A slight recasting of outlook:

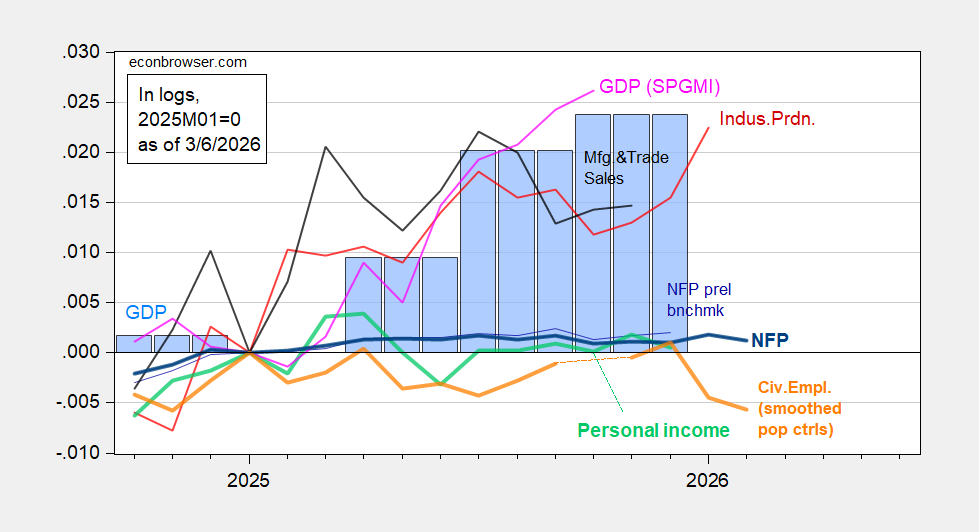

Figure 1: Implied NFP preliminary benchmark revision (thin blue), post-benchmark NFP (bold blue), civilian employment with smoothed population controls (bold orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), and monthly GDP in Ch.2017$ (pink),GDP (blue bars), all log normalized to 2025M01=0. Source: BLS via FRED, BLS, Federal Reserve, BEA 2025Q4 advance release,S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (1/21/2026 release), and author’s calculations.

A week or two ago the issue came up of whether Prof. Leamer’s paper, “Housing IS the Business Cycle,” was obsolete.

Well, here was how he concluded that paper:

“In the years before recessions … consumers contribute a total of 65% of the leading weakness. In contrast, business spending contributes only 10%…. The temporal ordering of the spending weakness is: residential investment, consumer durables, consumer nondurables, consumer services….”

So I subsequently took a look. And the result was that all of the dominos in the above conclusion have toppled over except for the last one. Obviously we are well beyond the average of 7 Quarters he postulated as the average lag between housing declining and recession, but here we are (and this morning’s jobs report certainly didn’t help.

Leamer’s finding that consumers drive recessions is supporred by Mian, Sufi and Werner. The old notion that mistakes in business investment end expansions is mostly outdated. Consumers turn business investment decisions into mistakes. Could be the Y2K computer cycle is an exception.

On a related topic – China has announced a growth target for the coming year of 4.5% to 5.0%, compared to a reported growth rate of 5.0% over the past year. Pretty much as expected:

https://apnews.com/article/china-congress-economy-gdp-trump-target-1822006cd39ff43505fa9a47a4581a16

There are incremental adjustments to economic policy, rather than big new initiatives.

Meanwhile, press reports indicate renewed price competition among firms in sectors with excess capacity – deflationary behavior that China’s government has tried to prevent. I don’t have a grip on the cost to China of the closure of Hormuz, but if input costs are rising while producers engage in price competition, that’ll reduce profits – bad for loan quality.

Doesn’t look like any of China’s fundamental economic problems are being resolved.

Let’s step back from monthly wobbles and strikes and model adjustments. Here’s a look at the y/y change in payroll employment over time:

https://fred.stlouisfed.org/graph/?g=1T65D

The current 156,000 y/y gain is not merely consistent with recession; it’s consistent with late recession or early post-recession readings from earlier cycles.

Same story for aggregate weekly hours:

https://fred.stlouisfed.org/graph/?g=1T67j

And yet, real GDP keeps climbing. Not sure how that works…

“But if it can’t go on forever it will stop.” H. Stein

Looking at where Total NonFarm employment was at the beginning of numerous past recessions suggests that the US entered recession in mid-2025. But we didn’t notice because the stock market level still showed excitement about AI. The aggregate weekly hours chart indicates many people in 2025 were ’employed’, but weren’t getting the hours they were accustomed to. Lower paycheck, continuing inflation – slammed on both sides. The ‘affordability’ became a common word.