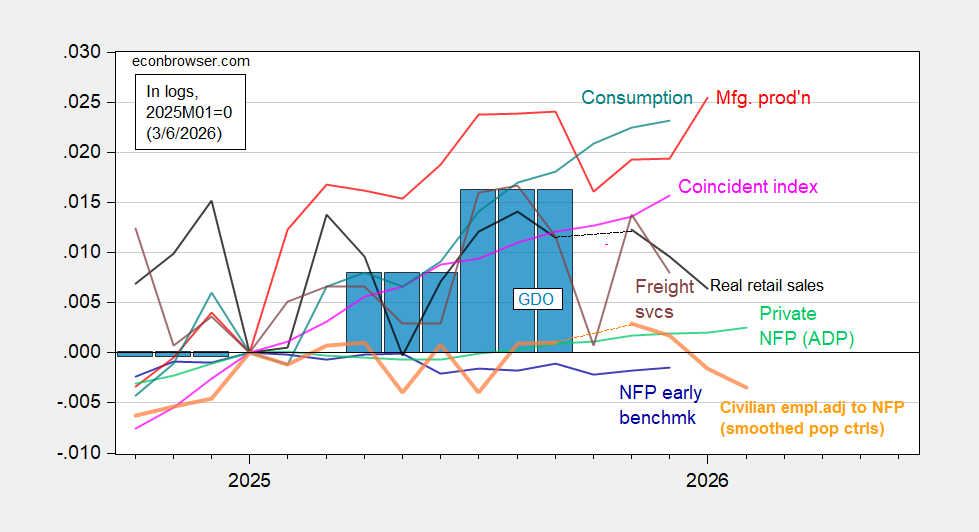

Civilian employment adjusted to NFP concept is diving (after retroactive application of 2026 population controls to January 2026 data), as are real retail sales in January.

Figure 1: Implied Nonfarm Payroll early benchmark (NFP) (blue), civilian employment adjusted to NFP concept, using smoothed population controls (bold orange), manufacturing production (red), private NFP from ADP (light green), real retail sales (black), freight services index (brown), coincident index in Ch.2017$ (pink), and GDO (blue bars), all log normalized to 2021M11=0. Retail sales deflated by CPI. Source: Philadelphia Fed [1], Philadelphia Fed [2], Federal Reserve via FRED, BEA 2025Q4 advance release, and author’s calculations.

The pattern of output measures diverging from employment — also displayed in the set of indicators focused on by the NBER’s Business Cycle Dating Committee (BCDC) — is replicated here. Notable observations: (1) Civilian employment adjusted to NFP concept is now on a pretty clear downswing, now that the 2026 population controls are applied to January’s data; (2) inflation adjusted retail sales are down as well.

Nowcasts have been downshifted as well; GDPNow for Q1 dropped from 3.2% q/q AR yesterday to 2.1% today. NY Fed’s nowcast dropped from 2.4% last Friday to 2.2% today. Goldman Sachs tracking as of today stayed at 3.4%.

From the Hutchins Center’s latest fiscal impact update:

“We expect fiscal policy to add 2 percentage points to GDP growth in the first quarter of 2026. This reflects the reversal of the temporary effects of the government shutdown, which we assume will boost real GDP in the quarter by 1.3 percentage points, as well as the stimulative effects of the OBBBA on both purchases and taxes.”

Not sure how some of these forecasts accommodate the Q1 rebound from the Q4 shutdown, but:

GDPNow + Hutchins = Goldman (almost)

GDPNow + Hutchins was a pretty good forecast for Q4 GDP

Oh, and when it comes to war’s impact on Q1, take wha tever mechanical GDP forecast makes you comfortable and then cogitate over war’s effect on inventories and trade. We produce oil and gas, so may enjoy a bump in exports. Typically, inventories and trade tend to offset each other, but we’re burning through munitions inventories by “exports” to Iran that aren’t reflected in the GDP stats. That’s war-related trade as an add to GDP, war-related inventories as a drag. Get the magnitudes right and you capture war’s impact on Q1 GDP.