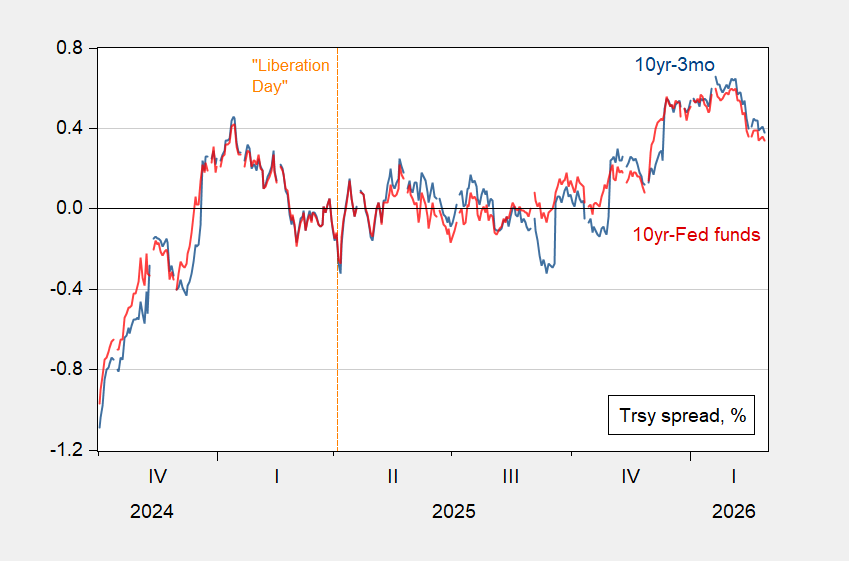

At high frequency, the 10yr-3mo and 10yr-Fed funds spreads are shrinking:

What to think of this? Typically, we decompose the (risk free) Treasury long yield as:

tp is the term premium. However, the default risk on Treasurys have been relatively high over this period.

For comparison, 5 year German CDS are at 7.7. US 5 year CDS were under 10 early in Biden’s term.

If we could adjust for inflation risk (as DKW do, but only through January 31) and default risk, the resulting adjusted term spread might be even smaller. Adjusting for the inflation risk, today’s 10yr-3mo spread would be 25 19 bps instead of 36 30, using the end-January difference.

Speaking of the inflation premium, but only kind of…

We hear a lot about the rise in electricity prices as a result of growing AI demand for electricity. Like most things, it’s more complicated than a single comparison can reveal. For instance, over the 12 months to January, the CPI electricity index has risen just 1.9%, compared to 3.0% for overall CPI and 3.3% for core CPI. What’s to complain about?

Well, for one thing, we’ve been learning that the public is sensitive to price levels, as well as price increases, and the price level for electricity has been on a tear:

https://fred.stlouisfed.org/series/CUSR0000SEHF01#

Electricity is only 2.3% of the CPI expenditure basket, but gasoline is only 2.9%, eggs only about 0.2%, and we know how concerned people can be about those prices.

Electricity prices have historically risen more slowly than overall CPI. Since 1913, the average annual rise in the price of electricity is 1.67%, slightly more than half the 3.14% average pace for overall CPI:

https://www.in2013dollars.com/Electricity/price-inflation

Here is analysis of electrical utilities’ capital requirements which suggests a steady rise in electricity prices just to keep up with rising demand:

https://oilprice.com/Energy/Energy-General/The-Hidden-Math-Behind-Rising-Electricity-Prices.html

This analysis doesn’t extend to an actual forecast of electricity prices, but merely concludes that capital spending projections are too low, so projected revenue needs are too low, so prices have to rise more than projected.

Given the relatively small share of electricity in CPI (and PCE) consumption baskets, this doesn’t strike me as a big problem for monetary policy. Rather, it’s a big problem for particular regions, businesses and households. Lower-income households spend a far greater share of their budget on electricity than do better-off households. Some businesses are electricity-intense, others not so much. And some markets are experiencing much faster price increases for electricity than others.

Oh, and we are electrifying the economy, whether the felon-in-chief likes it or not, and that exacerbates the problem of demand-driven price increases.

it seems to me trump is once again using the government to pick winners and users in the technology front. the assault on anthropic is nothing short of bullying. why should a business be blacklisted because it does not want its technology to be used for illegal purposes? my guess is in the background, trump and musk are playing footsie again. and the stunted growth from aix, gronk, will replace it in the government profile. once again, musk will have access to enormous amounts of private, confidential and classified data. and once again, he will violate the law in parsing that data for his own economic benefit. grifters gonna grift.