Up for geopolitical risk, not for financial.

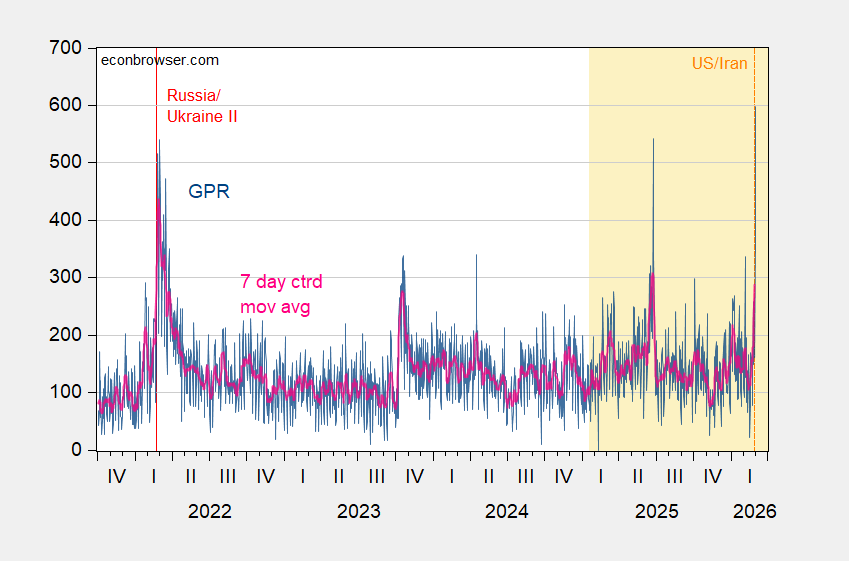

Figure 1: Geopolitical Risk (GPR) index (blue), 7 day centered moving average (red). Source: Caldara et al.

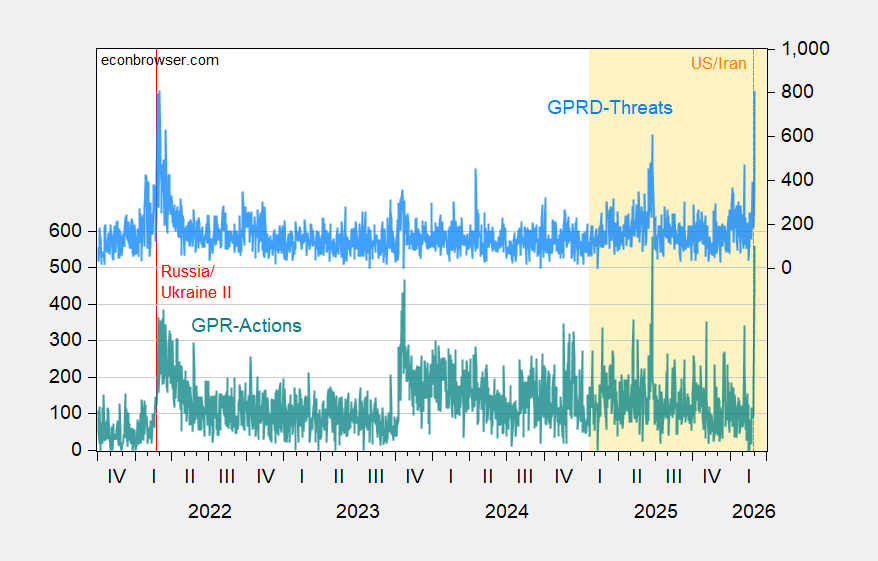

Here are the subcomponents of GPR, GPRD-Action, GPRD-Threats.

Figure 2: Geopolitical Risk Action index (teal), GPR Threats (sky blue). Source: Caldara et al.

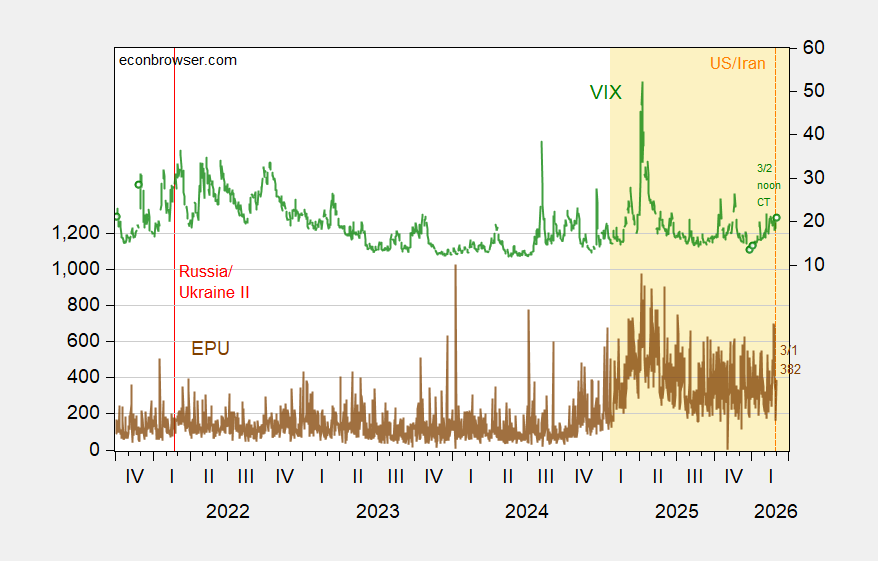

Economic policy uncertainty and financial risk are not similarly elevated, thus far (through 3/1 for EPU, through 3/2 noon CT for VIX).

Figure 3: EPU (brown, left scale), VIX (green, right scale). Source: policyuncertainty.com, CBOE via FRED.

That being said, elevated GPR and EPU both rose with slowing economic activity, as illustrated in this post.

Interesting – Today, the Institute for Supply Management reported that Manufacturing PMI: 52.4 (second month of expansion) and Prices Paid: 70.5 (highest since 2022 inflation peak). Typically a Prices Paid reading above 70 historically signals rapid cost acceleration at the factory gate. During the 2021–2022 inflation surge, ISM Prices Paid led CPI by ~2–4 months. It tends to lead PPI first, then core goods CPI. There is pressure building in the pipeline. importantly, the survey responses were collected before the airstrikes and oil spike.

Nice.

One related issue not much discussed in the U.S. financial press so far is the differential effect of the closing of Hormuz on the rest of the world vs the U.S. We have our own oil and natural gas. Europe and Asia depend on shipments out of the Straits. If supplies become 1978-style tight, it will be the rest of the world that suffers from outright supply interruptions. We will have higher prices, but the risk of physical shortage is low. One lesson of the embargo period is that physical shortage is more economically damaging than mere price increases. Turns out, rationing through the price mechniam is more economically efficient than other forms of rationing.

Anyhow, a slowing in the rest of the world is likely to mean reduced demand for U.S. exports. Because weakness overseas would be the result of a supply shock, imports to the U.S. are likely to be more expensive. The non-energy trade balance is likely to swing toward deficit as the result if any oil-supply disruption through the Strait.

It would be great if a world-class energy economist would jump in here and tell us what’s what.