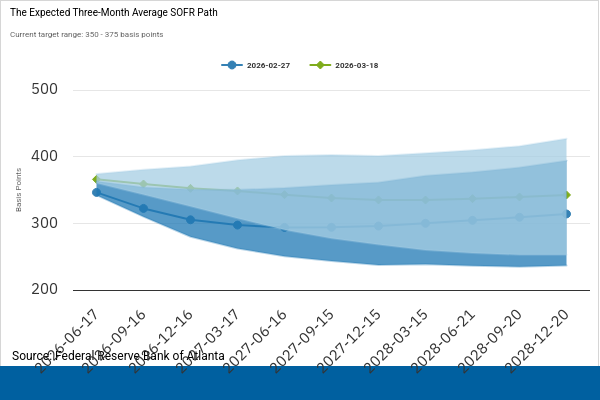

Professional market chatterers are noting the increased priced-in odds of a rate hike as the next Fed pokicy move. Mostly, they add “I personally doubt it”, but that’s pretty much to say “I agree with something near the median estimate”.

Perhaps worth mentioning is that when the Fed reacts to deteriorating conditions, either recession or inflation, the median funds rate estimate from a few months previous is nearly always wrong. The move from the notion that we are in equilibrium to out of equilibrium may take time to develop, but once it develops, the policy outlook changes fast.

Macroduck

Do I remember correctly that the world once had a deal with Iran to allow Iran to export oil as long as they laid off the nuke thing? What ever happened to that?

Another example of the felon-in-chief saying he’s going to fix something a little bit that he broke a lot.

Macroduck

One reason to think Fed easing is unlikey in the near term is the rise in the expected rate of inflation over the next 5 years. The current 5-year TIPS breakeven is 2.6%:

In other words, the priced-in average rate of inflation over the next 5 years is 2.6%, up from 2.3% at the end of 2025. Five years is probably beyond “transitory”. Inflation is above target, expected inflation is above target and rising, trade and immigration and war policy are all inflationary. Conventional Taylor rule settings show policy is already neutral, so there is no strong argument for easing.

Easing now could help to entrench inflationary expectations, if you believe in that sort of thing.

Professional market chatterers are noting the increased priced-in odds of a rate hike as the next Fed pokicy move. Mostly, they add “I personally doubt it”, but that’s pretty much to say “I agree with something near the median estimate”.

Perhaps worth mentioning is that when the Fed reacts to deteriorating conditions, either recession or inflation, the median funds rate estimate from a few months previous is nearly always wrong. The move from the notion that we are in equilibrium to out of equilibrium may take time to develop, but once it develops, the policy outlook changes fast.

Do I remember correctly that the world once had a deal with Iran to allow Iran to export oil as long as they laid off the nuke thing? What ever happened to that?

https://thehill.com/homenews/administration/5791639-bessent-oil-sanctions-lift-iran-conflict/

Another example of the felon-in-chief saying he’s going to fix something a little bit that he broke a lot.

One reason to think Fed easing is unlikey in the near term is the rise in the expected rate of inflation over the next 5 years. The current 5-year TIPS breakeven is 2.6%:

https://fred.stlouisfed.org/graph/?g=1TRiJ

In other words, the priced-in average rate of inflation over the next 5 years is 2.6%, up from 2.3% at the end of 2025. Five years is probably beyond “transitory”. Inflation is above target, expected inflation is above target and rising, trade and immigration and war policy are all inflationary. Conventional Taylor rule settings show policy is already neutral, so there is no strong argument for easing.

Easing now could help to entrench inflationary expectations, if you believe in that sort of thing.