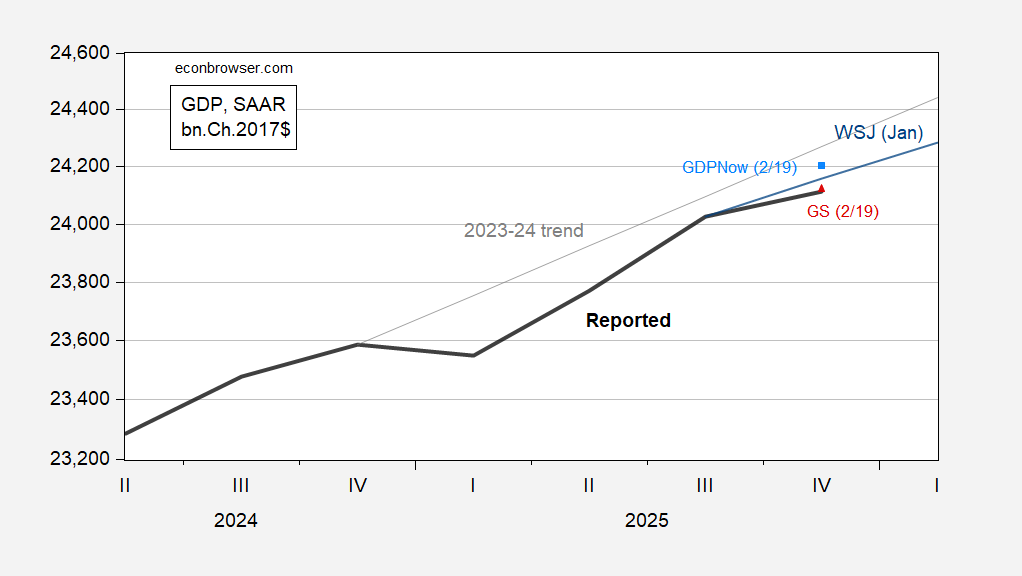

Yesterday, Jim moved the Econbrowser Little Econ Watcher’s countenance to neutral 😐, based primarily on Q3 growth, using the methodology outlined in this post. Remember, there will be two revisions for Q4 growth (before the annual revision, and succeeding revisions). What are some other readings from the Q4 release?

First, GDPNow — as expected — over-nowcasted growth because it couldn’t take into account the government shutdown. On the other hand, the Goldman Sachs tracking estimate, incorporating judgment, was largely on mark.

Figure 1: GDP Q4 advance reported (bold black), GDPNow (sky blue square), Goldman-Sachs (red triangle), WSJ January survey mean (blue), 2023-24 stochastic trend (gray), all in bn.Ch.2017$ SAAR. Source: BEA via FRED, Atlanta Fed (2/19), Goldman Sachs (2/19), WSJ January survey of economists, and author’s calculations.

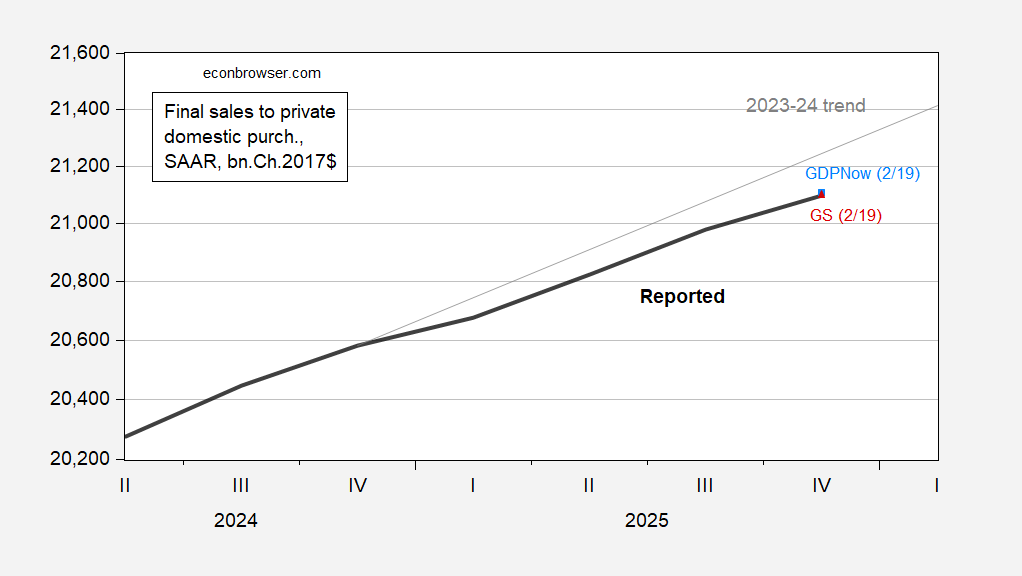

Note that the Little Econ Watcher assessment is based on data through Q3; Q4 evidences a big slowdown (1.4% q/q AR). To the extent this was a “one-off” to be reversed in 2026Q1, one might not want to make an assessment on trajectories solely on GDP. Given the abnormal behavior of external balances (imports, exports) and government spending (record shutdown). I show the trajectory of a proxy for aggregate demand which excludes those two components (technically, final sales to private domestic purchasers, aka “Core GDP”):

Figure 2: Final sales to private domestic purchasers Q4 advance reported (bold black), GDPNow nowcast (sky blue square), Goldman-Sachs (red triangle), ad 2023-24 stochastic trend (gray), all in bn.Ch.2017$ SAAR. Source: BEA via FRED, Atlanta Fed (2/19), Goldman Sachs (2/19), and author’s calculations.

Visually, advance reported q/q AR sales growth of 2.4% seems to have largely have hit the mark, in accord with the view that it’s easier to predict these domestic components. However, growth was below GDPNow’s 2.6% nowcast (but roughly at GS’s). Recession in 2025Q4 seems highly unlikely given what we’ve seen thus far. Nowcasts for 2026Q1 range from 2.7% (NY Fed) to 3.1 (Atlanta Fed).

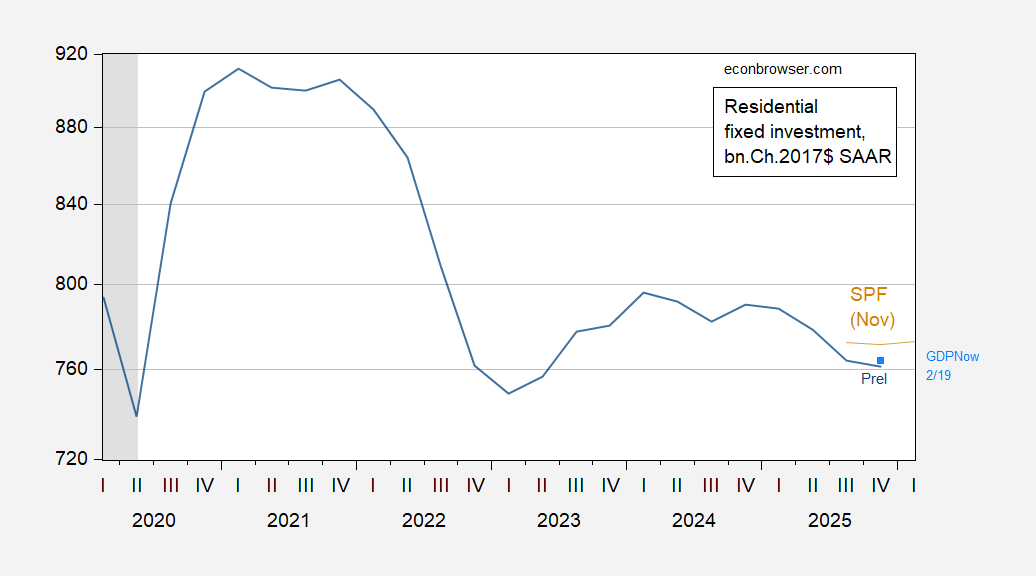

Finally, what about residential investment, discussed in this post? Well, advance numbers undershot GDPNow’s nowcast (and are well below November 2025 Survey of Professional Forecasters forecasts).

Figure 3: Residential Fixed Investment Q4 advance reported (bold black), GDPNow nowcast (sky blue square), November Survey of Professional Forecasters forecast, all in bn.Ch.2017$ SAAR. Source: BEA via FRED, Atlanta Fed (2/19), Goldman Sachs (2/19), and author’s calculations.

Two points:

1. Private residential fixed investment as a share of GDP made a new post-pandemic low in Q4. Further, while the other long leading indicator in the GDP, corporate profits, won’t be reported for at least another month, a good placeholder, proprietors’ income, was, and declined for the third quarter in a row. The below link shows it deflated by the PCE index, but the result even holds nominally:

https://fred.stlouisfed.org/graph/fredgraph.png?g=1Sl3w&height=490

This would suggest a recession could happen at any time.

2. Looking at 4 coincident indicators that the NBER is said to track, 3 of them have been stalled for about the last 6 months. The graph linked to below norms them to 100 as of September. I’ve also included real retail sales, since the reporting on real manufacturing and trade industries sales is lagging so badly:

https://fred.stlouisfed.org/graph/fredgraph.png?g=1Sf0w&height=490

This is the same series YoY:

https://fred.stlouisfed.org/graph/fredgraph.png?g=1Sf0S&height=490

All of them except for industrial production are converging towards 0.

Speaking of the housing market, here is one version of a map that is getting a good bit if attention these days:

https://www.datawrapper.de/_/x4Utg/?v=4

It represents relative price changes in local housing markets since 2022.

Notice the geographic distribution – price gains mostly in the North, price declines in the South. There are exceptions, of course – take a gander at Miami. Until recently, declining prices were rare in major urban areas. Now, fairly common.

Falling prices are dandy if affordability is the only concern, but affordability is decidedly not the only concern. The interaction of debt and deflation is notoriously bad.

Here’s a map of the distribution of underwater mortgages:

https://www.newsweek.com/map-shows-americas-most-underwater-housing-markets-11488118

The correspondence between recent price declines and negative equity isn’t perfect, but if price declines continue, the correspondence will improve with time.

In Florida the primary driver of price declines is the cost of insuring against hurricane damage. Many people simply can no longer afford their homeowner’s insurance premiums.

To my outhouse economist’s eye, this sure seems like 2006. We may not have a 2008 style meltdown, but we are right on the edge. For the sake of a whole lot of people, I hope that’s a wrong impression.

Off topic, sort of – tariffs:

The Mad King has announced 10% tariffs – or is it 15%? – to replace his pet IEEPA tariffs just struck down by the Supreme Court, starting Tuedsay, because there’s nothing impossible about that. I haven’t found any calculation of the revenue effect of that change, but I’m sure the Yale Budget Lab will have one soon. There are, however, a few things we can figure out about other effects.

Any country which had reached a trade “deal” with the Mad King has just learned that his deals aren’t worth spit. Should already have known, but now they do. Tariffs for everybody.

Any firm which had adjusted to the earlier round of tariffs by finding low-tariff suppliers now have to go through the process again. Sand in the gears of commerce. This is particularly bad for smaller firms, which have to spread the cost of adjustment over smaller revenues.

Uncertainty is reinforced. The tariff system, already a product of vanity and whim, is now evidently even more changeable than it had seemed.

We’ll no doubt get an earful at the State of the Union about the evil Court. And the evil Fed. Notice any similarities between the two? And the evil of left-wing radicals and immigrants and about how the Mad King has solved the affordability problem – which is a hoax – and about Iran and federal troops at polling stations and about how the Mad King has done more good in less time than any president before him. And probably about ill-conceived new programs meant to buy votes at the midterm.

Democrats, lots of booing, ease.