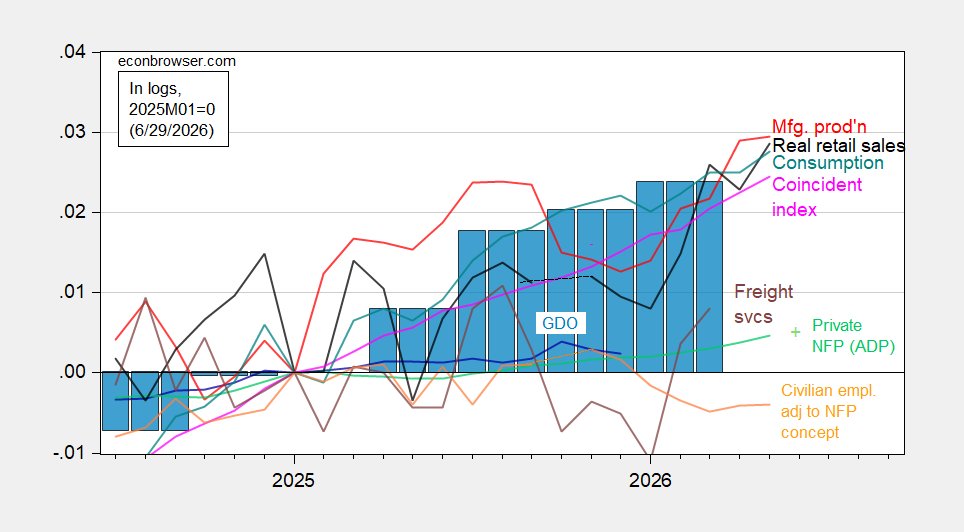

Coincident continues to rise through May, while Bloomberg consensus for NFP growth is for +114K, roughly same growth rate as in May:

Figure 1: Civilian employment adjusted to NFP concept smoothed population controls (bold orange), manufacturing production (red), ADP private nonfarm payroll employment (light green), Bloomberg consensus of 6/29 (light green +), real retail sales, CPI deflated (black), freight services indexes (brown), and coincident index in Ch.2017$ (pink), GDO (blue bars), all log normalized to 2025M01=0. Source: BLS, ADP via FRED, Philadelphia Fed, Bureau of Transportation Statistics, Federal Reserve via FRED, BEA 2026Q1 3rd release, and author’s calculations.

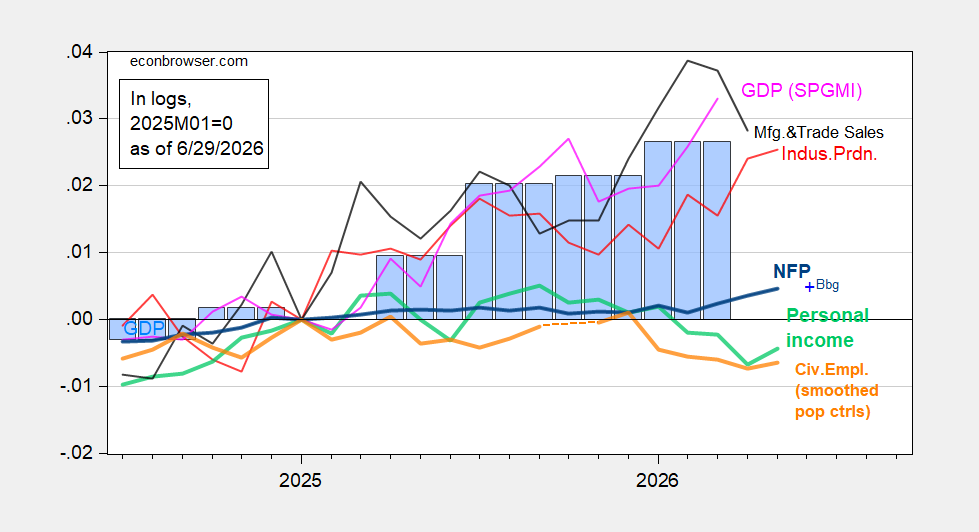

Compare against BCDC key indicators:

Figure 2: NFP employment (bold blue), Bloomberg consensus of 6/29 (blue +), civilian employment with smoothed population controls (bold orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold light green), manufacturing and trade sales in Ch.2017$ (black), and monthly GDP in Ch.2017$ (pink), GDP (blue bars), all log normalized to 2025M01=0. Source: BLS via FRED, BLS, Federal Reserve, BEA 2026Q1 3rd release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (5/7/2026 release), and author’s calculations.

The coincident index, which is scaled to grow at the pace of GDP over longer horizons, lags somewhat the expenditure side measure of GDP, both official and S&P’s Global Market Insight series. This makes some sense to the extent that the coincident index relies mostly on labor market information, which has been growing slowly relative to other real side indicators.