024 was 48K. The +133K vs. +66K consensus constitutes a 1.5 MAE miss.

Nonetheless, the picture that’s painted is one very similar to that indicated by the implied preliminary benchmark (wedge in -911K for 2024M04-25M03, reported changes thereafter). The widening gap between output measures and employment measures remains.

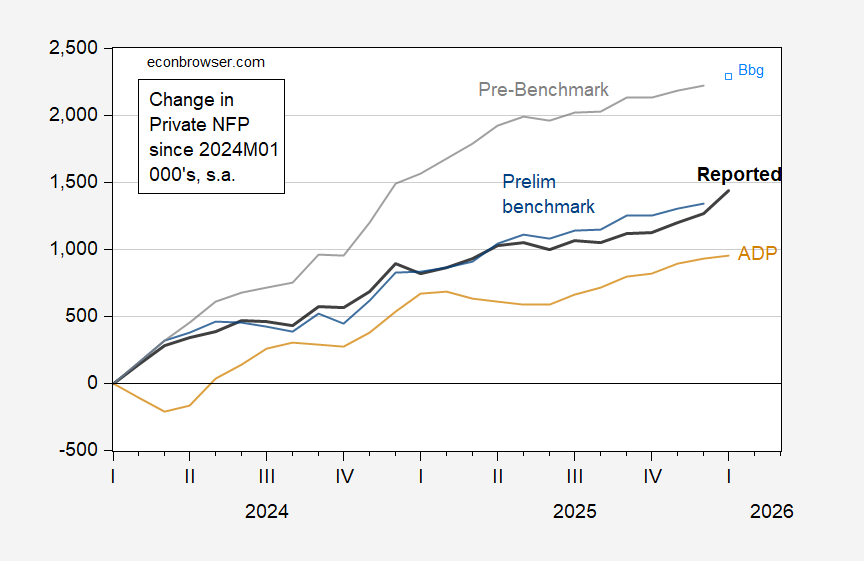

For private NFP employment, we have a check with ADP data. Here’s cumulative change from 2024M01:

Figure 2: Change since 2024M01 in reported (post-benchmark) private nonfarm payroll employment (bold black), pre-benchmark NFP (gray), implied preliminary benchmark (blue), implied preliminary benchmark (red), ADP (light brown, all in 000’s, s.a. Source: BLS, BLS via FRED, ADP and author’s calculations.

It’s interesting that the ADP series did not show a comparable increase in private employment.

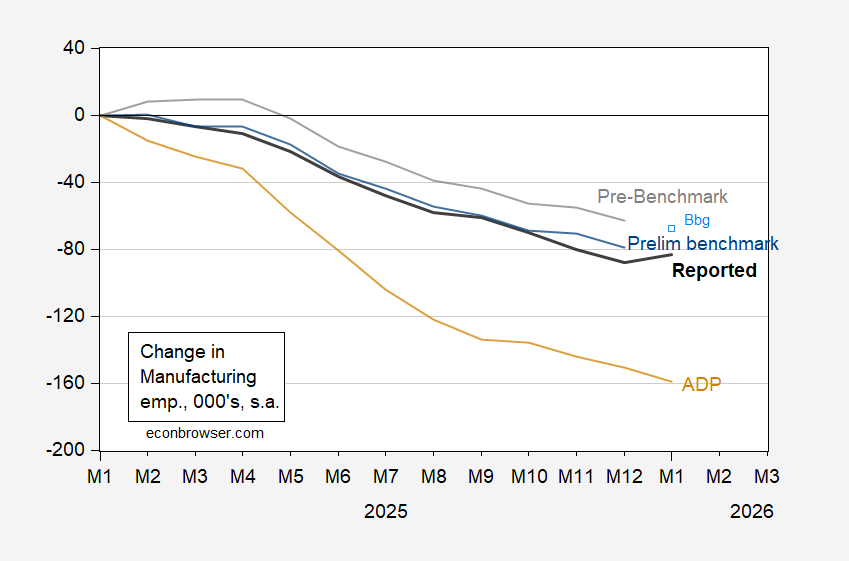

Finally, manufacturing registered an increase (+5K vs. -5K consensus), which however did not change the trajectory overall trajectory since 2025M01. The increase also did not manifest in the ADP series, which has trended down faster than the post-benchmark BLS series.

Figure 3: Change since 2025M01 in reported (post-benchmark) private nonfarm payroll employment (bold black), pre-benchmark NFP (gray), implied preliminary benchmark (blue), implied preliminary benchmark (red), ADP (light brown, all in 000’s, s.a. Source: BLS, BLS via FRED, ADP and author’s calculations.

Either way, manufacturing employment has not rebounded, and the drop accelerated post-“Liberation Day”.

We have been instructed by our racist overlords that the only important measures of employment are those for native-born workers. Oops:

https://fred.stlouisfed.org/graph/?g=1RCkB

Native-born unemployment is trending higher, while the y/y* gains in emoyment are slipping away.

*This series is not seasonally adjusted, so year-over-year comparisons are the way to go.

Shutdown recovery, nothing more or less. 100000 of the jobs were directly related to shutdown spending. Even the 5000 manufacturing jobs were a lag. Next month won’t be so kind.

Healthcare is shutdown related?