The White House receives embargoed BLS (and other) releases before the official release at 8:30am. If memory serves (and is still relevant), this is late afternoon the day before. So (if as before), Trump starts posting to get people to ignore the numbers, be prepared for a disappointing release.

Current consensus is +66K for NFP, +70K for private NFP (Bloomberg).

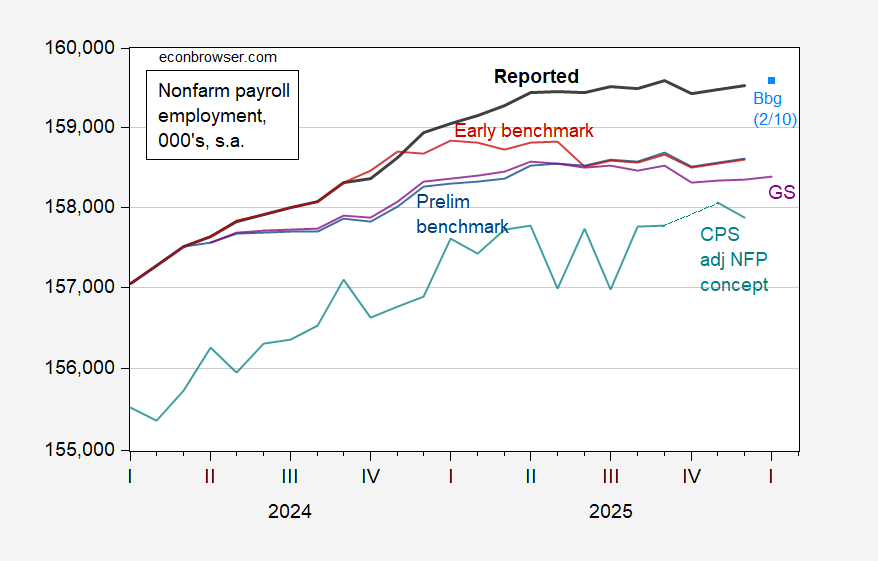

Figure 1: Reported nonfarm payroll employment (bold black), Bloomberg consensus of 2/10 (light blue square), implied preliminary benchmark (blue), early benchmark (red), CPS household employment series adjusted to NFP concept (teal). Goldman Sachs implied (purple), all in 000’s, s.a. Preliminary benchmark data to March 2025, reported changes thereafter. Early benchmark data to June 2025, reported changes thereafter. Goldman Sachs uses midpoint of estimated final benchmark, midpoint of downward adjustment due to revised birth-death model (825, 40, respectively). Source: BLS via FRED, BLS, Philadelphia Fed, Goldman Sachs, and author’s calculations.

The GS downward adjustment to monthly changes post-March is set at 40K (midpoint 30-60, at least that’s my reading), which is smaller than the Powell conjecture of 60K.

Update, 7:40pm CT:

Last month, Trump posted numbers early, at 8:20pm ET, as discussed by Bloomberg.

Peter Navarro is already there:

https://thehill.com/business/5731440-peter-navarro-jobs-report-warning/

“The jobs report’s going to come out tomorrow. We have to revise our expectations down significantly for what a monthly job number should look like,”

Navarro blames immigration for Biden-era job growth and says 50,000 is the right expectation given current ICE behavior. So I’m down for something just over 50k.

Off topic – Menzie recently discussed alternative estimates of China’s GDP:

https://econbrowser.com/archives/2026/02/official-gdp-vs-alternatives-china

As part of that discussion, he wrote:

“Assuming the trade figures are being reported more accurately than domestic ones…, this means that domestic final demand is desperately faltering, and Chinese economic growth is incredibly dependent on exports…”

Apparently, there is official support for Menzie’s view: When a scholar with ties to the government says growth is at risk without “a strong turnaround in total factor productivity and a meaningful expansion in household consumption”, we can assume the public is being prepared for a sizable policy change. This time, the heads-up comes from Zhou Tianyong, former deputy head of the Central Party School’s Institute of International Strategic Studies:

https://www.scmp.com/economy/china-economy/article/3342679/chinas-future-growth-rate-could-drop-25-without-market-reforms-economist

The problem for the CCP is that the macro tools it has used in the past to goose growth don’t work on productivity, nor on household demand. Recent efforts to spur stronger household demand haven’t done diddly.

Command economies work by telling nominally private businesses how to invest and what to produce – supply-side stuff. China is still, in many regards, a command economy. Using credit as the instrument of command is different, but not so different, from old fashioned quotas. Regional governments still face overall growth quotas.

Dousing favored sectors with credit is often inimical to productivity gains. We are regularly treated to news of China’s giant advances in this or that, but China remains a laggard in productivity, ranked 91st in the world by the ILO, behind Botswana, Cuba and Iran:

https://en.wikipedia.org/wiki/List_of_countries_by_labour_productivity

Not sure what plan for growth will be announced next month, but I’m interested to see whether Xi takes a big swing, making fundamental changes to China’s system of economic management, or simply recalibrates the tools already in use. I’m no expert, but I don’t think Xi is ready to relax his grip, and that means he won’t allow fundamental change to economic management.