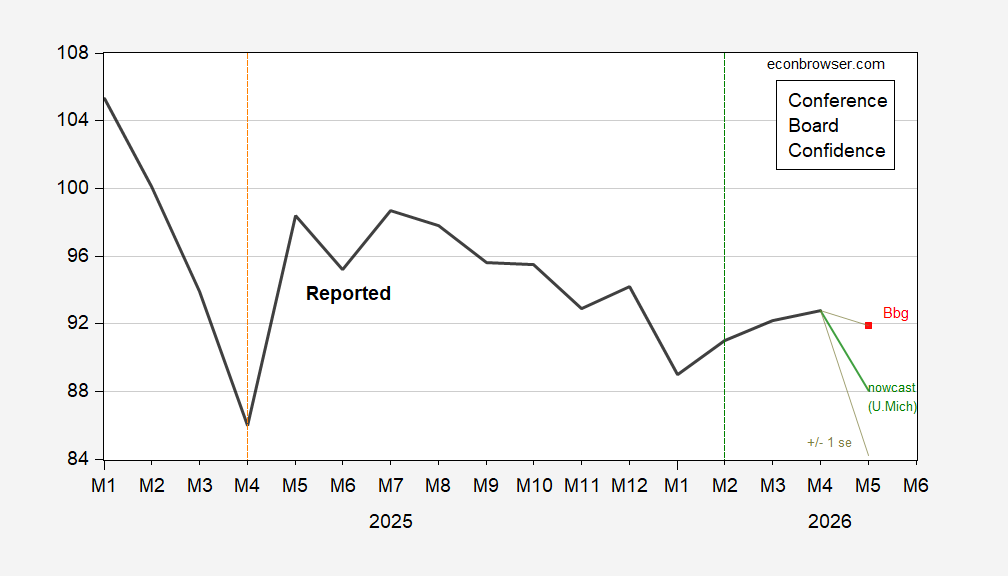

Deterioration, but not as much as implied by U.Michigan. May number out tomorrow.

Figure 1: Confidence Index (bold black), Bloomberg consensus (red square), predicted based on U.Michigan Sentiment, 25M01-26M04 (green), +/- 1 std error band (chartreuse lines). Orange dashed line at “Liberation Day”, green dashed line at US-Israel-Iran war. Source: Conference Board, Bloomberg, and author’s calculations.

The equation used to predict Conference Board Confidence has an adjusted R2 of 0.48, SER of 3.22.

The U Michigan survey was conducted before the U.S. and Iran arrived at agreement on 95% of the issues which led to the war…and which have never been clearly laid out. The Conference Board survey was conducted before new shooting happened today:

https://www.npr.org/2026/05/25/nx-s1-5833690/u-s-iran-negotiations-updates

Oil prices are up today, though still lower than before the war-criminal-in-chief claimed that Iran had agreed to a lot of things Iran has since said it hasn’t agreed to.

I kinda think the oil market isn’t actually trading on the state of the negotiations; how could it be? Seems more like it’s trading on an impression of how desperate the war criminal is to end the war and get oil prices down. His effort to gin up tough-sounding “leaked” responses to the howl from Bibi and Loomer and Cruz and AIPAC sounds like he’s truly desperate for a deal. So oil prices fell.

Iran smells the war criminal’s fear. Playing a longer game, they’re digging their heels in. Oil prices rise in response.

And there’s the “he’ll bomb Iran after the hajj” story. The war criminal isn’t sophisticated enough to think of that. Is he cowed enough by Sunni leaders to take the hajj into account, while ignoring domestic voters’ anger ahead of the mid-term? Dunno. Sounds like something war mongers would say to help themselves sleep.

In his first term he was well know to adapt the opinion of the last guy who talked to him. Problem is there are a lot of people saying opposite things.

Off topic – UK economy:

https://archive.is/KolZz

The headline blatantly tortures both math and semantics; bank lending is NOT at the lowest level in 30 years. The point made in the article, that credit is drying up, is true. Bank lending AS A SHARE OF GDP has fallen sharply. Big firms, of course, have ready access to the bond market, so it’s small and medium firms under greatest pressure.

High borrowing rates probably account for some of the decline in borrowing – a credit demand issue. The effect is the same as reduced supply of credit – weak economic activity.

More about the dishonest FT headline on bank lending. In Q3 last year, U.S. bank lending was at its lowest point as a share of GDP in just over 20 years; real GDP grew at a 4.4% annual rate in that quarter. Banks are a smaller part of the overall supply of credit now than in the past. The headline writer at the FT seems not to know much about that.

But yes, the UK economy is in trouble.

From Bloomberg:

“Strategists Warn of High Yields Even If Iran War Ends”

https://ca.finance.yahoo.com/news/bond-strategists-warn-yields-to-stay-high-even-if-iran-war-ends-130000537.html

The central point is that inflation has not been the only driver of a rise in bond yields. Real, inflation-adjusted bond yields are also higher. Here’s the picture:

https://fred.stlouisfed.org/graph/?g=1WDhc

Since late 2002, real 10-year rates have been higher than at any time since before the housing crash. However, there is no upward trend in real rates since late 2022. What is trending higher recently is term premium:

https://fred.stlouisfed.org/graph/?g=1WDhC

There are a number of reasons this might be happening, including the Fed’s reduction in reserves, policy uncertainty at home and abroad, demographic shifts, credit demand… Worth noting is that the cost of funds and the inflation premium are typically more volatile than term premium. Based on what we can see in these data, the oil shock is the big new element in bond yields. The rise in real yields has been with us for a few years already. The FT is pearl clutching over real rates. That could change, of course. Bad policy certainly could drive up real yields.