That’s the title of a paper by Yanshuo Chen, (PhD, UCSC):

This paper shows that the dot-com crash contributed to the early-2000s housing boom through a household portfolio reallocation channel. Areas more exposed to declines in stock market participation experienced significantly stronger house price growth, as households shifted investment from equities toward housing. Identification relies on a shift–share design exploiting predetermined cross-state variation in stock market participation. I document that this reallocation operated through changes in the marginal investor, including increased investor activity and disproportionate inflows of young households. A stylized heterogeneous agent framework rationalizes these findings through competing wealth and flow-of-funds effects, with the latter dominating in the data and generating persistent price dynamics through extrapolative learning. These findings highlight a general mechanism through which financial shocks propagate across asset markets via household portfolio adjustment, suggesting that one crisis can sow the seeds of another.

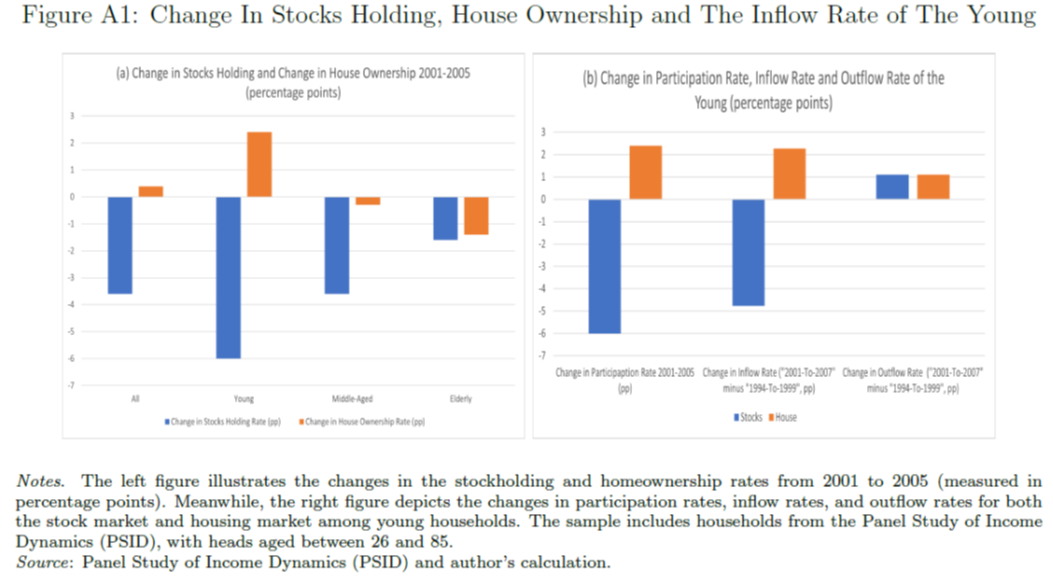

Some casual visual inspection of the changes in investment is useful.

Source: Yanshuo Chen (2026).

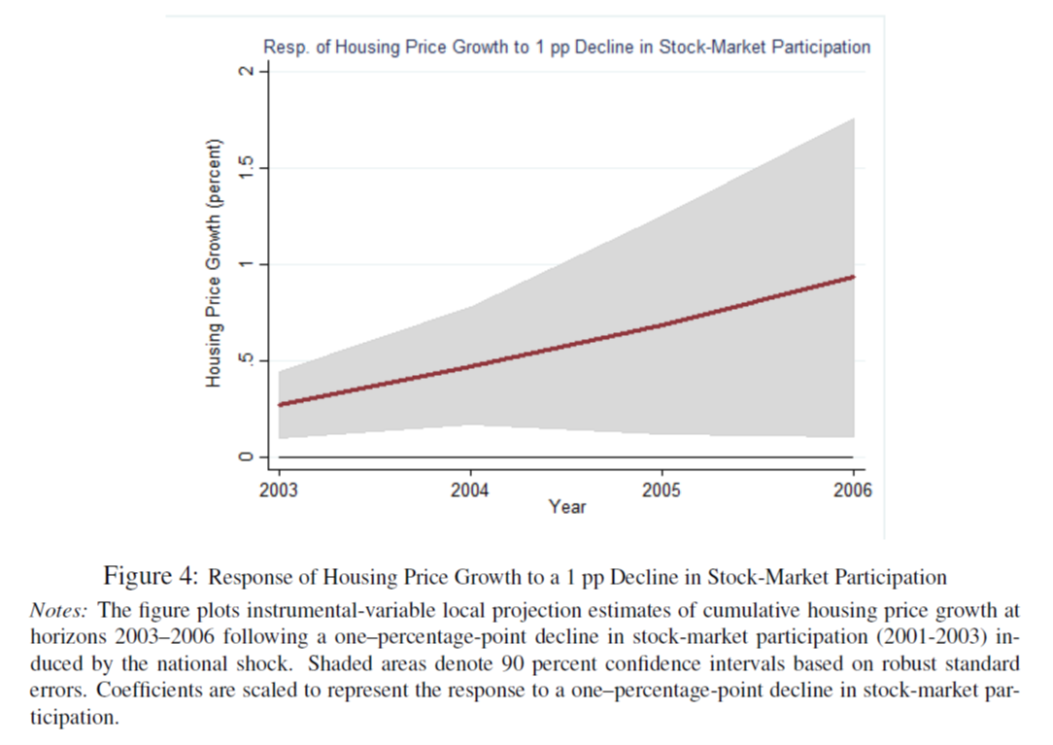

However, in order to infer a causal effect, one has to resort to econometrics. The key graph if Figure 4:

Source: Yanshuo Chen (2026).

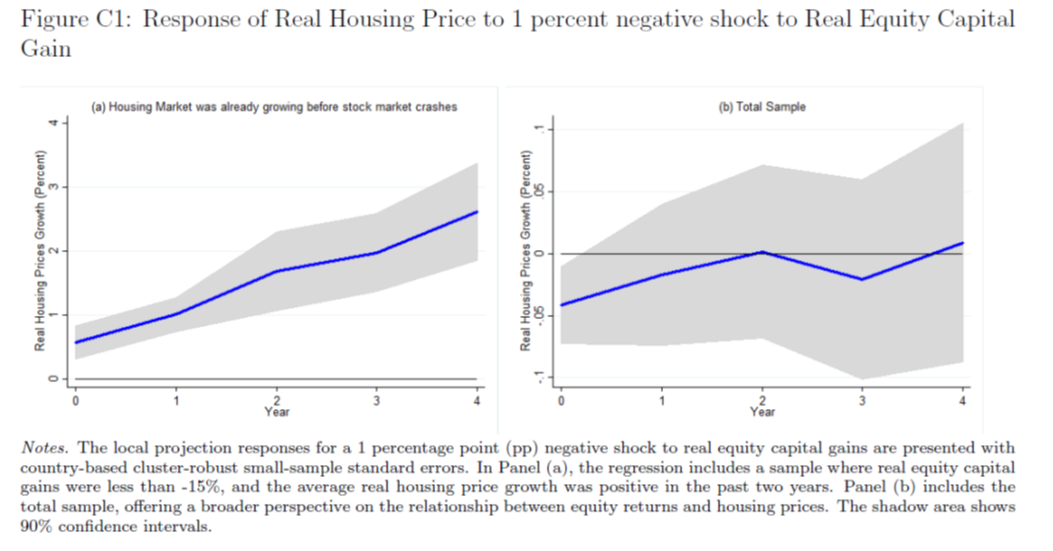

Chen also includes some cross-country results (40 advanced and emerging countries) demonstrating that this effect is not specific to the US. From Appendix C.

Source: Yanshuo Chen (2026).

From the conclusion:

While the analysis focuses on a single episode, the mechanism is not episode-specific and applies more broadly to environments with large financial shocks. For example, during the COVID-19 period, increases in household savings were associated with simultaneous increases in both equity and housing prices. Although this reflects a reallocation between consumption and saving rather than across asset classes, it highlights the broader role of household balance sheet adjustments in shaping asset price dynamics.

The paper thus has important policy impliations, particularly with respect to how different kinds of financial shocks can affect the housing market’s stability, affordability, and spillover effects to the rest of the macro-financial system.

Link to the paper.