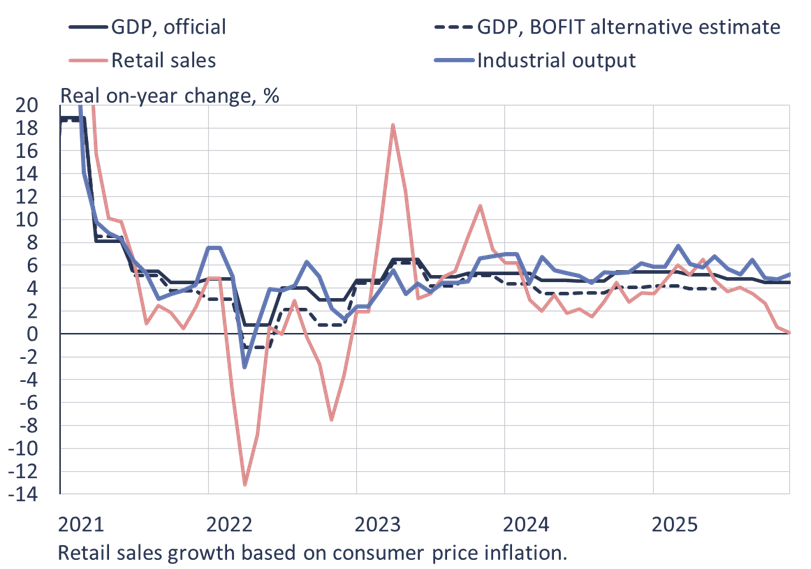

Bank of Finland’s BOFIT concludes:

China’s National Bureau of Statistics (NBS) reports fourth-quarter growth of the Chinese economy slowed to 4.5 % y-o-y. Third-quarter GDP growth last year was still 4.8 % and first-half growth exceeded 5 %. The NBS data also indicate that consumption demand accounted for 2.4 percentage points of 4Q GDP growth, while net exports contributed 1.4 percentage points and investment demand 0.7 percentage point. GDP growth for all of 2025 (5.0 %) unremarkably matched the official “about 5 %” target announced at the National People’s Congress last spring.

BOFIT’s alternative GDP calculation suggests that economic growth for all of 2025 was roughly 1 percentage point below the official figure. The alternative GDP growth estimate for the fourth quarter was 3.3 %. Industrial output growth accelerated slightly in December from previous months to over 5 % y-o-y. For all of 2025, industrial output rose by roughly 6 % y-o-y. Foreign trade, which is closely linked to industrial output, remained strong throughout the year. Net exports clearly supported economic growth for the entire year.

Source: BOFIT, 23 January 2026.

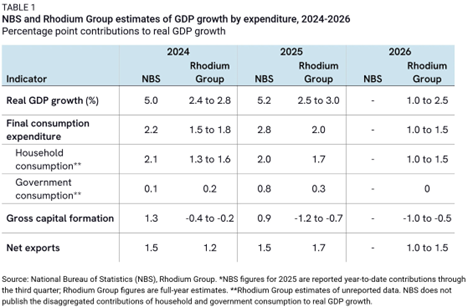

Rhodium Group estimates are less sanguine about growth:

China’s statistics show real GDP growth of 5.2% year to date through the third quarter of 2025, an acceleration from 2024. They will almost certainly claim 5% growth or better for the full year. A year ago, we said China could perform better in 2025, hitting 3 to 4.5% if Beijing prioritized growth after a poor 2024 performance in the mid-2s. But actual 2025 growth fell short of 3% again, with a strong first half and then a badly down-sloping second half.

Here’s Rhodium Group’s (December 22, 2025) assessment:

Source: Rosen et al. (2025).

One can’t directly compare the NBS results to Rhodium Group’s as the NBS measure is Q3 YTD, and the latter’s is full year. However, it’s clear that Q4 growth would have to be very fast in order to hit the overall 5%.

The authors trace the divergence between reported and actual to the collapse of the residential housing sector, beginning in 2021. In my view, this implies that while Chinese misstatement of growth might have been present before 2021, overstatement has been the case since then.

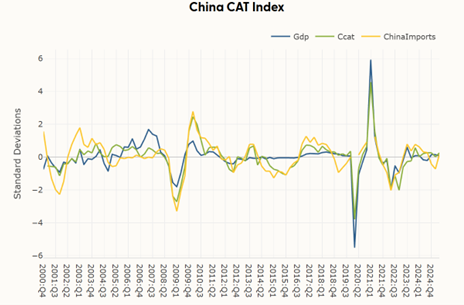

The Fernald-Hsu-Spiegel (2020) China Cyclical Activity Tracker — which provides estimates of deviations from trend — does suggest an official overstatement relative to actual in 2022 (while partner-country imports suggest an overstatement in 2025Q1):

Source: SF Fed CCAT, accessed 2/5/2026.

Assuming the trade figures are being reported more accurately than domestic ones (who knows? lot’s of things are now considered state secrets and reporting on them is considered espionage), this means that domestic final demand is desperately faltering, and Chinese economic growth is incredibly dependent on exports, at exactly the time when protectionist pressures are increasing Europe and the rest of East Asia.

A side note: This fog of data uncertainty, which pervades both private and public sector policymaking, is the natural consequence of political forces forcing the statistical agencies to propagate a given view of the economy. We should be on-guard for further attempts to distort or suppress data in the US, lest we become China-like in this respect.

The National People’s Congress, which kicks off on March 5, will produce the official 2026 growth target. Provincial forecasts already released add up to slower growth for China as a whole:

https://asia.nikkei.com/economy/china-s-provinces-ease-growth-targets-fueling-expectations-of-national-cut

The provincial estimates are part of the formal preparation for the National Congress, so adding up gives a pretty solid guess about the 2026 growth target.

As hinted at in the Nikkei link, debt management is now a big issue in setting growth targets. The higher the growth target imposed by the central government, the more provincial governments, and the banks answerable to provincial governments, will resort to debt expansion, and Chinese debt expansion is already well into diminishing returns. Lowering the growth target is a prudent move.

When high-flying real estate generated tons of money through provincial land sales and tons of growth through new construction, positive feedback paid for everything. (Another name for “positive feedback” in economics is…?) Since the collapse, provincial borrowing has paid for growth, but growth isn’t paying back.

Papering over the cost of adjustment with bad data is simply macro accounting with Chinese Characteristics. Bigger problems are debt, unemployment, cry-cry horses and the “are you dead” app; the longstanding justification for CCP rule is eroding, while Xi is purging the military and stepping up threats to Taiwan. Domestic prudence is accompanied by a leadership cult and foreign adventurism.

Speaking of growth, anybody elsr think the productivity story currently in vogue is a little too easy?

The latest from Jared Bernstein, hardly an apologist for anti-labor policies in general, is in part about productivity bridging the gap between weak job growth and solid output gains.:

https://econjared.substack.com/p/the-media-really-doesnt-know-what

His is a positive story in which productivity is driven by growth.

Also recent, Marketplace radio quotes Courtney Shupert with MacroPolicy Perspectives saying “Part of that [the declining share of wages in national income] is because as industries have become more productive, they need fewer workers,”

This is a pretty common theme in economic chit-chat lately, a response to what otherwise seems a conundrum – how is output growing as well as it is when employment is stagnating?

What neither Bernstein nor Shupert nor most participants in the chit-chat have mentioned is cost shedding. Corporate managers who feel compelled to spend on artificial intelligence have to finance that spending somehow. We know that AI providers are financing their spending with borrowing – lots of borrowing – but AI buyers are left to find their own money, and it seems pretty clear some are cutting spending in other parts of the business. Across private business in general, labor is over half of outlays. And, by the way, there are other sources of rising costs which need to be offset, tariffs foremost among them. So maybe instead of technology driving productivity gains, it is instead stepped up pressure on workers.

I’ve mentioned before that a sharp rise in productivity is often a harbinger of recession. That’s because managers respond to weak demand growth and late-cycle increases in costs by cutting labor costs. We are experiencing a sharp rise in productivity. Both the decline in wages and the relatively high share of profits as a share of national income show the trick is working.

Yeah, history suggests this is unsustainable, but that’s not my point here. My point is that explaining a short-term divergence in labor hours and output by invoking a longer-term process of integrating new technology into production seems pretty glib. Cyclical, late-cycle pressure on workers may be a better explanation than longer-term structural change for short-term developments.

Another issue, one with which I am intimately familiar, is the overhiring of software engineers and data scientists in response to the AI / LLM hype boom sometime after the pandemic began. We (a very, very large retailer) did exactly that, thinking that AI was just about ready to revolutionize a lot of business processes, and we were going to need to have these people on board to make it all work. Unfortunately, several years later, AI is still just about ready to revolutionize a lot of business processes, and, having learned our lesson about hype vs. reality in this area, we have been slowly shedding IT and data science professionals for well over a year now. And we know what we are doing! We’ve won awards for data science stuff! I can only imagine the situation that less tech-savvy firms have found themselves in.

Of course, this won’t account for most of the observed phenomenon, but it surely didn’t help.

lot’s of things …

*lots of things ….

You’re sending too much time around millenials.

One morr thing – JOLTS and jitters.

Instead of the “Mad King” risk-off trade we’ve been seeing this past year, today’s financial market activity looked more like a conventional risk-off trade, with the understanding that jacked-up gold prices mean gold is now a risk asset. Dollar up, Treasuries up, stocks (especially AI) and crypto (bigtime) down. Expectations for Fed policy softened.

Far as I can tell, JOLTS and claims data were the proximate cause of the trade. I can only speculate that surprisingly weak openings numbers for December and a jump in claims were seen as reinforcing weak January ADP hiring data. With Friday’s payroll numbers delayed, ya gotta shed risk for the weekend when you get a hint payrolls will be bad.

Notice that openings for healthcare and social assistance were among the big losers, even though ADP showed healthcare hiring in good shape. Could be we’re seeing early effects of the end to enhanced Obamacare subsidies. Or not.

Information openings had another weak month – thank you AI miracle. Finance openings tanked. There were lesser signs of weakness in several categories.

Hires data, while not jolly, were not terrible the way openings data were, with the notable exception of finance. The heneral upward trend in layoffs persisted, but didn’t go nuts.

I don’t trust openings data since they diverged from hires in the mid-teens, but what happened in December certainly is an attention-getter.