Due to the Federal government shutdown, the employment release is going to be delayed. Here are NBER business cycle indicators, including the latest monthly GDP, that we have now:

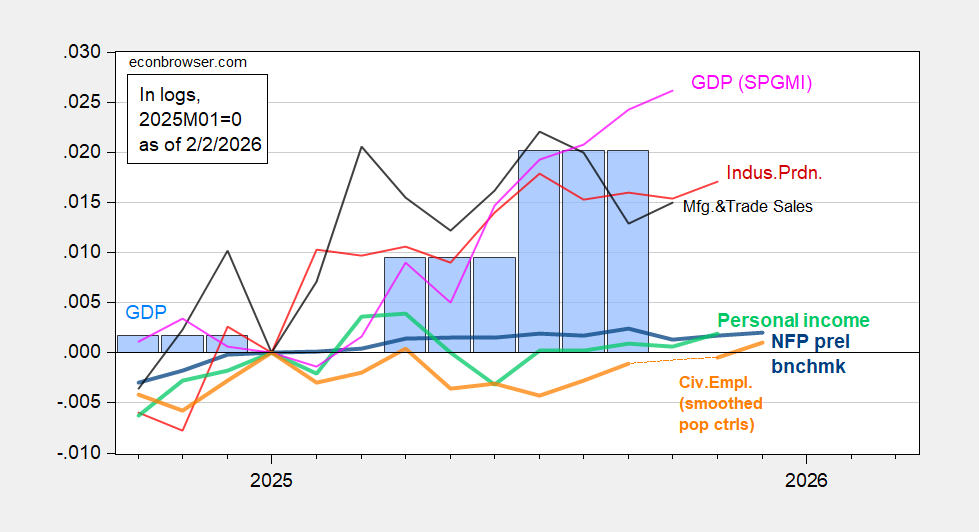

Figure 1: Implied NFP preliminary benchmark revision (bold blue), civilian employment with smoothed population controls (bold orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), and monthly GDP in Ch.2017$ (pink),GDP (blue bars), all log normalized to 2025M01=0. Source: BLS, ADP, via FRED, Federal Reserve, BEA 2025Q3 updated release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (2/2/2026 release), and author’s calculations.

Output measures are rising smartly, or remain above January levels. However, the key measures followed by the NBER — personal income and employment — all remain mired at near January levels.

Here are some alternative indicators:

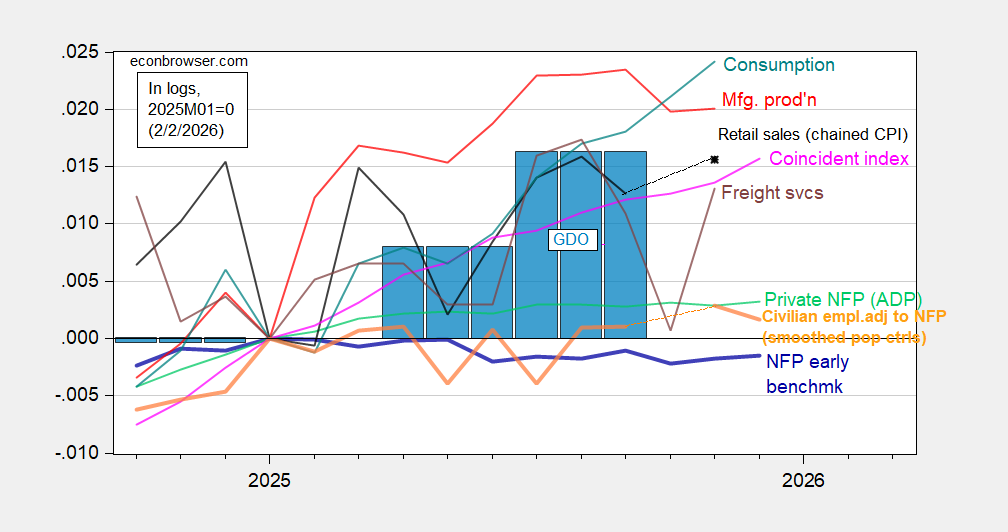

Figure 2: Implied Nonfarm Payroll early benchmark (NFP) (bold blue), civilian employment adjusted to NFP concept, smoothed population controls (bold orange), manufacturing production (red), consumption (light blue), real retail sales (black), freight services index (brown), and coincident index (pink), GDO (blue bars), all log normalized to 2025M01=0. Source: Philadelphia Fed [1], Philadelphia Fed [2], Federal Reserve, BTS via FRED, BEA 2025Q3 updated release, and author’s calculations.

Once again, employment series remain flattish through December even as GDO is up, and consumer spending rises through November. November consumption is 2.5% above January levels. (Bloomberg consensus for ADP private NFP in January is only +48K.)

In other words, the dichotomy between aggregate indicators and the labor market measures remains, in both sets of indicators.

Off topic – TACO Tuesday:

https://www.cnbc.com/2026/02/03/trump-us-india-trade-deal-europe-india-deal-compared.html

The Mad King has announced that the U.S. and India has reached a trade agreement. Big cut in U.S. tariffs and India will no longer buy Russian oil. No details have been released that I can find, possibly because there are none.

I have a hard time understanding why Modi would agree to stop buying Russian oil now in return for lower tariffs when the imposition of steep tariffs didn’t stop him from buying Russian oil earlier. Could be, but it seems odd, even for big tariff cut. Maybe the Venezuelan oil he gets is at a massive discount? FX markets seem to see it as a win for India.

Anyhow, the general response from talking heads is that the trade deal between the EU and India showed the Mad King’s all-stick-no-carrot approach to be a failure; the U.S. just gets left behind. So TACO.

Could be bad for Russia if it’s true. Can India refine Venezuelan crude?

Russia says they haven’t been notified of an end to Indian oil purchases:

https://www.republicworld.com/world-news/russia-keen-to-deepen-ties-with-india-no-signal-on-halting-oil-purchases-kremlin

Of course, they would say that.

Russia’s share of Indian oil exports have been falling since November; western efforts to curb Russian tanker traffic and penalties against India have both been cited in the press as reasons for the decline. OPEC’s effort to remain relevant by pumping oil into a glut probably hurt Russia, too.

India’s interest in Russian oil isn’t limited to cheap imported oil; India is heavily invested in Russian oil production. Not sure how that figures into this “end” to imports of Russian oil.

This is all a sideshow for the oil market. Constant change in tensions betwen the U.S. and Iran have prices bouncing around a good bit, mostly higher.

Since US breaks its deals at any time its convenient – its not big deal to say words that Trump likes; then do whatever you want. Russian oil could go to China then from there to India. If Trump finds out India says they didn’t know of it.

We won’t get January jobs data from BLS this week. May not get weekly jobless claims, either. ADP on Wednesday willl, at least briefly, take center stage.

Meanwhile, there’s chit-chat about an increase in layoff announcements. Amazon, Home Depot, and UPS have all made job cut announcements, and talking heads continue to point out that layoffs in the JOLTS report (which didn’t come out today) and weekly claims data don’t rflect big layoffs. Challenger, Grey and Christmas, on the other hand, continues to report big layoffs and slack hiring:

https://www.challengergray.com/blog/category/job-cuts-report/

I’ve heard it suggested that low unemployment insurance rates in some place are making the true pace of job losses in weekly claims data. Here’s overed employment as a share of payroll employment:

https://fred.stlouisfed.org/graph/?g=1RdP4

Coverage is high for a non-recessionary period, low for recession. Curious. Maybe layoffs are concentrated among non-covered workers. Maybe this is a grinding away at the labor market instead of a recessionary disaster – which would be consistent with the slow pace of job gains we’ve seen, consistent with the Powell conjecture. Maybe states are expanding coverage…nah, that ain’t it.

Masking the true pace of layoffs, not making.