Consider Germany over the last five years:

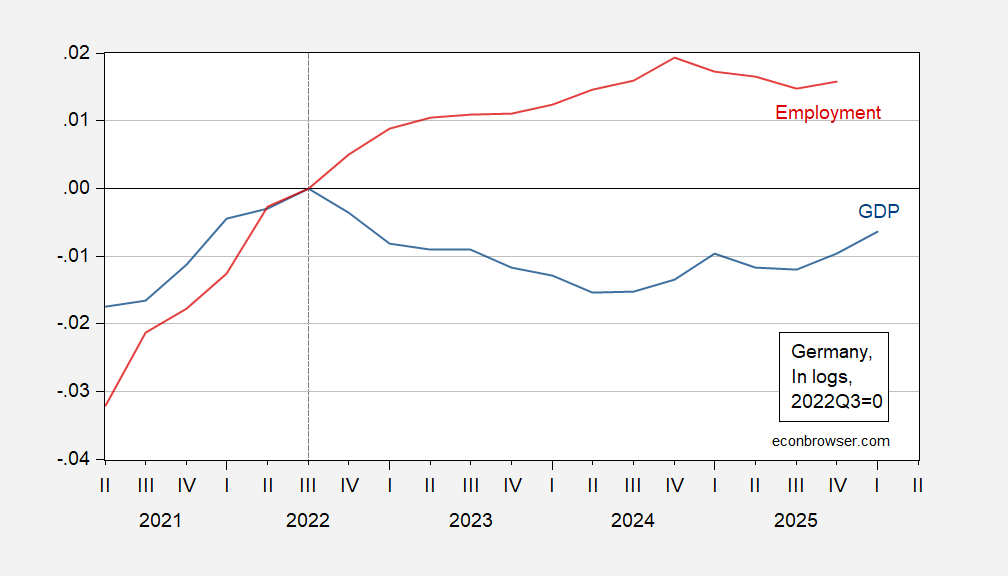

Figure 1: German GDP (blue), and employment (red), both in logs, 2022Q3=0. Source: OECD via FRED, and author’s calculations.

For the period that GDP was declining, employment was rising, up to 2024Q4. As a consequence, neither the German Council of Economic Experts, nor (private sector firm) ECRI or nonprofit Conference Board have declared a German recession.

Interestingly, there is no active prediction market on Kalshi for a German recession. That’s because the rules define two consecutive quarters of negative GDP growth as a recession, so the market is labeled as “determined”. (In contrast, for the US, Polymarket relies on either the 2 quarter rule or a NBER determination).

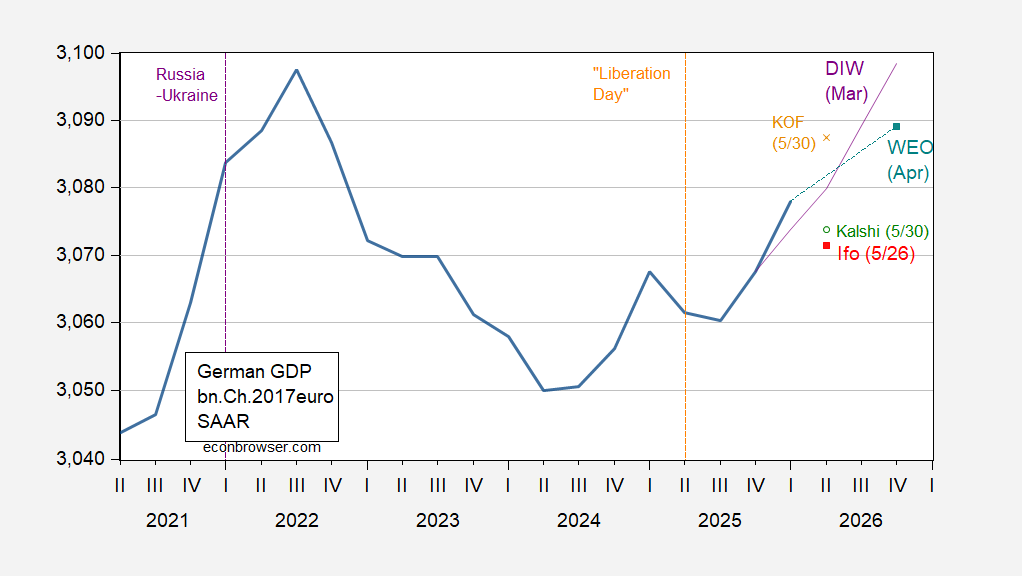

What’re prospects for Q2? Here’s a picture of GDP incorporating the latest Ifo forecast of 5/26, and the IMF’s WEO baseline projection of April.

Figure 2: German GDP (blue), Ifo nowcast of 5/26 (red square), KOF nowcast of 5/30 (tan x), Kalshi betting as of 5/30 (green circle), March DIW forecast (purple), and April WEO baseline (teal square), all in bn.Ch.2017Eur SAAR. Source: OECD via FRED, Ifo,KOF, Kalshi, DIW, IMF, and author’s calculations.

The Ifo number is of a bean counting exercise, as is the KOF (Konjunkturforschungsstelle/Swiss Economic Institute) Nowcasting Lab estimate. The Kalshi odds are a mix of differently conditioned bets, while the WEO projection and DIW (Deutsches Institut für Wirtschaftsforschung) forecast condition on very specific assumptions, especially regarding oil and natural gas prices. There is no particular reason the betting and the nowcasts should match, nor should the nowcasts match given the different methodologies.