CEA Chair (Acting) Pierre Yared (NYT):

… consumer prices would “go back down” once the war ended. That, he added, would relax pressure on families, who would see wages continue to grow “following the tailwinds of the economy.”

“Consumers are continuing to spend, and they do seem to be looking through the shock,” Mr. Yared said. “It looks to us like consumers understand the situation is temporary.”

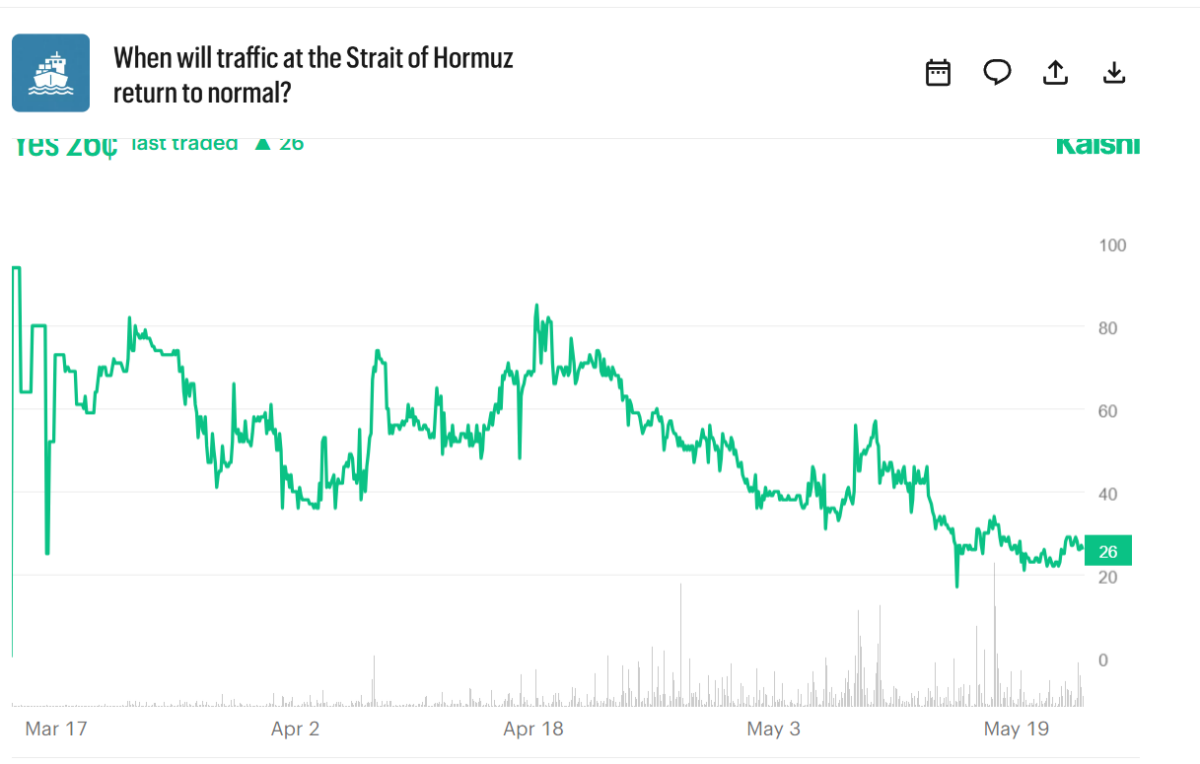

Well, if we define when “the war ended” as when the Strait of Hormuz is re-opened, then it might be a while.

Source: Kalshi.com, accessed 5/19/2026 4pm CT.

Odds for a reopening by September 1st is a coin-flip.

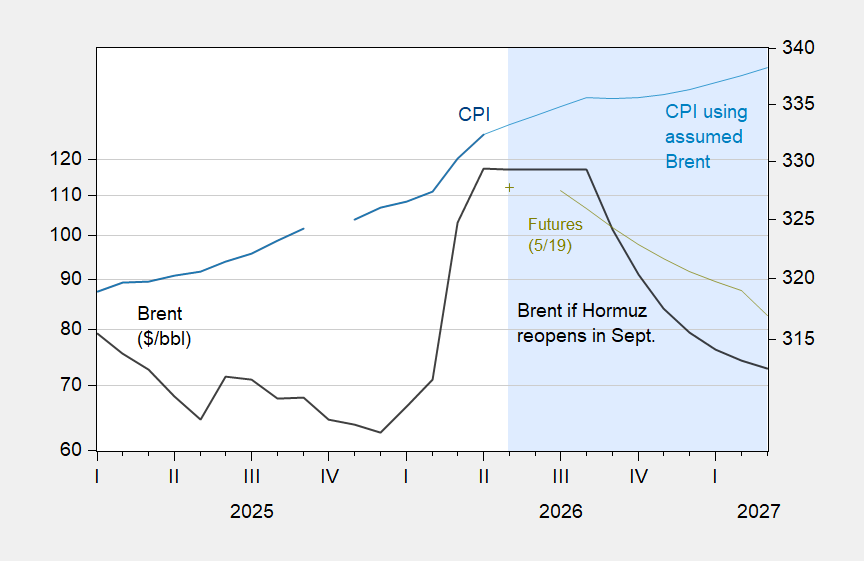

But suppose we did see a clear war’s end. Suppose further prices would revert within a year to the pre-War Brent price of $70, with 70% of gap between April price ($117) and $70 eliminated within 3 months (this is proportional to the estimated flow resumption, as reported by Goldman Sachs). Then we would see the following evolution of headline CPI.

Figure 1: Oil price – Brent (black, left hand side), Brent futures as of 5/19 6pm ET (chartreuse); and CPI (blue), and simulated CPI (light blue). Oil price for May through March 2027 are scenario projection assuming constant April price through August, and reopening in September; price gap decays 70% per quarter. Projection period shaded light blue. Source: EIA, BLS via FRED, NYMEX via barchart, and author’s calculations.

The CPI projection uses log CPI on log core CPI and log oil price, 2022M01-2026M04 sample. Core CPI assumed to increase at 2025M05-26M04 rate.

Under these assumptions, the CPI level barely budges downward. The rate of inflation clearly drops, but disinflation is clearly different than deflation.

Of course, should the oil price drop faster than projected, one could get a short term decrease in the price level. However, this runs counter to the view that even when the Strait reopens, flow will remain below 100% of pre-War level given the destruction of facilities.

Okay, the corruption just gets better. You’ve all heard about the settlement over Trump’s $10 Billion lawsuit that gives him a $1.8 Billion slush fund to reward is political allies. But now it turns out there was another part of the settlement that FOREVER BARS AND PRECLUDES the IRS from examining or prosecuting Trump, his family members and any of their companies for past tax violations.

This is a settlement forged by acting Attorney General Todd Blanche, Trumps personal attorney that defended Trump in his felony conviction in New York for tax violations. Blanche couldn’t win at trial in court but he can as Attorney General by simply banning any future trials.

The Trump administration has gone all in on blatant corruption, pulling out all the stops. It’s the YOLO strategy.

So, among the early “Oh, yeah, we depend on the Persian Gulf for that, too” headlines was that Qatar’s LNG industry is also a source of helium, so helium would be in short supply. Y’all knew that; the U.S. will have birthday ballons and squeaky voices, but the rest of the world will do without. And also, microchips. Yes? We talked about this.

Well, Forbes says the microchip helium problem starts to bite in June:

https://www.forbes.com/sites/guneyyildiz/2026/05/18/the-chip-shortage-is-a-gulf-energy-crisis-wearing-a-different-costume/

However, chip fabrication requires a STEADY flow of electricity, and that is already a problem in Taiwan and South Korea because of fuel shortages. Beyond that, Forbes outlines a two-year supply chain problem in chip fabrication as a result of the Iran war.

I don’t know enough about the AI data-center build-out to know how big a deal this is. I just know the big-4 AI firms’ spending war is driving a major chunk of U.S. growth.

There is a great deal going on in international financial flows. Less oil trade means fewer dollar payments. Also, fewer petrodollars. Less oil means more inflation, higher interest rates and more sovereign risk, none of which is equally shared among currencies. There’s a big (often ill-informed) debate underway about the dollar’s role in global finance.

It would be great if we could rely on the pool press to keep us informed about these issues.

Here’s a standard press report covering the latest batch of TICS data, and reaching the conclusion that China has been steadily shedding U.S. Treasury debt, and did so again in April:

https://www.cnbc.com/2026/05/19/central-banks-offload-us-treasuries-china-holdings-at-18-year-low.html

Here’s Brad Setser at the Council on Foreign Relations, perhaps the foremost China-Treasury-holdings watcher, saying that China’s holdings are too opaque to allow the use of TICS data to draw any such conclusion:

https://www.cfr.org/articles/finding-china-and-the-u-s-tic-data

Setser has been doing this for a long time and is very widely quoted. CNBC is apparently ignorant of that fact, and they aren’t the only ones. When the press can’t be bothered to understand its subject material or to gather expert analysis, we needn’t bother with the press.

Amen

But in an era of clickbait headlines and eviscerated newsrooms, is this any surprise?

“Abandoning the dollar” would be extremely costly for China because of its effects on their own currency. Abandoning their holdings of dollars in places that could b e targeted by US and European sanctions would make a lot of sense – given what happened to Russia.

I completely agree that journalists should consult with actual subject experts before they write anything. The problem is that when there is a conflicts between writing for profit (shock effects) and writing for truth, corporate media will sell out truth. It’s eventually going to kill Wall Street predatory corporation news. The will all go full Faux and just sell people the news they want to hear.

CNBC has been a crank outlet for years now. ever since the santelli meltdown during the financial crisis.

if you want to get real unbiased business news, my suggestion is Bloomberg, and their radio show is top notch in the morning. they are interested in learning things on that show.