Primarily from the production function approach (discussion here).

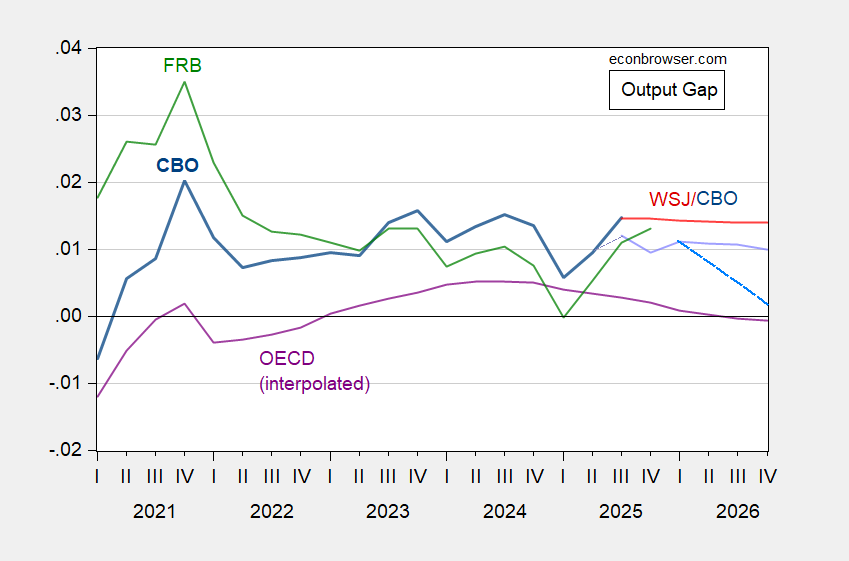

Figure 1: CBO output gap, calculated using latest BEA data and February 2026 estimate of potential GDP (dark blue), projected using February CBO GDP and potential GDP (lilac), CBO GDP omitting fiscal impulse from BBB (sky blue dashed blue), WSJ January survey mean and CBO potential GDP (red), FRB/US output gap (green), OECD December Economic Outlook estimate interpolated from annual data (purple), all as share of potential. Source: BEA 2025Q3 updated release, CBO February 2026 Budget and Economic Outlook, CBO, WSJ January survey, FRB via Atlanta Fed Taylor Rule Utility, OECD December 2024 Economic Outlook, and author’s calculations.

A caveat is worthwhile for the CBO output gap measures. Since GDP measures are revised, the first-release GDP implied output gap may well differ from final vintage (or even second release, as in the case of 2025Q3) implied output gap.

It is interesting to note that both the CBO based and FRB measures of the output gap are in excess of 1%, suggesting that the economy at the aggregate level is doing well. In contrast, the OECD’s forecasted measure of the output gap is 0% for 2026.

The CBO’s assessment of the fiscal stimulus emanating from the 2025 BBB is roughly 0.9 ppts of growth in 2026. In the absence of the BBB, the output gap would decline to about 0.2 ppts of GDP by end-2026. It’s against this backdrop that one might want to consider the correct level of the Fed funds target rate (after all, it’s not the change in GDP, but the output gap, that shows up in the Taylor Rule).

Also worth noting:

https://abovethelaw.com/2026/02/stock-traders-are-no-longer-taking-employment-and-inflation-data-from-the-trump-administration-at-face-value/

Off topic, but relevant – industrial policy:

The U.S. is engaged in two natural experiments in government industrial policy. One is the Mad King’s tariff scheme, the other the CHIPS Act. The tariff experiment is broad in its application, with the stated goal of increasing factory output and employment. The CHIPS Act is narrowly focused, with the stated aim of bringing microchip production, especially the most technologically advanced production, back to the U.S.

How’s that going? Here’s factory employment and output for the period covering both tariff episodes:

https://fred.stlouisfed.org/graph/?g=1S5IP

Both times, factory jobs have declined under tariffs after climbing previously. Both times, the rise in output has slowed after a faster rise prior to tariffs. Only in the latter episodes does recovery from Covid offer any excuse.

Here’s spending on factory construction in the 21st century so far:

https://fred.stlouisfed.org/series/TLMFGCONS

That massive rise earlier in this decade represents the CHIPS Act. Notice that the rise is cooling now under tariffs.

The CHIPS Act succeeded in its goal. Tariffs have not.

For a look at the thinking that went into CHIPS Act implementation, here’s the text of an interview with Mike Schmidt, the director of the CHIPS Act program office, and Todd Fisher, the original CIO of the CHIPS Program Office:

https://www.chinatalk.media/p/how-the-us-won-back-chip-manufacturing

This is careful, step-by-step planning and implementation, with careful consideration of the tradeoffs involved. Not top-down deal-driven buffoonery. Not for the enrichment of cronies.

Notice that the two CHIPS Act guys credit the AI boom with pulling construction of microchip manufacturing forward in time – about a quarter of a century ahead of schedule. Given that there was no advanced microchip production in the U.S. prior to the CHIPS Act, it’s not a stretch to think that the U.S. wouldn’t have captured any of the AI chip manufacturing boom absent the CHIPS Act.

They also suggest ways in which future industrial policy ought tobe approached. Given the success of their endeavor, we should pay attention.