Nowcasts are typically below pre-war forecasts.

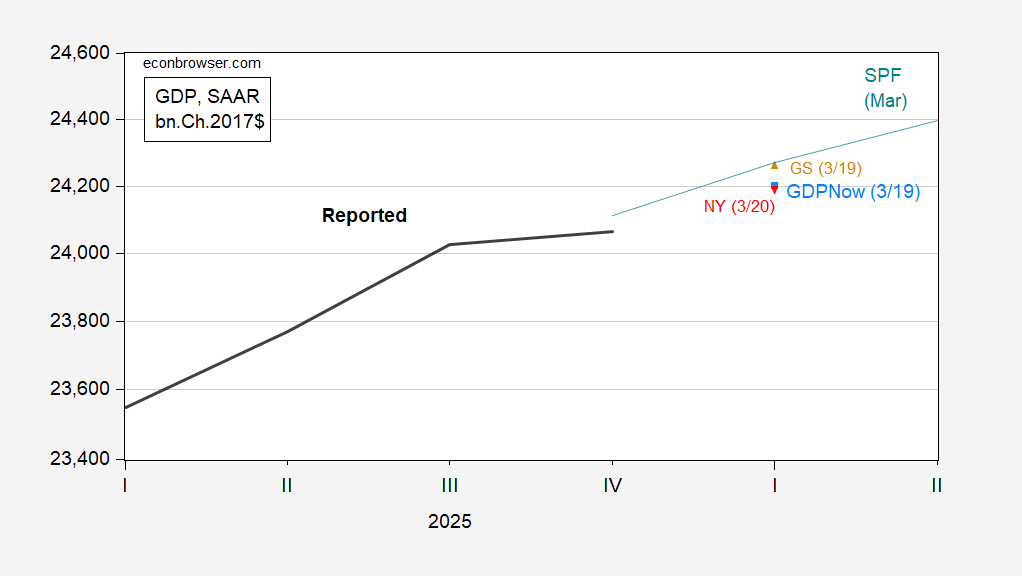

Figure 1: GDP as reported (bold black), March SPF (teal), Goldman Sachs tracking (light brown triangle), GDPNow (sky blue square), NY Fed nowcast (inverted red triangle), all in bn.Ch.2017$ SAAR, all on log scale. Source: BEA 2025Q4 2nd release, Philadelphia Fed, Goldman Sachs, Atlanta Fed, NY Fed, and author’s calculations.

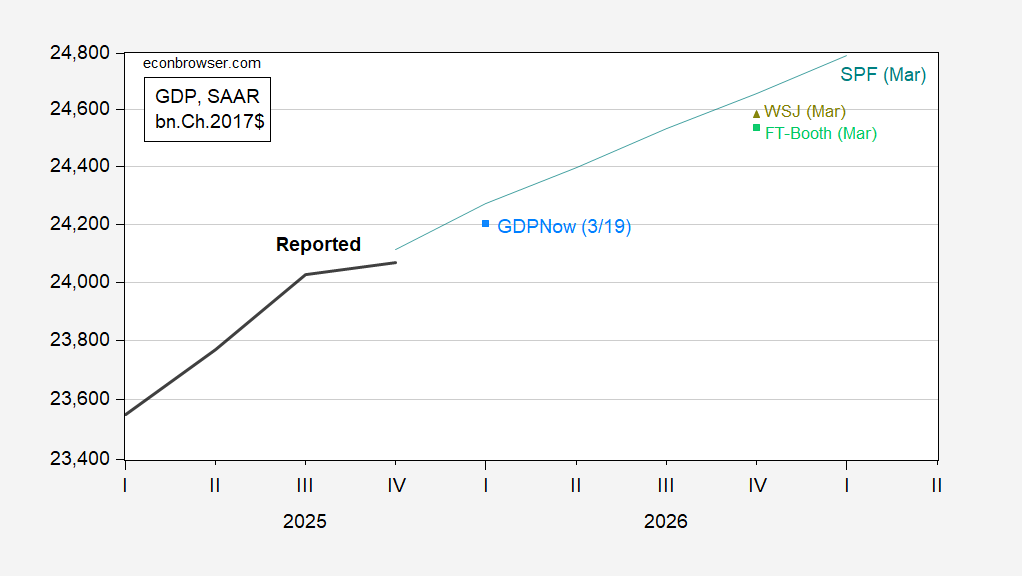

Most of the responses to the March Survey of Professional Forecasters were submitted before the beginning of the US-Israel-Iran war, so can be considered to some degree a pre-war outlook. The WSJ and FT-Booth forecasts for Q4 can be considered then downward revisions to the pre-war outlook.

Figure 2: GDP as reported (bold black), March SPF (teal), GDPNow (sky blue square), March WSJ survey mean (chartreuse triangle), FT-Booth March survey median (light green square), all in bn.Ch.2017$ SAAR, all on log scale. Source: BEA 2025Q4 2nd release, Philadelphia Fed, WSJ, FT-Booth Survey of Macroeconomists, and author’s calculations.

I’ll note that the WSJ survey mean, taken a week ago or so, so incorporating knowledge of the war’s onset, does not indicate recession. Indeed, no respondent indicates negative Q4/Q4 growth for 2026.

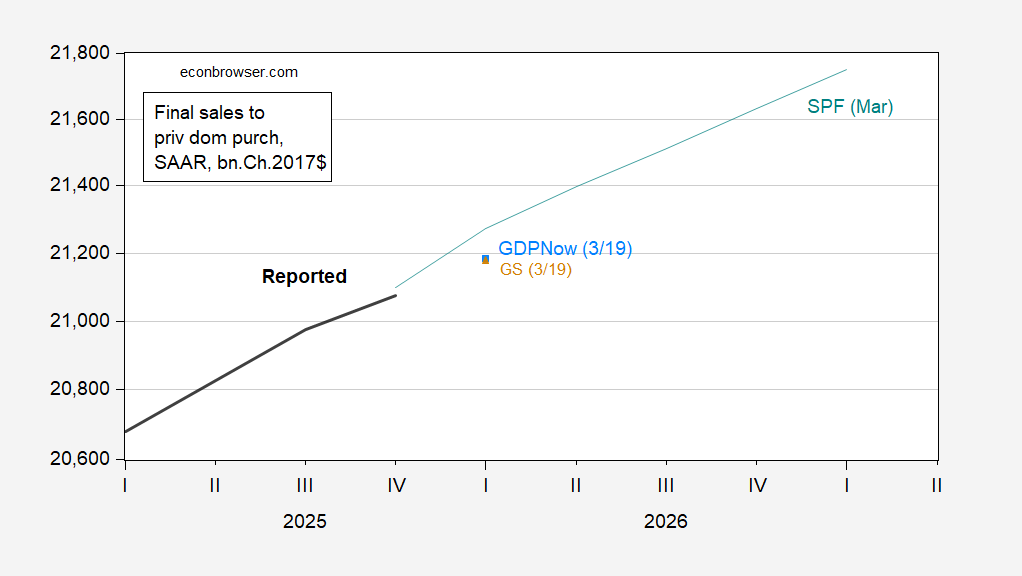

That being said, there is a certain softness indicated by nowcasts of final sales to private domestic purchasers (aka “core GDP”).

Figure 3: Final sales to private domestic purchasers as reported (bold black), March SPF (teal), GDPNow (sky blue square), GS (light brown triangle), all in bn.Ch.2017$ SAAR, all on log scale. Source: BEA 2025Q4 2nd release, Philadelphia Fed, WSJ, FT-Booth Survey of Macroeconomists, and author’s calculations.

We are less reliant on oil, and fairly immune to a physical shortage of oil now, so the Arab oil embargo of 1973 is an unreliable analog for the U.S. today. That said, back then the economic effects came quickly.

Real GDP at the time of the October 1973 oil embargo.:

https://fred.stlouisfed.org/graph/?g=1TUge

Payroll employment at the time of the October 1973 oil embargo:

https://fred.stlouisfed.org/graph/?g=1TUgz

NBER called the beginning of the recession in December of 1973, within two months of the embargo.

The 1973 embargo is probably a better analogy for countries which today are reliant on energy from the Persian Gulf. They face actual physical shortages of oil and gas.

Speaking of forecasts, the yield curve is doing something interesting right now. The 10year/3month spread has increased, while the 10year/2year speead has declined – big action in the 2year/3month spread. That’s due to changing expectations for policy rates, of course, as well as to a related change in inflation expectations.

It comes doen to not much chance of a rate hike in the next 3 months, but a substantially reduced possibility of a rate cut over 2 years, and a rise in the odds of a rate hike.

No inversion yet.

The yield curve isn’t just doing something “interesting,” as far as I have been able to tell, it is doing something *unprecedented* — it has un-inverted (normalized) by short to medium term yields *rising.* I have taken the data back 60 years, and as far as I have been able to tell, this has never happened before.

Old-school forecasting systems that predated the Fed manipulating the Fed funds rate would treat this as a negative for the economy, because the average “cost of renting money” has risen.

Knew this was coming:

‘Iran is planning to enshrine a “new status” for the Strait of Hormuz to require every passing ship to pay fees to Tehran for the privilege, Expediency Council member Mohammad Mokhber, an adviser to the supreme leader on economic affairs, told the country’s Mehr news agency.’

https://www.wsj.com/world/middle-east/iran-war-negotiations-demands-85555522?st=YhBEZw&reflink=article_copyURL_share

Mokhber reads Econbrowser comments?:

Macroduck

March 17, 2026 at 6:15 pm

Iran is going to need money for reconstruction. The world wants oil, gas, urea, aluminum… from the Gulf. Hows ’bout Iran collects tolls for passage through the Strait?

Iran could confer privileges on friendly countries, embargo unfriendly ones, just like the U.S. does.

https://econbrowser.com/archives/2026/03/deployment-of-arg-tripoli-betting-on-hormuz-re-opening#comment-322492

The Fed is not the only central bank reassessed its rate path in reaction to the war:

https://www.cnbc.com/2026/03/19/interest-rates-bonds-bank-of-england-european-central-bank-investors-iran-war-ecb-inflation.html

The hyperbole from trading desks might need a grain of salt, but the facts are pretty clear. So is the conclusion that keeping borrowing costs down requires a quick end to the war. What are the odds?

“We are getting very close to meeting our objectives as we consider winding down our great Military efforts in the Middle East with respect to the Terrorist Regime of Iran,” Trump wrote on Truth Social.

At the same time:

“The Pentagon is sending three California-based warships and roughly 2,500 Marines to the Middle East, the second significant deployment in a week, the Associated Press and other outlets reported Friday”

https://www.latimes.com/politics/story/2026-03-20/iran-war-oil-prices

There is internet chit-chat about “pack up, we’re going tomorrow” orders for stateside Marines to deploy overseas; doesn’t sound well planned.

Maybe this is just the fog of war. Maybe we’re keeping our options open. Maybe we don’t know what we’re doing.