Civilian employment adjusted to NFP concept is diving (after retroactive application of 2026 population controls to January 2026 data), as are real retail sales in January.

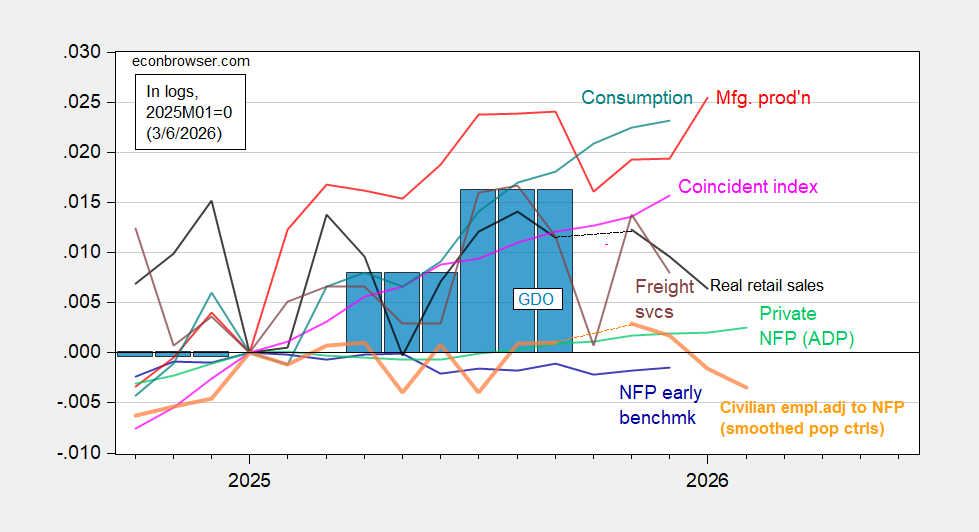

Figure 1: Implied Nonfarm Payroll early benchmark (NFP) (blue), civilian employment adjusted to NFP concept, using smoothed population controls (bold orange), manufacturing production (red), private NFP from ADP (light green), real retail sales (black), freight services index (brown), coincident index in Ch.2017$ (pink), and GDO (blue bars), all log normalized to 2021M11=0. Retail sales deflated by CPI. Source: Philadelphia Fed [1], Philadelphia Fed [2], Federal Reserve via FRED, BEA 2025Q4 advance release, and author’s calculations.

The pattern of output measures diverging from employment — also displayed in the set of indicators focused on by the NBER’s Business Cycle Dating Committee (BCDC) — is replicated here. Notable observations: (1) Civilian employment adjusted to NFP concept is now on a pretty clear downswing, now that the 2026 population controls are applied to January’s data; (2) inflation adjusted retail sales are down as well.

Nowcasts have been downshifted as well; GDPNow for Q1 dropped from 3.2% q/q AR yesterday to 2.1% today. NY Fed’s nowcast dropped from 2.4% last Friday to 2.2% today. Goldman Sachs tracking as of today stayed at 3.4%.

From the Hutchins Center’s latest fiscal impact update:

“We expect fiscal policy to add 2 percentage points to GDP growth in the first quarter of 2026. This reflects the reversal of the temporary effects of the government shutdown, which we assume will boost real GDP in the quarter by 1.3 percentage points, as well as the stimulative effects of the OBBBA on both purchases and taxes.”

Not sure how some of these forecasts accommodate the Q1 rebound from the Q4 shutdown, but:

GDPNow + Hutchins = Goldman (almost)

GDPNow + Hutchins was a pretty good forecast for Q4 GDP

Oh, and when it comes to war’s impact on Q1, take wha tever mechanical GDP forecast makes you comfortable and then cogitate over war’s effect on inventories and trade. We produce oil and gas, so may enjoy a bump in exports. Typically, inventories and trade tend to offset each other, but we’re burning through munitions inventories by “exports” to Iran that aren’t reflected in the GDP stats. That’s war-related trade as an add to GDP, war-related inventories as a drag. Get the magnitudes right and you capture war’s impact on Q1 GDP.

Q: “It sounds like the Russians are helping Iran target and attack Americans–”

Trump: ” That’s an easy problem compared to what we’re doing here. What a stupid question that is to be asking at this time.”

Trump is rattled by the suggestion that his good buddy Putin is helping Iran kill Americans. What happened to putting America first? Why isn’t every journalist asking Trump this same question every single day?

And don’t forget that Trump removed the sanctions on Russian oil yesterday in his panic about gas prices.

If I recall correctly, the US has been providing Ukraine lots of help with targets inside Russia, so from their point of view, turnabout is fair play.

(With condolences to the families of ordinary US military personnel and civilians killed as a result)

Also, adding fuel to the fire w/r/t this spilling over into a wider regional war.

Off topic – This is in response to an earlier post on the closing of Hormuz to shipping:

https://econbrowser.com/archives/2026/03/closing-the-strait-of-hormuz

There’s a YouTube channel by the name of “What’s going on with shipping” (@wgowshipping), run by a shipping specialist. In a video entitled “Strait of Hormuz and Persian Gulf Update” he predicts that shopping through the Strait will resume in about a week. I won’t link, but it’s easy to find.

His claim is that insurance is the reason ships have stopped transiting the Strait. Shipping insurance is structured so that as risks rise, insurers must increase capital in order to offer coverage; increased insurance rates are not enough. You can see the logic: higher rates bring in money over time, but in the short term, cannot provide sufficient coverage for a sharp increase in likely payouts. Only increasing the capital base can do that.

Raising capital can be done, but not instantaneously. Meetings are held, votes taken, prospectuses written – the usual stuff.

So that’s the story – gotta raise enough capital to cover the risk of operating in a war zone. That risk includes not just the potential for losing vessels and cargos, but also the liability for damage to third parties. It takes time.

In the event of a sinking, the oil oligarchs get their money back but the crew don’t get their lives back.

What a disgusting, shameful business.

that covers insurance. but a captain and crew will need higher compensation as well. not sure I would take on a job that I know has a high probability of death. you may be able to force some of the crew into action, but I would guess many sea captains will say no thank you. unless you pay them enough. so trade costs grow even more.

Funding insurance is different matter than exposing your valuable asset and it’s loaded cargo to high probability of loss.

Losing the ship represents years of lost revenues, to say nothing of harm to your crew. Unless there are a lot of super tankers up for sale.

Btw, remove utilities from industrial production, and August and September were the peak:

https://fred.stlouisfed.org/graph/fredgraph.png?g=1T8Gn&height=490

In other words, with the exception of AI data center related spending, the US economy has probably been in a shallow recession since the start of the government shutdown last autumn.

and a second partial shutdown does not help matters at all.